|

시장보고서

상품코드

2065527

미국 심혈관 및 연부조직 수복 패치 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Cardiovascular & Soft Tissue Repair Patch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

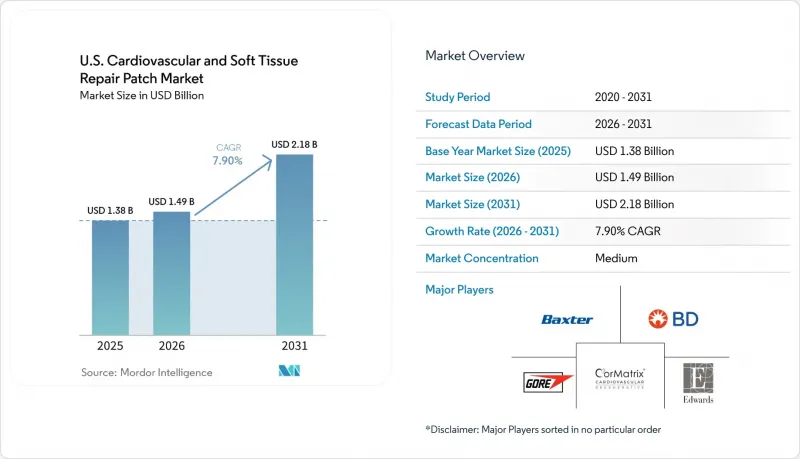

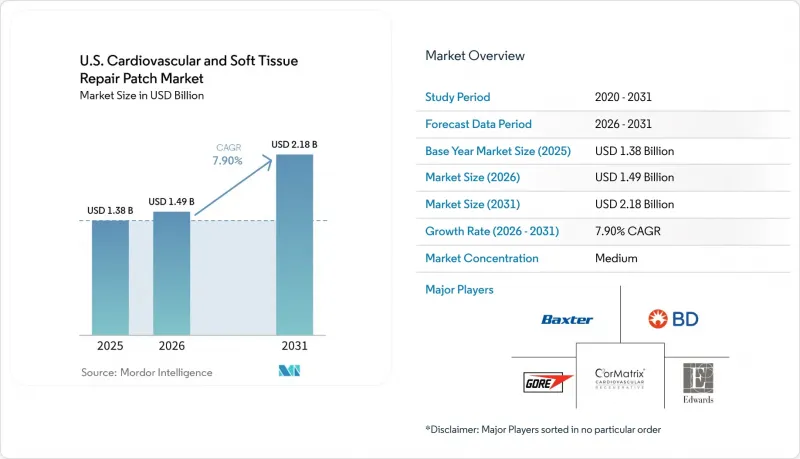

미국의 심혈관 및 연부조직 수복 패치 시장 규모는 2025년 13억 8,000만 달러로 평가되었고, 2026년에는 14억 9,000만 달러로 추정되고, 2031년까지 21억 8,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 7.90%로 성장할 전망입니다.

본 보고서는 소재별(합성, 생체 유래, 조직공학/복합), 용도별(심장 복원, 혈관 복원·재건, 심막 복원, 경막 복원, 연조직 복원) 및 최종 사용자별(병원, 외래수술센터(ASC), 전문 심혈관 센터, 전문 외과 센터)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 심혈관 및 연부조직 수복 패치 시장 동향과 인사이트

경동맥 내막 절제술 및 개복식 말초 혈관 재건술 시행 건수 증가

경동맥 내막 절제술은 동맥 절개 부위의 폐쇄가 여전히 이 수술에 필수적이기 때문에 패치에 대한 직접적인 수요를 지속적으로 견인하고 있습니다. 2017년 1월부터 2024년 9월까지 메디케어 수급자를 대상으로 한 39만 5,092건의 경동맥 혈관 재건술에 대한 2025년 분석에 따르면, 경동맥 내막 절제술이 전체 수술의 76.7%를 차지했으며, 경동맥 스텐트 삽입술은 23.3%를 차지했습니다. 스텐트 삽입술의 비율은 2017년 13%에서 2024년 38%로 증가했으나, 경동맥 내막 절제술이 여전히 주된 치료법으로 자리 잡고 있습니다. 경동맥 혈관 재건술의 총 건수는 2017년 6만 1,280건에서 2023년 4만 3,735건으로 감소했으나, 경동맥 내막 절제술 사례가 패치 수요를 지속적으로 지탱하고 있습니다. 또한, 대퇴동맥이나 장골동맥 우회술과 같은 개복 수술을 통한 말초 혈관 재건술 역시, 복잡한 증례에서 패치를 이용한 폐쇄술을 더욱 뒷받침하고 있습니다.

지속적인 선천성 심장병 치료의 부담

선천성 심장병의 교정 수술은 환자가 영아기부터 성인기에 이르기까지 여러 차례의 시술이 필요한 경우가 많기 때문에 장기적인 수요를 창출하고 있습니다. 미국심장협회(AHA)의 보고에 따르면, 북미의 출생 시 유병률은 1,000명당 12.3명이며, 2024년 미국의 환자 수는 46만 6,566명에 달했고, 이 중 60%가 20세 미만이었습니다. 미국 흉부외과학회(STS)의 2024년 데이터베이스 업데이트에서는 수술 건수 증가가 강조되었으며, 그중에서도 심방중격결손증 및 심실중격결손증에 대한 패치 봉합술이 가장 일반적인 것으로 나타났습니다. 지역별 비용 및 입원 기간의 차이에 영향을 받는 이러한 지속적인 수요는 공급업체에게 유연한 가격 책정과 다양한 제품 라인업의 중요성을 부각시키고 있습니다.

고가의 생체 유래 패치의 조달 비용과 보험 급여 격차

생체 유래 심혈관용 패치는 합성 대체품보다 높은 조달 비용으로 인해 도입에 어려움을 겪고 있습니다. 이러한 가격 격차는 가치 분석 심사를 복잡하게 만들고, 병원에서의 전환을 지연시키며, 미국 내 프리미엄 제품 시장 출시 주기를 길게 만들고 있습니다. 상환 제도는 여전히 제각각이며, 많은 생체 유래 패치의 경우 보험사와의 협상이나 의료기관의 승인이 필요하기 때문에 도입이 6-18개월 지연될 수 있습니다. 또한, 프리미엄 제품이 조달에 대한 거부감이나 예산 심사에 직면할 경우, 공급업체들은 수익 측면에서 압박을 받고 있다고 보고하고 있습니다.

부문별 분석

2025년, 미국의 심혈관 및 연조직 복원용 패치 시장에서 합성 패치는 매출 점유율의 54.20%를 차지했습니다. 이러한 우위는 ePTFE, 폴리에스터, 폴리프로필렌과 같은 소재의 비용 효율성, 치수 일관성, 그리고 임상 현장에서의 친숙함에 기반을 두고 있습니다. ePTFE는 그 신뢰성과 시술에 대한 숙련도 덕분에, 경동맥 및 말초동맥의 개창부 폐쇄에 있어 여전히 필수적인 소재로 자리 잡고 있습니다. 또한, 합성 제품은 조달 과정이 간소화되어 있다는 장점도 있어, 가격과 성능의 균형을 예측하기 쉬워졌습니다.

생체 유래 패치는 오염된 부위, 감염 위험이 높은 부위의 복원, 그리고 더 우수한 조직 통합이 요구되는 증례에서의 사용을 배경으로, 2026-2031년 연평균 성장률(CAGR) 8.52%를 나타낼 것으로 예측됩니다. 소 심막은 가장 널리 사용되는 생체 유래 재료이지만, 돼지 유래 SIS나 ECM을 기반으로 한 제품은 재건 수술이나 심장 관련 용도에서 주목을 받고 있으며, 틈새 용도에 그치지 않고 적용 범위를 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the u.S. cardiovascular & soft tissue repair patch market size is expected to increase from USD 1.38 billion in 2025 to USD 1.49 billion in 2026 and reach USD 2.18 billion by 2031, growing at a CAGR of 7.90% over 2026-2031.

This report is Segmented by Material (Synthetic, Biologic, Tissue-Engineered/Composite), Application (Cardiac Repair, Vascular Repair and Reconstruction, Pericardial Repair, Dural Repair, Soft Tissue Repair), and End User (Hospitals, Ambulatory Surgical Centers, Specialty Cardiovascular and Specialty Surgical Centers). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Cardiovascular & Soft Tissue Repair Patch Market Trends and Insights

Rising Carotid Endarterectomy and Open Peripheral Reconstruction Volumes

Carotid endarterectomy continues to drive direct patch demand as arteriotomy closure remains integral to the procedure. A 2025 analysis of 395,092 carotid revascularizations among Medicare beneficiaries from January 2017 to September 2024 showed carotid endarterectomy accounted for 76.7% of procedures, while carotid artery stenting represented 23.3%. Despite stenting's rise from 13% in 2017 to 38% by 2024, carotid endarterectomy remains the dominant treatment. Although total carotid revascularization volumes declined from 61,280 in 2017 to 43,735 in 2023, carotid endarterectomy cases continue to sustain patch demand. Additionally, open peripheral vascular reconstructions, such as femoral and iliac bypasses, further support patch-assisted closures in complex cases.

Persistent Congenital Heart Defect Repair Burden

Congenital heart defect repairs create long-term demand as patients often require multiple interventions from infancy into adulthood. The American Heart Association reported a birth prevalence of 12.3 per 1,000 in North America, with a 2024 United States prevalence of 466,566 individuals, 60% of whom were under 20 years old. The Society of Thoracic Surgeons' 2024 database update highlighted growth in procedure volumes, with atrial and ventricular septal defect patch repairs among the most common. This recurring demand, influenced by regional cost and stay variations, underscores the importance of flexible pricing and diverse product offerings for suppliers.

High Biologic Patch Acquisition Cost and Reimbursement Gaps

Biologic cardiovascular patches face adoption challenges due to high acquisition costs, often exceeding those of synthetic alternatives. This pricing disparity complicates value analysis reviews, slows hospital transitions, and extends the commercial cycle for premium products in the United States. Reimbursement remains fragmented, with many biologic patches requiring payer negotiations and institutional approvals, delaying adoption by 6 to 18 months. Suppliers also report revenue pressures when premium products encounter procurement resistance or budget scrutiny.

Other drivers and restraints analyzed in the detailed report include:

- Biologic Matrices Gaining Favor in Infection-Prone or Complex Cases

- ASC Migration of Select Soft Tissue Repair Procedures

- Product Failure, Recall Risk, and Durability Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, synthetic patches held a 54.20% revenue share in the United States cardiovascular and soft tissue repair patch market. Their dominance is driven by the cost efficiency, dimensional consistency, and clinical familiarity of materials like ePTFE, polyester, and polypropylene. ePTFE remains critical for carotid and peripheral arteriotomy closures due to its reliability and procedural familiarity. Synthetic products also benefit from simplified procurement processes, enabling predictable price-performance alignment.

Biologic patches are projected to grow at an 8.52% CAGR from 2026 to 2031, driven by their use in contaminated fields, infection-prone repairs, and cases requiring better tissue integration. Bovine pericardium is the most widely used biologic material, while porcine SIS and ECM-based formats are gaining traction in reconstruction and cardiac applications, expanding their adoption beyond niche uses.

List of Companies Covered in this Report:

- AROA BIOSURGERY LIMITED

- Artivion, Inc.

- B. Braun

- Baxter

- Beckton Dickinson

- CorMatrix Cardiovascular, Inc.

- Edward Lifesciences

- Elutia Inc.

- FOC Medical

- Getinge

- Integra LifeSciences

- INTERVASCULAR SAS

- Labcor Laboratorios Ltda.

- LeMaitre Vascular

- Synovis Life Technologies, Inc.

- TELA Bio, Inc.

- Terumo

- Tisgenx, Inc.

- VASCUTEK

- W. L. Gore & Associates

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Carotid Endarterectomy and Open Peripheral Reconstruction Volumes

- 4.2.2 Persistent Congenital Heart Defect Repair Burden

- 4.2.3 Biologic Matrices Gaining Favor in Infection-Prone or Contaminated Fields

- 4.2.4 ASC Migration of Select Soft Tissue Repair Procedures

- 4.2.5 Redo Sternotomy Adhesion Mitigation Raising Pericardial Closure Demand

- 4.2.6 Pediatric Patch Selection Shifting Toward Lower-Calcification Bioscaffolds

- 4.3 Market Restraints

- 4.3.1 High Biologic Patch Acquisition Cost and Reimbursement Scrutiny

- 4.3.2 Product Failure, Recall Risk, and Durability Concerns

- 4.3.3 Endovascular and Transcatheter Substitution Reducing Open-Patch Case Mix

- 4.3.4 Single-Source Tissue Processing and Biologic Raw-Material Dependence

- 4.4 Value Chain / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining power of suppliers

- 4.7.2 Bargaining power of buyers

- 4.7.3 Threat of new entrants

- 4.7.4 Threat of substitutes

- 4.7.5 Competitive rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Synthetic

- 5.1.1.1 ePTFE

- 5.1.1.2 Polyester

- 5.1.1.3 Polypropylene and other synthetics

- 5.1.2 Biologic

- 5.1.2.1 Bovine pericardium

- 5.1.2.2 Porcine SIS / ECM

- 5.1.2.3 Human acellular dermal matrix

- 5.1.3 Tissue-engineered / Composite

- 5.1.3.1 Bioengineered ECM scaffolds

- 5.1.3.2 Hybrid resorbable composites

- 5.1.1 Synthetic

- 5.2 By Application

- 5.2.1 Cardiac Repair

- 5.2.2 Vascular Repair and Reconstruction

- 5.2.3 Pericardial Repair

- 5.2.4 Dural Repair

- 5.2.5 Soft Tissue Repair

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Cardiovascular Clinics and Specialty Surgical Centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AROA BIOSURGERY LIMITED

- 6.3.2 Artivion, Inc.

- 6.3.3 B. Braun Melsungen AG

- 6.3.4 Baxter International Inc.

- 6.3.5 Becton, Dickinson and Company

- 6.3.6 CorMatrix Cardiovascular, Inc.

- 6.3.7 Edwards Lifesciences Corporation

- 6.3.8 Elutia Inc.

- 6.3.9 FOC Medical S.A.

- 6.3.10 Getinge AB

- 6.3.11 Integra LifeSciences Holdings Corporation

- 6.3.12 INTERVASCULAR SAS

- 6.3.13 Labcor Laboratorios Ltda.

- 6.3.14 LeMaitre Vascular, Inc.

- 6.3.15 Synovis Life Technologies, Inc.

- 6.3.16 TELA Bio, Inc.

- 6.3.17 Terumo Corporation

- 6.3.18 Tisgenx, Inc.

- 6.3.19 VASCUTEK Ltd.

- 6.3.20 W. L. Gore & Associates, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment