|

시장보고서

상품코드

2065531

인공지능(AI) 기반 기업 연수 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)AI-Powered Corporate Training - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

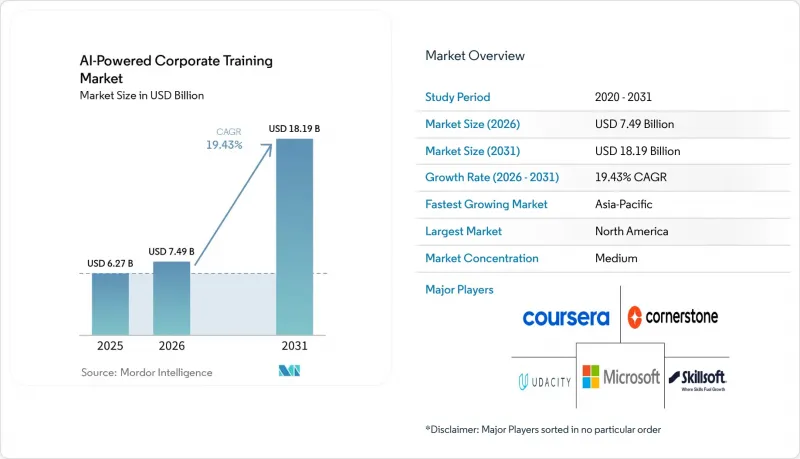

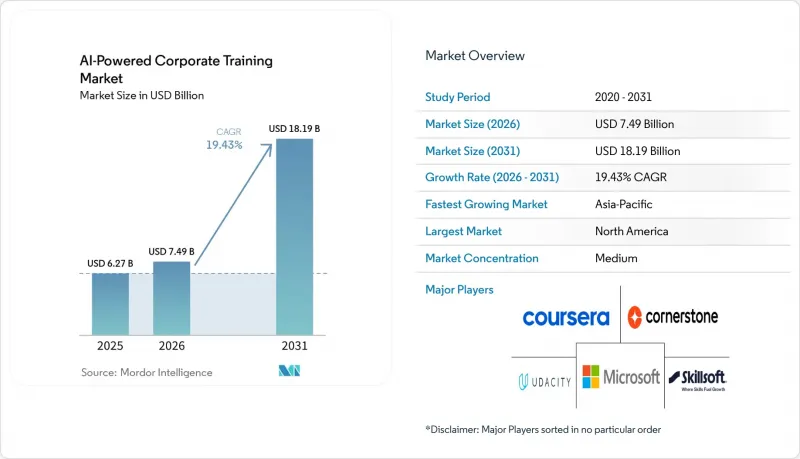

Mordor Intelligence에 의하면, 인공지능(AI) 기반 기업 연수 시장 규모는 2025년 62억 7,000만 달러로 평가되었습니다. 2026년에는 74억 9,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 19.43%로 성장을 지속하여, 2031년에는 181억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(솔루션, 서비스), 배포 방식(클라우드, On-Premise, 하이브리드), 조직 규모(대기업, 중소기업), 최종 사용자 산업(BFSI 등), 학습 모델(자율 학습형, 강사 주도형 등), 기술(머신러닝 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 인공지능(AI) 기반 기업 연수 시장 동향 및 인사이트

스킬의 반감기가 급격히 단축됨에 따른 교육 조달 주기의 재정의

인공지능(AI) 기반 기업 연수 시장은 특히 디지털 분야나 데이터 집약형 직종에서 기술 역량의 유효 기간이 단축됨에 따라 형성되고 있습니다. 세계경제포럼(WEF)의 보고서에 따르면, 2030년까지 기존 노동력의 기술 역량의 39%가 변화하거나 구식이 될 것으로 예상되며, 고용주의 63%는 기술 격차를 비즈니스 혁신의 가장 큰 장애물로 꼽고 있습니다. 이로 인해 역할 요건이 비즈니스 사이클 전반에 걸쳐 변화하는 것이 아니라 사이클 내에서 변화하게 되었기 때문에 연 1회 교육에 의한 기술 갱신의 효과는 떨어지고 있습니다. 따라서 AI 기반 기업 교육 시장은 정적인 카탈로그 형식에서 상시 업데이트되는 컨텐츠, 맞춤형 학습 경로, 그리고 직무 수행 능력에 대한 빈번한 검증으로 전환되고 있습니다. 『Frontiers in Artificial Intelligence』 저널의 2026년 연구에 따르면, 리스킬링 피로가 인지적 및 동기 부여 측면에서 상당한 부담이 된다고 지적되고 있으며, 이는 지속적인 도입을 실현하기 위해서는 컨텐츠의 폭뿐만 아니라 플랫폼의 설계도 중요하다는 것을 의미합니다. 지속적인 재교육이 일반적인 운영 비용으로 자리 잡은 상황에서 학습 내용을 단계적으로 갱신하고 실제 업무 상황과 연계할 수 있는 벤더는 기업과의 계약을 유지하는 데 유리한 입장에 있습니다.

원격 및 하이브리드 근무의 확산이 인프라 투자를 견인하고 있습니다.

인공지능(AI) 기반 기업 연수 시장은 원격 및 하이브리드 근무로의 지속적인 전환으로 인해 계속해서 혜택을 보고 있습니다. 이는 교육 시스템이 현재, 장소, 시간대, 기기를 초월하여 직원들에게 서비스를 제공해야 하기 때문입니다. 2025년에는 클라우드 도입이 78.44%의 점유율을 차지했으며, 이는 분산된 조직 전반에 걸친 유연한 컴퓨팅, 통합된 컨텐츠 관리, 그리고 실시간 데이터 연결에 대한 수요를 반영하고 있습니다. 하이브리드 근무 방식이 미치는 눈에 잘 띄지 않는 영향 중 하나로, 비동기식 학습으로 인해 고용주가 팀 간의 실제 기술 수준을 비교하기가 어려워지고 있다는 점을 들 수 있습니다. 이에 따라 더욱 강력한 벤치마킹과 검증 가능한 자격 증명에 대한 수요가 높아지고 있습니다. Skillsoft에 따르면, Percipio의 AI 관련 ‘Skill Benchmark’ 수료 건수는 2024년 12월부터 2025년 12월까지 전년 대비 994% 증가했으며, AI 컨텐츠 수료 건수는 261% 증가했고, AI 달성 배지 획득 건수는 241% 증가했습니다. 이러한 이용 경향은 구매자들이 더 이상 수료율만으로는 만족하지 않고, 교육이 실무 대응 능력을 향상시킨다는 증거를 요구하고 있음을 보여줍니다. 인공지능(AI) 기반 기업 연수 시장은 이러한 변화의 혜택을 누리고 있습니다. 왜냐하면 컨텐츠 배포, 평가, 그리고 직원 성과 지표 추적을 통합한 플랫폼이 단순한 컨텐츠 라이브러리보다 그 중요성이 커지고 있기 때문입니다.

초기 통합 및 컨텐츠 변환에 드는 높은 비용이 도입을 지연시키고 있습니다.

인공지능(AI) 기반 기업 연수 시장은 기존 컨텐츠의 변환이나 새로운 시스템을 기존 기업 소프트웨어에 연동하는 데 필요한 비용과 노력이라는 측면에서 여전히 큰 도입 장벽에 직면해 있습니다. 이미 도입된 과정의 대부분은 기존의 학습 형식에 맞추어 설계되었기 때문에 맞춤형 제공, AI 기반 피드백, 대화형 연습을 구현하기 위해서는 사소한 수정이 아닌 전면적인 재설계가 필요한 경우가 적지 않습니다. 이러한 부담은 2031년까지 21.93%의 성장이 예상되는 중소기업(SME) 부문에서 특히 두드러집니다. 왜냐하면 초기 변환 및 통합 작업에 드는 비용이 소프트웨어 자체의 가격에 육박하는 경우가 있기 때문입니다. Workday, SAP SuccessFactors, Oracle HCM 및 ID 관리 도구와의 통합은 권한, API, 거버넌스 규칙, 데이터 매핑 측면에서 도입의 복잡성을 더욱 가중시키는 요인이 됩니다. SAP의 ‘Learning Compliance Agent’와 Docebo의 MCP 기반 아키텍처는 모두 벤더가 사전에 구축해 둔 커넥터나 내장된 자동화 기능을 통해 이러한 장벽을 완화하고자 하고 있음을 보여줍니다. 그럼에도 불구하고, 인공지능(AI) 기반 기업 연수 시장에서는 도입에 드는 노력을 감당할 수 있는 구매자가 여전히 유리한 입장에 있어, 그로 인해 총 수요가 시사하는 것보다 도입 현황에 편차가 나타나고 있습니다.

부문별 분석

2025년, 솔루션은 AI 기반 기업 교육 시장의 64.52%를 차지했으며, 이는 플랫폼 부문이 여전히 기업 구매자들에게 핵심적인 수익원임을 입증하고 있습니다. 이 부문에는 AI를 활용한 학습 플랫폼, 적응형 개인화 엔진, 스킬 인텔리전스 도구, 컨텐츠 생성 용도, 평가 시스템, 대화형 어시스턴트, 몰입형 교육 환경 등이 포함됩니다. 구매자들이 솔루션에 가장 많은 비용을 지속적으로 지출하는 이유는 학습 주기 전반에 걸친 발견, 개인화, 제공, 검증, 분석을 관리할 수 있는 단일 운영 계층을 원하기 때문입니다. 이 층의 깊이가, 기업의 기대가 성과 위주로 바뀌고 있음에도 불구하고 솔루션이 여전히 큰 비중을 차지하고 있는 이유이기도 합니다. AI 기반 기업 교육 시장에서 솔루션 스택은 단순한 디지털 과정 카탈로그가 아니라, 직원의 학습 신호를 기록하는 ‘시스템 오브 레코드’의 역할을 하고 있습니다.

주요 벤더들이 광범위한 제품 아키텍처 내에서 분산된 학습 기능을 통합하려고 시도함에 따라, 플랫폼 통합이 이러한 추세를 더욱 강화하고 있습니다. Docebo는 2026년 4월, 스킬 인텔리전스, 기업 지식, 에이전트형 AI를 단일 폐쇄 루프 환경 내에서 연동하는 ‘AgentHub’를 출시했습니다. 또한, Microsoft Copilot 등의 LLM(대규모 언어 모델) 내에서 Docebo가 기본 지식 소스로 기능할 수 있도록 ‘MCP Server’도 도입했습니다. 한편, SAP에 따르면 2026년 4월 조사 대상이었던 경영진의 62%가 인재 데이터와 실적 간의 연관성을 파악하는 방식에 불만을 가지고 있으며, 이는 교육과 경영 성과를 연결해 주는 분석 도구에 대한 수요를 높이고 있습니다. 서비스 부문 시장 점유율은 여전히 낮은 수준이지만, 기업들이 컨텐츠 변환, 모델 튜닝, 도입, 분석 및 성과 연계형 자문 서비스에 대한 지원을 필요로 하고 있기 때문에 2031년까지 연평균 20.27%의 성장이 예상됩니다. 따라서 인공지능(AI) 기반 기업 연수 시장에서 서비스의 중요성이 높아지고 있는 것은 소프트웨어의 중요성이 떨어지고 있기 때문이 아니라, 공급업체의 지속적인 참여 없이는 대규모 도입을 운영 단계로 전환하기 어렵기 때문입니다.

2025년 기준으로 인공지능(AI) 기반 기업 연수 시장 규모의 78.44%를 클라우드가 차지했으며, 이는 적응형 학습, LLM 추론, 스킬 매핑, 지속적인 데이터 동기화 등의 기술적 요구를 반영한 것입니다. 이 부문 역시 2031년까지 연평균 21.42%의 성장률을 보일 것으로 전망되며, 대규모 시장에서 확고한 리더십을 바탕으로 성장세가 꺾이지 않고 있음을 보여주고 있습니다. 기업들이 보다 신속한 업데이트, 통합 관리, 협업 도구 및 인사 플랫폼과의 손쉬운 연동을 원하고 있기 때문에 클라우드는 여전히 선호되는 선택지로 남아 있습니다. 또한 클라우드는 개인 맞춤형 학습 과정과 측정 가능한 직원 준비 상태에 필요한 실시간 피드백 루프도 지원합니다. 인공지능(AI) 기반 기업 연수 시장에서 클라우드는 현재 속도, 규모, 그리고 직원들의 광범위한 접근성을 우선시하는 구매자들에게 있어 기본 아키텍처로 자리 잡고 있습니다.

최근의 제품 발표는 그 우위가 왜 지속되고 있는지를 보여주고 있습니다. 마이크로소프트는 자사의 ‘Learning Agent’가 기술 격차 분석 및 맞춤형 학습 계획을 Microsoft 365 Copilot 및 Teams에 통합한다고 발표했습니다. 이 모델은 해당 회사의 클라우드 환경과 통합된 생산성 제품군에 의존하고 있습니다. 한편, 국방, 원자력 및 기밀을 다루는 정부 기관의 경우, 데이터 주권이나 보안 규제로 인해 클라우드 SaaS 이용이 현실적으로 어려운 경우가 있으므로, On-Premise 도입은 여전히 중요합니다. 또한 은행/금융서비스/보험, 의료 등 각 업계에서도 하이브리드형에 대한 수요가 여전히 뿌리 깊게 남아 있습니다. 이러한 사용자들은 기밀성이 높은 기록을 보다 엄격한 내부 관리 하에 두면서도, 클라우드 측의 AI 기능을 활용하고자 하는 경우가 많기 때문입니다. 인도, 독일, 중국 등 시장에서 데이터 상주 요건에 대한 기대가 이러한 균형을 유지하고 있어, 클라우드의 우위가 계속 확대되고 있음에도 불구하고 인공지능(AI) 기반 기업 연수 시장이 완전히 클라우드로만 전환될 가능성은 낮을 것으로 보입니다.

지역별 분석

2025년, 북미는 인공지능(AI) 기반 기업 연수 시장 점유율의 38.74%를 차지하며 여전히 지역별 최대 수익 기반을 유지했습니다. 그 지위의 상당 부분은 미국이 차지하고 있으며, 이는 기술 분야 고용 밀도가 높고, 성숙한 기업 소프트웨어 조달 체계, 그리고 플랫폼 공급업체와 기업 구매자의 높은 집중도가 결합되어 실현된 결과입니다. 캐나다와 멕시코는 성장하는 기술 생태계와 니어쇼어링과 관련된 기술 향상 수요를 통해 성장세를 보였지만, 이 지역의 중심은 여전히 미국에 있었습니다. 또 다른 장점은 학습 시스템과 보다 광범위한 엔터프라이즈 플랫폼 간의 긴밀한 통합에 있으며, 이를 통해 HCM 및 ERP 환경에 이미 저장된 직원 데이터를 활용하여 교육을 손쉽게 개인화할 수 있습니다. 북미의 인공지능(AI) 기반 기업 연수 시장은 전 세계의 많은 벤더들이 새로운 AI 학습 기능을 다른 지역에 출시하기 전에 이 지역에서 개발 및 테스트를 진행하고 있다는 사실로부터도 혜택을 받고 있습니다.

아시아태평양은 2031년까지 연평균 20.58%의 성장률이 예상되며, 인공지능(AI) 기반 기업 연수 시장에서 가장 빠르게 성장하는 지역 부문이 될 전망입니다. 이러한 성장은 기업 내 AI의 광범위한 도입, 대규모 노동력 기반, 그리고 중국, 인도, 일본, 한국, 아세안 시장 전반에 걸쳐 기술 역량 격차를 해소해야 한다는 압박이 커지고 있는 데 힘입은 것입니다. 특히 인도는 기업들이 AI와 인력을 결합한 모델을 추진하며, AI 역량 구축을 뒷전으로 미루는 프로그램이 아닌 전략적 요건으로 삼고 있다는 점에서 두드러집니다. 유럽은 독일, 영국, 프랑스가 주도하는 중요한 시장이며, 이들 국가에서는 규정 준수 요건이 직접적인 투자 수익률(ROI)의 논리와 마찬가지로 교육 수요를 형성하고 있습니다. EU의 AI법은 2025년 2월부터 AI 리터러시를 공식 요건으로 지정했으며, 2026년 8월부터는 이행 의무를 확대했습니다. 이에 따라 문서화된 기업용 AI 교육에 대한 보다 체계적인 조달 수요가 대두되고 있습니다. Coursera가 인용한 조사 결과에 따르면, 독일에서 인력 부족으로 인한 연간 비용은 3,390억 유로(3,830억 달러)에 달할 것으로 추정되며, 이는 기술 개발에 대한 투자 부족이 초래하는 거시경제적 비용을 여실히 보여주고 있습니다.

남미는 여전히 규모가 작은 지역 시장이지만, 브라질과 아르헨티나는 기술 부문의 확대와 다국적 기업의 진출이 공식적인 AI 교육 도입을 뒷받침하고 있어 실질적인 성장의 거점으로 부상하고 있습니다. 해당 지역에서는 기업이 지리적으로 분산되어 있고, 다양한 언어를 사용하는 직원들에게 도입 과정에서 발생하는 마찰을 최소화하며 서비스를 제공해야 하기 때문에 클라우드 네이티브 및 다국어 지원이 가장 중요하게 여겨지고 있습니다. 중동 및 아프리카은 상황에 따라 차이가 있습니다. 사우디아라비아와 아랍에미리트(UAE) 등 걸프협력회의(GCC) 회원국들은 국가 디지털화 전략의 일환으로 AI 인재의 역량 강화에 투자하고 있습니다. 아프리카 대륙에서 남아프리카공화국은 여전히 가장 발전된 기업 대상 연수 시장이지만, 사하라 이남 아프리카 전체에서의 도입은 아직 초기 단계에 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the aI-powered corporate training market size is expected to grow from USD 6.27 billion in 2025 to USD 7.49 billion in 2026 and is forecast to reach USD 18.19 billion by 2031 at 19.43% CAGR over 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment Model (Cloud, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, and More), Learning Model (Self-Paced, Instructor-Led, and More), Technology (Machine Learning, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Powered Corporate Training Market Trends and Insights

Rapid Skills Half-Life Is Redefining The Training Procurement Cycle

The AI-powered corporate training market is being shaped by the shrinking usable life of technical skills, especially in digital and data-heavy roles. The World Economic Forum reported that 39% of existing workforce skill sets will transform or become outdated by 2030, and 63% of employers identified skill gaps as the biggest barrier to business transformation. This makes annual training refreshes less effective because role requirements are now shifting inside active business cycles rather than between them. The AI-powered corporate training market is therefore moving toward always-on content updates, adaptive pathways, and frequent validation of role readiness instead of static catalogs. A 2026 study in Frontiers in Artificial Intelligence described reskilling fatigue as a real cognitive and motivational burden, which means platform design now matters as much as content breadth for sustained adoption. Vendors that can refresh learning in smaller steps and tie it to real work context are better placed to hold enterprise contracts as continuous reskilling becomes a normal operating expense.

Remote and Hybrid Workforce Proliferation Drives Infrastructure Investment

The AI-powered corporate training market continues to benefit from the lasting shift to remote and hybrid work because training systems now need to serve employees across locations, time zones, and devices. Cloud deployment led with 78.44% share in 2025, which reflects the need for elastic compute, centralized content management, and live data connections across distributed organizations. A less visible effect of hybrid work is that asynchronous learning makes it harder for employers to compare actual skill levels across teams, which raises demand for stronger benchmarking and verifiable credentials. Skillsoft said AI-related Skill Benchmark completions on Percipio rose 994% year over year from December 2024 to December 2025, while AI content completions increased 261% and AI achievement badges rose 241%. Those usage patterns show that buyers are no longer satisfied with completion rates alone and are instead asking for evidence that training improves job readiness. The AI-powered corporate training market is gaining from this shift because platforms that combine delivery, assessment, and workforce signal tracking are becoming more relevant than standalone content libraries.

High Up-Front Integration and Content-Conversion Costs Slow Adoption

The AI-powered corporate training market still faces a meaningful adoption barrier in the cost and effort needed to convert legacy content and connect new systems to existing enterprise software. Much of the installed course base was designed for older learning formats, so adaptive delivery, AI-based feedback, and conversational practice often require full redesign rather than light editing. That burden is especially visible among SMEs, even though the segment is projected to grow at 21.93% through 2031, because upfront conversion and integration work can approach the cost of the software itself. Integration with Workday, SAP SuccessFactors, Oracle HCM, and identity tools adds another layer of implementation complexity around permissions, APIs, governance rules, and data mapping. SAP's Learning Compliance Agent and Docebo's MCP-based architecture both show that vendors are trying to reduce this friction with prebuilt connectors and embedded automation. Even so, the AI-powered corporate training market still favors buyers that can absorb implementation effort, which keeps adoption more uneven than top-line demand might suggest.

Other drivers and restraints analyzed in the detailed report include:

- Rising Enterprise Spend on Personalized Learning Pathways

- LLM-Powered Coaching Bots Integrating With ERP-HCM Data Pipelines

- Data-Privacy and Intellectual-Property Concerns Dampen Platform Confidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 64.52% of the AI-powered corporate training market share in 2025, which confirms that the platform layer remains the core revenue engine for enterprise buyers. This segment covers AI-powered learning platforms, adaptive personalization engines, skills intelligence tools, content generation applications, assessment systems, conversational assistants, and immersive training environments. Buyers continue to spend most heavily on solutions because they want a single operating layer that can manage discovery, personalization, delivery, verification, and analytics across the learning cycle. The depth of this layer also explains why solutions continue to command a larger share, even as enterprise expectations become more outcome-focused. In the AI-powered corporate training market, the solution stack has become the system of record for workforce learning signals rather than a simple catalog of digital courses.

Platform consolidation is reinforcing that position, as leading vendors are trying to unify fragmented learning functions within broader product architectures. Docebo launched AgentHub in April 2026 to connect skills intelligence, enterprise knowledge, and agentic AI within a single closed-loop environment, and it also introduced an MCP Server so Docebo could serve as a native knowledge source within LLMs such as Microsoft Copilot. At the same time, SAP said 62% of C-suite executives surveyed in April 2026 were dissatisfied with the way people data connected to business performance, which strengthens demand for analytics that link training to operating outcomes. Services remain smaller in share, but they are projected to grow at 20.27% through 2031, as enterprises need support with content conversion, model tuning, implementation, analytics, and performance-linked advisory services. The AI-powered corporate training market is therefore seeing services gain importance not because software is losing relevance, but because large deployments are harder to operationalize without ongoing vendor involvement.

Cloud accounted for 78.44% of AI-powered corporate training market size in 2025, which reflects the technical needs of adaptive learning, LLM inference, skills mapping, and continuous data synchronization. The segment is also projected to expand at 21.42% through 2031, which shows that market leadership at scale has not reduced its growth momentum. Cloud remains the preferred route because enterprises want faster updates, centralized administration, and easier integration with collaboration tools and HR platforms. It also supports the real-time feedback loops required for personalized learning journeys and measurable workforce readiness. In the AI-powered corporate training market, cloud is now the default architecture for buyers that prioritize speed, scale, and broad employee access.

Recent product launches show why that advantage persists. Microsoft said its Learning Agent would integrate skill gap analysis and personalized learning plans into Microsoft 365 Copilot and Teams, a model that depends on the company's cloud environment and embedded productivity stack. On-premise deployments still matter in defense, nuclear, and classified government settings because data sovereignty and security rules can make cloud SaaS impractical. Hybrid demand is also holding up in banking, financial services, insurance, and healthcare because these users often want cloud-side AI functionality while keeping sensitive records under tighter internal control. National data residency expectations in markets such as India, Germany, and China are sustaining that balance, which means the AI-powered corporate training market is unlikely to become fully cloud-only even as cloud keeps widening its lead.

Geography Analysis

North America held 38.74% of the AI-powered corporate training market share in 2025, which kept it as the largest regional revenue base. The United States accounted for the bulk of that position because it combines dense technology employment, mature enterprise software procurement, and a strong concentration of platform vendors and enterprise buyers. Canada and Mexico added momentum through growing technology ecosystems and nearshoring-linked upskilling needs, but the regional center of gravity remained in the United States. Another advantage is the depth of integration between learning systems and broader enterprise platforms, which makes it easier to personalize training using workforce data already housed in HCM and ERP environments. The AI-powered corporate training market in North America also benefits from the fact that many global vendors build and test new AI learning features in this region before scaling them elsewhere.

Asia-Pacific is projected to grow at 20.58% through 2031, making it the fastest-growing regional segment in the AI-powered corporate training market size. Growth is being supported by broad enterprise AI adoption, large workforce bases, and increasing pressure to close technical skill gaps across China, India, Japan, South Korea, and ASEAN markets. India stands out because enterprises are moving ahead with AI-human workforce models and treating AI capability building as a strategic requirement rather than a delayed program. Europe remains a significant market led by Germany, the United Kingdom, and France, where compliance requirements are shaping training demand as much as direct return-on-investment logic. The EU AI Act made AI literacy a formal requirement from February 2025 and expanded enforcement obligations from August 2026, which has created a more structured procurement case for documented corporate AI training. Germany's estimated annual cost of unfilled vacancies reached EUR 339 billion (USD 383 billion), in findings cited by Coursera, which underlines the macroeconomic cost of underinvestment in skills development.

South America is still a smaller regional base, but Brazil and Argentina are emerging as practical growth pockets because technology-sector expansion and multinational presence are pushing formal AI training adoption. Cloud-native and multilingual deployments are most relevant there because enterprises often need to serve geographically spread and language-diverse workforces with limited implementation friction. The Middle East and Africa is more uneven, with Gulf Cooperation Council countries such as Saudi Arabia and the United Arab Emirates investing in AI workforce capability as part of national digitalization agendas. South Africa remains the most developed corporate training market on the African continent, while broader sub-Saharan adoption is still at an earlier stage.

- Microsoft Corporation

- Coursera, Inc.

- Skillsoft Corporation

- Cornerstone OnDemand, Inc.

- Udacity, Inc.

- SAP SE (Litmos)

- IBM Corporation (SkillsBuild)

- Google LLC (Cloud Learning Services)

- Oracle Corporation

- Pluralsight LLC

- Degreed, Inc.

- Docebo S.p.A.

- OpenSesame Inc.

- EdCast Inc. (upGrad)

- Fuse Universal Ltd.

- 360Learning SA

- Workday, Inc.

- NovoEd, Inc.

- Valamis Group Oy

- CYPHER Learning

- Absorb Software Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Skills-half-life in Tech Roles

- 4.2.2 Explosion of Remote Hybrid Workforces

- 4.2.3 Rising Enterprise Spend on Personalized Learning Pathways

- 4.2.4 Integration of LLM-powered Coaching Bots With ERP-HCM Data

- 4.2.5 Auto-generated Micro-credentials Linked to Internal Talent Marketplaces

- 4.2.6 ESG-driven Mandates for Continuous Reskilling Disclosures

- 4.3 Market Restraints

- 4.3.1 High Up-front Integration Content-conversion Costs

- 4.3.2 Data-Privacy Intellectual-Property Concerns

- 4.3.3 'Shadow-learning' Risk From Unsanctioned Gen-AI Tools

- 4.3.4 Algorithmic Bias Audits Delaying Procurement Cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 AI-powered Learning Platforms

- 5.1.1.2 Adaptive Learning and Personalization Engines

- 5.1.1.3 AI Skills Intelligence Platforms

- 5.1.1.4 AI Content Generation Tools

- 5.1.1.5 AI Assessment and Learning Analytics

- 5.1.1.6 Conversational AI Learning Assistants

- 5.1.1.7 Immersive AI Training Platforms

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 IT Telecom

- 5.4.2 BFSI

- 5.4.3 Manufacturing

- 5.4.4 Healthcare Life Sciences

- 5.4.5 Retail eCommerce

- 5.4.6 Other End-User Industries

- 5.5 By Learning Model

- 5.5.1 Self-Paced

- 5.5.2 Instructor-Led

- 5.5.3 Blended

- 5.6 By Technology

- 5.6.1 Machine Learning

- 5.6.2 Natural Language Processing

- 5.6.3 Speech an Voice Recognition

- 5.6.4 Computer Vision

- 5.6.5 Other Emerging AI Technology

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 ASEAN

- 5.7.4.6 Australia New Zealand

- 5.7.4.7 Rest of Asia-Pacific

- 5.7.5 Middle East Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of the Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Coursera, Inc.

- 6.4.3 Skillsoft Corporation

- 6.4.4 Cornerstone OnDemand, Inc.

- 6.4.5 Udacity, Inc.

- 6.4.6 SAP SE (Litmos)

- 6.4.7 IBM Corporation (SkillsBuild)

- 6.4.8 Google LLC (Cloud Learning Services)

- 6.4.9 Oracle Corporation

- 6.4.10 Pluralsight LLC

- 6.4.11 Degreed, Inc.

- 6.4.12 Docebo S.p.A.

- 6.4.13 OpenSesame Inc.

- 6.4.14 EdCast Inc. (upGrad)

- 6.4.15 Fuse Universal Ltd.

- 6.4.16 360Learning SA

- 6.4.17 Workday, Inc.

- 6.4.18 NovoEd, Inc.

- 6.4.19 Valamis Group Oy

- 6.4.20 CYPHER Learning

- 6.4.21 Absorb Software Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment