|

시장보고서

상품코드

2063907

가상현실(VR) 기업 연수 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Virtual Reality (VR) Corporate Training - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

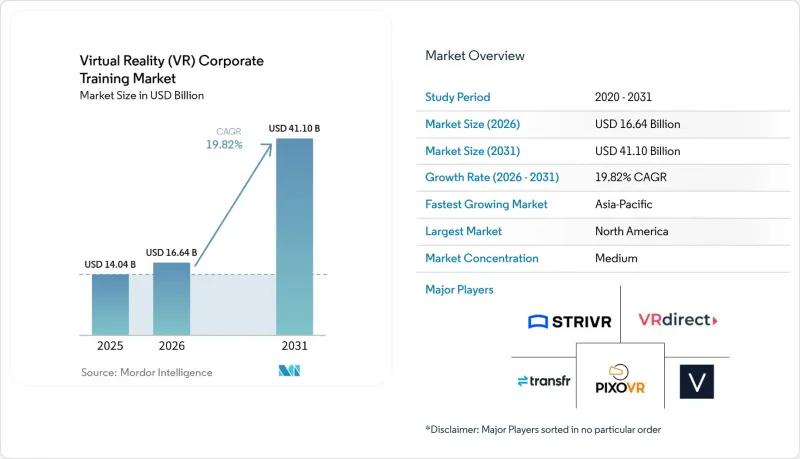

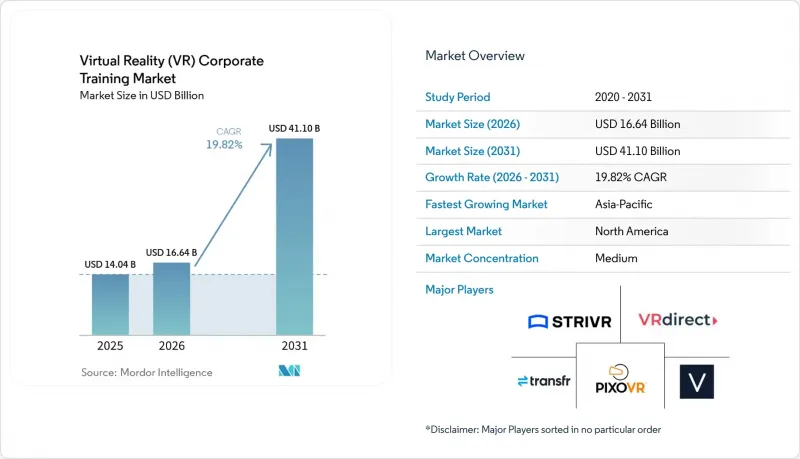

Mordor Intelligence에 의하면, 가상현실(VR) 기업 연수 시장 규모는 2025년에 140억 4,000만 달러로 평가되었고 2026년 166억 4,000만 달러에서 2031년까지 411억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 19.82%를 나타낼 전망입니다.

본 보고서는 구성 요소(하드웨어, 소프트웨어, 서비스), 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 기업 규모(대기업, 중소기업), 교육 유형(안전·규정 준수, 기술·운영, 기타), 업종(제조, 의료, 소매, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 가상현실(VR) 기업 연수 시장 동향과 인사이트

교육 시간 단축과 오류율 감소 효과가 입증됨

가상현실(VR) 기업 연수 시장에서 몰입형 학습과 역량 습득까지 걸리는 시간 단축을 연계할 수 있다면, 도입은 가장 빠르게 확대될 것입니다. 2025년에 발표된, 37건의 동료 심사를 거친 연구를 종합한 리뷰에 따르면, VR 기반 안전 교육은 기존의 강의실 형식 교육보다 즉각적인 지식 습득과 위험 요소 파악 측면에서 더 뛰어난 성과를 가져다주는 것으로 밝혀졌습니다. 해당 리뷰에서는 기존 연수 그룹이 동일한 기간 동안 선언적 지식을 훨씬 더 빨리 상실한다는 사실이 밝혀졌으며, 세션 종료 후에도 지속되는 VR의 가치가 강조되었습니다. 2025년에 실시된 또 다른 연구에 따르면, 산업 종사자들이 VR 교육을 받은 후 안전 의식이 30%, 안전 지식이 25%, 위험 인식이 30% 향상된 것으로 나타났습니다. 또한, 기업 내 활용 사례에 따르면, 교육에 소요되는 평균 시간이 기존의 대면 수업 방식인 120분에서 VR을 활용할 때는 30분으로 단축되었다고 보고되고 있습니다. 이처럼 교육 시간 단축과 정착률 향상이 맞물리면서, 대규모 직원을 대상으로 정기적인 자격 갱신이 필요한 조직에서 지속적인 투자를 뒷받침하고 있습니다.

고위험 업무 프로세스에서 안전한 시뮬레이션에 대한 수요 증가

실지 훈련에서는 근로자가 부상이나 장비 손상, 가동 중단 등의 위험에 노출되기 때문에 가상현실(VR)을 활용한 기업 연수 시장에는 고위험 업무 프로세스에서 명확한 활용 사례가 있습니다. VR을 활용하면 사람이나 자산을 위험에 빠뜨리지 않고, 통제된 환경에서 위험한 작업을 반복적으로 수행할 수 있습니다. 2025년 조사에 따르면, 창고 환경 전문가의 86.67%가 VR 안전 교육을 효과적이고 현실적이라고 평가했습니다. 또한, 해당 조사에서 응답자의 75%가 VR 안전 교육을 비용 대비 효과가 높다고 인식하고 있는 것으로 나타났습니다. 또한, 2025년에 실시된 또 다른 조사에서는 VR을 활용한 훈련을 받은 산업 종사자들 사이에서 안전 의식과 위험 의식이 측정 가능한 수준으로 향상된 것으로 나타났습니다. 물류, 제조, 건설 업계의 고용주들이 보다 안전한 훈련 방법을 모색하는 가운데, 몰입형 시뮬레이션은 VR 기업 연수 시장의 중심에 점점 더 가까워지고 있습니다.

맞춤형 컨텐츠, 시스템 통합 및 기기 도입에 따른 고액의 초기 비용

가상현실(VR) 기업 연수 시장에서는 구매자들이 맞춤형 컨텐츠, 시스템 통합 및 기기 도입에 드는 첫해 총 비용을 평가할 때 여전히 주저하는 모습을 보이고 있습니다. VRC의 보고서에 따르면, 전문가용 인터랙티브 모듈은 기존에 컨텐츠 1시간당 5만-20만 달러의 비용이 들었으며, 변화하는 절차에 맞추어 시나리오를 업데이트하기 위한 지속적인 유지보수도 필요했습니다. 같은 소식통에 따르면, 하드웨어, 라이선싱, IT 통합을 포함할 경우, 첫해에 100-200명의 사용자를 대상으로 하는 프로그램 비용은 15만-30만 달러에 달할 가능성이 있습니다. 이러한 부담은 전문 인력이 부족한 조직이나 연수 빈도가 낮은 조직에 가장 크게 짓누르게 됩니다. 왜냐하면 투자 회수 기간이 길어지기 때문입니다. AutoVRse 및 기타 노코드 접근 방식을 통해 개발 기간이 단축되고 맞춤형 구축 비용 부담도 줄어들고 있지만, 극히 특수한 워크플로우의 경우 여전히 설계, 검증 및 내부 프로세스 매핑이 필요합니다. 따라서 가상현실(VR) 기업 연수 시장의 구매자 중에는 기업 전체에 즉시 도입하기보다는 거점별로 단계적으로 도입을 진행하는 사례도 여전히 볼 수 있습니다.

부문별 분석

2025년, 하드웨어는 가상현실(VR) 기업 연수 시장 점유율 43.81%를 차지했습니다. 이는 여러 거점을 보유한 조직에서 기업용 차량 함대를 구축하는 데 드는 비용을 반영한 것입니다. 독립형 헤드셋은 설치 과정이 간편하고 구매자의 유지 관리 부담을 줄여주었기 때문에 신규 도입의 대부분을 차지했습니다. 유선 연결 방식의 시스템은 여전히 높은 시각적 충실도가 중요시되는 외과, 항공, 국방 분야의 교육에서 중요한 역할을 유지해 왔습니다. 컨트롤러, 트래커, 햅틱 도구는 상호작용을 추가함으로써 절차의 현실감을 높여주었기 때문에 유지보수 및 장비 시뮬레이션 분야에서 그 중요성이 커졌습니다. 가상현실(VR) 기업 연수 시장은 구매자가 장래에 가치 창출의 중심을 소프트웨어로 전환할 계획이었습니다 하더라도, 도입 초기 단계에서는 여전히 하드웨어 중심의 구성을 유지하고 있었습니다.

소프트웨어 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 22.42%로 확대될 것으로 예상되며, 가상현실(VR) 기업 연수 시장에서 가장 빠르게 성장하는 분야가 될 전망입니다. 이러한 변화는 맞춤형 엔진 개발에서 사내 학습 팀이 모듈을 보다 신속하게 구축할 수 있는 노코드 저작 플랫폼으로 점차 전환되고 있습니다. 클라우드 기반 컨텐츠 관리, 행동 분석, LMS(학습 관리 시스템)과의 통합은 더 이상 선택적 부가 기능이 아니라 소프트웨어의 표준 요건으로 자리 잡고 있습니다. 『Virtual Reality』지의 2026년 연구에 따르면, AI-LLM(대규모 언어 모델)을 통합한 VR 교육은 지식 습득, 1주일 후의 정착률, 그리고 교육생의 자기효능감 측면에서 표준 VR을 능가하는 성과를 보였습니다. 많은 기업이 여전히 맞춤형 시나리오 설계, 도입 계획, 운영 관리에 있어 외부 지원을 필요로 하고 있기 때문에 이 서비스는 VR 기업 연수 업계에서 계속해서 중요한 위치를 차지하고 있습니다.

2025년에는 클라우드 기반 배포가 가상현실(VR) 기업 연수 시장의 58.62%를 차지하며, 확장 가능한 컨텐츠 관리에 대한 강력한 수요가 부각되었습니다. 클라우드 배포를 통해 조직은 각 지점에서 기기를 재이미징할 필요 없이, 업데이트된 모듈을 전 세계의 헤드셋에 배포할 수 있습니다. 이러한 장점은 오래된 컨텐츠가 감사상의 문제를 야기할 가능성이 있는 규정 준수 프로그램에서 가장 중요합니다. On-Premise 배포는 보다 엄격한 데이터 상주 요건이나 격리된 시스템이 필요한 국방, 금융 및 기타 엄격하게 관리되는 환경에서 여전히 중요합니다. 따라서 VR 기업 연수 시장에서는 규모와 업데이트 속도가 중요한 분야에서는 클라우드가 선호되는 반면, 보다 정교한 제어가 요구되는 이용 사례에서는 On-Premise 옵션이 여전히 유지되고 있습니다.

가상현실(VR) 기업 연수 시장에서 하이브리드 방식 시장 규모는 2031년까지 연평균 성장률(CAGR) 21.36%로 성장할 것으로 전망됩니다. 이 모델은 클라우드 규모의 배포와 로컬에서의 ID 관리, 그리고 기밀성이 높은 성능 데이터의 로컬 처리를 결합하고 있습니다. 고용주들이 시선, 음성, 행동 데이터가 GDPR(EU 개인정보보호규정) 및 새로운 AI 거버넌스 규정에 어떻게 부합하는지 검토함에 따라, 이러한 균형의 중요성이 더욱 커지고 있습니다. 하이브리드 아키텍처는 엄격한 내부 보안 워크플로를 유지하면서 컨텐츠 관리를 일원화하고자 하는 대기업에게 특히 중요합니다. 따라서 가상현실(VR) 기업 연수 시장에서 도입 여부는 기기의 유형나 대역폭보다는 개인정보 보호 거버넌스나 기업의 IT 정책에 따라 좌우되는 경향이 점점 더 강해지고 있습니다.

지역별 분석

2025년, 북미는 가상현실(VR) 기업 연수 시장 점유율의 36.51%를 차지하며 1위를 유지했습니다. 미국은 제조업, 소매업, 의료, 금융 서비스 분야의 기업들의 조기 도입을 통해 그 수요의 상당 부분을 주도했습니다. 또한, 이 지역은 안전, 의료 시뮬레이션, 소프트 스킬, 기업 도입에 특화된 공급업체를 포함한 탄탄한 벤더 기반의 혜택을 누리고 있습니다. 이러한 집중화를 통해 구매자는 공급업체를 비교하고, 신속하게 시범 운영을 실시하며, 단일 이용 사례에서 더 광범위한 학습 프로그램으로 확대할 수 있게 됩니다. 따라서 가상현실(VR) 기업 연수 시장에서 북미는 여전히 대규모 기업 도입에 있어 가장 확실한 기준점이 되고 있습니다.

유럽은 독일, 영국, 프랑스를 필두로 가상현실(VR) 기업 연수 시장에서 2위의 규모를 유지했습니다. NMY의 보고에 따르면, 루프트한자 항공 훈련 센터는 연간 2만 명 이상의 승무원을 대상으로 VR 안전 시뮬레이션을 도입하여, 기존 방식에 비해 1,400만 유로(1,526만 달러)의 비용 절감을 달성했습니다. Uptale는 2025년 4월, VRdirect와의 전략적 제휴를 발표하고, 유럽, 북미, 아시아의 350개 이상의 기업 고객에게 서비스를 제공함으로써 해당 지역 내 플랫폼의 영향력을 강화했습니다. 또한, 유럽에서는 GDPR(EU 개인정보보호규정) 및 관련 AI 거버넌스 규정에 따라 생체 인증 데이터와 추론 데이터에 대한 감독이 강화되고 있어, 이는 도입을 지연시킬 가능성은 있지만, 개인정보 보호를 중시하는 플랫폼 설계에는 유리하게 작용할 수 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 23.81%로 확대될 것으로 예상되며, 가상현실(VR) 기업 연수 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 산업 종사자 수, 국내 헤드셋 생태계의 확대, 그리고 공공 직업 훈련 프로그램이 해당 지역 전체에서의 도입을 뒷받침하고 있습니다. 인도, 중국, 일본, 한국, 싱가포르, 호주는 방대한 노동력과 산업별 기술 격차를 동시에 안고 있기 때문에 VR 교육과 매우 잘 어울립니다. 중동도 건설, 에너지, 정부, 국방 프로그램에 대한 투자를 확대하고 있는 반면, 남미에서는 제조업의 디지털화와 노동력의 현대화로 인해 성장세가 가속화되고 있습니다. 아프리카에서는 아직 도입 초기 단계이지만, 광업, 에너지, 정부 기관에서의 활용 사례가 남아프리카공화국, 이집트, 나이지리아 등 여러 국가에서 VR 기업 연수 시장의 견고한 기반이 되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the virtual reality (VR) corporate training market size was valued at USD 14.04 billion in 2025 and estimated to grow from USD 16.64 billion in 2026 to reach USD 41.10 billion by 2031, at a CAGR of 19.82% during the forecast period (2026-2031).

This report is Segmented by Component (Hardware, Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and SMEs), Training Type (Safety and Compliance, Technical and Operational, and More), Industry Vertical (Manufacturing, Healthcare, Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Virtual Reality (VR) Corporate Training Market Trends and Insights

Proven Reduction In Training Time And Error Rates

In the virtual reality (VR) corporate training market, adoption rises fastest when employers can tie immersive learning to a faster time-to-competency. A 2025 review covering 37 peer-reviewed studies found that VR-based safety training produced stronger immediate knowledge acquisition and hazard identification than traditional classroom formats. The same review showed that traditional training groups lost declarative knowledge much faster over comparable periods, underscoring VR's value beyond the session. A separate 2025 study found that industrial workers improved safety awareness by 30%, safety knowledge by 25%, and risk awareness by 30% after VR training. Reports also showed that average training duration fell from 120 minutes in classroom settings to 30 minutes with VR in enterprise use cases. This mix of shorter training time and stronger retention supports recurring investment when organizations need repeat certification across large workforces.

Rising Need For Safe Simulation In High-Risk Workflows

The virtual reality corporate training market has a clear use case in high-risk workflows, as live practice exposes workers to injury, equipment damage, and downtime. VR lets workers repeat hazardous tasks in a controlled environment without risking people or assets. A 2025 study found that 86.67% of warehouse-environment experts rated VR safety training as effective and realistic. The same study found that 75% of respondents considered VR safety training cost-effective. Another 2025 study also showed measurable gains in safety awareness and risk awareness among industrial workers trained with VR. As logistics, manufacturing, and construction employers seek safer rehearsal methods, immersive simulation is moving closer to the core of the virtual reality corporate training market.

High Upfront Cost Of Custom Content, Integration, And Fleet Rollout

The virtual reality (VR) corporate training market still faces hesitation when buyers evaluate the full first-year cost of custom content, systems integration, and device fleets. VRC reported that professional interactive modules historically required USD 50,000 to USD 200,000 per completed hour of content, with ongoing maintenance needed to keep scenarios aligned with changing procedures. The same source said programs for 100 to 200 users in year 1 can range from USD 150,000 to USD 300,000, once hardware, licensing, and IT integration are included. This burden is hardest for organizations with small specialist crews or infrequent training because the payback period is longer. AutoVRse and other no-code approaches are reducing development time and easing pressure on custom build costs, but highly specific workflows still require design, validation, and internal process mapping. For that reason, some buyers in the virtual reality (VR) corporate training market still phase rollouts site by site instead of expanding immediately across the full enterprise.

Other drivers and restraints analyzed in the detailed report include:

- Standardization Of Training Across Distributed Workforces

- Falling Deployment Friction From Standalone Headsets And Cloud Delivery

- Motion Sickness, Headset Fatigue, And Hygiene Constraints In Repeated Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured 43.81% of the virtual reality (VR) corporate training market share in 2025, which reflected the cost of enterprise fleet buildouts across multi-site organizations. Standalone headsets led most new deployments because they reduced setup complexity and lowered the ownership burden for buyers. Tethered systems kept a premium role in surgical, aviation, and defense training where higher visual fidelity still mattered. Controllers, trackers, and haptic tools gained relevance in maintenance and equipment simulation because they added interaction, which improved procedural realism. The virtual reality (VR) corporate training market, remained hardware-heavy at the point of first rollout, even when buyers planned to shift value capture toward software over time.

Software is projected to expand at a 22.42% CAGR from 2026 to 2031, making it the fastest-growing component in the virtual reality (VR) corporate training market. The shift is moving from bespoke engine development toward no-code authoring platforms that let internal learning teams build modules faster. Cloud content management, behavioral analytics, and LMS integration are becoming baseline software requirements rather than optional add-ons. A 2026 study in Virtual Reality found that AI-LLM-integrated VR training outperformed standard VR on knowledge acquisition, 1-week retention, and trainee self-efficacy. Services remain important within the VR corporate training industry because many enterprises still need outside support for custom scenario design, rollout planning, and managed operations.

Cloud-based delivery captured 58.62% of the virtual reality (VR) corporate training market in 2025, underscoring a strong preference for scalable content management. Cloud delivery helps organizations push updated modules to global headset fleets without reimaging devices at each site. That advantage matters most in compliance programs where outdated content can create audit problems. On-premises deployments still matter in defense, finance, and other tightly controlled environments that require stronger data residency or isolated systems. The virtual reality corporate training market has therefore favored cloud, where scale and update speed matter, while preserving on-premises options for higher-control use cases.

Hybrid deployment is forecast to grow at a 21.36% CAGR through 2031 in the virtual reality (VR) corporate training market. This model combines cloud-scale distribution with local identity controls and local handling of sensitive performance data. That balance is gaining relevance as employers review how eye-gaze, voice, and behavioral data fit within GDPR and newer AI-governance rules. Hybrid architectures are especially relevant for large enterprises that want centralized content management without giving up tighter internal security workflows. Deployment choices in the virtual reality (VR) corporate training market are therefore being shaped more by privacy governance and enterprise IT policy than by device type or bandwidth.

Geography Analysis

North America held 36.51% of the virtual reality (VR) corporate training market share in 2025, maintaining its leading position. The United States drove most of that demand through earlier enterprise adoption across manufacturing, retail, healthcare, and financial services. The region also benefits from a dense vendor base, including providers focused on safety, healthcare simulation, soft skills, and enterprise deployment. This concentration helps buyers compare vendors, pilot faster, and expand from one use case into broader learning programs. In the virtual reality (VR) corporate training market, North America therefore remained the clearest reference point for scaled enterprise deployment.

Europe remained the second-largest region in the virtual reality (VR) corporate training market, led by Germany, the United Kingdom, and France. NMY reported that Lufthansa Aviation Training used VR safety simulations for more than 20,000 flight attendants annually and achieved EUR 14 million (USD 15.26 million) in savings relative to traditional formats. Uptale announced a strategic alliance with VRdirect in April 2025 to serve more than 350 enterprise customers across Europe, North America, and Asia, which strengthened regional platform reach. Europe also faces tighter scrutiny of biometric and inferred data under GDPR and related AI governance rules, which can slow procurement but also reward privacy-focused platform design.

Asia-Pacific is projected to expand at a 23.81% CAGR through 2031, making it the fastest-growing region in the virtual reality corporate training market. Industrial workforce scale, expanding domestic headset ecosystems, and public workforce upskilling programs are supporting adoption across the region. India, China, Japan, South Korea, Singapore, and Australia align well with VR training because they combine large labor pools with sector-specific skills gaps. The Middle East is also increasing investment in construction, energy, government, and defense programs, while South America is building momentum from manufacturing digitization and workforce modernization. Africa remains earlier in adoption, but mining, energy, and government use cases provide a strong base for the VR corporate training market in countries such as South Africa, Egypt, and Nigeria.

- Strivr Labs, Inc.

- VRdirect GmbH

- PixoVR, Corp.

- Transfr Inc.

- Virti Inc.

- Mursion, Inc.

- Osso VR, Inc.

- Oxford Medical Simulation Ltd.

- FVRVS Limited, trading as FundamentalXR

- Pixaera Inc.

- JCR Group Ltd, trading as Bodyswaps

- 3spin Learning GmbH & Co. KG

- TLN Training Limited, trading as Gemba

- WorldViz, Inc.

- SimX, Inc.

- Interplay Learning, Inc.

- Humulo Virtual Reality Inc.

- Skillveri Training Solutions Pvt Ltd.

- Moth+Flame, Inc.

- Innoactive GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proven Reduction in Training Time and Error Rates

- 4.2.2 Rising Need for Safe Simulation in High-Risk Workflows

- 4.2.3 Standardization of Training Across Distributed Workforces

- 4.2.4 Falling Deployment Friction from Standalone Headsets and Cloud Delivery

- 4.2.5 AI-Generated Scenario Authoring Compressing Custom Content Backlogs

- 4.2.6 Audit-Ready Skills Telemetry Supporting Regulated Competency Assurance

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Custom Content, Integration, and Fleet Rollout

- 4.3.2 Motion Sickness, Headset Fatigue, and Hygiene Constraints in Repeated Use

- 4.3.3 Biometric and AI-Governance Scrutiny Over Eye-Gaze, Voice, and Behavioral Data

- 4.3.4 Procurement Delays from Cybersecurity and Identity-Stack Validation Requirements

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Standalone Head-Mounted Displays

- 5.1.1.2 Tethered Head-Mounted Displays

- 5.1.1.3 Controllers, Trackers, and Peripherals

- 5.1.1.4 Haptics and Accessories

- 5.1.2 Software

- 5.1.2.1 Content Authoring and Scenario Design

- 5.1.2.2 Content Management and Delivery Platforms

- 5.1.2.3 Analytics and Assessment Software

- 5.1.2.4 LMS and HRIS Integration Software

- 5.1.3 Services

- 5.1.3.1 Custom Content Development

- 5.1.3.2 Implementation and Systems Integration

- 5.1.3.3 Managed Device and Program Operations

- 5.1.3.4 Support and Maintenance

- 5.1.1 Hardware

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Training Type

- 5.4.1 Safety and Compliance Training

- 5.4.2 Technical and Operational Training

- 5.4.3 Soft Skills and Leadership Training

- 5.4.4 Sales and Customer Interaction Training

- 5.4.5 Onboarding and Employee Orientation

- 5.4.6 Equipment Simulation and Maintenance Training

- 5.5 By End User Industry Vertical

- 5.5.1 Industrial Manufacturing

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Retail and Ecommerce

- 5.5.4 Energy and Utilities

- 5.5.5 Transportation and Logistics

- 5.5.6 BFSI

- 5.5.7 Construction and Engineering

- 5.5.8 Government, Defense, and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Nigeria

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Strivr Labs, Inc.

- 6.4.2 VRdirect GmbH

- 6.4.3 PixoVR, Corp.

- 6.4.4 Transfr Inc.

- 6.4.5 Virti Inc.

- 6.4.6 Mursion, Inc.

- 6.4.7 Osso VR, Inc.

- 6.4.8 Oxford Medical Simulation Ltd.

- 6.4.9 FVRVS Limited, trading as FundamentalXR

- 6.4.10 Pixaera Inc.

- 6.4.11 JCR Group Ltd, trading as Bodyswaps

- 6.4.12 3spin Learning GmbH & Co. KG

- 6.4.13 TLN Training Limited, trading as Gemba

- 6.4.14 WorldViz, Inc.

- 6.4.15 SimX, Inc.

- 6.4.16 Interplay Learning, Inc.

- 6.4.17 Humulo Virtual Reality Inc.

- 6.4.18 Skillveri Training Solutions Pvt Ltd.

- 6.4.19 Moth+Flame, Inc.

- 6.4.20 Innoactive GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment