|

시장보고서

상품코드

2065538

직원 온보딩용 신원 확인 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Identity Verification For Employee Onboarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

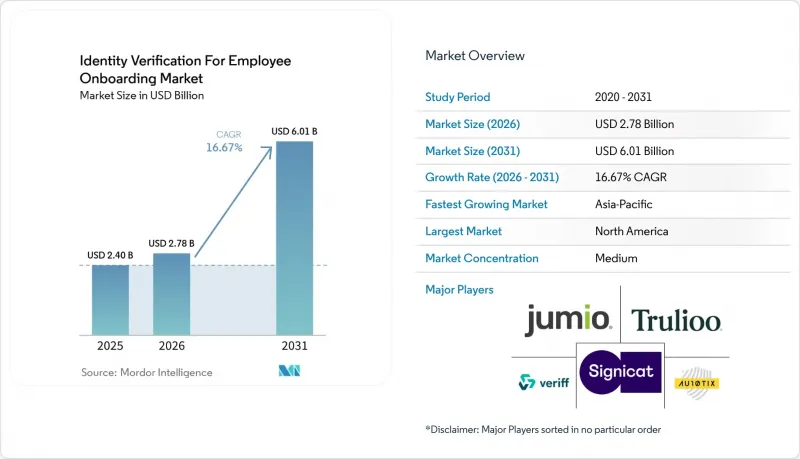

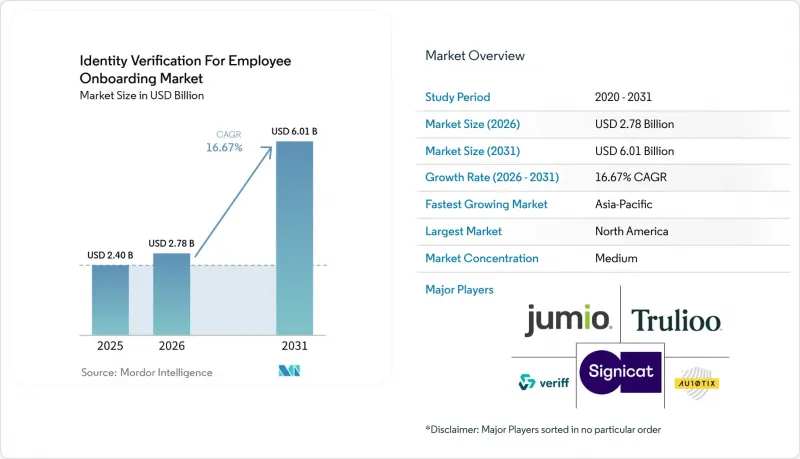

Mordor Intelligence에 의하면, 직원 온보딩용 신원 확인 시장 규모는 2025년 24억 달러로 평가되었습니다. 2026년에는 27억 8,000만 달러로 확대되어 2031년까지 60억 1,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 16.67%로 성장할 전망입니다.

본 보고서는 제공 내용(솔루션, 서비스), 배포 방식(클라우드 기반, 하이브리드 등), 기업 규모(대기업 등), 검증 방식(서류·자격 정보 확인 등), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 의료 및 생명과학 등), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 직원 온보딩용 신원 확인 시장 동향 및 인사이트

후보자 사칭 및 합성 신분증, 그리고 내부 부정 행위의 위험 증가

원격 업무 프로세스로 인해 부정 지원자가 대면 신원 확인 절차 없이 고용주와 접촉할 수 있게 되면서, 채용 절차는 직원 교육용 신원 인증 시스템에 대한 명백한 공격 대상이 되고 있습니다. 현재 조직적인 수법은 후보자 사칭, 가짜 신분증, 내부자의 부정 행위, 심지어 유령 채용 활동에까지 이르러 있으며, 이는 직원이 1차 심사 단계를 통과했다고 해서 위험이 사라지는 것은 아니라는 것을 의미합니다. 단 5분 만에 생성되는 AI 기반 피싱 공격은 사람이 수작업으로 만든 공격에 비해 4배 이상의 효과를 발휘합니다. 이 사실은 고용주들이 악의적인 사람들이 채용 전후의 소통을 얼마나 쉽게 조작할 수 있는지를 재평가하고 있는 이유를 설명해 줍니다. 이러한 위협 양상으로 인해 구매 결정의 범위가 확대되고 있습니다. 왜냐하면 신원 확인은 더 이상 입사 첫날의 온보딩뿐만 아니라, 급여 변경, 기기 등록, 인증 정보 복구, 특권 액세스 제어까지 지원해야 하기 때문입니다. 따라서 직원 온보딩용 신원 확인 시장에서는 단일 워크플로우 내에서 서류, 생체 인증, 생체 감지, 행동 연동형 제어를 다층적으로 결합한 솔루션에 대한 수요가 증가하고 있습니다. 또한, 채용 단계에서 ‘그 시점의 합격’만으로는 기업의 보안팀을 만족시킬 수 없게 되었기 때문에 지속적인 재확인을 지원할 수 있는 벤더가 유리한 입장에 서게 되었습니다.

원격 및 하이브리드 근무 방식의 확대

원격 및 하이브리드 근무 방식로의 영구적인 전환에 따라, 직원 교육을 위한 ID 인증의 잠재 시장은 계속해서 확대되고 있습니다. 이는 고용주가 대규모 대면 사무실 방문이나 서류 검사에 더 이상 의존할 수 없게 되었기 때문입니다. 또한, 분산형 채용은 인재 확보, 채용 담당자, IT, 컴플라이언스 팀 간의 업무 인계 과정에서 격차를 초래하여, 사기 집단이 프로세스의 관리 미비를 악용할 여지를 넓히고 있습니다. Checkr사는 2026년 3월에 IDV 제품을 출시했습니다. 이 제품에는 생체 감지, 문서 감식 분석, 디바이스 및 네트워크 인텔리전스가 채용 프로세스의 초기 단계에 통합되어 있어, 각 벤더들이 신원 확인을 후보자와의 첫 접점 시점으로 앞당기려 하고 있음을 보여줍니다. 또한, 원격 채용이 보편화됨에 따라 고용주가 동일한 인물을 확인하는 빈도도 증가하고 있습니다. 이는 계약직 직원의 재고용, 마켓플레이스에서의 업무, 그리고 반복되는 인력 배치 주기에서 과거의 단일 확인이 아닌 새로운 확인이 필요하기 때문입니다. 이러한 추세는 공급업체의 비즈니스 모델을 변화시키고 있습니다. 고용주가 직원의 전체 생애 주기에 걸친 신원 확인을 원할 경우, 거래별 과금 모델은 매력이 떨어지기 때문입니다. 직원 연수를 위한 ID 인증 시장은 이러한 변화의 혜택을 누리고 있습니다. 왜냐하면 구독형이나 플랫폼형 가격 책정은 일회성 서류 심사 수수료보다 지속적인 확인에 더 적합하기 때문입니다.

개인정보, 생체 인증에 대한 동의 및 데이터 저장 위치에 관한 제한 사항

개인정보보호법은 직원 온보딩용 신원 확인 시장 도입에 있어 여전히 가장 명확한 제약 요인 중 하나입니다. 왜냐하면, 가장 강력한 부정 방지 대책은 대부분의 경우 얼굴 생체 인증, 생체 감지, 그리고 장기간 보관되는 본인 확인 기록에 의존하고 있기 때문입니다. 일리노이주 BIPA(개인정보보호법)에 따르면, 2026년 4월 제7순회항소법원의 판결로 인해 일부 피고에 대한 과거 스캔 건별 법적 위험이 완화된 이후에도 여전히 엄격한 서면 동의, 보존 기간 및 파기 방침이 요구되고 있습니다. GDPR(EU 개인정보보호규정) 제9조에서는 고유한 식별을 목적으로 사용되는 생체 인식 데이터를 ‘특별 범주의 데이터’로 취급하고 있습니다. 이는 유럽의 고용주들이 이를 도입하기 전에 더 엄격한 법적 근거와 절차 설계 요건을 충족해야 함을 의미합니다. EU AI법은 또 다른 요건을 추가하고 있으며, 생체 인식 시스템은 고위험 의무의 대상이 될 가능성이 있어 공급업체나 고용주의 규정 준수 부담이 커질 우려가 있습니다. 인도의 데이터 보호 제도와 중국의 『개인정보보호법(PIPL)』 역시 전 세계적인 사업 확장을 어렵게 만들고 있습니다. 다국적 기업은 규정 준수를 유지하기 위해 지역별 인프라, 현지 데이터 처리 방침, 그리고 개별적인 법적 업무 절차가 필요한 경우가 많기 때문입니다. 이러한 법적 및 운영상의 부담은 도입 주기를 지연시키고 총 소유 비용을 상승시키며, 일부 고용주가 전체 직원에 대한 채용 과정 전반이 아닌 고위험 직책으로만 생체 인증의 활용을 제한하는 요인이 되고 있습니다.

부문별 분석

2025년, 이 솔루션은 직원 온보딩용 신원 확인 시장의 72.12%를 차지했습니다. 이는 서류 확인, 생체 인증 대조, 생체 감지, 워크플로우 조정, 규정 준수 보고를 단일 엔터프라이즈 제품에 통합한 SaaS 플랫폼의 지속적인 강점을 반영합니다. 또한 이 조사 결과는 신원 확인이 채용, 급여 계산, 접근 관리 시스템 등 서로 다른 사업 부문에 걸쳐 연계되어야 하는 경우에도 구매자들이 여전히 설정 가능한 소프트웨어 기반 제어 방식을 선호한다는 점을 보여줍니다. 플랫폼 기반 제공 방식은 예외 사례마다 수동 심사 팀에 의존하지 않고, 직접적인 API 접근, 정책 설정, 내부 거버넌스 관리 및 통합된 감사 기록을 원하는 고용주에게 효과적입니다. 이러한 솔루션의 장점은 대기업의 요구 사항과도 부합합니다. 대기업은 대개 소수의 주요 보안 및 인사 플랫폼을 표준화하고 있으며, 신원 확인 관리를 독립된 업무로 외부에 위탁하기보다는 해당 시스템에 통합하기를 원합니다. 직원 온보딩용 신원 확인 시장에서 이러한 구조는 동일한 스택 내에서 광범위한 문서 라이브러리, 국경을 초월한 채용 워크플로우, 그리고 엔터프라이즈급 보고 기능을 지원할 수 있는 공급업체에게 유리하게 작용합니다.

구매자들이 단순한 소프트웨어 접근 권한이 아닌, 검증된 성과, 최신 규정 준수 로직, 그리고 체계적으로 관리되는 부정 방지 업무를 점점 더 요구함에 따라, 서비스 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 17.71%로 확대될 것으로 전망됩니다. 전담 신원 확인 팀을 갖추지 않은 채, 템플릿 업데이트, 규칙 조정, 예외 처리 및 관할 구역을 넘나드는 정책 변경에 대한 지원이 필요한 고용주들 사이에서 관리형 신원 확인 워크플로가 주목받고 있습니다. 이는 특히 중견 기업에서 두드러지는데, 채용 규모가 위험에 노출될 만큼 크지만, 사내에 전문적인 신원 확인 운영 부서를 설치할 만큼 규모가 크지는 않은 경우가 이에 해당합니다. 또한, 서비스 부문도 지속적인 수익원으로 자리 잡고 있습니다. 이는 자문 계약, 규정 준수 모니터링, 지속적인 워크플로우 최적화가 초기 도입 단계를 훨씬 넘어 확대되고 있기 때문입니다. 이러한 추세가 강화됨에 따라, 직원 온보딩용 신원 확인 시장에서는 소프트웨어 라이선싱과 서비스 제공의 경계가 점차 모호해지고 있습니다. 과거에는 개별 제품을 판매하던 벤더들이 장기적인 관리형 서비스를 기반으로 한 관계를 구축하는 사례가 늘어나고 있으며, 이에 따라 수익 구조, 고객 유지율, 그리고 기업의 구매 담당자가 공급업체를 비교하는 기준이 변화하고 있습니다.

2025년에는 클라우드 기반 솔루션이 시장 점유율의 69.41%를 차지했으며, 이는 직원 온보딩용 신원 확인 시장이 현대의 HR, 급여 계산, 채용 시스템으로 구성된 광범위한 SaaS 아키텍처와 얼마나 밀접하게 연계되어 있는지를 여실히 보여주고 있습니다. 클라우드를 통한 제공은 문서 템플릿의 신속한 업데이트, 부정 신호의 실시간 개선, 채용 급증 시의 유연한 처리, 지리적으로 분산된 팀에 대한 손쉬운 배포를 가능하게 함으로써 채용 워크플로우와 조화를 이룹니다. 또한, 많은 조직이 이미 온보딩, 심사, 접근 권한 부여를 클라우드에서 수행하고 있기 때문에 이는 고용주가 ATS(채용 관리 시스템)나 HRIS(인사 정보 시스템) 소프트웨어를 구매하는 방식과도 부합합니다. 이러한 장점들, 특히 속도, 표준화, 그리고 사내 IT 부담 경감이 인프라에 대한 세부적인 통제보다 더 중요하게 여겨지는 경우, 클라우드 도입은 대부분의 고용주에게 기본적인 선택지가 되고 있습니다. 클라우드 도입은 공급업체와 고객 양측의 온보딩 과정에서 발생하는 마찰을 줄여주기 때문에 직원 온보딩용 신원 확인 시장은 이러한 추세로 인해 계속해서 혜택을 보고 있습니다.

하이브리드 업무 환경에서의 직원 온보딩용 신원 확인 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 16.73%로 확대될 것으로 전망됩니다. 이는 클라우드 기반의 신원 확인 인텔리전스를 활용하면서도 기밀 데이터에 대한 보다 강력한 관리를 요구하는 규제 대상 고용주들에 의해 주도되고 있습니다. 하이브리드 모델은 특정 기록이나 워크플로를 통제된 환경 내에 유지하고자 하는 금융 기관, 정부 계약업체, 의료 시스템에 매력적인 선택지입니다. 또한, GDPR(EU 개인정보보호규정)과 관련된 데이터 처리 요건, HIPAA와 관련된 직원 채용에 대한 우려, 그리고 보호 대상 정보를 규정하는 내부 보안 규정에 대응해야 하는 기업들에게 타협점을 마련해 주는 대안을 제시합니다. On-Premise 배포는 국방 분야, 공공 부문, 그리고 엄격하게 제한된 환경과 같은 제한된 분야에서는 여전히 중요하지만, 큰 시장 점유율을 확보할 가능성은 낮을 것으로 보입니다. 따라서 하이브리드 모델의 성장은 기존 아키텍처로의 회귀라기보다는 현실적인 타협점을 반영한 것입니다. 이를 통해 고용주는 현지에서의 데이터 거버넌스와, 사내에서 유지하기 어려운 클라우드 규모의 대조, 문서 분석, 그리고 부정 감지 모델 업데이트를 결합할 수 있게 됩니다.

지역별 분석

2025년, 북미는 직원 연수를 위한 신원 인증 시장 점유율의 39.71%를 차지하며, 고용 적격성에 관한 규정과 생체 인증의 개인정보 보호 요건이 더욱 적극적으로 적용되고 강제력이 있기 때문에 다른 지역을 확실히 앞서 나갔습니다. 미국은 광범위한 수요 기반을 제공합니다. 이는 미국에 거점을 둔 직원을 단 한 명이라도 채용하는 고용주는 온보딩 절차의 일환으로 신원 확인 및 취업 자격 심사를 완료해야 하기 때문입니다. 이러한 요건에 따라, 직원의 신원 확인은 일부 규제 대상 고용주에게만 국한된 틈새 관리 조치가 아니라, 일반적인 업무상 필요 사항이 되었습니다. 일리노이주의 BIPA로 대표되는 주 차원의 생체 인증 관련 법안 역시 동의, 데이터 보존, 감사 설계의 중요성을 강조하고 있으며, 이에 따라 공급업체들은 규정 준수를 위한 워크플로우 기능을 판매할 여지가 더욱 확대되고 있습니다. 유럽은 eIDAS 2.0 계획과 지갑형 디지털 ID 생태계에 대한 고용주들의 관심에 힘입어, 직원 온보딩용 신원 확인 시장에서 여전히 2위 지역 블록으로서의 위상을 유지하고 있습니다. 영국의 ‘디지털 신원 및 속성 신뢰 프레임워크(Digital Identity and Attributes Trust Framework)’는 고용주를 대신해 취업 자격 확인을 수행하는 제공업체를 위한 공인 인증 경로를 정의함으로써 실질적인 추진력을 제공했습니다.

아시아태평양의 직원 온보딩용 신원 확인 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 18.41%로 확대될 것으로 예상되며, 이 지역은 예측 기간 동안 가장 강력한 성장 동력이 될 전망입니다. 일본은 이러한 전망에서 중심적인 역할을 하고 있습니다. 2025년 12월까지 마이넘버 카드 발급 건수가 1억 장을 돌파하고, 인구 대비 보급률이 80%를 넘어서면서, 고용주는 공식적인 본인 확인 절차를 위한 훨씬 더 견고한 디지털 인증 기반을 확보하게 되었기 때문입니다. 또한, 디지털청이 2026년 2월에 발표한 지침에 따라 JPKI(일본전자인증기구)에 기반한 본인 확인이 민간 고용 분야로도 확대되면서, 디지털 ID가 채용 업무의 주류로 한 걸음 더 다가섰습니다. 2026년 3월, 데마에 캔은 배달 기사 등록에 NEC의 금융 등급 신원 확인 서비스를 도입했습니다. 이는 긱 노동이나 플랫폼 노동이 단순한 예외적인 사례가 아니라 중요한 수요원이 되어가고 있음을 보여줍니다. 인도와 한국 역시 디지털 ID 인프라, 핀테크 분야의 인재 수요, 그리고 원격 및 국경을 초월한 채용 환경에서 강화된 규정 준수 요건에 힘입어, 직원 온보딩용 신원 확인 시장에서 그 중요성이 커지고 있습니다.

남미, 중동 및 아프리카는 2026년 시점에서 아직 초기 단계에 머물러 있었으나, 직원 연수를 위한 ID 인증 시장은 이들 지역에서도 보다 명확한 장기적 기회 기반을 구축해 나가고 있습니다. 현재 상황에서 남미에서 가장 발전한 시장은 브라질이며, Jumio사는 2025년 10월 브라질에서 ‘selfie.DONE’을 처음 출시한 후, 2026년 4월에 남미 전역으로 사업을 확대했습니다. 사우디아라비아와 아랍에미리트에서는 광범위한 경제 현대화와 금융 서비스, 건설, 호텔·관광 분야의 확대에 발맞춘 디지털 인재 인프라 프로그램을 통해 수요가 발생하고 있습니다. 아프리카에서는 남아프리카공화국과 나이지리아가 두드러집니다. 핀테크 중심의 채용 활동과 모바일 통신 환경의 개선으로 인해, 생체 인증 및 생체 감지를 기반으로 한 온보딩을 대규모로 실시하기 위한 실질적인 여건이 점차 갖춰지고 있기 때문입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the identity verification for employee onboarding market size is expected to increase from USD 2.40 billion in 2025 to USD 2.78 billion in 2026 and reach USD 6.01 billion by 2031, growing at a CAGR of 16.67% over 2026-2031.

This report is Segmented by Offering (Solutions, and Services), Deployment Model (Cloud-Based, Hybrid, and More), Enterprise Size (Large Enterprises, and More), Verification Method (Document and Credential Verification, and More), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Identity Verification For Employee Onboarding Market Trends and Insights

Escalating Candidate Impersonation, Synthetic Identity, and Insider Fraud Risks

Hiring pipelines have become a visible attack surface for identity verification for the employee onboarding market, because remote workflows let fraudulent applicants reach employers without any physical identity touchpoint. Organized schemes now span candidate impersonation, synthetic identities, insider fraud, and ghost-hire activity, which means the risk no longer ends once a worker clears the first screening step. AI-generated phishing attacks created in 5 minutes are more than 4 times as effective as human-crafted attacks, which helps explain why employers are reassessing how easily bad actors can manipulate pre-hire and post-hire interactions. This threat pattern is widening the scope of buying decisions, because identity verification now needs to support payroll changes, device enrollment, credential recovery, and privileged access controls rather than only day-one onboarding. The identity verification for employee onboarding market is therefore seeing stronger demand for layered document, biometric, liveness, and behavior-linked controls in a single workflow. That shift is also favoring vendors that can support continuous reverification, since a point-in-time pass at the hiring stage no longer satisfies enterprise security teams.

Growth In Remote and Hybrid Hiring Workflows

The permanent shift to remote and hybrid hiring continues to expand the addressable market for identity verification in employee onboarding, as employers cannot rely on in-person office visits or document inspection at scale. Distributed recruiting also creates handoff gaps across talent acquisition, hiring managers, IT, and compliance teams, giving fraud rings more room to exploit weak ownership of the process. Checkr launched its IDV product in March 2026, with liveness detection, forensic document analysis, and device and network intelligence built into the early hiring flow, demonstrating how vendors are moving identity checks closer to the first candidate touchpoint. Remote hiring has also increased the frequency with which employers verify the same person, because contractor re-engagement, marketplace work, and repeat staffing cycles now trigger new checks rather than a single historical verification. That pattern is changing vendor economics, since per-transaction models become less attractive when employers want identity coverage across the full workforce lifecycle. The identity verification market for employee onboarding is benefiting from this shift, because subscription and platform pricing better align with recurring verification than one-off document-review fees.

Privacy, Biometric Consent, and Data Residency Constraints

Privacy law remains one of the clearest limits on adoption in the identity verification for employee onboarding market, because the strongest fraud controls often depend on facial biometrics, liveness checks, and long-lived identity records. Illinois BIPA still requires strict written consent, retention schedules, and destruction policies, even after the April 2026 Seventh Circuit ruling reduced historical per-scan exposure for some defendants. GDPR Article 9 treats biometric data used for unique identification as special-category data, which means employers in Europe face tighter legal bases and process design requirements before deployment. The EU AI Act adds another layer, as biometric identification systems may fall under high-risk obligations that increase compliance burdens for vendors and employers. India's data protection regime and China's PIPL also make global rollout harder, as multinational employers often need regional infrastructure, local data-handling policies, and separate legal workflows to remain compliant. These legal and operational burdens slow conversion cycles, raise total ownership costs, and lead some employers to limit biometric use to higher-risk roles rather than broad workforce onboarding.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Right-To-Work, Employment Eligibility, and Workforce Compliance Requirements

- Rising Adoption Of Biometric and Liveness Verification In Digital Onboarding

- Integration Complexity Across Legacy HR, ATS, And Compliance Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 72.12% of the identity verification for employee onboarding market share in 2025, which reflects the continued strength of SaaS platforms that bundle document verification, biometric matching, liveness checks, workflow orchestration, and compliance reporting into a single enterprise product. This lead also shows that buyers still prefer configurable software control when identity verification must connect with recruiting, payroll, and access management systems across different business units. Platform-based delivery works well for employers that want direct API access, policy configuration, internal governance controls, and centralized audit records without depending on a manual review team for every exception. The dominance of solutions also aligns with the needs of large enterprises, which often standardize on a few core security and HR platforms and want identity controls embedded in those systems rather than outsourced as isolated tasks. In the identity verification for employee onboarding market, this structure favors vendors that can support broad document libraries, cross-border hiring workflows, and enterprise-grade reporting inside the same stack.

Services are projected to expand at a 17.71% CAGR from 2026 to 2031, as buyers increasingly seek verified outcomes, updated compliance logic, and managed fraud operations, rather than just software access. Managed verification workflows are gaining traction among employers that lack dedicated identity teams and need help with template updates, rule tuning, exception handling, and policy changes across jurisdictions. This is especially relevant in the mid-market, where hiring volumes can be high enough to create risk exposure but not large enough to justify a specialized internal identity operations function. The service layer is also becoming more recurring, because advisory retainers, compliance monitoring, and ongoing workflow optimization now extend well beyond initial implementation. As that pattern grows, the identity verification for employee onboarding market is narrowing the line between software licensing and service delivery. Vendors that once sold point products are increasingly building long-term managed relationships, which changes revenue mix, customer stickiness, and the basis on which enterprise buyers compare providers.

Cloud-based deployments accounted for 69.41% of the market share in 2025, underscoring how closely the identity verification for employee onboarding market aligns with the broader SaaS architecture of modern HR, payroll, and recruiting systems. Cloud delivery aligns with hiring workflows by enabling fast updates to document templates, real-time improvements to fraud signal, elastic processing during recruitment surges, and easier rollout across geographically dispersed teams. It also aligns with how employers buy ATS and HRIS software, since many organizations already run onboarding, screening, and access provisioning in the cloud. These advantages make cloud deployment the default option for most employers, especially where speed, standardization, and lower internal IT burden matter more than deep infrastructure control. The identity verification market for employee onboarding continues to benefit from this bias, as cloud deployment reduces onboarding friction for both vendors and customers.

The identity verification market for employee onboarding in hybrid deployments is projected to expand at a 16.73% CAGR from 2026 to 2031, driven by regulated employers seeking stronger control over sensitive data while still leveraging cloud-based verification intelligence. Hybrid models appeal to financial institutions, government contractors, and healthcare systems that want certain records and workflows to remain inside controlled environments. They also provide a middle path for companies responding to GDPR-related data-handling requirements, HIPAA-linked workforce onboarding concerns, and internal security rules governing protected information. On-premises deployment remains relevant for a narrower set of defense, public-sector, and highly restricted environments, but it is unlikely to gain a significant share. Hybrid growth, therefore, reflects a practical compromise rather than a return to legacy architecture. It lets employers combine local data governance with cloud-scale matching, document analysis, and fraud model updates that would be harder to maintain internally.

Geography Analysis

North America held 39.71% of the identity verification for employee onboarding market share in 2025, keeping it firmly ahead of other regions because employment eligibility rules and biometric privacy requirements are both more active and enforceable there. The United States provides a broad structural base for demand, since any employer with even 1 U.S.-based hire must complete identity and work authorization checks as part of onboarding. That requirement makes workforce identity verification a common operational need rather than a niche control reserved for a few regulated employers. State-level biometric laws, led by Illinois BIPA, also raise the importance of consent, retention, and audit design, which gives vendors more room to sell compliance-ready workflow features. Europe remained the second-largest regional block in the identity verification for employee onboarding market, supported by eIDAS 2.0 planning and employer interest in wallet-based digital identity ecosystems. The United Kingdom's Digital Identity and Attributes Trust Framework added practical momentum by defining a recognized certification route for providers that perform right-to-work checks for employers.

The identity verification for employee onboarding market size in Asia-Pacific is projected to expand at 18.41% CAGR from 2026 to 2031, which makes the region the strongest growth engine over the forecast period. Japan is central to that outlook, because My Number Card circulation passed 100 million cards and exceeded 80% population penetration by December 2025, giving employers a much stronger digital credential base for formal identity workflows. The Digital Agency's February 2026 guidance then extended JPKI-based verification into private employment settings, which moved digital identity closer to mainstream hiring operations. Demae-can adopted NEC's financial-grade identity verification service for delivery driver registration in March 2026, showing that gig and platform labor is becoming a meaningful demand pool rather than a side case. India and South Korea are also becoming more important in the identity verification for employee onboarding market, supported by digital identity infrastructure, fintech staffing needs, and tighter compliance expectations in remote and cross-border hiring environments.

South America, the Middle East, and Africa remained earlier-stage regions in 2026, but the identity verification for employee onboarding market is building a clearer long-term opportunity base there. Brazil is the most developed South American market in the current mix, and Jumio expanded selfie.DONE across South America in April 2026 after first launching it in Brazil in October 2025. Saudi Arabia and the United Arab Emirates are generating demand through digital workforce infrastructure programs tied to broader economic modernization and sector expansion in financial services, construction, and hospitality. In Africa, South Africa and Nigeria stand out because fintech-led hiring and improving mobile connectivity are creating more workable conditions for biometric and liveness-based onboarding at scale.

- Jumio Corporation

- Veriff OU

- Trulioo Information Services Inc.

- IDnow GmbH

- Persona Identities, Inc.

- Yoti Limited

- Sum and Substance Ltd.

- AuthenticID, Inc.

- Incode Technologies, Inc.

- Signicat AS

- Innovatrics, s.r.o.

- PXL Vision AG

- Shufti Pro Limited

- HyperVerge Technologies Private Limited

- IDfy Technologies Private Limited

- iDenfy UAB

- Ondato UAB

- ComplyCube Limited

- Socure Inc.

- Zenoo Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth In Remote And Hybrid Hiring Workflows

- 4.2.2 Stricter Right-To-Work, Employment Eligibility, And Workforce Compliance Requirements

- 4.2.3 Escalating Candidate Impersonation, Synthetic Identity, And Insider Fraud Risks

- 4.2.4 Rising Adoption Of Biometric And Liveness Verification In Digital Onboarding

- 4.2.5 Reusable Digital Identity Wallets For Repeat Workforce Onboarding

- 4.2.6 ATS And HRIS Embedding Of Identity APIs For High-Volume Hiring

- 4.3 Market Restraints

- 4.3.1 Privacy, Biometric Consent, And Data Residency Constraints

- 4.3.2 Integration Complexity Across Legacy HR, ATS, And Compliance Systems

- 4.3.3 False Reject Risk In Tight Labor Markets

- 4.3.4 Jurisdiction-Specific Employment Document Rules Limiting Global Standardization

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact Of Macroeconomic Factors On The Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat Of New Entrants

- 4.8.2 Bargaining Power Of Buyers

- 4.8.3 Bargaining Power Of Suppliers

- 4.8.4 Threat Of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By Verification Method

- 5.4.1 Document And Credential Verification

- 5.4.2 Biometric Verification

- 5.4.3 Database And Identity Network Verification

- 5.4.4 Liveness And Deepfake Detection

- 5.4.5 Video And Assisted Verification

- 5.4.6 Reusable Identity And Wallet Verification

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Jumio Corporation

- 6.4.2 Veriff OU

- 6.4.3 Trulioo Information Services Inc.

- 6.4.4 IDnow GmbH

- 6.4.5 Persona Identities, Inc.

- 6.4.6 Yoti Limited

- 6.4.7 Sum and Substance Ltd.

- 6.4.8 AuthenticID, Inc.

- 6.4.9 Incode Technologies, Inc.

- 6.4.10 Signicat AS

- 6.4.11 Innovatrics, s.r.o.

- 6.4.12 PXL Vision AG

- 6.4.13 Shufti Pro Limited

- 6.4.14 HyperVerge Technologies Private Limited

- 6.4.15 IDfy Technologies Private Limited

- 6.4.16 iDenfy UAB

- 6.4.17 Ondato UAB

- 6.4.18 ComplyCube Limited

- 6.4.19 Socure Inc.

- 6.4.20 Zenoo Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment