|

시장보고서

상품코드

2065572

ERP 컨설팅 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Enterprise Resource Planning Consulting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

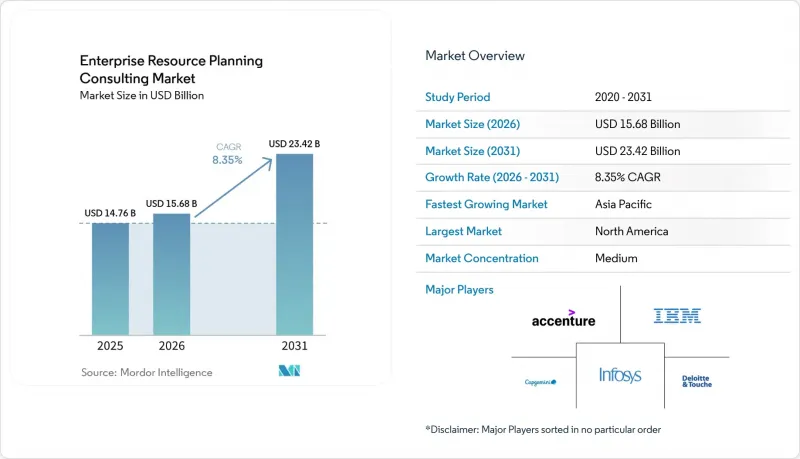

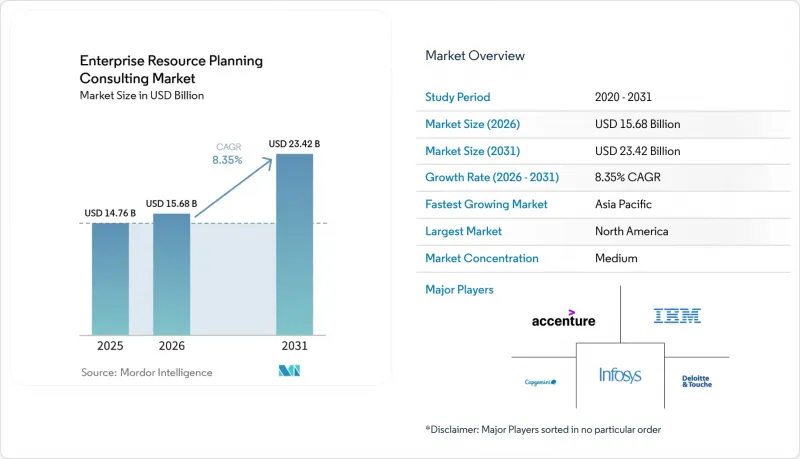

Mordor Intelligence에 의하면, ERP 컨설팅 시장 규모는 2025년에 147억 6,000만 달러로 평가되었고, 2026년에 156억 8,000만 달러로 추정되고, 2031년까지 234억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 8.35%로 성장할 전망입니다.

본 보고서는 배포 방식별(온프레미스, 클라우드, 하이브리드), 기업 규모별(중소기업, 대기업), 최종 사용자 산업별(제조, 은행, 금융서비스 및 보험(BFSI), 소매 및 전자상거래, 의료, 정부 및 공공 부문, IT 및 통신, 에너지 및 유틸리티 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 ERP 컨설팅 시장 동향 및 인사이트

중소기업에서의 클라우드 네이티브 ERP 수요

중소기업은 구독형 가격 책정을 통해 비용을 수익 주기에 맞출 수 있고, 온프레미스형 인프라의 부담이 줄어들기 때문에 클라우드 플랫폼 도입을 추진하고 있습니다. Workday는 캐나다 내 클라우드 ERP 시장 확대를 위해 10억 캐나다 달러(7억 7,000만 달러)를 투자했으며, 그동안 초급 수준의 회계 도구에 의존해 온 직원 수 500-5,000명의 기업을 주요 타겟으로 삼고 있습니다. 각 컨설팅 파트너사는 사전에 설정된 템플릿을 제공함으로써 마이그레이션 기술 부족을 보완하고, 가동 개시까지의 기간을 18개월에서 6개월 미만으로 단축하고 있습니다. SAP는 자사의 RISE 프로그램을 통해 2024년 4분기 아시아태평양(APAC)에서 수주한 프로젝트의 60%를 중소기업이 차지했다고 밝혔습니다. 유럽의 부티크형 컨설팅 회사에서는 데이터 정제 및 GDPR(EU 개인정보보호규정) 준수를 위한 데이터 소재지 관리 서비스에 대한 수요가 증가하고 있습니다.

컴포저블 ERP 아키텍처로의 전환

기업들은 모놀리식 제품군을 API로 연결된 구성 요소로 분해하고, 재무, 공급망, 인사 각 모듈을 개별적으로 업그레이드할 수 있도록 함으로써 벤더 종속의 위험을 줄이고 있습니다. 은행들은 고객용 채널을 핵심 원장 시스템에서 분리함으로써 상품 출시를 가속화하고 있습니다. 소매업체들은 MuleSoft나 Boomi의 미들웨어를 통해 SAP의 재무 모듈과 Blue Yonder의 재고 관리 엔진을 연동함으로써, 통합 중심의 컨설팅에 대한 수요를 창출하고 있습니다. 딜로이트와 캡제미니는 API를 자동으로 매핑하는 독자적인 가속기를 판매하며, 설계 단계의 단축을 도모하고 있습니다. 구성 가능성은 통합된 데이터 계층 아래에서 여러 ERP 시스템이 공존해야 하는 합병 시에도 유용하지만, 마스터 데이터 거버넌스에서의 불일치가 스튜어드십 프레임워크에 관한 자문 프로젝트의 계기가 되고 있습니다.

인증 ERP 컨설턴트의 부족

SAP S/4HANA, Oracle Fusion Cloud, Microsoft Dynamics 365 관련 기술에 대한 수요가 공급을 웃돌고 있어, 급여 수준 상승과 프로젝트 기간 연장을 초래하고 있습니다. SAP는 2024년에 인증된 S/4HANA 컨설턴트가 30% 부족할 것이라고 보고했습니다. 인도의 해외 연수 프로그램은 연간 1만 5,000명의 전문가를 인증하는 것을 목표로 하고 있지만, 20-25%에 달하는 이직률로 인해 인재들이 하이퍼스케일러의 클라우드 부문으로 유출되고 있습니다. 라틴아메리카와 아프리카에서는 현지에 파견되는 인력에 의존하고 있으며, 이로 인해 프로젝트 비용이 최대 40% 증가하고 있습니다. 로우코드 액셀러레이터는 설정 작업의 부담을 줄여주지만, 소규모 전문 기업들은 독자적인 지적 재산(IP)에 대규모 투자를 할 자금이 없습니다.

부문별 분석

2025년, 클라우드 솔루션은 ERP 컨설팅 시장의 58%를 차지한 것으로 평가되었으며, 이 부문은 2031년까지 연평균 성장률(CAGR) 12.40%로 성장할 것으로 전망됩니다. 이 성장률은 ERP 컨설팅 시장 전체보다 4% 높은 수치로, 자본 집약적인 데이터센터에서 벗어나는 결정적인 전환을 반영하고 있습니다. 각 하이퍼스케일러 기업들은 인프라, 마이그레이션, 1년간의 관리형 지원 서비스를 단일 청구서로 통합하여 영향력을 확대하고 있으며, 이로 인해 가격 및 책임성 측면에서 독립 자문사들이 어려움을 겪고 있습니다. ITAR(국제무기거래규정)의 적용을 받는 방위 관련 계약업체나, 검증된 제조 실행 시스템을 온프레미스로 유지해야 하는 제약 공장 사이에서는 하이브리드 모델이 여전히 자리 잡고 있습니다.

분기별 SaaS 릴리스에는 회귀 테스트, 변경 관리, 기능 활성화가 필요하기 때문에 지속적인 최적화 워크스트림이 형성되고 있습니다. 컨설턴트는 현재 프로젝트 기반의 로드맵이 아닌, 지속적인 DevOps 방식의 구독 서비스를 판매하고 있으며, 이를 통해 고객 생애 가치를 미묘하게 높이고 있습니다. 온프레미스 환경이 축소되는 추세임에도 불구하고, 기업들이 단계적으로 맞춤형 설정을 해제해 나가는 과정에서 API 계층을 도입하고 모듈을 단계적으로 폐지함으로써 여전히 자문 수익을 창출하고 있습니다. 하이브리드 환경의 연평균 성장률(CAGR)은 한 자릿수 중반 수준으로 예측되며, 이는 주권 감사 요건을 충족하면서도 프라이빗 클라우드와 퍼블릭 클라우드를 아우르는 안전한 통합 아키텍처에 대한 틈새 수요를 창출하고 있습니다.

지역별 분석

북미는 2025년 매출의 38%를 차지한 것으로 평가되었으며, 그 배경에는 의약품, 국방, 금융 분야의 엄격한 규제 체계가 있으며, 이러한 분야는 전문적인 통제 컨설팅이 필요합니다. 포춘 500대 기업의 합병은 조화 프로젝트를 촉진하는 한편, 미국에서 멕시코로의 니어쇼어링으로 인해 USMCA(미국·멕시코·캐나다 협정)의 원산지 규정에 관한 국경을 초월한 규정 준수 업무가 증가하고 있습니다. 캐나다는 하이퍼스케일러들의 투자를 유치하고 있으며, 그 예로 워크데이가 중견 제조업체를 대상으로 서비스를 제공하기 위해 10억 캐나다 달러(7억 7,000만 달러)를 투자해 사업을 확장한 것을 들 수 있습니다. 북미 고객사들이 인력 확충에 따른 공수보다 가치 실현을 우선시함에 따라, ERP 컨설팅 시장은 계속해서 성과 기반 계약으로 전환되고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 11.90%로 가장 빠르게 성장하고 있으며, 인도, 중국, 일본, 아세안(ASEAN) 시장 전반에서 클라우드 전환 계약을 수주하고 있습니다. SAP는 2024년 4분기 APAC 지역 수주 건의 60%가 RISE 번들을 통한 업그레이드를 진행하는 중소기업 관련 건이었다고 밝혔습니다. 인도에서는 전자기기 및 제약 분야의 생산 연계형 인센티브에 힘입어, 추적성 및 품질 감사 도입이 가속화되고 있습니다. 한편, 중국의 제조업체들은 ‘이중 순환’ 정책의 지침을 충족하기 위해 국내 기업인 Kingdee나 Yonyou의 플랫폼을 도입하고 있으며, 이로 인해 병행 통합 작업에 따른 부담이 발생하고 있습니다. 일본에서는 노동력의 고령화로 인해 인력 부족을 보완하기 위해 ERP 시스템과 RPA의 통합이 추진되고 있으며, 컨설팅 기업들은 봇 거버넌스 체계의 도입을 요구받고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)의 거주지 요건으로 인해 멀티테넌트형 클라우드 제공업체들이 현지화된 구역을 구축할 수밖에 없게 되었고, 이로 인해 국경을 넘는 사업 확장이 복잡해지며 프로젝트 범위 수립 주기가 장기화되면서 성장이 완만하게 그치고 있습니다. 독일, 영국, 프랑스에서는 ERP와 IoT 센서 데이터를 연동하는 ‘인더스트리 4.0’에 대한 투자가 지출을 견인하고 있는 반면, 남유럽에서는 EU의 보조금 프로그램과 액센츄어의 포르투갈 Fibermind사 인수를 배경으로 성장이 가속화되고 있습니다. 중동의 정부계 펀드는 이슬람 금융의 틀을 준수하면서, 자금 조달 및 세무 업무의 디지털화를 추진하는 정부의 현대화 프로젝트에 자금을 지원하고 있으며, 이를 통해 장기적인 컨설팅 계약을 유치하고 있습니다. 아프리카와 남미는 여전히 신흥 시장으로의 기회를 제공하고 있지만, 액센츄어의 시엔트라(Cientra) 인수를 계기로 브라질 제조업 및 광업 분야의 재편이 진행되면서 라틴아메리카의 프로젝트 수가 증가할 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the eRP consulting services market size is projected to be USD 14.76 billion in 2025, USD 15.68 billion in 2026, and reach USD 23.42 billion by 2031, growing at a CAGR of 8.35% from 2026 to 2031.

This report is Segmented by Deployment Mode (On-Premise, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises and Large Enterprises), End User Industry (Manufacturing, BFSI, Retail and E-Commerce, Healthcare, Government and Public Sector, IT and Telecom, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Resource Planning Consulting Market Trends and Insights

Cloud-Native ERP Demand Among SMEs

Small and medium enterprises are adopting cloud platforms because subscription pricing aligns costs with revenue cycles and removes the burden of on-premises infrastructure. Workday earmarked CAD 1 billion (USD 770 million) to expand Canadian cloud ERP capacity, targeting firms with 500-5,000 employees that previously relied on entry-level accounting tools. Consulting partners fill migration skill gaps by supplying pre-configured templates that cut go-live timelines from 18 months to fewer than six. SAP confirmed that SMEs represented 60% of its Q4 2024 APAC wins through its RISE program. Demand for data cleansing and GDPR-compliant residency services is growing across European boutique practices.

Shift to Composable ERP Architecture

Enterprises are decomposing monolithic suites into API-connected components that enable finance, supply chain, and HR modules to upgrade independently, reducing vendor lock-in risk. Banks separate customer-facing channels from core ledgers to launch products faster. Retailers pair SAP finance with Blue Yonder inventory engines via MuleSoft or Boomi middleware, creating demand for integration-centric consulting. Deloitte and Capgemini market proprietary accelerators that auto-map APIs, shortening design phases. Composability also aids mergers when multiple ERPs must coexist under a unified data layer, though inconsistencies in master-data governance spark advisory projects on stewardship frameworks.

Shortage of Certified ERP Consultants

Demand for SAP S/4HANA, Oracle Fusion Cloud, and Microsoft Dynamics 365 skills exceeds supply, elevating salaries and stretching project timelines. SAP recorded a 30% deficit in certified S/4HANA consultants during 2024. Offshore training pipelines in India aim to certify 15,000 specialists annually, yet attrition of 20-25% shifts talent to hyperscaler cloud divisions. Latin America and Africa rely on fly-in talent, which increases project costs by up to 40%. Low-code accelerators reduce configuration effort, but smaller boutiques cannot fund proprietary IP at scale.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Outcome-Based Consulting Contracts

- Post-Pandemic Digital Transformation Budgets Rebound

- Rising Cybersecurity Concerns Delaying Projects

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud solutions accounted for 58% of the ERP consulting services market in 2025, and the segment is projected to grow at a 12.40% CAGR through 2031. This growth surpasses the overall ERP consulting services market by four percentage points, reflecting a decisive shift away from capital-intensive data centers. Hyperscalers expand their influence by packaging infrastructure, migration, and 1-year managed support into a single invoice, challenging independent advisors on price and accountability. Hybrid models persist among defense contractors subject to ITAR and among pharmaceutical plants, where validated manufacturing execution systems must remain on-premises.

Recurring optimization work streams emerge because quarterly SaaS releases demand regression testing, change management, and feature enablement. Consultants now sell evergreen DevOps-style subscriptions rather than project-based roadmaps, thereby subtly raising lifetime client value. On-premises estates, though contracting, still generate advisory revenue from API layer insertion and phased module retirement as firms pursue gradual de-customization. Hybrid footprints, forecast at a mid-single-digit CAGR, create niche demand for secure integration architectures that span private and public clouds while satisfying sovereignty audits.

Geography Analysis

North America generated 38% of 2025 revenue, underpinned by stringent regulatory frameworks in pharmaceuticals, defense, and finance that necessitate specialized controls consulting. Fortune 500 mergers spur harmonization projects, while the United States near-shoring to Mexico elevates cross-border compliance work on USMCA origins. Canada attracts hyperscaler investment, exemplified by Workday's CAD 1 billion (USD 770 million) expansion to service midsize manufacturers. The ERP consulting services market continues to shift toward outcome-based deals as North American clients prioritize value realization over staff-augmentation hours.

Asia-Pacific is the fastest-growing region, with a 11.90% CAGR, capturing cloud migration contracts across India, China, Japan, and the ASEAN markets. SAP disclosed that 60% of its Q4 2024 APAC wins involved SMEs upgrading via RISE bundles. India's production-linked incentives in electronics and pharmaceuticals accelerate traceability and quality audit adoption, while Chinese manufacturers adopt domestic Kingdee and Yonyou platforms to satisfy dual-circulation directives, creating parallel integration workloads. Japan's aging workforce drives RPA integration with ERP systems to offset labor constraints, pushing consultancies to adopt bot-governance frameworks.

Europe experiences moderate growth as GDPR residency rules force multi-tenant cloud providers to spin up localized zones, complicating cross-border rollouts and inflating project scoping cycles. Germany, the United Kingdom, and France drive spending through Industry 4.0 investments tying ERP to IoT sensor data, while Southern Europe accelerates due to EU subsidy programs and Accenture's acquisition of Fibermind in Portugal. Middle East sovereign-wealth funds bankroll government modernizations that digitalize procurement and tax while adhering to Islamic finance structures, attracting long-duration consulting engagements. Africa and South America remain emerging opportunities, though Brazil's manufacturing and mining revamp, aided by Accenture's Cientra purchase, signals an uptick in Latin American deal flow.

- Accenture plc

- Deloitte Touche Tohmatsu Limited

- International Business Machines Corporation

- Capgemini SE

- Infosys Limited

- Tata Consultancy Services Limited

- Wipro Limited

- Cognizant Technology Solutions Corporation

- HCL Technologies Limited

- NTT DATA Corporation

- Tech Mahindra Limited

- Atos SE

- CGI Inc.

- DXC Technology Company

- BearingPoint Holding B.V.

- PwC International Limited

- KPMG International Limited

- Ernst and Young Global Limited

- Hitachi, Ltd.

- Sopra Steria Group SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Native ERP Demand Among SMEs

- 4.2.2 Shift to Composable ERP Architecture

- 4.2.3 Rise of Outcome-Based Consulting Contracts

- 4.2.4 Post-Pandemic Digital Transformation Budgets Rebound

- 4.2.5 Industry-Specific ERP Templates Accelerating Adoption

- 4.2.6 Integration of AI-Driven Process Mining

- 4.3 Market Restraints

- 4.3.1 Shortage of Certified ERP Consultants

- 4.3.2 Rising Cybersecurity Concerns Delaying Projects

- 4.3.3 Inflation-Driven IT Budget Compression

- 4.3.4 Vendor Lock-In Risks Reducing Consulting Flexibility

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By End User Industry

- 5.3.1 Manufacturing

- 5.3.2 BFSI

- 5.3.3 Retail and E-Commerce

- 5.3.4 Healthcare

- 5.3.5 Government and Public Sector

- 5.3.6 IT and Telecom

- 5.3.7 Energy and Utilities

- 5.3.8 Other End User Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Kenya

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Deloitte Touche Tohmatsu Limited

- 6.4.3 International Business Machines Corporation

- 6.4.4 Capgemini SE

- 6.4.5 Infosys Limited

- 6.4.6 Tata Consultancy Services Limited

- 6.4.7 Wipro Limited

- 6.4.8 Cognizant Technology Solutions Corporation

- 6.4.9 HCL Technologies Limited

- 6.4.10 NTT DATA Corporation

- 6.4.11 Tech Mahindra Limited

- 6.4.12 Atos SE

- 6.4.13 CGI Inc.

- 6.4.14 DXC Technology Company

- 6.4.15 BearingPoint Holding B.V.

- 6.4.16 PwC International Limited

- 6.4.17 KPMG International Limited

- 6.4.18 Ernst and Young Global Limited

- 6.4.19 Hitachi, Ltd.

- 6.4.20 Sopra Steria Group SA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment