|

시장보고서

상품코드

2065576

소프트웨어 부품표(SBOM) 관리 소프트웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Software Bill Of Materials (SBOM) Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

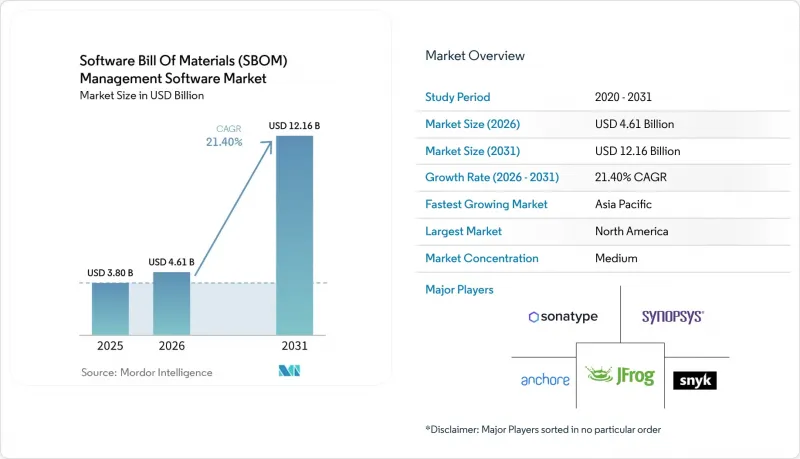

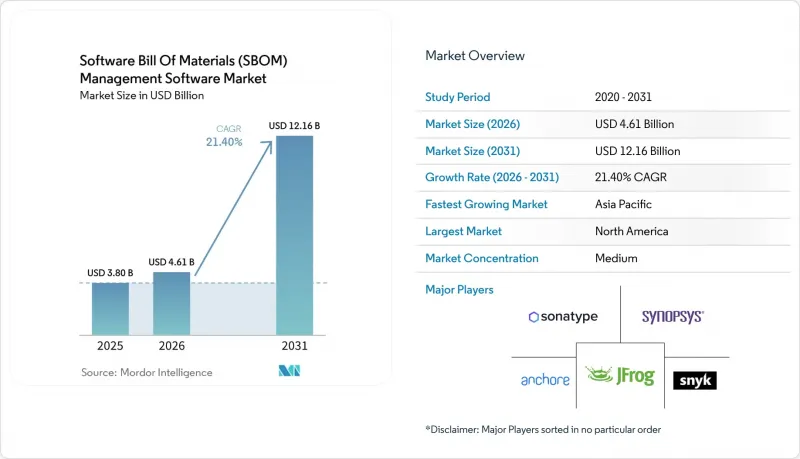

Mordor Intelligence에 의하면, 소프트웨어 부품표(SBOM) 관리 소프트웨어 시장 규모는 2025년에 38억 달러로 평가되었고, 2026년 46억 1,000만 달러로 추정되고, 2031년까지 121억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 21.4%를 나타낼 전망입니다.

본 보고서는 도입 형태별(온프레미스, 클라우드 기반, 하이브리드), 용도별(의료, 자동차, 국방, 소비자용 전자기기, 산업용, 기타 용도), 조직 규모별(대기업, 중소기업), 구성 요소별(소프트웨어 플랫폼, 서비스) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 소프트웨어 부품표(SBOM) 관리 소프트웨어 시장 동향 및 인사이트

소프트웨어 공급망 투명성에 관한 규제 요건의 강화

세계 각국 정부는 SBOM 공개를 조달의 전제조건으로 법제화함으로써, 자발적인 모범 사례를 법적 구속력이 있는 의무로 전환했습니다. 2025년 1월, 미국 사이버보안·인프라보안청(CISA)은 대통령령 제14028호의 적용 범위를 확대하고, 모든 연방 기관에 2026년 9월까지 중요 시스템의 SBOM 정확성을 검증하도록 지시했습니다. 2024년 12월에 발효되는 유럽연합(EU)의 ‘사이버 복원력 법’은 디지털 요소를 포함하는 제품의 제조업체에 대해 2026년 9월부터 기계 판독 가능한 형식의 SBOM 작성을 의무화하고 있으며, 이 의무는 임베디드 펌웨어가 탑재된 하드웨어로도 확대 적용됩니다. 이와 더불어, 미국 식품의약국(FDA)의 규정에 따라 의료기기 승인이 SBOM 제출 기한과 연계되게 됨에 따라 투명성이 한층 더 제도화되고 있습니다. 따라서 다국적 벤더 기업들은 여러 형식으로의 내보내기 및 지역별로 상이한 스키마에 대한 정책의 자동 매핑이 가능한 플랫폼에 대한 투자를 확대하고 있으며, 규제의 복잡성이 도구 투자의 계기가 되고 있습니다.

오픈소스 구성 요소를 표적으로 한 사이버 보안 위협의 심화

공격자가 공개 저장소에 악성 라이브러리를 심어 놓고, 구형 의존성에 숨어 있는 수정되지 않은 취약점을 악용한 결과, 공급망 공격이 급증했습니다. Sonatype의 기록에 따르면, 2024년에 업로드된 악성 패키지는 24만 5,000건 이상에 달했고, 전년 대비 156% 증가했으며, 이를 기회로 삼은 침입의 규모가 얼마나 큰지 여실히 드러났습니다. 미국의 ‘알려진 악용된 취약점’ 목록은 2026년 초까지 1,200건을 넘어설 전망이며, 상용 제품 내 패치가 적용되지 않은 오픈소스 모듈과 관련된 비중이 증가하고 있습니다. 2026년 3월, 오픈소스 SBOM 생성기인 Trivy를 대상으로 한 침해 시도가 발생하면서, 이제는 보안 도구 자체조차도 공격의 표적이 되고 있음이 밝혀졌습니다. 조직들은 제로데이 취약점이 발생했을 때 노출된 부분을 신속하게 파악하고, 수정까지 걸리는 평균 시간을 단축하며, 횡방향 공격의 확산을 제한하기 위한 유일한 실용적인 수단으로서 SBOM을 점점 더 중요하게 여기고 있습니다.

SBOM 형식 및 교환 프로토콜에 대한 표준화의 부재

SPDX와 CycloneDX가 공존하며, 각각 별도의 로드맵에 따라 발전하고 있기 때문에 기업들은 병행되는 툴체인을 활용하거나, 비가역적인 변환 유틸리티에 의존할 수밖에 없는 상황입니다. 미국 국가통신정보국(NTIA)은 두 스키마 모두를 승인했으나, 단일 표준을 지정하기에는 이르지 못했고, 의도치 않게 분열을 고착화시켜 버렸습니다. 산업 분야 및 소비자 분야의 소규모 벤더들은 어댑터 개발 자금 확보에 어려움을 겪고 있으며, 이로 인해 생태계 전체의 상호 운용성이 지연될 뿐만 아니라 예상 성장률도 3.4퍼센트 포인트 하락하고 있습니다.

부문별 분석

규제가 엄격한 업계가 클라우드의 민첩성과 엄격한 데이터 주권 규정을 양립시키려 노력하는 가운데, 하이브리드 환경은 2031년까지 연평균 성장률(CAGR) 17.2%로 성장할 전망입니다. 2025년에는 클라우드 서비스가 매출의 57.7%를 차지했으나, 기밀 정보, 환자 정보 또는 금융 데이터를 다루는 조직에서는 워크로드를 분할하는 경향이 강해지고 있어, 원본 SBOM 파일은 온프레미스에 보관하고 분석 처리만 클라우드로 전송하는 사례가 늘고 있습니다. 미국 식품의약국(FDA)의 2025년 지침에 따라, 의료기기 제조업체들은 공개 의무를 이행하면서도 자체 펌웨어의 세부 정보를 보호하기 위해 이러한 이중 아키텍처의 도입을 가속화했습니다.

하이브리드 모델을 도입한 기업들은 순수한 온프레미스 환경 사용자와 비교했을 때, ISO 27001 및 SOC 2 감사에서 증거 수집 주기가 30% 단축되었다고 보고하고 있으며, 이는 실질적인 이점이 입증된 것입니다. 클라우드 플랫폼이 컨테이너 레지스트리나 취약점 스캐너에 SBOM 연동 기능을 통합함에 따라, 온프레미스 구성 요소는 분석 엔진이라기보다는 보안 엔클레이브로서의 역할을 점점 더 많이 수행하게 되고 있습니다. 이러한 구조적 변화로 인해 2020년대 후반에는 하이브리드 설계가 소프트웨어 부품 목록(SBOM) 시장의 표준이 될 것이며, 사설 데이터센터와 하이퍼스케일 클라우드를 아우르는 통합 대시보드에 대한 생태계 수요가 증가할 것으로 예측됩니다.

방위 분야의 워크로드는 모든 용도 중에서 가장 높은 연평균 성장률(CAGR) 18.6%를 나타낼 것으로 전망됩니다. 이러한 성장은 주로 미국 국방부가 사이버 보안 성숙도 모델 인증(CMMC) 2.0 평가에 소프트웨어 구성품 목록(SBOM) 검증을 의무화한 데 기인합니다. 이 요건에 따라, 도급업체는 지속적인 증빙 자료를 제출하여 엄격한 사이버 보안 기준을 준수해야 할 의무가 있습니다. 이러한 변화로 인해, 기존에는 이러한 기술의 도입이 늦어졌던 워터폴형 개발 프로세스에도 자동화가 도입되고 있습니다. 실시간 검증 및 보고에 대한 수요는 SBOM 도구의 혁신을 촉진하여, 방위 산업 관련 계약업체들이 규제 요건을 충족하면서 동시에 업무 흐름을 효율화할 수 있게 될 것으로 예측됩니다.

의료 분야는 2025년에 24.2%의 점유율을 차지했으며, 매출 1위 자리를 계속 유지할 전망이지만, 규제가 주로 신규 의료기기 승인 신청에 적용되기 때문에 성장세는 완만해질 것으로 보입니다. 자동차 및 산업용 장비 제조업체들은 유엔 WP.29 규정과 산업 안전 기준에서 부품의 투명성이 점점 더 중요시됨에 따라 도입을 가속화하고 있습니다. 이러한 산업 전반에 걸친 압력은 물리적 안전 위험 관리에서 SBOM의 중요성을 더욱 부각시키고 있으며, 소프트웨어 부품 목록(SBOM) 시장의 잠재적 총 수요를 확대시키고 있습니다.

지역별 분석

북미는 연방 정부의 조달 의무화 및 의료 기술 및 SaaS 공급업체가 밀집해 있는 점을 배경으로, 2025년 매출의 37.2%를 차지했습니다. 2025년 1월의 CISA 지침과 미국 식품의약국(FDA)의 섹션 524B 지침이 맞물리면서 공개에 대한 기대감이 높아짐에 따라, SBOM 작성은 ‘모범 사례’에서 ‘시장 진입의 필수 요건’으로 변화하고 있습니다. 캐나다 공급업체들은 국경을 넘는 공급망에서 입지를 공고히 하기 위해 미국과 마찬가지로 활발한 움직임을 보이고 있는 반면, 멕시코에서의 도입은 자동차 및 항공우주 산업의 수출 거점을 중심으로 집중되고 있습니다.

유럽에서는 ‘사이버 복원력법’에 따라 규정 준수 기한이 2026년 9월로 앞당겨진 데 따라 견조한 성장세가 나타나고 있습니다. 독일의 기술 지침인 ‘TR-03183-2’는 중요 인프라 사업자를 위한 청사진 역할을 하며, 그 영향은 유럽연합(EU) 전역으로 파급되고 있습니다. 브렉시트 이후 영국은 단일 시장 접근권을 유지하기 위해 긴밀한 협력을 이어가고 있으며, 이는 이 지역의 통일된 방향성을 여실히 보여주고 있습니다. 펌웨어를 탑재하는 하드웨어 제조업체는 순수한 소프트웨어 출판사와 동일한 투명성 규정의 적용을 받게 되며, 이에 따라 유럽의 소프트웨어 부품 목록(SBOM) 시장의 잠재 고객 기반이 확대되고 있습니다.

아시아태평양은 중국의 ‘다층 보호 체계 2.0’, 일본의 정보처리추진기구(IPA)의 지침, 그리고 인도의 CERT-In이 발표한 권고에 힘입어 세계 최고 수준인 연평균 성장률(CAGR) 16.4%를 기록하며 성장할 것으로 전망됩니다. 국내 주권 정책에 따라 중국에서는 현지 호스팅형 도구 및 데이터 소재지 보장에 대한 수요가 높아지고 있습니다. 일본의 주요 자동차 기업들은 WP.29의 수출 의무에 대응하여 SBOM 워크플로우를 공급망 계약에 반영하고, 그 요건을 부품 공급업체까지 확대 적용하고 있습니다. 한편, 중동 및 아프리카 및 남미에서는 공식적인 규제 도입이 늦어지고 있지만, 다국적 기업들이 독자적인 기준을 도입함에 따라 에너지, 통신, 은행 등 각 부문에서 소프트웨어 부품 목록(SBOM) 시장의 초기 기반을 다져가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the software bill of Materials market size was valued at USD 3.8 billion in 2025 and estimated to grow from USD 4.61 billion in 2026 to reach USD 12.16 billion by 2031, at a CAGR of 21.4% during the forecast period (2026-2031).

This report is Segmented by Deployment Mode (On-Premise, Cloud-Based, Hybrid), Application (Healthcare, Automotive, Defense, Consumer Electronics, Industrial, Other Applications), Organization Size (Large Enterprises, Small and Medium Enterprises), Component (Software Platform, Services), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Software Bill Of Materials (SBOM) Management Software Market Trends and Insights

Growing Regulatory Mandates for Software Supply Chain Transparency

Governments worldwide codified SBOM disclosure as a purchasing prerequisite, transforming a voluntary best practice into an enforceable obligation. In January 2025, the United States Cybersecurity and Infrastructure Security Agency directed all federal bodies to verify SBOM accuracy for critical systems by September 2026, extending Executive Order 14028's reach.The European Union's Cyber Resilience Act, effective December 2024, compels manufacturers of products with digital elements to produce machine-readable SBOMs starting September 2026, widening the obligation to hardware with embedded firmware. Parallel rules from the United States Food and Drug Administration now bind medical-device approval to SBOM submission timelines, further institutionalizing transparency. Multinational vendors are therefore investing in platforms that export multiple formats and map policies automatically to divergent regional schemas, converting regulatory complexity into a catalyst for tooling spend.

Escalating Cybersecurity Threats Targeting Open-Source Components

Supply-chain attacks rose sharply as adversaries seeded malicious libraries into public repositories and exploited dormant flaws in legacy dependencies. Sonatype logged more than 245,000 rogue packages uploaded in 2024, up 156% year on year, underscoring the scale of opportunistic infiltration. The United States Known Exploited Vulnerabilities catalog topped 1,200 entries by early 2026, with a growing share linked to unpatched open-source modules inside commercial products. A March 2026 breach attempt on Trivy, an open-source SBOM generator, demonstrated that even security tooling itself is now a target.Organizations increasingly view SBOMs as the only practical way to pinpoint exposure quickly when zero-days emerge, compressing mean time to remediation and limiting lateral attack movement.

Lack of Standardization Across SBOM Formats and Exchange Protocols

The coexistence of SPDX and CycloneDX, each advancing on separate roadmaps, forces enterprises to juggle parallel toolchains or resort to lossy conversion utilities. The United States National Telecommunications and Information Administration recognized both schemas but stopped short of naming a single canonical standard, inadvertently entrenching fragmentation. Small vendors in industrial and consumer sectors struggle to fund adapters, delaying ecosystem-wide interoperability and shaving 3.4 percentage points from forecast growth.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of DevSecOps Practices Across Enterprises

- Increasing Integration of SBOM Platforms with CI/CD Pipelines

- Limited Awareness Among Small and Medium Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid setups are on track to expand at a 17.2% CAGR through 2031 as highly regulated verticals reconcile cloud agility with strict data-sovereignty rules. While cloud services commanded 57.7% revenue in 2025, organizations handling classified, patient, or financial data increasingly split workloads, keeping raw SBOM files on-premise and sending analytics to the cloud. The Food and Drug Administration's 2025 guidance spurred medical-device makers to adopt such dual architectures, safeguarding proprietary firmware details while satisfying disclosure mandates.

Enterprises adopting hybrid models reported 30% shorter evidence-collection cycles for ISO 27001 and SOC 2 audits compared with pure on-premise users, underscoring a practical payoff. As cloud platforms embed SBOM hooks into container registries and vulnerability scanners, on-premise components increasingly act as secure enclaves rather than analytic engines. This structural shift positions hybrid designs as the default for the Software Bill of Materials market by late decade, fostering ecosystem demand for unified dashboards that span private data centers and hyperscale clouds.

Defense workloads are projected to register an 18.6% CAGR, the highest among all applications. This growth is primarily driven by the Department of Defense's mandate to incorporate Software Bill of Materials (SBOM) verification into Cybersecurity Maturity Model Certification (CMMC) 2.0 assessments. The requirement compels contractors to provide continuous attestations, ensuring compliance with stringent cybersecurity standards. This shift is pushing automation into traditionally waterfall development processes, which have historically been slower to adopt such technologies. The demand for real-time verification and reporting is expected to drive innovation in SBOM tools, enabling defense contractors to streamline their workflows while meeting regulatory requirements.

Healthcare remains the revenue leader thanks to a 24.2% share in 2025, yet its growth moderates because mandates apply chiefly to new device submissions. Automotive and industrial manufacturers are moving up the adoption curve as United Nations WP.29 rules and industrial safety norms increasingly reference component transparency. These cross-sector pressures reinforce the centrality of SBOMs to physical-safety risk management, broadening total addressable demand for the Software Bill of Materials market.

Geography Analysis

North America accounted for 37.2% of 2025 revenue, anchored by federal procurement mandates and a dense concentration of medical-technology and SaaS vendors. The January 2025 CISA directive and the Food and Drug Administration's Section 524B guidance jointly heighten disclosure expectations, turning SBOM creation into a go-to-market necessity rather than a best practice. Canadian suppliers mirror the United States momentum to remain viable in cross-border supply chains, while Mexico's adoption clusters around automotive and aerospace export hubs.

Europe follows with robust growth as the Cyber Resilience Act pushes compliance deadlines toward September 2026. Germany's technical guideline TR-03183-2 serves as a blueprint for critical-infrastructure operators and ripples outward to the wider European Union. Post-Brexit, the United Kingdom keeps tight alignment to preserve single-market access, underlining the region's unified trajectory. Hardware makers embedding firmware now fall under the same transparency rules as pure software publishers, broadening the European Software Bill of Materials market addressable base.

Asia-Pacific is forecast to rise at a 16.4% CAGR, the fastest globally, thanks to China's Multi-Level Protection Scheme 2.0, Japan's Information-technology Promotion Agency guidelines, and India's CERT-In advisories. Domestic sovereignty policies drive Chinese demand for locally hosted tools and data-residency guarantees. Japan's automotive giants, responding to WP.29 export obligations, embed SBOM workflows into supply-chain contracts, radiating requirements to component suppliers. While Middle East and Africa plus South America lag in formal mandates, multinational operators import their own standards, seeding initial footprints for the Software Bill of Materials market across energy, telecom, and banking sectors.

- Anchore Inc.

- Sonatype Inc.

- Synopsys Inc.

- Flexera Software LLC

- Snyk Limited

- Mend.io Ltd.

- FOSSA Inc.

- JFrog Ltd.

- Veracode Inc.

- Checkmarx Ltd.

- Rezilion Inc.

- Phylum LLC

- GrammaTech Inc.

- Cybeats Technologies Corp.

- Deepfence Inc.

- Oxeye Security Ltd.

- Legit Security Ltd.

- Aqua Security Software Ltd.

- Chainguard Inc.

- Stacklok Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Regulatory Mandates for Software Supply Chain Transparency

- 4.2.2 Escalating Cybersecurity Threats Targeting Open-Source Components

- 4.2.3 Rising Adoption of DevSecOps Practices Across Enterprises

- 4.2.4 Increasing Integration of SBOM Platforms with CI/CD Pipelines

- 4.2.5 Emergence of AI-Powered Vulnerability Prioritization in SBOM Tools

- 4.2.6 Expansion of Software Composition Analysis into IoT Firmware SBOM

- 4.3 Market Restraints

- 4.3.1 Lack of Standardization Across SBOM Formats and Exchange Protocols

- 4.3.2 Limited Awareness Among Small and Medium Enterprises

- 4.3.3 Concerns Over Intellectual Property Exposure in SBOM Disclosure

- 4.3.4 Inadequate Integration with Legacy Application Security Tools

- 4.4 Industry Value and Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premise

- 5.1.2 Cloud-Based

- 5.1.3 Hybrid

- 5.2 By Application

- 5.2.1 Healthcare

- 5.2.2 Automotive

- 5.2.3 Defense

- 5.2.4 Consumer Electronics

- 5.2.5 Industrial

- 5.2.6 Other Applications

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Component

- 5.4.1 Software Platform

- 5.4.2 Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Anchore Inc.

- 6.4.2 Sonatype Inc.

- 6.4.3 Synopsys Inc.

- 6.4.4 Flexera Software LLC

- 6.4.5 Snyk Limited

- 6.4.6 Mend.io Ltd.

- 6.4.7 FOSSA Inc.

- 6.4.8 JFrog Ltd.

- 6.4.9 Veracode Inc.

- 6.4.10 Checkmarx Ltd.

- 6.4.11 Rezilion Inc.

- 6.4.12 Phylum LLC

- 6.4.13 GrammaTech Inc.

- 6.4.14 Cybeats Technologies Corp.

- 6.4.15 Deepfence Inc.

- 6.4.16 Oxeye Security Ltd.

- 6.4.17 Legit Security Ltd.

- 6.4.18 Aqua Security Software Ltd.

- 6.4.19 Chainguard Inc.

- 6.4.20 Stacklok Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment