|

시장보고서

상품코드

2065579

CRM 통합 전사적 자원 계획(ERP) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)CRM-Integrated Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

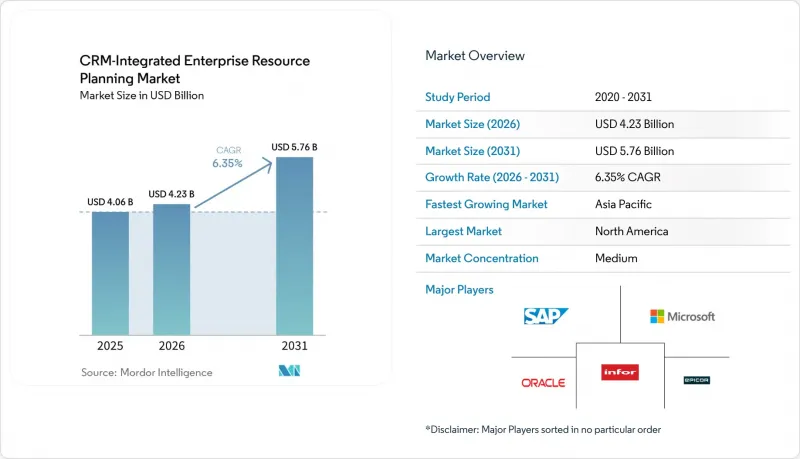

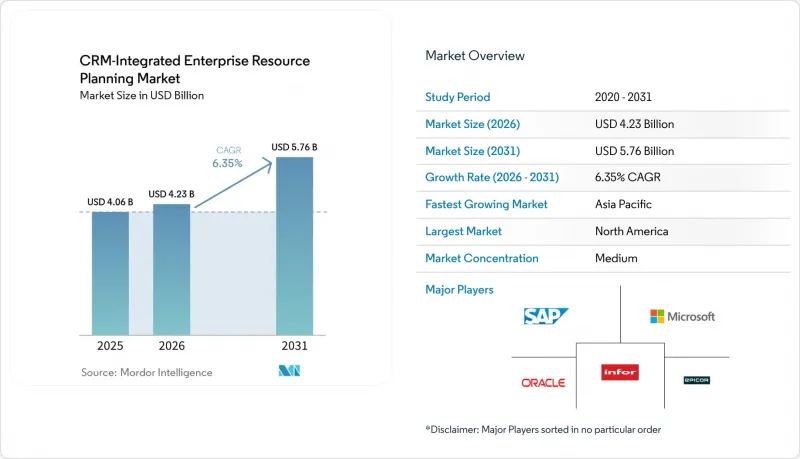

Mordor Intelligence에 의하면, CRM 통합 전사적 자원 계획(ERP) 시장 규모는 2026년 42억 3,000만 달러로 추정되고, 2031년까지 57억 6,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 6.35%를 나타낼 것으로 예측됩니다.

본 보고서는 도입 형태별(온프레미스, 클라우드, 하이브리드), 조직 규모별(중소기업, 대기업), 구성 요소별(소프트웨어, 서비스), 업종별(제조, 소매 및 전자상거래, 의료, 은행 및 금융 서비스·보험, IT 및 통신, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 CRM 통합 전사적 자원 계획(ERP) 시장 동향 및 인사이트

‘클라우드 퍼스트’ 방식의 디지털 전환이 필수적일 것

기업들이 온프레미스 하드웨어를 폐지하고 고객 데이터와 거래 데이터를 실시간으로 동기화하는 확장 가능한 플랫폼을 도입함에 따라, 클라우드 도입은 2031년까지 연평균 성장률(CAGR) 14.20%로 확대되고 있으며, 이는 CRM 통합 전사적 자원 계획(ERP) 시장 전체 성장률의 2배 이상에 달할 전망입니다. 2026년과 2027년으로 정해진 중동의 전자 청구서 도입 기한에 더해, 일본에서 중소기업의 전환 비용의 최대 50%를 지원하는 보조금 프로그램도 이러한 추세를 가속화하고 있습니다. Microsoft Dynamics 365 사용자들은 재무, 재고, 고객 모듈을 통합한 결과, 평균 주문에서 입금까지의 주기를 이미 30% 단축했습니다. 각 벤더사는 이에 대응하여 자동으로 업데이트되는 세무 엔진과 현지화 팩을 통합함으로써, 온프레미스 시스템의 골칫거리였던 수동 패치 적용의 부담을 해소하고 있습니다.

고객 데이터와 업무 데이터 통합의 필요성

데이터베이스가 조각화되면 숨겨진 비용이 증가하지만, 통합 제품군을 도입하면 이를 해결할 수 있습니다. CRM과 ERP를 통합한 플랫폼을 도입한 기업에서는 주문 확정 전에 고객의 신용 상태, 재고, 물류 데이터가 검증되기 때문에 견적서의 오류가 40% 감소하고 납기 준수율이 25% 향상되었다고 보고되고 있습니다. BFSI(은행 및 금융 및 보험) 업계의 도입 기업들은 360도 고객 뷰를 활용하여 실시간으로 교차 판매 제안을 하고 있으며, 소매업체들은 온라인과 매장의 재고를 동기화하여 비용이 많이 드는 품절 상황을 방지하고 있습니다. 이러한 성과를 뒷받침하는 것은 API 우선 설계이며, 이를 통해 취약한 배치 인터페이스에 의존하지 않고도 타사 앱이 이벤트 기반 엔드포인트를 활용할 수 있게 되었습니다.

복잡한 도입에 따른 높은 총 소유 비용

소프트웨어 라이선스 비용은 프로젝트 총 비용의 불과 20%-30%에 불과하며, 나머지는 데이터 마이그레이션, 맞춤 설정, 변경 관리에 소요되어 예산이 3배로 늘어나기도 합니다. 컨설턴트의 시간당 요금은 200-350달러이지만, 규제 대상 업계의 경우 FDA 21 CFR Part 11 테스트와 같은 추가 검증 절차가 필요하며, 이로 인해 25%-40%의 비용이 추가로 발생합니다. 교육에 대한 투자가 부족할 경우 사용자의 반발을 불러일으키기 쉬우며, 변경 프로그램에 할당된 예산이 15% 미만일 경우 실패율은 60%를 초과합니다. 클라우드 고객이라 하더라도, 구독 서비스의 무분별한 확대에 주의해야 합니다. 사용하지 않는 SaaS 라이선스는 지속적인 비용을 증가시킬 가능성이 있기 때문입니다.

부문별 분석

클라우드 도입은 2025년 매출의 49.80%를 차지한 것으로 평가되었으며, 연평균 성장률(CAGR) 14.20%로 성장할 것으로 전망되는데, 이는 CRM 통합 전사적 자원 계획(ERP) 시장의 벤치마크보다 2배 이상 높은 수치입니다. 기업들은 서버 투자를 줄이고 분석 및 혁신에 자금을 재배분하고 있는 반면, 벤더들은 Oracle의 80억 달러 규모 도쿄 거점 확장 등 지역별 용량 확충을 추진하고 있습니다. EU 데이터법은 데이터 마이그레이션성을 의무화함으로써 서비스 제공업체 변경을 용이하게 하고 있지만, 중국의 현지화 규제는 퍼블릭 클라우드 도입을 억제하고 있습니다. 하이브리드 아키텍처는 타협안으로 기능하지만, 설계가 미흡할 경우 통합 지연이나 보안 관리 문제로 인해 비용 절감 효과가 저하될 가능성이 있습니다.

지적 재산권 관련 우려나 방위 규제로 인해 외부 호스팅이 금지된 경우, 하이브리드 및 온프레미스 방식이라는 대안이 여전히 남아 있습니다. 제약 기업들은 인사 및 조달 업무를 클라우드로 이전하고 있는 반면, 검증 완료된 제조 모듈은 여전히 사내에 유지하고 있습니다. 그 결과, CRM 통합 전사적 자원 계획(ERP) 시장은 여전히 여러 도입 모델을 지원하고 있지만, 이용 경향은 확실히 SaaS 쪽으로 쏠리고 있습니다.

중소기업 부문은 연평균 성장률(CAGR) 15.90%로 성장하고 있으며, 이는 CRM 통합 전사적 자원 계획(ERP) 시장 전체의 성장률보다 약 3배 높은 수치입니다. 인도의 2,925.39 카롤 루피(3억 5,000만 달러) 규모의 PACS ERP 이니셔티브와 같은 정부 프로그램은 농촌 협동조합에 보조금을 지원하고 있는 반면, 유럽연합(EU)의 ‘디지털 데케이드’ 보조금은 2030년까지 중소기업의 90%가 디지털화를 달성하는 것을 목표로 하고 있습니다. 2025년 시점에서도 여전히 54.10%의 시장 점유율을 차지한 대기업들은 시스템 갱신 주기가 길고 자체 개발한 코드가 정착되어 있어 성장 속도가 둔화되고 있습니다. 그러나 통합에 따른 오버헤드를 최소화하기 위해, 서로 분리된 시스템들을 통합된 제품군으로 집약하고 있습니다.

중소기업은 온프레미스 환경을 완전히 생략하고, 비즈니스 요구 사항의 확대에 맞추어 확장 가능한 모듈형 클라우드 번들을 채택하는 경우가 많습니다. 그 위험 요소로는 ‘구독 피로감’을 들 수 있습니다. 추가 기능을 도입함에 따라 월 이용료가 500달러에서 5,000달러로 급증하여, 시간이 지남에 따라 영구 라이선스 보유 비용과 비슷한 수준에 도달할 가능성이 있기 때문입니다. 그렇긴 하지만, AI 기능과 실시간 분석에 접근할 수 있게 됨에 따라 중소기업과 세계의 기존 기업 간의 기능 격차는 점차 좁혀지고 있습니다.

지역별 분석

2025년에는 북미가 매출의 38.20%를 차지하며 1위를 차지했습니다. 시장 침투율이 성숙 단계에 접어들면서 신규 고객 확보는 정체 상태에 이르렀으며, 공급업체들은 기존 고객의 계약 갱신, AI 부가 기능, 그리고 산업별 사업 확장에 주력하고 있습니다. USMCA(미국·멕시코·캐나다 협정)에 따른 국경 간 무역은 관세 및 원산지 증명 서류를 실시간으로 자동화하는 솔루션에 대한 수요를 촉진하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 13.80%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 중국의 사이버 보안 관련 법규에 따라 국내 호스팅이 의무화되어 있기 때문에 현지 공급업체들이 우위를 점하고 있으며, 다국적 기업들은 국내에 데이터센터를 구축할 수밖에 없는 상황입니다. 인도의 전국적인 PACS 도입, 일본의 중소기업을 대상으로 한 6억 6,000만 달러 규모의 보조금, 그리고 Oracle의 도쿄 지역 용량 확대가 SaaS의 급속한 보급을 뒷받침하고 있습니다. 다양한 언어와 규제로 인해 현지화 비용은 증가하지만, 해당 지역의 틈새 시장 업체들에게는 비즈니스 기회가 되고 있습니다.

유럽의 성장은 EU 데이터법과 영국의 브렉시트 이후 데이터 규제에 대한 이중적인 규정 준수로 인해 제약을 받고 있으며, 국경을 초월한 사업 확장을 위해서는 병행된 거버넌스 체제가 요구되고 있습니다. 독일, 영국, 프랑스가 해당 지역 전체 지출의 대부분을 차지하고 있으며, 독일의 경우 독자적인 스케줄링 알고리즘을 온프레미스에서 관리하는 것을 선호하는 경향이 있습니다. 중동에서는 전자 청구서 의무화 법안으로 인해 시장이 빠르게 성장하고 있는 반면, 아프리카와 남미는 여전히 신흥 시장이지만 레거시 IT의 부담이 최소화되어 있어 클라우드 도입이 활발하게 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the cRM-Integrated eRP market size is expected to grow from USD 4.23 billion in 2026 to USD 5.76 billion by 2031 at a CAGR of 6.35% over 2026-2031.

This report is Segmented by Deployment Mode (On-Premises, Cloud, and Hybrid), Organization Size (Small and Medium Enterprises, and Large Enterprises), Component (Software and Services), Industry Vertical (Manufacturing, Retail and E-Commerce, Healthcare, Banking, Financial Services and Insurance, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global CRM-Integrated Enterprise Resource Planning Market Trends and Insights

Cloud-First Digital Transformation Mandates

Cloud deployments are growing at a 14.20% CAGR through 2031, more than double the overall CRM-Integrated ERP market rate, as enterprises retire on-premises hardware in favor of scalable platforms that synchronize customer and transactional data in real time. Middle Eastern e-invoicing deadlines for 2026 and 2027, together with Japan's subsidy program that funds up to 50% of migration costs for SMEs, are accelerating this movement. Microsoft Dynamics 365 users have already cut average order-to-cash cycles by 30% after consolidating finance, inventory, and customer modules. Vendors are responding by embedding tax engines and localization packs that update automatically, removing the manual patching burden that plagued on-premises systems.

Need for Unified Customer and Operational Data

Fragmented databases inflate hidden costs that integrated suites eliminate. Enterprises with unified CRM-ERP platforms reported 40% fewer quote errors and 25% better on-time delivery because customer credit, inventory, and logistics data are validated before order confirmation. BFSI adopters are harnessing 360-degree customer views to recommend cross-sell offers in real time, while retailers synchronize online and store inventory to avert costly stock-outs. An API-first design underpins these gains, exposing event-driven endpoints that third-party apps consume without brittle batch interfaces.

High Total Cost of Ownership for Complex Deployments

Software licenses account for just 20%-30% of project spend, with the rest consumed by data migration, customization, and change management that can triple budgets. Consultants bill USD 200-350 per hour, while regulated industries face extra validation steps, such as FDA 21 CFR Part 11 testing, which adds another 25%-40%. Underfunded training often leads to user resistance, pushing failure rates above 60% when less than 15% of budgets go to change programs. Even cloud customers must guard against subscription sprawl, as unused SaaS seats can inflate recurring costs.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of AI-Driven Process Automation

- Rising Subscription-Based Licensing Models

- Cyber-Security and Data-Sovereignty Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments secured 49.80% of 2025 revenue and are forecast to grow at 14.20% CAGR, more than twice the CRM-Integrated ERP market benchmark. Enterprises are routing capital away from servers toward analytics and innovation, while vendors reinforce regional capacity, such as Oracle's USD 8 billion Tokyo build-out. The EU Data Act eases provider switching by mandating data portability, yet China's localization rules temper public cloud adoption. Hybrid architectures act as a compromise, but integration latency and security management can erode savings if poorly engineered.

Hybrid and on-premises options persist where intellectual-property concerns or defense regulations prohibit external hosting. Pharmaceutical firms still maintain validated manufacturing modules on-site, even as they place HR and procurement in the cloud. Consequently, the CRM-Integrated ERP market continues to support multiple deployment models, though the usage tilt clearly favors SaaS.

Small and medium enterprises are advancing at a 15.90% CAGR, nearly triple the overall CRM-Integrated ERP market growth rate. Government programs such as India's INR 2,925.39 crore (USD 350 million) PACS ERP initiative subsidize rural cooperatives, while European Union Digital Decade grants aim to achieve 90% digitization of SMEs by 2030. Large enterprises, which still held 54.10% market share in 2025, face slower growth due to longer refresh cycles and entrenched custom code. Yet they are consolidating disparate stacks into unified suites to minimize integration overhead.

SMEs often skip on-premises footprints entirely, adopting modular cloud bundles that expand as business needs grow. The risk is subscription fatigue, as incremental add-ons can escalate monthly spend from USD 500 to USD 5,000, converging with perpetual ownership costs over time. Nevertheless, accessibility to AI features and real-time analytics is narrowing the capability gap between small firms and global incumbents.

Geography Analysis

North America led with 38.20% revenue in 2025. Mature penetration limits new-logo growth, steering vendors toward replacements, AI add-ons, and vertical expansions. Cross-border trade under USMCA is stimulating demand for suites that automate tariff and origin documentation in real time.

Asia-Pacific is the fastest-growing region, with a 13.80% CAGR. China's cybersecurity statutes obligate domestic hosting, giving local suppliers an edge and compelling multinationals to build in-country data centers. India's national PACS rollout, Japan's USD 660 million SME subsidy, and Oracle's Tokyo capacity expansion are powering rapid SaaS uptake. Diverse languages and regulations inflate localization costs but create openings for regional niche players.

Europe's growth is moderated by dual compliance with the EU Data Act and the U.K.'s post-Brexit data regime, which forces parallel governance frameworks for cross-border deployments. Germany, the United Kingdom, and France account for a significant share of regional spend, with Germany favoring on-premises control of proprietary scheduling algorithms. The Middle East is accelerating under mandatory e-invoicing laws, while Africa and South America remain emerging but demonstrate strong cloud adoption where legacy IT debt is minimal.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Epicor Software Corporation

- Workday Inc.

- Sage Group plc

- IFS AB

- Syspro (Pty) Ltd.

- Unit4 N.V.

- Acumatica, Inc.

- Plex Systems, Inc.

- QAD Inc.

- Deltek, Inc.

- Ramco Systems Limited

- Odoo SA

- Zoho Corporation Pvt. Ltd.

- Priority Software Ltd.

- TOTVS S.A.

- Epicor Kinetic (Epicor rebrand)

- Infor M3 (Infor solution)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-First Digital Transformation Mandates

- 4.2.2 Need for Unified Customer and Operational Data

- 4.2.3 Rapid Adoption of AI-Driven Process Automation

- 4.2.4 Rising Subscription-Based Licensing Models

- 4.2.5 Growing Demand for Vertical-Specific ERP Suites

- 4.2.6 Government Incentives for SME Digitalization

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Complex Deployments

- 4.3.2 Cyber-Security and Data-Sovereignty Concerns

- 4.3.3 Limited Qualified Implementation Talent Pool

- 4.3.4 Interoperability Challenges with Legacy Systems

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premises

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Component

- 5.3.1 Software

- 5.3.2 Services

- 5.4 By Industry Vertical

- 5.4.1 Manufacturing

- 5.4.2 Retail and E-Commerce

- 5.4.3 Healthcare

- 5.4.4 Banking, Financial Services and Insurance

- 5.4.5 Information Technology and Telecommunications

- 5.4.6 Government

- 5.4.7 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 Workday Inc.

- 6.4.7 Sage Group plc

- 6.4.8 IFS AB

- 6.4.9 Syspro (Pty) Ltd.

- 6.4.10 Unit4 N.V.

- 6.4.11 Acumatica, Inc.

- 6.4.12 Plex Systems, Inc.

- 6.4.13 QAD Inc.

- 6.4.14 Deltek, Inc.

- 6.4.15 Ramco Systems Limited

- 6.4.16 Odoo SA

- 6.4.17 Zoho Corporation Pvt. Ltd.

- 6.4.18 Priority Software Ltd.

- 6.4.19 TOTVS S.A.

- 6.4.20 Epicor Kinetic (Epicor rebrand)

- 6.4.21 Infor M3 (Infor solution)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment