|

시장보고서

상품코드

2065584

유럽의 LED 모듈 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

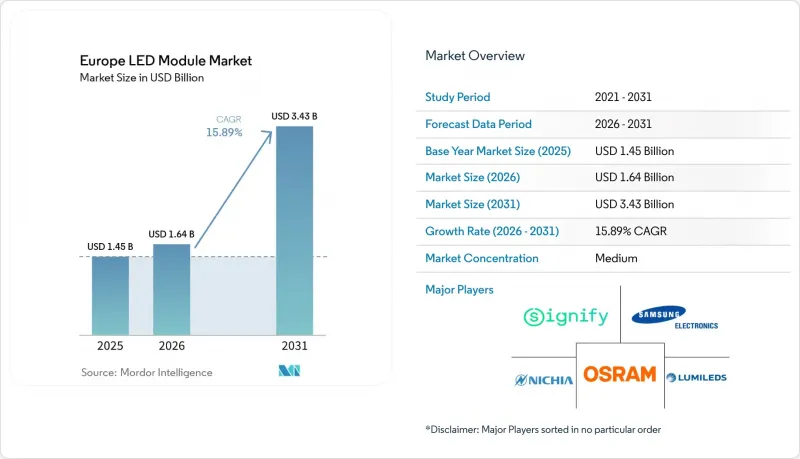

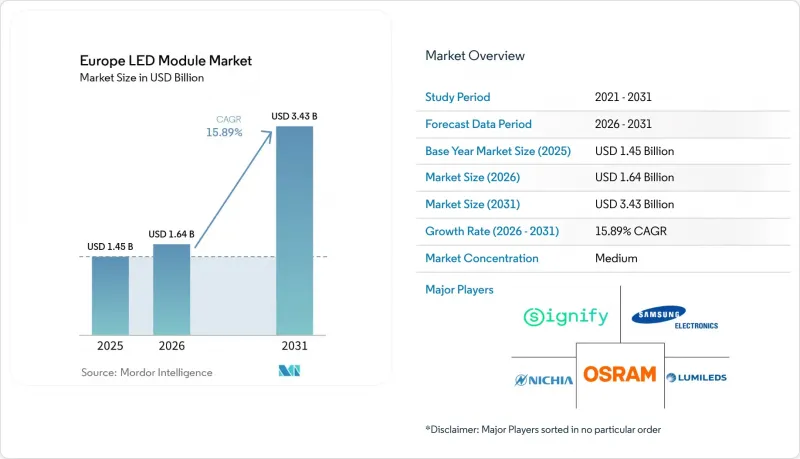

Mordor Intelligence에 의하면, 유럽의 LED 모듈 시장 규모는 2025년에 14억 5,000만 달러로 평가되었고, 2026년에 16억 4,000만 달러로 추정되고, 2031년까지 34억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 15.89%로 성장할 전망입니다.

본 보고서는 모듈 유형별(COB LED 모듈, SMD LED 모듈, 선형 LED 모듈, LED 백라이트 모듈, 기타 모듈 유형), 용도별(일반 조명, 자동차, 디스플레이 및 백라이트, 사이니지, 기타 용도), 전력 범위별(저, 중, 고), 폼 팩터별(리지드 LED 모듈, 플렉서블 LED 모듈)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 LED 모듈 시장 동향 및 인사이트

EU 전역에서 백열등의 신속한 단계적 폐지

에코디자인 규정(EU) 2019/2020에 따른 백열등 및 할로겐 램프의 강제 판매 중단 조치는 2024년 9월 에너지 라벨 재설정을 통해 더욱 강화되어, 소매 채널에서 기존 제품들이 퇴출됨과 동시에 유럽의 LED 모듈 시장을 주거, 상업 및 지자체 용도에서의 LED 기반 교체 주기로 더욱 가속화시켰습니다. 이러한 변화로 인해 모듈형 LED 제품이 유리한 입지를 차지하고 있습니다. 시설 관리자나 전기 공사업자는 조명 기구 전체를 교체하는 것보다 모듈을 교체하는 것이 더 쉬우므로, 가동 중단 시간을 단축하고 이미 설치된 조명 설비 전체에 대한 예비 부품 관리의 복잡성을 줄일 수 있기 때문입니다. 독일 베데마르크시는 4,300기의 LED 가로등을 개조하여 에너지 사용량을 80% 절감하고, 연간 전력 소비량을 90만 kWh 줄이고, 27만 유로(30만 5,000달러)의 비용 절감을 실현한 사례를 통해, 이러한 전환이 실제로 어떻게 작동하는지 보여주었습니다. 또한, 모듈의 정격 수명은 12만 시간입니다. 이러한 전환은 SMD 및 COB 공급업체들에게 특히 유리한 상황으로 작용하고 있습니다. 이는 이러한 형식이 다양한 조명 기구에서 표준화된 소켓이나 열 관리와 같은 일반적인 개조 요건을 충족하기 때문입니다. 독일의 Bundesnetzagentur나 프랑스의 DGCCRF 등 당국이 국내에서 규제를 집행함으로써, 유럽 LED 모듈 시장에서 규정을 준수하지 않는 제품의 수입 및 그레이 마켓 제품의 유통 여지를 제한하고, 이를 통해 규정을 준수하는 공급업체를 지속적으로 지원하고 있습니다.

유럽 그린딜의 에너지 효율 목표

에너지 효율 지침(EU) 2023/1791에 근거한, 2030년까지 최종 에너지 소비량을 11.7% 감축하겠다는 유럽 그린딜의 목표는 LED 모듈이 백열등에 비해 최대 90%의 에너지 절감 효과를 가져온다는 점에서 유럽 LED 모듈 시장에 장기적인 수요 기반을 조성하고 있습니다. 또한, 이 정책 체계에서는 2028-2030년 연간 에너지 절감 의무를 1.9%로 상향 조정했으며, 이에 따라 회원국 전체의 공공기관 및 상업용 건물 운영자들에게 있어 조명 설비 교체는 계속해서 조달 계획의 중요한 과제로 남아 있습니다. 유럽연합 집행위원회의 추산에 따르면, 조명 교체로 인해 2030년까지 연간 41.9 TWh의 전력을 절약하고, 소비자에게는 520억 유로(586억 달러)의 비용 절감 효과가 있을 것으로 예상되며, 이로 인해 LED 모듈은 건물 및 지방자치단체 인프라의 배출 감축을 위한 가장 비용 효율적인 수단 중 하나로서의 위상을 유지하고 있습니다. 제8조의 조달 규정은 에너지 효율이 가장 높은 등급을 우선하고 있으며, 이에 따라 기준을 충족하는 모듈 공급업체는 공공 입찰에 참여할 수 있는 경로가 명확해지는 반면, 할로겐 램프와 형광등은 주요 교체 주기에서 제외되고 있습니다. 뮌헨에서 실시된 적응형 가로등 시범 사업에서는 3,000K에서 1,700K에 이르는 가변 상관 색온도와 조광 프로파일이 시험되었으며, 교통량이 적은 시간대에는 최대 93%의 에너지 절감 효과가 확인되었습니다. 이로 인해 단순한 램프 교체에 그치지 않고, 제어 기능을 갖춘 네트워크형 LED 시스템에 대한 관심이 높아졌습니다.

LED 모듈 제조에 필요한 막대한 초기 설비 투자

유럽에서 경쟁력 있는 LED 모듈 생산 라인을 구축하기 위해서는 다이 본딩 장비, 리플로우 오븐, 자동 광학 검사 장비, 환경 시험실 등에 대한 초기 투자로 여전히 5,000만 유로에서 1억 5,000만 유로(5,600만 달러에서 1억 6,900만 달러)가 필요하며, 이로 인해 신규 진입이 제한되고 생산 능력이 기존 공급업체에 계속 집중되고 있습니다. 전력 등급, 기판, 광학 아키텍처 분야 수요가 변화함에 따라, 기술의 변천으로 인해 3-5년 이내에 설비가 노후화될 가능성이 있으므로, 이러한 부담은 더욱 커지게 됩니다. 남유럽 및 동유럽의 중소규모 조립 제조업체들은 자금 조달 여력이 제한적이어서, 2025년 유럽투자은행이 LED 제조를 위해 제공한 대출 총액은 고작 2억 5,000만 유로(2억 8,200만 달러)에 그쳤으며, 국내 생산의 추가 확대를 지원하기 위해 필요한 수준에는 미치지 못한 상태입니다. ams OSRAM이 2030년까지 오스트리아에서의 사업 확장을 위해 5억 8,800만 유로(6억 6,300만 달러)를 투자하겠다고 밝힌 것은 자본 장벽이 주로 재무 기반이 탄탄한 기업, 정책 지원을 받고 있는 기업, 혹은 반도체 분야에서 전략적으로 중요한 기업들에게는 극복 가능한 것임을 보여줍니다. 유럽의 LED 모듈 시장에서 생산량이 적고 맞춤형 사양의 제품이 많은 플렉서블 및 특수 분야에서는 일반 조명 제품 라인만큼 고정비를 효율적으로 분산시킬 수 없기 때문에 이러한 부담이 더욱 심각하게 느껴지고 있습니다.

부문별 분석

2025년, SMD LED 모듈은 유럽 LED 모듈 시장에서 33.43%의 점유율을 차지했습니다. 이는 3528, 5050, 2835 패키지 등 표준화된 실적가 자동 조립 및 조명 기기 브랜드 간의 호환성을 뒷받침하고 있기 때문에 주거용 및 상업용 일반 조명 분야에서 그 사용이 정착되었음을 반영합니다. 백라이트 모듈 시장은 가전 제조업체들이 더 높은 명암비와 고밀도 로컬 디밍을 구현하는 미니 LED 및 마이크로 LED 아키텍처로 전환함에 따라, 2026-2031년 연평균 성장률(CAGR) 16.43%를 기록하며 성장할 것으로 전망됩니다. Philips는 2026년 10월, 11,520개의 로컬 디밍 존과 2,500니트의 최대 밝기를 갖춘 ‘MLED981 RGB 미니 LED TV’를 출시하며 이러한 전환을 강조했습니다. COB 모듈은 열 성능과 루멘 밀도 측면에서 SMD 제품보다 15%에서 25% 더 우수하기 때문에 산업용 하이베이 조명이나 소매점의 스포트라이트 용도로 계속해서 활용되고 있습니다. 리니어 LED 모듈은 건축용 코브 조명이나 캐비닛 하단 설치에서 여전히 중요한 역할을 하고 있습니다. 이는 연속 배치 방식이 좁은 설치 공간에 적합하며, 끊김 없는 빛의 선을 통해 시각적 효과를 심플하게 구현할 수 있기 때문입니다.

30W를 초과하는 고출력 LED 모듈도 수직 농업 분야에서 주목을 받고 있습니다. 최대 3.5μmol/J의 광합성 유효 복사(PAR) 효율 덕분에, 북유럽의 시설에서는 일년내내 작물의 생육 주기를 조절할 수 있게 되었습니다. 플렉서블 스트립, 미니 LED 어레이, 맞춤형 어셈블리 등 기타 모듈 형식은 보다 전문적인 프로젝트에 활용되고 있습니다. 예를 들어, ‘아레나 밀라노’에서는 2026년 동계 올림픽 경기장으로 사용될 예정인 이곳에, 총 길이 50km에 달하는 5만 4,560개의 특별 주문 제작 리니어 LED 바가 설치되었습니다. 여기에는 IP67 규격의 RGBW 모듈과 3,785 유니버스에 걸친 DMX512 제어가 적용되었습니다. 이러한 조합에서 열 관리와 색상 품질이 경쟁 우위를 좌우하고 있습니다. CRI 95 이상 및 R9 값 80 이상이 요구되는 용도에서는 COB 모듈이 여전히 강점을 발휘하고 있는 반면, CRI 80이면 충분한 일반 조명 분야에서는 저비용 SMD 제품이 계속해서 주류를 차지하고 있습니다. 백라이트 모듈에는 높이 1mm 미만이라는 제한이나 양자점 필름과의 정밀한 결합 등 독자적인 설계 요건이 부과되어 있어, 이에 따라 투자는 플립칩 실장 및 마이크로 렌즈 어레이에 집중되고 있습니다. 플리커 제한 및 최소 발광 효율과 관련된 에코디자인 규정을 준수함에 따라, 유럽의 LED 모듈 시장에서는 하위 등급의 SMD 공급업체들이 고품질 부문에서 배제되고, 드라이버 및 열 설계 역량이 뛰어난 Tier 1 제조업체들에게 생산량이 집중되고 있습니다.

2025년, 일반 조명은 유럽 LED 모듈 시장 규모의 42.72%를 차지했습니다. 이는 주거, 상업, 산업 각 분야에서 LED 모듈이 형광등 트로퍼, 다운라이트, 하이베이 조명 기구를 대체했기 때문입니다. 디스플레이 및 백라이트 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 16.78%를 나타낼 것으로 예측됩니다. 이는 스크린 제조업체와 자동차 제조업체들이 고급 TV, 계기판, 센터 정보 디스플레이에서 로컬 디밍 방식으로의 전환을 추진하고 있기 때문입니다. 서유럽의 프리미엄 TV 수요가 이러한 추세를 뒷받침함에 따라, 2025년에는 65인치 이상의 제품이 판매 대수의 38%를 차지하게 될 전망이며, 이로 인해 공급업체들은 더욱 고밀도이고 고휘도의 백라이트 시스템을 제공해야 한다는 압박을 지속적으로 받고 있습니다.

자동차용 조명은 여전히 전략적인 부문으로 남아 있습니다. 이는 매트릭스 LED 헤드램프와 디지털 라이트 프로젝션 시스템이 1밀리초 미만의 스위칭 속도와 자동차 등급 인증을 필요로 하기 때문에 전 세계 OEM 프로그램에 대응할 수 있는 공급업체의 범위가 좁아지고 있기 때문입니다. ams OSRAM은 자사의 ‘Digital Light’ 플랫폼에서 5억 유로(5억 6,400만 달러)를 넘는 설계 채택 실적을 보고했으며, 이는 유럽 LED 모듈 시장에서 용도 특화형 역량이 양산에 따른 경제성을 능가할 가능성이 있음을 시사합니다.

디지털 사이니지 및 광고 분야에서는 주간 가시성을 확보하기 위해 IP65 또는 IP67 보호 등급을 갖추고, 휘도가 10,000니트를 초과하는 실외용 모듈에 대한 의존도가 계속되고 있으며, 이 분야에서는 비용뿐만 아니라 성능도 중요하게 여겨지고 있습니다. 그 밖의 용도로는 건축 외관 조명, 450 nm 및 660 nm의 피크 파장에 최적화된 원예용 모듈, 265-280 nm에서 작동하는 UV-C 살균 모듈, 3,000K에서 6,500K까지 색온도(CCT)를 조절할 수 있는 수술용 조명 등이 있습니다. 현재의 용도 구성을 살펴보면, 범용적인 일반 조명 프로그램과 자동차, 원예, 디스플레이 백라이트와 같은 특수한 틈새 시장 사이에 뚜렷한 양극화가 나타나고 있습니다. 후자의 경우, 더 엄격한 공차, 더 긴 인증 기간, 그리고 더 높은 수준의 광학 요구 사항 덕분에 이익률이 유지되고 있습니다. 일반 조명은 여전히 판매량의 기반을 이루고 있지만, 특수 용도의 경우 신속하게 재현하기 어려운 인증 시험, 스펙트럼 조정, 시스템 통합이 필요하기 때문에 기술적 가치에서 더 큰 비중을 차지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSHAccording to Mordor Intelligence, the europe lED module market size is projected to be USD 1.45 billion in 2025, USD 1.64 billion in 2026, and reach USD 3.43 billion by 2031, growing at a CAGR of 15.89% from 2026 to 2031.

This report is Segmented by Module Type (COB LED Modules, SMD LED Modules, Linear LED Modules, LED Backlight Modules, and Other Module Types), Application (General Lighting, Automotive, Display and Backlighting, Signage, and Other Applications), Power Range (Low, Mid, and High), and Form Factor (Rigid LED Modules and Flexible LED Modules). The Market Forecasts are Provided in Terms of Value (USD).

Europe LED Module Market Trends and Insights

Rapid Phasing Out Of Incandescent Lighting Across EU

The mandatory withdrawal of incandescent and halogen lamps under Ecodesign Regulation (EU) 2019/2020, reinforced by energy-label rescaling in September 2024, removed legacy options from retail channels and pushed the Europe LED Module Market further toward LED-based replacement cycles in residential, commercial, and municipal uses. This change has favored modular LED products because facility managers and electrical contractors can replace modules more easily than complete luminaires, which lowers downtime and reduces spare-part complexity across installed fleets.Wedemark municipality in Germany showed how this shift works in practice when it retrofitted 4,300 LED lanterns, cut energy use by 80%, reduced annual consumption by 900,000 kWh, and avoided EUR 270,000 (USD 305,000) in costs, with module life rated at 120,000 hours. The transition has been especially favorable for SMD and COB suppliers because these formats fit common retrofit requirements for standardized sockets and thermal management across a wide set of luminaires. National enforcement by authorities such as Germany's Bundesnetzagentur and France's DGCCRF continues to support compliant suppliers by limiting the room for non-compliant imports and gray-market products in the Europe LED Module Market.

Energy Efficiency Targets Under European Green Deal

The European Green Deal target to reduce final energy consumption by 11.7% by 2030, backed by the Energy Efficiency Directive (EU) 2023/1791, creates a long-duration demand base for the Europe LED Module Market because LED modules can deliver up to 90% energy savings against incandescent alternatives. The policy framework also raises annual savings obligations to 1.9% during 2028-2030, which keeps lighting upgrades on procurement agendas for public bodies and commercial building operators across member states. European Commission assessments linked lighting upgrades to 41.9 TWh of annual electricity savings by 2030 and EUR 52 billion (USD 58.6 billion) in consumer savings, which keeps LED modules positioned as one of the lowest-cost pathways for abatement in buildings and municipal infrastructure. Article 8 procurement rules favor top energy-performance classes, which gives compliant module suppliers a clearer path into public tenders while keeping halogen and fluorescent options out of the main replacement cycle. Munich's adaptive street-lighting pilot, which tested tunable correlated color temperature from 3,000K to 1,700K and dimming profiles, showed energy reductions of up to 93% during low-traffic periods and pushed attention beyond simple lamp replacement toward networked LED systems with controls.

High Initial Capital Expenditure For LED Module Manufacturing

Building a competitive LED module line in Europe still requires EUR 50 million to EUR 150 million (USD 56 million to USD 169 million) in upfront spending on die-bonding tools, reflow ovens, automated optical inspection, and environmental chambers, which limits new entry and keeps capacity concentrated among established suppliers. This burden is heavier because technology shifts can strand equipment within 3-5 years as demand moves across power classes, substrates, and optical architectures. Smaller assemblers in Southern and Eastern Europe face a narrower financing window, and European Investment Bank lending for LED manufacturing totaled only EUR 250 million (USD 282 million) in 2025, which remains below what would be needed to support stronger domestic scaling. ams OSRAM's commitment of EUR 588 million (USD 663 million) through 2030 for its Austria expansion shows that the capital barrier is manageable mainly for companies with balance-sheet strength, policy support, or strategic semiconductor relevance The burden is felt more sharply in flexible and specialty segments because lower volumes and custom formats do not spread fixed costs as efficiently as general-lighting lines do in the Europe LED Module Market.

Other drivers and restraints analyzed in the detailed report include:

- Declining LED Cost Per Lumen

- Surge In European Commission Funding For Smart City Retrofits

- Supply Chain Disruptions For Semiconductor Chips

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SMD LED Modules held 33.43% of Europe LED Module Market share in 2025, which reflected their entrenched use in residential and commercial general lighting where standardized footprints such as 3528, 5050, and 2835 packages support automated assembly and interchangeability across luminaire brands. Backlight Modules are projected to grow at a 16.43% CAGR through 2026-2031 as consumer-electronics manufacturers shift toward mini-LED and micro-LED architectures that support higher contrast and denser local dimming. Philips underlined this shift with the October 2026 launch of the MLED981 RGB Mini-LED TV, which featured 11,520 local dimming zones and 2,500-nit peak brightness. COB modules continue to serve industrial high-bay and retail spotlight applications where thermal performance and lumen density support a 15% to 25% premium over SMD alternatives. Linear LED modules remain important in architectural cove lighting and under-cabinet installations because continuous-run formats fit narrow installation spaces and simplify the visual effect of uninterrupted light lines.

High-power LED modules above 30 W are also gaining traction in vertical farming, where photosynthetically active radiation efficacies of up to 3.5 μmol/J help Nordic facilities run controlled crop cycles across the year. Other module formats, including flexible strips, mini-LED arrays, and custom assemblies, are serving more specialized projects such as Arena Milano, where 54,560 bespoke linear LED bars spanning 50 km were specified for the 2026 Winter Olympics venue with IP67-rated RGBW modules and DMX512 control across 3,785 universes. Thermal management and color quality are shaping competitive positions inside this mix, because COB modules remain strong in applications that need CRI of 95 or more and R9 values above 80, while lower-cost SMD products continue to dominate utility lighting where CRI 80 is sufficient. Backlight modules face separate design demands such as sub-1 mm height limits and precise coupling with quantum-dot films, which keeps investments focused on flip-chip attachment and micro-lens arrays. Ecodesign compliance around flicker limits and minimum efficacy has pushed lower-tier SMD suppliers out of higher-quality categories and concentrated volume around Tier-1 manufacturers with stronger driver and thermal design capabilities in the Europe LED Module Market.

General Lighting accounted for 42.72% of the Europe LED Module Market size in 2025, as LED modules replaced fluorescent troffers, downlights, and high-bay fixtures across residential, commercial, and industrial settings. Display and Backlighting is expected to advance at a 16.78% CAGR through 2026-2031 as screen makers and vehicle manufacturers move toward local-dimming architectures in premium televisions, instrument clusters, and center-information displays. Premium TV demand in Western Europe supported this trend, with 65-inch and larger screens accounting for 38% of unit sales in 2025, which kept pressure on suppliers to deliver denser and brighter backlight systems.

Automotive Lighting remains a strategic segment because matrix LED headlamps and digital-light projection systems require sub-millisecond switching and automotive-grade qualification, which narrows the field of suppliers that can serve global OEM programs. ams OSRAM reported more than EUR 500 million (USD 564 million) in design wins for its Digital Light platform, showing how application-specific capability can outweigh volume economics in the Europe LED Module Market.

Signage and Advertising continue to depend on outdoor-rated modules with IP65 or IP67 protection and brightness levels above 10,000 nits for daylight readability, which keeps this segment tied to performance rather than only cost. Other applications span architectural facade lighting, horticulture modules optimized for 450 nm and 660 nm peaks, UV-C disinfection modules operating at 265-280 nm, and surgical lighting with adjustable CCT from 3,000K to 6,500K. The application mix now shows a clear split between commodity general-lighting programs and specialty niches such as automotive, horticulture, and display backlighting, where margins are supported by tighter tolerances, longer qualification periods, and stronger optical requirements. General lighting remains the volume base, but specialty applications keep a larger share of technical value because they demand qualification testing, spectral tuning, and system integration that are harder to replicate quickly.

List of Companies Covered in this Report:

- Signify N.V.

- Osram Opto Semiconductors GmbH

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- Cree LED

- Tridonic GmbH and Co KG

- Bridgelux, Inc.

- Citizen Electronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- Lextar Electronics Corporation

- LG Innotek Co., Ltd.

- Edison Opto Corporation

- Fagerhult Group

- Zumtobel Group AG

- Hella GmbH and Co. KGaA

- Stanley Electric Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Phasing-Out of Incandescent Lighting Across the EU

- 4.2.2 Energy-Efficiency Targets Under the European Green Deal

- 4.2.3 Declining LED Cost Per Lumen

- 4.2.4 Surge in European Commission Funding for Smart-City Retrofits

- 4.2.5 Growing Preference for Human-Centric Tunable-White Modules in Office Spaces

- 4.2.6 Demand Spike From Vertical-Farming Facilities in Nordics

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Expenditure for LED-Module Manufacturing

- 4.3.2 Supply-Chain Disruptions for Semiconductor Chips

- 4.3.3 Stringent Ecodesign Regulations Limiting Hazardous-Substance Use

- 4.3.4 Volatile Rare-Earth-Phosphor Prices Post-EU Critical Raw Materials Act

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 COB (chip-on-board) LED modules

- 5.1.2 SMD LED modules

- 5.1.3 Linear LED modules

- 5.1.4 LED backlight modules

- 5.1.5 High-power LED modules

- 5.1.6 Other module types (flexible, mini, custom assemblies)

- 5.2 By Application

- 5.2.1 General lighting

- 5.2.1.1 Residential

- 5.2.1.2 Commercial

- 5.2.1.3 Industrial

- 5.2.2 Automotive lighting

- 5.2.3 Display and backlighting

- 5.2.4 Signage and advertising

- 5.2.5 Other applications (architectural, horticulture, UV, specialty lighting)

- 5.2.1 General lighting

- 5.3 By Power Range

- 5.3.1 Low Power (less than or equal to 5 W)

- 5.3.2 Mid Power (greater than 5 W to less than or equal to 30 W)

- 5.3.3 High Power (greater than 30 W)

- 5.4 By Form Factor

- 5.4.1 Rigid LED modules

- 5.4.2 Flexible LED modules

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Osram Opto Semiconductors GmbH

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 Nichia Corporation

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Seoul Semiconductor Co., Ltd.

- 6.4.7 Cree LED

- 6.4.8 Tridonic GmbH and Co KG

- 6.4.9 Bridgelux, Inc.

- 6.4.10 Citizen Electronics Co., Ltd.

- 6.4.11 Everlight Electronics Co., Ltd.

- 6.4.12 Lextar Electronics Corporation

- 6.4.13 LG Innotek Co., Ltd.

- 6.4.14 Edison Opto Corporation

- 6.4.15 Fagerhult Group

- 6.4.16 Zumtobel Group AG

- 6.4.17 Hella GmbH and Co. KGaA

- 6.4.18 Stanley Electric Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment