|

시장보고서

상품코드

2065590

통합 커뮤니케이션(UC) 하드웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Unified Communications (UC) Hardware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

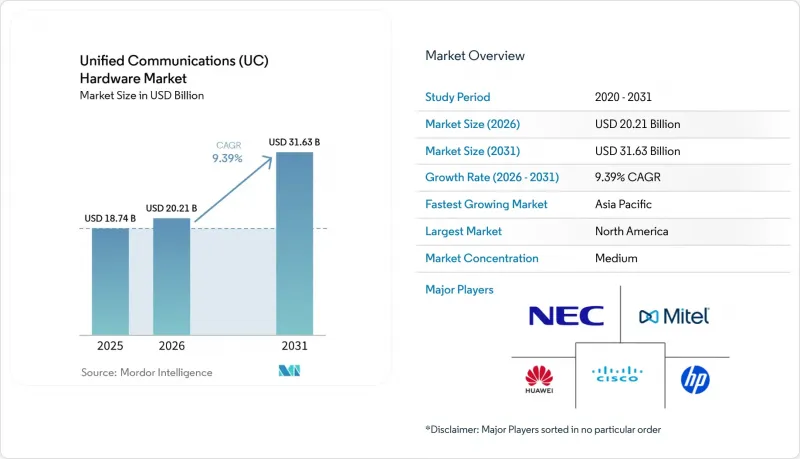

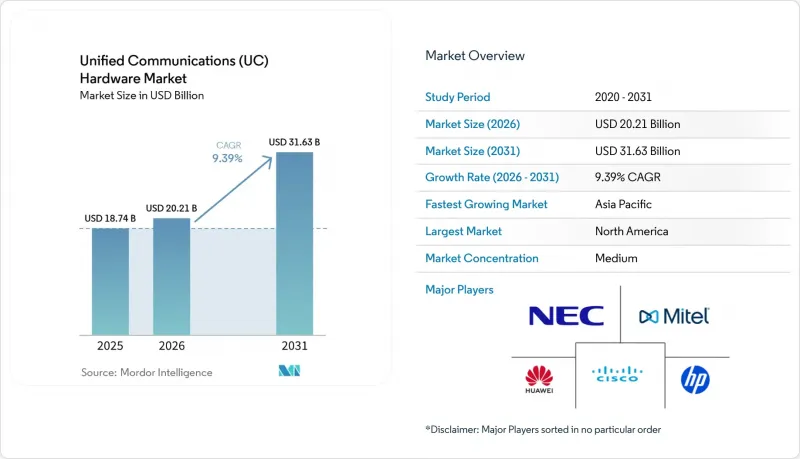

Mordor Intelligence에 의하면, 통합 커뮤니케이션(UC) 하드웨어 시장 규모는 2025년에 187억 4,000만 달러로 평가되었고, 2026년 202억 1,000만 달러로 추정되고, 2031년까지 316억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 9.39%를 나타낼 전망입니다.

본 보고서는 하드웨어 유형별(IP 전화 하드웨어, 화상 회의 시스템 등), 판매 모델별(오프라인, 온라인), 최종 사용자 산업 분야별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학 등), 조직 규모별(대기업, 중소기업) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 통합 커뮤니케이션(UC) 하드웨어 시장 동향 및 인사이트

하이브리드 근무 환경의 확산

상시적인 하이브리드 근무 체제가 정착됨에 따라, 기업들은 임시방편으로 사용하던 개인용 기기를, 일원화된 관리 및 보안 대책이 가능한 기업 인증 엔드포인트로 교체할 수밖에 없게 되었습니다. 가트너는 기기의 품질 저하가 직원의 약 3분의 2에게 디지털 마찰의 원인이 되고 있으며, 이로 인해 교체 주기가 3-4년으로 단축되고 있다고 지적했습니다. 시스코(Cisco) 등 벤더들은 AI 연산 기능을 탑재한 협업 보드를 제공함으로써 이에 대응하고 있으며, 이를 통해 외부 주변 기기가 필요 없어지고 원격 프로비저닝이 간소화되었습니다. 역할이나 회의실 유형별로 기기 구성을 표준화함으로써 지원 비용을 절감하고 사용자 경험을 향상시킬 수 있습니다. 이에 따라 고성능 UC 하드웨어는 인재의定着과 업무의 회복탄력성을 실현하는 전략적 요소로 자리매김하고 있습니다.

전사적인 화상 협업 수요의 급증

비디오 사용이 임원실에서 각 책상 및 소규모 회의실로 확대되면서, 모듈식 업그레이드가 가능한 확장형 시스템에 대한 수요를 이끌고 있습니다. Jabra의 ‘2026 PanaCast Room Kits’는 1대, 3대, 5대의 카메라 구성으로 제공되므로, IT 팀은 향후 확장성을 확보하면서 적절한 규모의 투자를 진행할 수 있습니다. 로지텍의 ‘Rally AI Camera Pro’는 2,999달러의 가격대에 듀얼 카메라의 지능형 기능을 탑재하여 넓은 공간에서의 시야 사각지대를 해소합니다. 스케줄링 패널을 통합함으로써 고가의 회의 공간을 효율적으로 활용하고, ‘유령 회의’를 줄이며, 부동산 활용을 최적화할 수 있습니다.

레거시 UC 엔드포인트의 평균 판매 가격 하락

Yealink 등 아시아 업체들은 현재 Microsoft Teams 인증 데스크폰을 유럽 및 미국의 기존 업체들보다 최대 40% 저렴한 가격에 제공하고 있어, 범용 하드웨어의 이익률을 압박하고 있습니다. 이러한 상품화 추세로 인해 구매자는 여러 공급업체로부터 엔드포인트를 조달할 수 있게 되었으며, 기존 공급업체들은 부가가치가 높은 소프트웨어를 번들로 제공하거나 AI 기능을 강화한 프리미엄 카테고리에 집중할 수밖에 없게 되었습니다. 각 벤더사는 Jabra Engage AI Complete와 같은 구독형 서비스를 통해 이에 대응하고 있습니다. 이 서비스는 음성 분석 및 텍스트 변환 기능을 사용자당 요금제에 통합하여, 하드웨어의 이익률 하락을 상쇄할 수 있는 지속적인 수익을 창출하고 있습니다.

부문별 분석

IP 전화 하드웨어는 여전히 가장 높은 매출을 기록하고 있으며, 2025년에는 통합 커뮤니케이션(UC) 하드웨어 시장에서 32.25%의 점유율을 차지했지만, 음성 기능이 보다 광범위한 협업 솔루션에 통합됨에 따라 성장세는 둔화되고 있습니다. 화상 회의 시스템은 가장 빠른 성장세를 기록하며, 2026-2031년 연평균 성장률(CAGR) 11.24%로 확대될 전망입니다. 기업들이 하이브리드 팀 전체를 아우르는 종합적인 회의 경험을 추구하는 가운데, 이 시스템은 새로운 기능에 대한 투자의 핵심으로 자리 잡고 있습니다.

엣지 AI 칩의 발전으로 인해, 카메라는 클라우드 컴퓨팅에 의존하지 않고도 실시간 화자 추적 및 음성 텍스트 변환이 가능해졌으며, 이를 통해 지연 시간을 줄이는 동시에 개인정보 보호 요건도 충족하게 되었습니다. 카메라, 마이크, 스피커, 코덱을 하나의 기기에 통합한 협업 바는 설치의 복잡성을 줄여주며, 신속한 도입 프로그램에서 선호되는 폼 팩터로 자리 잡고 있습니다. 강력한 소프트웨어 로드맵과 검증된 크로스 플랫폼 호환성을 갖춘 벤더들은 하드웨어 전문 경쟁사들을 계속해서 앞지르고 있습니다.

2025년에도 오프라인 판매 모델이 판매 채널의 주류를 차지하며, 총 매출의 68.27%를 차지했습니다. 이는 주로 대기업이나 미션 크리티컬한 환경에서 복잡한 회의실과의 통합이나 현장 지원이 필요하기 때문입니다. 그럼에도 불구하고, 온라인 채널은 틈새 시장에서의 선택지에서 주류 구매 경로로 빠르게 전환되고 있으며, 연평균 성장률(CAGR) 12.08%로 성장을 지속하고, 있습니다. 이러한 보급은 도입의 복잡성을 최소화한 USB 헤드셋이나 개인용 웹캠과 같은 표준화된 플러그 앤 플레이 제품에서 특히 두드러집니다.

이러한 변화를 활용하기 위해 각 제조업체들은 고객이 인증된 번들을 신속하고 효율적으로 구성하고 구매할 수 있는 직접 판매형 전자상거래 플랫폼 및 클라우드 기반 마켓플레이스에 대한 투자를 확대되고 있습니다. 중소기업(SME)은 투명한 가격 책정과 효율적인 조달 프로세스 덕분에 이러한 플랫폼을 특히 선호하여 이용하고 있습니다. 동시에, 시스코의 진화하는 파트너 전략과 같은 노력은 거래 중심의 판매가 점점 더 디지털 채널로 전환되는 가운데, 기존 재판매업체들이 부가가치가 더 높은 서비스 분야로 재편되고 있다는 업계 전반의 광범위한 변화를 반영하고 있습니다.

지역별 분석

북미는 견조한 기업용 장비 교체 주기와 FCC의 올-IP 현대화 계획에 힘입어 2025년 매출 점유율의 34.82%를 차지했습니다. 미국 기업들은 엄격한 보안 지침을 충족하는 AI 탑재 기기를 계속해서 우선시하고 있는 반면, 캐나다에서는 공공 부문의 활발한 수요가 기업들의 지출을 보완하고 있습니다. 멕시코는 국경을 초월한 공급망 통합과 조립 업무의 니어쇼어링을 촉진하는 USMCA(미국·멕시코·캐나다 협정)의 인센티브 혜택을 누리고 있습니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 11.92%를 기록할 전망이며, 지역별로는 가장 높은 성장률을 보일 것으로 전망됩니다. 중국에서 국가 주도로 추진되는 AI 정책과 도시 차원의 스마트 오피스 도입 의무화는 화웨이와 ZTE 같은 국내 대기업들에게 유리하게 작용하고 있습니다. 인도의 2급 도시들은 정부 주도의 디지털화 프로그램에 따라 시청과 학교로의 광섬유 연결이 확대되고 있어, 새로운 주목받는 지역으로 부상하고 있습니다. 일본과 한국은 성숙한 5G 네트워크를 활용해 모바일 중심의 협업 솔루션을 전개하고 있는 반면, 호주는 광활한 지역에 흩어져 있는 광업 및 에너지 시설을 지원하기 위해 내환경성이 뛰어나고 위성 통신이 가능한 장비에 의존하고 있습니다.

유럽의 전망은 2027년 1월로 예정된 영국의 PSTN(공중전화망) 폐지에 따라 독특한 양상을 띠고 있으며, 기업들이 구리선에 의존하는 장비를 교체함에 따라 단계적으로 조달 수요가 급증하고 있습니다. 규모 면에서는 독일과 프랑스가 그 뒤를 잇고 있지만, 엄격한 GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정) 요건으로 인해 수요는 하이브리드형 또는 온프레미스형 아키텍처 쪽으로 쏠리고 있습니다. 남미의 성장은 브라질과 아르헨티나에 집중되어 있으며, 광대역 환경의 개선으로 중소기업들이 클라우드 네이티브 UC로 직접 전환할 수 있게 되었습니다. 중동에서는 사우디아라비아의 국가 AI 계획과 엑스포를 계기로 한 인프라 확충으로 인해, 비록 불규칙적이긴 하지만 수익성이 높은 입찰 기회가 생겨나고 있습니다. 한편, 아프리카는 여전히 초기 단계의 기회로 남아 있으며, 남아프리카공화국, 나이지리아, 케냐에 집중되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the unified communications (UC) hardware market size was valued at USD 18.74 billion in 2025 and estimated to grow from USD 20.21 billion in 2026 to reach USD 31.63 billion by 2031, at a CAGR of 9.39% during the forecast period (2026-2031).

This report is Segmented by Hardware Type (IP Telephony Hardware, Video Conferencing Systems, and More), Distribution Model (Offline, and Online), End-User Industry (IT and Telecommunication, BFSI, Healthcare and Life Sciences, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Unified Communications (UC) Hardware Market Trends and Insights

Increasing Adoption of Hybrid Work Environments

Permanent hybrid schedules are compelling organizations to replace ad-hoc consumer devices with enterprise-certified endpoints that can be centrally managed and secured. Gartner has noted that poor device quality contributes to digital friction for roughly two-thirds of employees, prompting refresh cycles to shrink to three-to-four years. Vendors such as Cisco have responded with collaboration boards that embed AI compute, eliminating the need for external peripherals and simplifying remote provisioning. Standardizing device portfolios by role and room type reduces support costs and improves the user experience, positioning high-performance UC hardware as a strategic enabler of talent retention and operational resilience.

Surge in Enterprise-Wide Video Collaboration Demand

Video usage has expanded from executive suites to every desk and huddle room, driving demand for scalable systems that support modular upgrades. Jabra's 2026 PanaCast Room Kits, offered in one-, three-, and five-camera variants, allow IT teams to right-size investments while preserving future expansion paths. Logitech's Rally AI Camera Pro introduces dual-camera intelligence at the USD 2,999 price point, addressing visibility gaps in large spaces. Integration of scheduling panels ensures that expensive meeting spaces are utilized efficiently, reducing "ghost meetings" and optimizing real estate.

Declining Average Selling Prices of Legacy UC Endpoints

Asian vendors such as Yealink now offer Microsoft Teams-certified desk phones at prices up to 40% below Western incumbents, eroding margins on commodity hardware. The commoditization trend enables buyers to source endpoints from multiple suppliers, forcing legacy providers to bundle value-added software or shift focus to premium AI-enhanced categories. Vendors have responded with subscription offerings like Jabra Engage AI Complete, which fuses tone analytics and transcription into a per-user fee, creating recurring revenue to offset lower hardware margins.

Other drivers and restraints analyzed in the detailed report include:

- Migration from PSTN to IP-Based Telephony Systems

- Cost Efficiencies Achieved Through Equipment Consolidation

- Security Concerns Around SIP and VoIP Gateways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IP telephony hardware still generated the highest category revenue, holding a 32.25% Unified Communications Hardware market share in 2025, yet its growth rate is moderating as voice becomes an embedded feature within broader collaboration suites. Video conferencing systems recorded the fastest growth, advancing at an 11.24% CAGR between 2026 and 2031. They remain the focal point of new feature investment as enterprises seek inclusive meeting experiences across hybrid teams.

Advances in edge-AI silicon now allow cameras to perform real-time speaker tracking and language transcription without relying on cloud compute, reducing latency and meeting privacy mandates. Collaboration bars that integrate a camera, microphone, speaker, and codec into a single device lower installation complexity and have become a preferred form factor for rapid rollout programs. Vendors with strong software roadmaps and certified cross-platform compatibility continue to displace pure-play hardware competitors.

Offline distribution model continued to dominate the distribution landscape in 2025, accounting for 68.27% of total revenue, largely due to the need for complex room integrations and on-site support in large enterprises and mission-critical environments. Despite this, online channels are rapidly transitioning from a niche option to a mainstream purchasing route, growing at a CAGR of 12.08%. Their adoption is particularly strong for standardized, plug-and-play products such as USB headsets and personal webcams, where deployment complexity is minimal.

To capitalize on this shift, manufacturers are expanding investments in direct e-commerce platforms and cloud-based marketplaces that allow customers to configure and purchase certified bundles quickly and efficiently. Small and medium-sized enterprises (SMEs) are particularly inclined toward these platforms due to transparent pricing and streamlined procurement processes. At the same time, initiatives like Cisco's evolving partner strategy reflect a broader industry transition, where traditional resellers are being repositioned toward higher-value services as transactional sales increasingly migrate to digital channels.

Geography Analysis

North America captured 34.82% revenue share in 2025, buoyed by robust enterprise refresh cycles and the FCC's all-IP modernization agenda. United States enterprises continue to prioritize AI-infused devices that meet stringent security guidelines, while Canada's strong public-sector demand complements corporate spending. Mexico benefits from cross-border supply-chain integration and USMCA incentives that encourage nearshoring of assembly operations.

Asia-Pacific is projected to record the fastest regional growth at an 11.92% CAGR between 2026-2031. China's sovereign AI push and city-level smart-office mandates favor domestic champions such as Huawei and ZTE. India's tier-2 cities are emerging hotspots as government-led digitization programs extend fiber connectivity to municipal buildings and schools. Japan and South Korea leverage mature 5G networks to roll out mobile-centric collaboration solutions, while Australia relies on ruggedized, satellite-ready gear to support mining and energy installations spread across vast distances.

Europe's outlook is uniquely shaped by the United Kingdom's January 2027 PSTN switch-off, which is generating staggered procurement spikes as enterprises replace copper-dependent devices. Germany and France are next in scale, although strict GDPR requirements tilt demand toward hybrid or on-premises architectures. South American growth is clustered in Brazil and Argentina, where improved broadband is allowing SMEs to leapfrog directly to cloud-native UC. In the Middle East, Saudi Arabia's national AI plan and Expo-driven infrastructure upgrades create lumpy but lucrative tenders, while Africa remains an early-stage opportunity concentrated in South Africa, Nigeria, and Kenya.

- Cisco Systems, Inc.

- Avaya LLC

- HP Inc.

- Mitel Networks Corporation

- NEC Corporation

- Unify Software and Solutions GmbH and Co. KG

- 8x8, Inc.

- Alcatel-Lucent Enterprise International

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Grandstream Networks, Inc.

- Yealink Network Technology Co., Ltd.

- Ribbon Communications Inc.

- Sangoma Technologies Corporation

- AudioCodes Ltd.

- GN Audio A/S (Jabra)

- Logitech International S.A.

- Crestron Electronics, Inc.

- Lifesize Communications, Inc.

- ClearOne, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Hybrid Work Environments

- 4.2.2 Surge in Enterprise-Wide Video Collaboration Demand

- 4.2.3 Migration From PSTN to IP-Based Telephony Systems

- 4.2.4 Cost Efficiencies Achieved Through Equipment Consolidation

- 4.2.5 Rise of Hardware-Optimised UCaaS Gateways in Emerging Markets

- 4.2.6 Growing Integration of AI-Enabled Audio Peripherals

- 4.3 Market Restraints

- 4.3.1 Declining Average Selling Prices of Legacy UC Endpoints

- 4.3.2 Security Concerns Around SIP and VoIP Gateways

- 4.3.3 Persistent Supply-Chain Chips Shortage in Networking ASICs

- 4.3.4 Environmental Regulations Limiting Single-Use Plastics in Headsets

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Hardware Type

- 5.1.1 IP Telephony Hardware

- 5.1.2 Video Conferencing Systems

- 5.1.3 UC Gateways and Infrastructure Hardware

- 5.1.4 Headsets and Audio Devices

- 5.1.5 Collaboration Bars/Room Kits

- 5.1.6 Other Hardware Types

- 5.2 By Distribution Model

- 5.2.1 Offline

- 5.2.2 Online

- 5.3 By End-user Industry

- 5.3.1 IT and Telecommunication

- 5.3.2 BFSI

- 5.3.3 Healthcare and Lifesciences

- 5.3.4 Retail and Consumer Goods

- 5.3.5 Education

- 5.3.6 Government and Public Sector

- 5.3.7 Manufacturing

- 5.3.8 Media and Entertainment

- 5.3.9 Other Industry Verticals

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Avaya LLC

- 6.4.3 HP Inc.

- 6.4.4 Mitel Networks Corporation

- 6.4.5 NEC Corporation

- 6.4.6 Unify Software and Solutions GmbH and Co. KG

- 6.4.7 8x8, Inc.

- 6.4.8 Alcatel-Lucent Enterprise International

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 ZTE Corporation

- 6.4.11 Grandstream Networks, Inc.

- 6.4.12 Yealink Network Technology Co., Ltd.

- 6.4.13 Ribbon Communications Inc.

- 6.4.14 Sangoma Technologies Corporation

- 6.4.15 AudioCodes Ltd.

- 6.4.16 GN Audio A/S (Jabra)

- 6.4.17 Logitech International S.A.

- 6.4.18 Crestron Electronics, Inc.

- 6.4.19 Lifesize Communications, Inc.

- 6.4.20 ClearOne, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment