|

시장보고서

상품코드

2065622

남미의 관개 펌프 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South America Irrigation Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

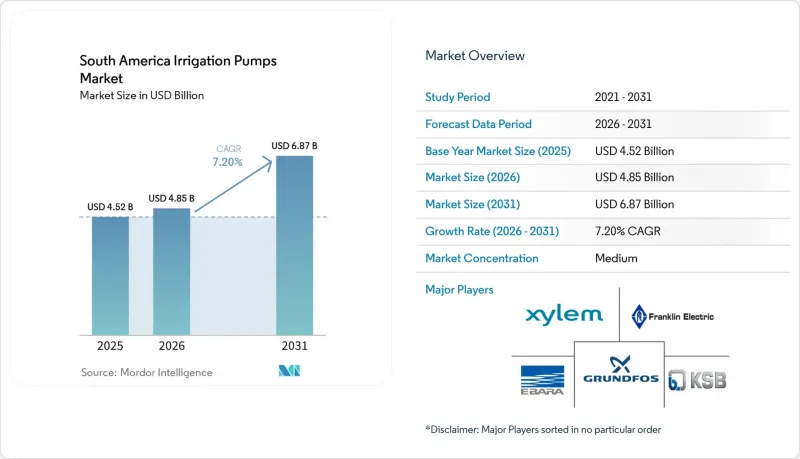

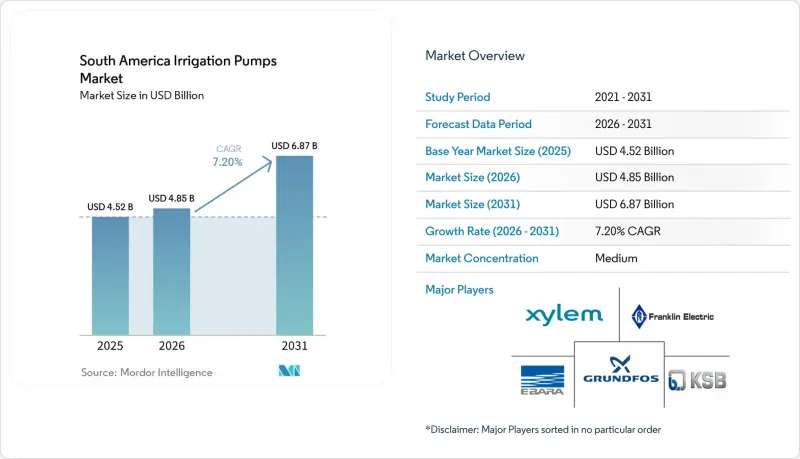

Mordor Intelligence에 의하면, 남미 관개 펌프 시장 규모는 2025년에 45억 2,000만 달러로 평가되었고 2026년 48억 5,000만 달러에서 2031년까지 68억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.20%를 나타낼 전망입니다.

본 보고서는 제품 유형별(원심 펌프, 수중 펌프, 용적식 펌프, 와류 펌프), 동력원별(상용 전원식 펌프, 디젤 펌프, 태양광 펌프, 태양광·디젤 하이브리드 펌프, 태양광·배터리 하이브리드 펌프), 지역별(브라질, 아르헨티나, 칠레, 페루, 콜롬비아 및 기타 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

남미 관개 펌프 시장 동향 및 분석

관개 네트워크의 확장 및 현대화

관개용지의 확대는 남미의 관개 펌프 시장에 있어 여전히 가장 뚜렷한 성장 요인으로 작용하고 있습니다. 이는 새로운 용수로, 양수 시설 및 농경지 시스템에는 처음부터 다양한 유형의 펌프가 필요하기 때문입니다. 유엔 식량농업기구(FAO)의 보고서에 따르면, 남미에서는 지난 10년 동안 관개 면적이 꾸준히 확대되어 왔으며, 이는 연작 및 수출용 농업 분야의 관개 시설에 대한 장기적인 계획 주기를 뒷받침하고 있습니다. 페루 정부는 2025년까지 총 투자액 240억 달러, 100만 헥타르의 추가 확대를 목표로 삼고, 주로 민관협력(PPP) 주도의 실행 모델을 통해 22건의 관개 프로젝트를 발표했습니다. 브라질 역시 새로운 공공 프로그램과 주 차원의 체계를 통해 관개 투자에 대한 제도적 기반을 확대하고 있으며, 이를 통해 상업 농장과 소규모 농장 모두에서 펌프를 보다 안정적으로 조달할 수 있게 되었습니다. 또한, 새로운 네트워크가 구축될 때마다 펌프장의 업그레이드, 제어 시스템 및 교체용 유닛과 관련된 장기적인 서비스 주기가 형성됩니다. 이를 통해 수직 통합형 공급업체는 초기 판매에만 주력하는 기업보다 더 안정적인 사후 시장 기회를 확보할 수 있습니다. 이러한 추세로 인해 남미의 관개 펌프 시장은 신규 프로젝트뿐만 아니라 지속적인 유지보수 지출과도 밀접하게 연관되어 있습니다.

물 부족이 관개 인프라 수요를 견인하고 있습니다.

물 부족 문제로 인해 많은 농장에서 관개에 대한 지출이 단순히 수확량 증대를 위한 선택지에서 위험 관리상의 필수 요건으로 변화하고 있으며, 이로 인해 남미 관개 펌프 시장 수요 구조가 변화하고 있습니다. Assessment Capacities Project(ACAPS)에 따르면, 2023년부터 2024년까지 브라질의 59%가 가뭄의 영향을 받았으며, 이는 생산자들이 안정적인 물 공급과 기존 양수 설비에 더 큰 중요성을 두게 된 이유를 뒷받침합니다. 브라질에서는 2023년부터 2025년까지 반복된 가뭄으로 인해, 가뭄의 영향을 쉽게 받는 주에 있는 더 많은 농가들이 전면 관개 또는 부분 관개 생산 시스템으로 전환하게 되었으며, 그 결과 시추 우물 및 수중 펌프에 대한 관심이 높아졌습니다. 이와 유사한 압박은 페루의 해안 지역이나 아르헨티나의 건조한 지역에서도 나타나고 있으며, 그곳에서는 신뢰할 수 있는 양수 설비가 단순한 예비 수단이 아니라 재배 계획의 핵심 요소로 자리 잡고 있습니다. 또 다른 영향은 그리 바람직하지 않습니다. 대수층의 수위 저하로 인해 수중 펌프 설비의 수명이 단축되어, 연간 교체 수요가 증가할 가능성이 있기 때문입니다. 즉, 가뭄은 단기적인 장비 판매를 촉진하는 한편, 일부 펌프 설비의 경우 운영 환경을 더욱 어렵게 만들고 있습니다.

높은 초기 투자 비용

높은 초기 투자 비용은 여전히 수요에 명백한 걸림돌이 되고 있으며, 특히 높은 양정을 필요로 하는 보홀 시스템이나 대형 원심 펌프가 필요한 농가들이 보조금 지원 대출 대상에서 제외되는 경우에 그 현상이 두드러집니다. 실제로 이 문제는 콜롬비아와 아르헨티나의 중소규모 농가들에게 가장 심각한 문제이며, 이러한 지역에서는 펌프에 대한 투자가 운전 자금 수요나 계절적 자금 사정 압박과 상충되는 경우가 종종 있습니다. 따라서 남미의 관개 펌프 시장에서는 물 부족으로 인해 관개 필요성이 높아지고 있는 경우에도, 잠재적 수요가 모두 구매로 이어지는 것은 아닙니다. 이러한 자금 조달 격차는 공공 대출 프로그램이 보다 잘 갖춰진 브라질의 일부 지역에서는 그리 심각하지 않지만, 차입자가 우대 프로그램의 기준 금액을 초과하거나 대출 기관이 요구하는 담보를 제공할 수 없는 경우에는 여전히 도입의 걸림돌이 되고 있습니다. 그 결과, 대규모 상업 농장일수록 조기에 설비를 교체하는 반면, 소규모 사업자는 장비 교체나 신규 도입을 미루는 등 지역별 격차가 발생하고 있습니다. 이러한 불균형으로 인해 대규모 농장 수요는 견조한 추세를 보이고 있음에도 불구하고, 고객 기반의 확대는 주춤하고 있습니다.

부문별 분석

2025년에는 원심 펌프가 49.9%라는 최대 시장 점유율을 차지하고 있으며, 이러한 주도적 지위는 브라질과 아르헨티나의 대규모 곡물·사탕수수 산지에서 널리 채택되고 있는 지표 관개 시스템 및 수로 연계형 배치 방식과의 적합성을 반영하고 있습니다. 남미의 관개 펌프 시장에서 엔드 흡입형 및 스플릿 케이스형 원심 펌프는 설치 공간의 절약보다는 대유량이나 수평 송수가 중시되는 상황에서 여전히 표준적인 선택지로 자리 잡고 있습니다. 또한, 페루 해안 지역의 관개 프로젝트에서는 수직 터빈식 펌프도 중요한 역할을 하고 있습니다. 이는 이러한 시스템에서 하천 취수구나 대수층에서 물을 퍼 올려 용수로망으로 보내야 하는 경우가 많기 때문입니다. 수중 펌프는 지하수 개발이 확대되고 있는 지역, 특히 페루의 계곡 지대나 브라질 북동부의 건조한 지역에서 이용이 증가하고 있습니다. 볼텍스 펌프 시장 규모는 여전히 작지만, 물에 토사가 포함되어 있어 일반적인 지표용 펌프로는 가동상 제약이 발생하는 장소에서는 여전히 중요한 역할을 하고 있습니다.

남미의 관개 펌프 시장에서 용적식 펌프 시장 규모는 2031년까지 연평균 성장률(CAGR) 5.2%로 확대될 것으로 예상되며, 예측 기간 동안 가장 빠르게 성장할 제품 카테고리가 될 전망입니다. 이러한 성장은 대량 이송보다 정확한 유량 제어가 중시되는 비료 관개, 점적 관개 시스템 및 지하 관개 시스템과 밀접한 관련이 있습니다. 페루에서는 2025년에 15개 지역에 걸친 관개 프로젝트가 승인되었으며, 기술 기반 관개에 중점을 두고 있습니다. 이로 인해 제어식 살포 시스템에 적합한 펌프 유형에 대한 수요가 증가하고 있습니다. 용적식 펌프는 페루와 칠레의 수출 지향적 원예 농업에서도 혜택을 보고 있으며, 이들 지역에서는 높은 물 이용 효율이 고부가가치 관개 장비의 도입을 촉진하고 있습니다. 따라서 남미의 관개 펌프 업계에서는 물 공급의 정확도가 작물의 품질 및 비료 관리와 밀접한 관련이 있는 분야에서 더욱 빠른 성장이 나타나고 있습니다. 또한, 인증된 수력 성능이 중시되는 프로젝트에서 국제표준화기구(ISO) 9906 표준 준수가 점점 더 중요해지고 있으며, 사양 요건이 까다로운 입찰에서 대형 공급업체에게 경쟁 우위를 제공합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the south america irrigation pumps market size was valued at USD 4.52 billion in 2025 and is estimated to grow from USD 4.85 billion in 2026 to reach USD 6.87 billion by 2031, at a CAGR of 7.20% during the forecast period (2026-2031).

This report is Segmented by Product Typem(Centrifugal Pumps, Submersible Pumps, Positive Displacement Pumps, and Vortex Pumps), by Power Source (Grid-Electric Pumps, Diesel Pumps, Solar Pumps, and Hybrid Solar-Diesel and Solar-Battery Pumps), and by Geography (Brazil, Argentina, Chile, Peru, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

South America Irrigation Pumps Market Trends and Insights

Irrigation Network Expansion and Modernization

Expansion of irrigated land remains the clearest growth driver for the South America irrigation pumps market because new canals, lift stations, and field systems require a broad mix of pump types from the start. The Food and Agriculture Organization (FAO) showed that South America sustained strong irrigated area growth over the last decade, which supports long planning cycles for irrigation equipment across row crops and export agriculture. Peru's government presented 22 irrigation projects in 2025 with total investment of USD 24 billion, a target of 1 million additional hectares, and a delivery model led mainly by public-private partnerships (PPPs). Brazil also expanded the institutional base for irrigation investment through new public programs and state-level frameworks, which makes pump procurement more repeatable across both commercial farms and smaller operations. Each new network also creates a long service cycle for station upgrades, controls, and replacement units, which gives vertically integrated suppliers a steadier aftermarket opportunity than firms focused only on first-time sales. That pattern is keeping the South America irrigation pumps market tied not only to greenfield projects, but also to recurring maintenance spending.

Water Scarcity Driving Demand for Irrigation Infrastructure

Water stress is shifting irrigation spending from a yield improvement choice into a risk management requirement for many farms, and that is changing the demand profile of the South America irrigation pumps market. According to Assessment Capacities Project (ACAPS), drought conditions affected 59% of Brazil during the 2023 to 2024 cycle, which underlines why producers are placing more weight on secure water access and installed pumping capacity. In Brazil, recurring drought from 2023 through 2025 pushed more farms in exposed states toward fully irrigated or partially irrigated production systems, which increased interest in borehole and submersible units. The same pressure is visible in Peru's coastal belts and in drier parts of Argentina, where dependable pumping is becoming central to crop planning rather than a backup option. A second effect is less favorable, because aquifer drawdown can reduce the working life of submersible installations and raise annual replacement demand. That means drought is supporting near-term equipment sales while also creating a harder operating environment for some pump assets.

High Upfront Capital Costs

High capital cost remains a clear brake on demand, especially where growers need high-head borehole systems or larger centrifugal units and do not qualify for subsidized financing. In practical terms, the issue is strongest for smallholders and medium farms in Colombia and Argentina, where pump investment often competes with working capital needs and seasonal cash flow pressure. The South America irrigation pumps market therefore does not convert all latent demand into purchases, even when water stress makes irrigation more necessary. This funding gap is less severe in parts of Brazil, where public credit programs are more developed, but it still limits adoption where borrowers exceed concessional program thresholds or cannot provide the supporting structure required by lenders. The result is a tiered regional pattern in which larger commercial farms upgrade sooner while smaller operators delay replacement and postpone new installations. That imbalance slows the broadening of the customer base even as demand from large farms remains resilient.

Other drivers and restraints analyzed in the detailed report include:

- Subsidized Government Pump Financing Programs

- Solar and Hybrid Pumping Adoption on Off-Grid Farms

- Rural Grid Limitations Constraining Electric Pump Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal pumps held the largest market share at 49.9% in 2025, and that leadership reflects their fit with the surface irrigation systems and canal-linked layouts used across large grain and sugarcane areas in Brazil and Argentina. In the South America irrigation pumps market, end-suction and split-case centrifugal models remain the standard choice where high volumes and horizontal delivery matter more than compact installation. Vertical turbine units also hold an important place in Peru's coastal irrigation projects because those systems often need water lifted from river intakes or aquifers into canal networks. Submersible pumps are gaining use where groundwater development is expanding, especially in Peru's valleys and in drier parts of northeastern Brazil. Vortex pumps remain smaller in volume, but they retain relevance where water carries sediment and basic surface units face operating limits.

The South America irrigation pumps market size for positive displacement pumps is projected to grow at a 5.2% CAGR through 2031, making them the fastest product category over the forecast period. That growth is tied to fertigation, drip systems, and subsurface irrigation layouts where accurate flow control matters more than bulk transfer. Peru approved irrigation projects across 15 regions in 2025 with a technified irrigation focus, which supports demand for pump types suited to controlled application systems. Positive displacement equipment is also benefiting from export-oriented horticulture in Peru and Chile, where water efficiency supports the case for higher-value irrigation hardware. The South America irrigation pumps industry is therefore seeing faster growth in applications where water delivery precision is closely linked to crop quality and fertilizer management. International Organization for Standardization (ISO) 9906 compliance is also becoming more relevant in projects that favor certified hydraulic performance, which gives larger suppliers an advantage in specification-heavy tenders.

List of Companies Covered in this Report:

- Franklin Electric Co., Inc.

- KSB SE & Co. KGaA

- Grundfos Holding A/S

- Xylem Inc.

- Ebara Corporation

- Wilo SE

- Flowserve Corporation

- Sulzer Ltd

- ITT Inc.

- Jimenez Motores e Sistemas de Irrigacao Ltda

- Pentair plc

- Ruhrpumpen GmbH

- Dover Corporation

- IDEX Corporation

- Hidromecanica Germek Ltda.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Irrigation network expansion and modernization

- 4.2.2 Water scarcity driving demand for irrigation infrastructure

- 4.2.3 Subsidized government pump financing programs

- 4.2.4 Solar and hybrid pumping adoption on off-grid farms

- 4.2.5 Diesel-to-solar pump transitions

- 4.2.6 PPP-led co-investment in rural water infrastructure

- 4.3 Market Restraints

- 4.3.1 High upfront capital costs

- 4.3.2 Rural grid limitations constraining electric pump deployment

- 4.3.3 Basin configuration and hydrology constraints

- 4.3.4 Water-right allocation and regulatory barriers

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Centrifugal Pumps

- 5.1.2 Submersible Pumps

- 5.1.3 Positive Displacement Pumps

- 5.1.4 Vortex Pumps

- 5.2 By Power Source

- 5.2.1 Grid-electric Pumps

- 5.2.2 Diesel Pumps

- 5.2.3 Solar Pumps

- 5.2.4 Hybrid Solar-Diesel and Solar-Battery Pumps

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Chile

- 5.3.4 Peru

- 5.3.5 Colombia

- 5.3.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Franklin Electric Co., Inc.

- 6.4.2 KSB SE & Co. KGaA

- 6.4.3 Grundfos Holding A/S

- 6.4.4 Xylem Inc.

- 6.4.5 Ebara Corporation

- 6.4.6 Wilo SE

- 6.4.7 Flowserve Corporation

- 6.4.8 Sulzer Ltd

- 6.4.9 ITT Inc.

- 6.4.10 Jimenez Motores e Sistemas de Irrigacao Ltda

- 6.4.11 Pentair plc

- 6.4.12 Ruhrpumpen GmbH

- 6.4.13 Dover Corporation

- 6.4.14 IDEX Corporation

- 6.4.15 Hidromecanica Germek Ltda.