|

시장보고서

상품코드

2072953

유럽의 관개 펌프 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Irrigation Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

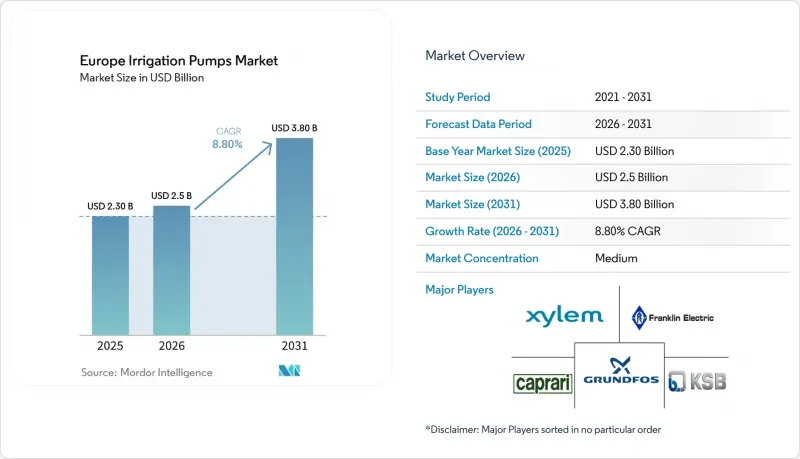

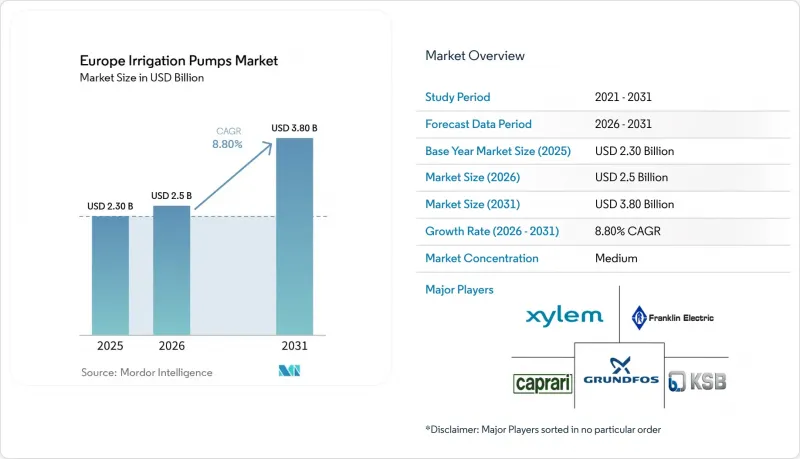

Mordor Intelligence에 의하면, 유럽 관개 펌프 시장 규모는 2025년에 23억 달러, 2026년에 25억 달러되어, 2031년까지 38억 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 8.80%로 성장할 전망입니다.

본 보고서는 제품 유형별(원심 펌프, 수중 펌프, 용적식 펌프, 소용돌이 펌프), 동력원별(상용 전력, 디젤, 태양광, 태양광·디젤 하이브리드, 태양광·배터리 하이브리드), 지역별(독일, 영국, 프랑스, 스페인, 이탈리아, 러시아 및 기타 유럽)으로 분류되어 있습니다. 시장 전망은 달러 기준 금액으로 제시되어 있습니다.

유럽 관개 펌프 시장 동향 및 분석

물 부족을 배경으로 한 구형 관개 펌프의 개보수

유럽의 관개 펌프 시장에서 물 부족 문제는 더 이상 계절적인 운영상의 문제로 간주되지 않습니다. 이미 취수가 어려운 유역에서는 물 부족 문제가 시설 갱신을 위한 행정적 계기가 되고 있습니다. 유럽연합 공동연구센터(JRC)는 2026년 2월, 유럽 대부분의 지역에서 인간 활동으로 인해 재생 가능한 담수의 10%에서 50%가 소비되고 있다고 보고했으며, 특히 남부 및 지중해 연안 지역에서는 과다 이용으로 인한 압박이 가장 심한 것으로 나타났습니다. 이러한 상황에서 유량 측정 기능이 없어 현재의 모니터링 요구 사항을 쉽게 충족할 수 없는 구형 정속 설비의 교체가 진행되고 있습니다. 사실, 생산자들은 단순히 새로운 펌프를 구입하는 것뿐만이 아닙니다. 그들은 유량을 모니터링하고 제어 기능을 지원하며, 더욱 엄격해진 유역 관리 규정을 준수할 수 있는 시스템으로 구식 관개 설비를 교체하고 있습니다.

공통농업정책(CAP)에 기반한 관개 현대화를 위한 지출

공통농업정책(CAP)의 지출 주기는 여전히 유럽 관개 펌프 시장에 있어 가장 확실한 지원 요인 중 하나입니다. 2021년부터 2027년까지의 계획에 따른 투자액은 314억 유로(339억 달러)에 달하며, 이는 제73조 및 제74조에 근거한 농업·관개 프로젝트에 대한 유럽연합(EU) 및 각국의 공동 자금 지원을 포함하고 있습니다. 2025년 제안에서는 다음 정책 주기에서도 수자원 관리와 토양의 건전성이 계속해서 중시되고 있으며, 단일 기간에 한정된 지원이 아닌 지속성이 시사되고 있습니다. 프랑스, 스페인, 독일, 이탈리아는 공동농업정책(CAP)의 지원을 가장 많이 받고 있을 뿐만 아니라 대규모 관개 현대화 프로젝트를 추진하고 있어, 여전히 가장 활발한 국가 자금 지원의 중심지 역할을 하고 있습니다. 중요한 점은 보조금 승인 전에 수량 계측 장치의 설치가 종종 의무화되어 있다는 것입니다. 이 규정에 따라 노후화된 펌프 설비는 순전히 자발적인 지출 주기가 아닌, 규제에 따른 교체 일정을 따르게 됩니다.

중소규모 농장의 펌프 시스템에 필요한 고액의 초기 설비 투자

자본 비용은 유럽의 관개 펌프 시장에서 여전히 가장 뚜렷한 수요 억제요인으로 작용하고 있습니다. 펌프, 가변 주파수 구동 장치, 계량 기기 및 설치를 포함한 시스템 전체의 업그레이드는 계절적 현금 흐름이 어려운 농장에게 여전히 큰 부담이 되고 있습니다. 유럽연합(EU) 규정 2021/2115에 따르면, 대상 투자 비용에 대한 지원이 허용되고 있지만, 나머지 자비 부담분은 많은 중소규모 농장, 특히 중동부 유럽 회원국에서 현실적인 기계 구입 예산을 계속해서 압박하고 있습니다. 지원금이 지급 결정 시점보다 훨씬 뒤늦게 지급되는 경우가 있기 때문에 상환 시기도 문제의 일부가 되고 있습니다. 공급업체들은 모듈식 펌프 스테이션 형태로 이에 대응하고 있지만, 비용 절감 효과는 아직 충분하지 않아 소규모 사업자들이 턴키 방식의 업그레이드를 쉽게 이용할 수 있는 상황은 아닙니다. 그 결과, 대규모 생산자, 협동조합, 관개 단체 등 자본 비용을 더 많은 헥타르나 이용자 수로 분담할 수 있는 곳에서 도입이 가장 활발히 이루어지고 있습니다.

부문별 분석

2025년, 원심 펌프는 가장 큰 시장 점유율을 차지하며, 유럽 관개 펌프 시장 점유율의 71.2%를 차지했습니다. 이 지위는 밭작물 및 원예 두 분야 모두에서 지표수 취수, 개방 수로 관개, 우물과 연계된 농장 시스템 등 폭넓은 용도로 활용되고 있음을 반영하고 있습니다. 수요가 가장 높은 곳은 특정 작물 재배 체계에 국한되지 않고, 다양한 양정 및 유량 조건에 대응할 수 있는 사업자들이 익숙하게 사용하는 유연한 솔루션을 필요로 하는 지역입니다. 대규모 공공 및 컨소시엄 주도의 관개 사업에서도 특히 수직 터빈형이나 스플릿 케이스형 원심 펌프가 계속해서 채택되고 있습니다. 카프라리(Caprari S.p.A.)는 2024년, 이탈리아 시글리아티(Scigliati) 플랜트 프로젝트를 통해 이러한 역량을 입증했습니다. 이 프로젝트에서는 5기의 맞춤형 수직 라인 샤프트 유닛을 도입함으로써 유역의 관개 유량 용량을 50% 이상 향상시켰습니다.

유럽의 관개 펌프 시장에서 용적식 펌프 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 8.2%로 확대될 것으로 전망됩니다. 이러한 성장은 주요 원심 분리 방식 카테고리보다 전문성이 더 높은 용도와 관련이 있습니다. 포도원, 베리류 재배지, 과수원 및 온실 시스템에서 정밀한 비료 시비 및 관개를 위해서는 제어된 소량 투여가 필요하며, 이것이 다이어프램 펌프와 프로그레시브 캐비티 펌프의 도입을 촉진하고 있습니다. 또한, 유럽의 관개 펌프 시장에서는 재생수를 이용한 관개에 대한 관심이 높아지고 있으며, 표준 임펠러식 시스템에서는 마모가 빨리 진행되기 쉬운 와류 펌프나 고형물에 대한 내성이 필요한 이용 사례와 같은 틈새 시장을 뒷받침하고 있습니다. 수중 펌프는 스페인과 이탈리아에서 심정 관개가 여전히 중요하기 때문에 안정적인 제2의 카테고리로서의 위상을 유지하고 있습니다. 다만, 교체 수요는 효율이 더 높고 보호 성능이 뛰어난 기종으로 점차 이동하고 있습니다. 이러한 점들을 종합해 보면, 제품 수요는 대량 소비형이 주류를 이루는 원심 펌프와, 정밀 투여, 재생수, 보호 재배를 중심으로 빠르게 성장하고 있는 특수 용도 부문으로 양분되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the europe irrigation pumps market size is projected to be USD 2.30 billion in 2025, USD 2.5 billion in 2026, and reach USD 3.80 billion by 2031, growing at a CAGR of 8.80% from 2026 to 2031.

This report is Segmented by Product Type (Centrifugal Pumps, Submersible Pumps, Positive Displacement Pumps, and Vortex Pumps), by Power Source (Grid-Electric, Diesel, Solar, and Hybrid Solar-Diesel and Solar-Battery), and by Geography (Germany, United Kingdom, France, Spain, Italy, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value in USD.

Europe Irrigation Pumps Market Trends and Insights

Water-Scarcity-Driven Retrofit of Legacy Irrigation Pumps

Water stress is no longer treated as a seasonal operating issue in the Europe irrigation pumps market. It is becoming an administrative trigger for equipment renewal in basins where abstraction is already under pressure. The Joint Research Centre reported in February 2026 that human activity appropriates 10% to 50% of renewable freshwater in most European regions, while southern and Mediterranean areas face the greatest overuse pressure. These conditions favor replacement of older fixed-speed assets that lack metering and cannot easily meet current monitoring needs. In practice, growers are not just buying a new pump. They are replacing an older irrigation setup with a system that can track flow, support control functions, and fit within stricter basin management rules.

Common Agricultural Policy (CAP)-Backed Irrigation Modernization Spending

The Common Agricultural Policy spending cycle remains one of the clearest supports for the Europe irrigation pumps market. Planned investment under the 2021 to 2027 framework reached EUR 31.4 billion (USD 33.9 billion), covering European Union and national co-financing for farm and irrigation projects under Articles 73 and 74. The 2025 proposal also kept water management and soil health visible in the next policy cycle, signaling continuity rather than a one-period support window. France, Spain, Germany, and Italy remain the most active national funding centers because they are the largest recipients of Common Agricultural Policy support and also run sizable irrigation modernization pipelines. A key point is that metering is often required before subsidy approval. That rule pushes older pump fleets onto a regulatory replacement schedule rather than a purely voluntary spending cycle.

High Upfront Pump-System Capital Expenditure for Small and Mid-Size Farms

Capital cost remains the clearest demand restraint in the Europe irrigation pumps market. A full system upgrade that includes the pump, variable frequency drive, metering hardware, and installation can still place a heavy burden on farms that operate with tight seasonal cash flow. Regulation (European Union) 2021/2115 allows support for eligible investment costs, but the remaining co-payment still stretches practical machinery budgets in many small and mid-size farms, especially in central and eastern member states. The timing of reimbursement is part of the problem because support can arrive well after installation decisions must be made. Suppliers have responded with modular pump station formats, but the cost reduction has not yet been enough to bring turnkey upgrades within easy reach for the smallest operators. As a result, adoption is strongest where larger growers, cooperatives, and irrigation bodies can spread capital costs across more hectares or more users.

Other drivers and restraints analyzed in the detailed report include:

- Precision Irrigation and Variable Frequency Drive-Linked Pump Automation

- Solar and Hybrid Pumping Economics Improving

- Groundwater Permitting and Abstraction Caps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal pumps held the largest market share and accounted for 71.2% of the Europe irrigation pumps market share in 2025. Their position reflects broad utility across surface abstraction, open-channel irrigation, and borehole-linked farm systems in both field crops and horticulture. Demand is strongest where operators need a familiar and flexible solution that can serve different heads and flow conditions without narrowing use to one crop system. Large public and consortium irrigation schemes also continue to rely on centrifugal formats, especially vertical turbine and split-case designs. Caprari S.p.A. illustrated this role in 2024 through its Scigliati plant project in Italy, which lifted basin irrigation flow capacity by more than 50% with 5 customized vertical lineshaft units.

The Europe irrigation pumps market size for positive displacement pumps is projected to expand at an 8.2% CAGR from 2026 to 2031. This growth is tied to uses that are more specialized than the main centrifugal category. Precision fertigation in vineyards, berry crops, orchards, and greenhouse systems needs controlled low-volume dosing, and that favors diaphragm and progressive cavity pump formats. The Europe irrigation pumps market is also seeing wider interest in reclaimed-water irrigation, and that supports niche use cases for vortex and solids-tolerant applications where standard impeller systems can wear faster. Submersible pumps remain a stable second-tier category because deep-well irrigation still matters in Spain and Italy, even as replacement demand shifts toward higher-efficiency and better-protected units. Taken together, product demand is separating into a high-volume mainstream centrifugal base and a faster specialty layer built around precision dosing, reclaimed water, and protected cultivation.

Complete Report Scope:

- By Product Type

- Centrifugal Pumps

- End-suction Surface Pumps

- Split-case Pumps

- Vertical Turbine Pumps

- Submersible Pumps

- Borehole Pumps

- Submersible Multistage Pumps

- Positive Displacement Pumps

- Diaphragm Pumps

- Progressive Cavity Pumps

- Vortex Pumps

- Centrifugal Pumps

- By Power Source

- Grid-electric Pumps

- Diesel Pumps

- Solar Pumps

- Hybrid Solar-Diesel and Solar-Battery Pumps

- By Geography

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- Grundfos Holding A/S

- Xylem Inc.

- KSB SE & Co. KGaA

- Franklin Electric Co., Inc.

- Caprari S.p.A.

- Wilo SE

- Calpeda S.p.A.

- Pentair plc

- Ebara Corporation

- Flowserve Corporation

- Sulzer Ltd.

- Pedrollo S.p.A.

- DAB Pumps S.p.A.

- SAER Elettropompe S.p.A.

- ANDRITZ AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Water-scarcity-driven retrofit of legacy irrigation pumps

- 4.2.2 Common Agricultural Policy (CAP)-backed irrigation modernization spending

- 4.2.3 Precision irrigation and variable frequency drive-linked pump automation

- 4.2.4 Solar and hybrid pumping economics improving

- 4.2.5 Reclaimed-water irrigation creates retrofit demand

- 4.2.6 Vineyard, orchard, and greenhouse irrigation intensity

- 4.3 Market Restraints

- 4.3.1 High upfront pump-system capital expenditure for small and mid-size farms

- 4.3.2 Groundwater permitting and abstraction caps

- 4.3.3 Country-by-country grid and hybrid-system compliance complexity

- 4.3.4 Water-savings rebound limits net pumping-volume growth

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Centrifugal Pumps

- 5.1.1.1 End-suction Surface Pumps

- 5.1.1.2 Split-case Pumps

- 5.1.1.3 Vertical Turbine Pumps

- 5.1.2 Submersible Pumps

- 5.1.2.1 Borehole Pumps

- 5.1.2.2 Submersible Multistage Pumps

- 5.1.3 Positive Displacement Pumps

- 5.1.3.1 Diaphragm Pumps

- 5.1.3.2 Progressive Cavity Pumps

- 5.1.4 Vortex Pumps

- 5.1.1 Centrifugal Pumps

- 5.2 By Power Source

- 5.2.1 Grid-electric Pumps

- 5.2.2 Diesel Pumps

- 5.2.3 Solar Pumps

- 5.2.4 Hybrid Solar-Diesel and Solar-Battery Pumps

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 Russia

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Grundfos Holding A/S

- 6.4.2 Xylem Inc.

- 6.4.3 KSB SE & Co. KGaA

- 6.4.4 Franklin Electric Co., Inc.

- 6.4.5 Caprari S.p.A.

- 6.4.6 Wilo SE

- 6.4.7 Calpeda S.p.A.

- 6.4.8 Pentair plc

- 6.4.9 Ebara Corporation

- 6.4.10 Flowserve Corporation

- 6.4.11 Sulzer Ltd.

- 6.4.12 Pedrollo S.p.A.

- 6.4.13 DAB Pumps S.p.A.

- 6.4.14 SAER Elettropompe S.p.A.

- 6.4.15 ANDRITZ AG