|

시장보고서

상품코드

2065720

의료기기 전자데이터교환 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Medical Devices Electronic Data Interchange - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

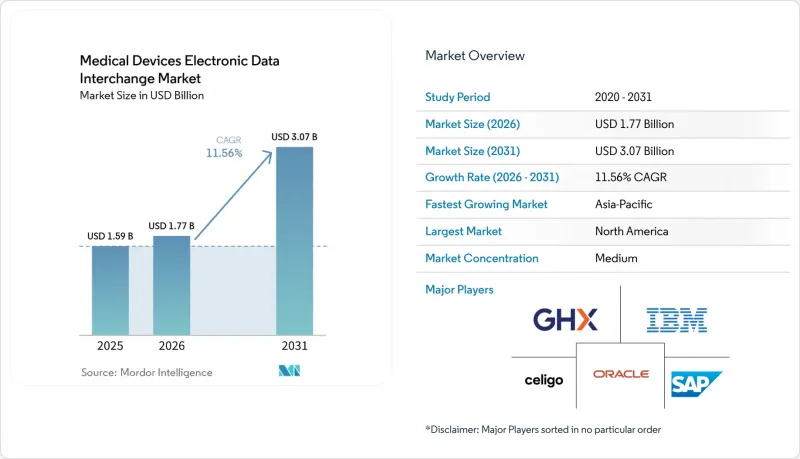

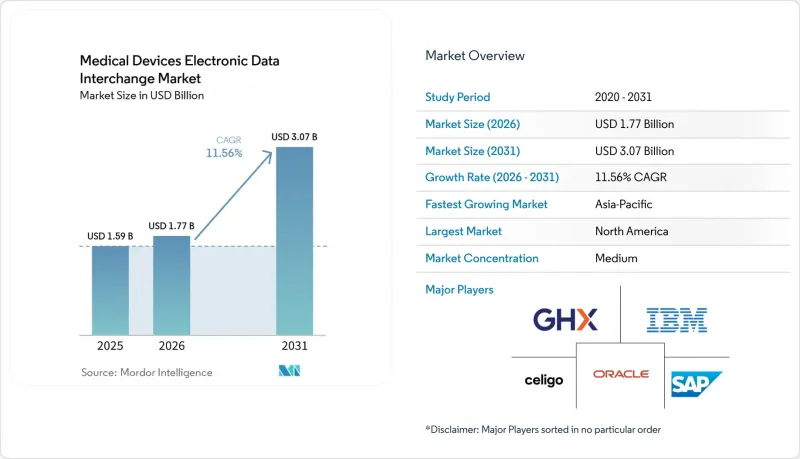

Mordor Intelligence에 의하면, 의료기기 전자데이터교환(EDI) 시장 규모는 2025년 15억 9,000만 달러로 평가되었고, 2026년에는 17억 7,000만 달러로 추정되고, 2031년까지 30억 7,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 11.56%로 성장할 전망입니다.

본 보고서는 구성 요소별(솔루션 및 소프트웨어, 서비스), 도입 형태별(클라우드 기반, 온프레미스형, 하이브리드형, 멀티채널/포털/모바일 EDI), 거래 유형별(조달, 물류, 결제, 제품 데이터 동기화), 최종 사용자별(의료기기 제조업체, 유통업체, GPO, 병원/IDN, ASC), 지역별(북미, 유럽, APAC, MEA, 남미)로 분류되어 있습니다. 시장 예측치는 금액(달러)으로 표시되어 있습니다.

세계의 의료기기 전자데이터교환(EDI) 시장 동향 및 인사이트

UDI 및 GUDID를 통한 의료기기 마스터 데이터의 표준화

UDI 규제로 인해 의료기기 전자데이터교환 시장에서 정확한 데이터에 대한 수요가 증가하고 있습니다. 2026년까지 제조업체들은 EU, 호주, 스위스 전역에서 제출 요건을 준수해야할 것입니다. 각 지역마다 고유한 데이터 속성과 프로토콜이 있어, 수작업에 따른 업무 부담이 증가하고 있습니다. 이 과제로 인해 중견 제조업체들은 아이템 마스터, 카탈로그, 거래처 레코드에 통합하기 전에 UDI-DI 데이터를 보강하는 워크플로우를 도입해야 하는 상황에 놓여 있습니다. 현재 규정 준수 대응 준비 상황은 공급업체 선정에 있어 중요한 요소로 자리 잡고 있으며, 구매 주기의 더 이른 단계에서 고려되고 있습니다.

병원에서의 비접촉식 ‘조달부터 결제’ 거래로의 전환

병원에서는 사무 처리 지연을 줄이고 거래의 정확성을 높이기 위해, 비접촉식 조달부터 지급(Procure-to-Pay) 워크플로우를 우선적으로 도입하고 있습니다. 구매 담당자들은 현재 주문의 정확성, 청구서 대조 및 결제 속도를 기준으로 플랫폼을 평가했습니다. 2026년에는 AI 기반 오케스트레이션 플랫폼과 통합 조달 및 결제 솔루션과 같은 기술의 발전이 새로운 기준을 제시할 것이며, 병원 측은 자동화가 일반적인 발주서에 그치지 않고 재고 보충 및 청구 업무까지 확대될 것으로 기대하고 있습니다.

연결된 거래 네트워크에서의 사이버 보안 및 PHI 유출 위험

사이버 보안 문제는 의료기기의 전자 데이터 교환(EDI) 시장에 막대한 영향을 미치고 있습니다. 새로운 거래 파트너가 늘어날 때마다 위험의 범위가 확대되고 운용 비용도 증가합니다. 2025년과 2026년에 발생한 의료 분야의 정보 유출 사건에서는 수백만 건의 기록이 유출되었으며, 이에 따라 조달 팀은 HIPAA 및 HITECH에 기반한 더욱 강력한 보안 보장을 요구하고 있습니다. PHI는 발주 및 청구서를 포함한 다양한 워크플로우를 통해 유통되기 때문에 추가적인 위험이 발생하고 있습니다. 소규모 시스템 통합사업자들은 엔터프라이즈급 제어 기능에 대한 투자로 인해 재정적 부담을 겪고 있으며, 보안을 중시하는 고객층을 대상으로 한 시장 도입 속도가 둔화되고 있습니다.

부문별 분석

2025년, 이 서비스는 의료기기 전자데이터교환(EDI) 시장 점유율의 53.12%를 차지한 것으로 평가되었고, 2026-2031년 연평균 성장률(CAGR) 11.76%로 성장할 것으로 전망됩니다. 이러한 성장은 매니지드 통합, 거래처 파트너 온보딩, 예외 처리 및 도입 후 규정 준수 지원에 대한 지속적인 수요를 반영하고 있습니다. 프로젝트에는 대개 구매자 측의 시스템이 3-5개 관여하기 때문에 일회성 소프트웨어 도입만으로는 운영상의 요구를 충족시키기 어려우며, 도입 후의 서비스가 필수적입니다. 서비스 수익은 규제 환경 하에서 정확하고 실용적인 거래 흐름을 유지하는 것과 밀접한 관련이 있습니다.

소프트웨어 솔루션은 필수적이지만, 구매자들은 이를 독립적인 도구로 사용하는 것보다는 실제 워크플로우에 통합된 자동화 기능을 선호합니다. 2026년 2월에 출시된 SPS Commerce의 ‘MAX’는 공급업체가 자동화를 강화하여 고객 가치를 유지할 수 있는 방법을 제시합니다. 그러나 예외 처리, 온보딩, 거버넌스 변경을 관리하는 데 있어 서비스 팀은 여전히 필수적입니다. 소프트웨어는 차별화를 촉진하지만, 서비스는 지속적인 수익, 사용자의 신뢰 및 고객 유지를 보장합니다.

2025년, 의료기기 전자데이터교환(EDI) 시장에서 클라우드 기반 도입 비중은 41.87%를 차지했으며, 2026-2031년 연평균 성장률(CAGR) 11.98%로 성장할 것으로 전망됩니다. 이러한 성장은 유연한 트랜잭션 처리 능력에 대한 수요, 유지보수 부담의 경감, 그리고 ERP 현대화와의 연계성에 의해 주도되고 있습니다. 2026년 가트너의 ‘iPaaS 매직 쿼드런트’에 SEEBURGER의 플랫폼이 선정된 것에서도 알 수 있듯이, 구매자들은 EDI, API, 관리형 파일 전송을 통합한 통합 플랫폼을 점점 더 선호하고 있습니다.

온프레미스형 모델은 엄격한 데이터 소재지 요건이나 관리 정책을 갖춘 조직, 특히 레거시 ERP 시스템을 도입한 조직에게 여전히 중요한 선택지로 남아 있습니다. 하이브리드 구성은 온프레미스 시스템을 완전히 대체하지 않고도 클라우드 네트워크에 연결할 수 있기 때문에 주목을 받고 있습니다. 다중 채널 EDI 및 API 지원 모델이 점점 더 중요해지는 한편, 포털 및 모바일 연결은 IT 자원이 제한적인 소규모 공급업체를 지원하고 있습니다.

지역별 분석

2025년, 북미는 의료기기 전자데이터교환(EDI) 시장의 42.25%를 차지했으며, 거래 자동화 및 플랫폼 도입 분야에서 계속해서 주도적인 위치를 유지했습니다. 이 지역은 ANSI X12의 확고한 활용, 성숙한 GPO(그룹 구매 조직) 체계, 그리고 뿌리 깊은 전자 거래 관행의 혜택을 누리고 있으며, 공급업체, 유통업체, 제조업체 간에 견고한 도입 기반을 구축하고 있습니다. 미국에서는 구식 부가가치 네트워크를, 고도의 분석 기능, 예외 처리, 청구서 발행 자동화 기능을 갖춘 클라우드 네이티브 플랫폼으로 업그레이드하고 있으며, 최근 발생한 보안 침해 사고로 인해 보안 심사가 엄격해졌음에도 불구하고 북미의 지속적인 우위를 확보하고 있습니다.

UDI(의료기기 고유 식별자) 의무화 및 디지털 헬스 이니셔티브가 국경을 초월한 구조화된 의료기기 데이터 교환과 규제 관련 기록 공유를 촉진함에 따라, 유럽의 중요성은 점점 더 커지고 있습니다. 각 제조업체들은 규제 대상 데이터베이스에 대한 제출 및 갱신 요건 관리에 어려움을 겪고 있으며, 일관성 있는 국경을 초월한 데이터 파이프라인의 필요성이 강조되고 있습니다. 독일은 EDI 프로세스의 과제 해결을 위한 노력을 주도하고 있는 반면, 프랑스는 공급 중단 통지 요건을 강화하여 공급업체와 의료 제공업체 간의 데이터 교환을 강화하고 있습니다. 스위스에서는 새로운 제출 엔드포인트가 추가되었으며, 영국, 이탈리아, 스페인은 여전히 지역 수요를 뒷받침하는 주요 병원 조달 시장으로 자리 잡고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2026-2031년 연평균 성장률(CAGR) 12.88%를 나타낼 것으로 전망됩니다. 이는 중국, 인도, 일본, 한국 등 각국의 정부 디지털화 프로그램, 보험 적용 범위 확대, 의료기기 제조업의 성장, 그리고 클라우드 우선 인프라 구축에 힘입은 결과입니다. 의료 인프라의 디지털화는 급속히 확대되고 있으며, 이는 지역 및 전 세계 공급망의 발전을 반영하고 있습니다. 중동 및 아프리카는 도입 초기 단계에 있으며, 남미는 여전히 가장 작은 시장이지만, 두 지역 모두 다중 통화 환경과 인프라상의 과제를 능숙하게 관리할 수 있는 공급업체에게 기회를 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the medical devices electronic data interchange market size is expected to increase from USD 1.59 billion in 2025 to USD 1.77 billion in 2026 and reach USD 3.07 billion by 2031, growing at a CAGR of 11.56% over 2026-2031.

This report is Segmented by Component (Solutions/Software, Services), Deployment (Cloud-Based, On-Premises, Hybrid, Multi-channel/Portal/Mobile EDI), Transaction Type (Procurement, Logistics, Settlement, Product Data Sync), End User (Device Manufacturers, Distributors, Gpos, Hospitals/IDNs, Ascs), and Geography (North America, Europe, APAC, MEA, South America). Forecasts in Value (USD).

Global Medical Devices Electronic Data Interchange Market Trends and Insights

UDI and GUDID-Driven Device Master-Data Standardization

UDI regulations are driving the need for accurate data in the medical devices electronic data interchange market. By 2026, manufacturers face submission requirements across the EU, Australia, and Switzerland, each with unique data attributes and protocols, increasing the burden on manual processes. This challenge is pushing mid-sized manufacturers to adopt workflows that enhance UDI-DI data before integration into item masters, catalogs, and trading-partner records. Compliance readiness is now a key factor in vendor selection, moving earlier in the buying cycle.

Hospital Preference for Touchless Procure-to-Pay Transactions

Hospitals are prioritizing touchless procure-to-pay workflows to reduce administrative delays and improve transaction accuracy. Buyers now evaluate platforms based on order accuracy, invoice matching, and payment speed. In 2026, advancements like AI-driven orchestration platforms and integrated procure-to-pay solutions are setting new standards, with hospitals expecting automation to extend beyond standard purchase orders to include replenishments and bill-only activities.

Cybersecurity and PHI Exposure Across Connected Trading Networks

Cybersecurity challenges significantly impact the electronic data interchange market for medical devices. Each new trading partner increases the risk perimeter and operational costs. Healthcare breaches in 2025 and 2026 exposed millions of records, prompting procurement teams to demand stronger HIPAA and HITECH security attestations. PHI flows through various workflows, including orders and invoices, creating additional risks. Smaller integrators face financial strain as they invest in enterprise-grade controls, slowing market adoption in security-sensitive accounts.

Other drivers and restraints analyzed in the detailed report include:

- Consignment Implant and Bill-Only Order Automation

- Cloud-Based EDI Modernization and ERP Integration for Suppliers

- Legacy ERP, WMS, EHR, and Supplier-System Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, services accounted for 53.12% of the medical devices electronic data interchange market share and are projected to grow at an 11.76% CAGR from 2026 to 2031. This growth reflects the ongoing demand for managed integration, trading-partner onboarding, exception resolution, and compliance support post-deployment. With projects often involving 3 to 5 buyer-side systems, one-time software installations rarely meet operational needs, keeping post-implementation services essential. Services revenue remains tied to maintaining accurate and usable transaction flows in a regulated environment.

While software solutions are critical, buyers prefer automation integrated into live workflows rather than as separate tools. SPS Commerce's MAX, launched in February 2026, demonstrates how vendors enhance automation to retain account value. However, service teams remain vital for managing exceptions, onboarding, and governance changes. Software drives differentiation, but services ensure recurring revenue, user trust, and customer retention.

Cloud-based deployment held 41.87% of the medical devices electronic data interchange market in 2025 and is forecast to grow at an 11.98% CAGR from 2026 to 2031. This growth is driven by demand for flexible transaction capacity, reduced maintenance, and alignment with ERP modernization. Buyers increasingly prefer unified platforms that integrate EDI, API, and managed file transfer, as seen with SEEBURGER's platform inclusion in the 2026 Gartner Magic Quadrant for iPaaS.

On-premises models remain relevant for organizations with strict data residency or control policies, particularly those with legacy ERP systems. Hybrid setups are gaining traction as they connect on-premises systems to cloud networks without full replacements. Multi-channel EDI and API-enabled models are becoming more relevant, while portal and mobile connectivity support smaller suppliers with limited IT resources.

Geography Analysis

In 2025, North America accounted for 42.25% of the medical devices electronic data interchange market, maintaining its leadership in transaction automation and platform deployment. The region benefits from established ANSI X12 usage, a mature GPO framework, and entrenched electronic transaction practices, creating a strong adoption base among providers, distributors, and manufacturers. The U.S. is upgrading older value-added networks to cloud-native platforms with enhanced analytics, exception handling, and bill-only automation, ensuring North America's continued dominance despite stricter security reviews following recent breaches.

Europe is becoming increasingly significant as UDI mandates and digital health initiatives drive structured device data exchanges across countries and regulatory records. Manufacturers face challenges in managing submission and update requirements across regulated databases, emphasizing the need for consistent cross-border data pipelines. Germany leads efforts to address EDI process gaps, while France enforces stricter supply interruption notifications, enhancing supplier-provider data exchanges. Switzerland adds another submission endpoint, and the UK, Italy, and Spain remain key hospital procurement markets supporting regional demand.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 12.88% from 2026 to 2031, driven by government digitization programs, expanded insurance coverage, growing device manufacturing, and cloud-first infrastructure in countries like China, India, Japan, and South Korea. Healthcare infrastructure digitization is scaling rapidly, reflecting broader regional and global supply chain advancements. While the Middle East and Africa are in early adoption stages and South America remains the smallest market, both regions offer opportunities for suppliers adept at managing multi-currency conditions and infrastructure challenges.

- Celigo, Inc.

- Cleo Communications US, LLC

- Comarch

- EDICOM CAPITAL, S.L.

- Generix Group SAS

- Global Healthcare Exchange, LLC

- IBM

- MuleSoft, LLC

- OpenText

- Oracle America, Inc.

- Reed Tech

- SAP

- SEEBURGER AG

- SPS Commerce, Inc.

- SupplyOn AG

- Syndigo LLC

- Tecsys Inc.

- The Descartes Systems Group Inc.

- TrueCommerce, Inc.

- Veradigm Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 UDI and GUDID-Driven Device Master-Data Standardization

- 4.2.2 Hospital Preference for Touchless Procure-to-Pay Transactions

- 4.2.3 Consignment Implant and Bill-Only Order Automation

- 4.2.4 Cloud-Based EDI Modernization and ERP Integration for Medtech Suppliers

- 4.2.5 UDI-DI Enrichment of Contract and Price Files

- 4.2.6 AI-Assisted Exception Handling and Transaction-Quality Controls

- 4.3 Market Restraints

- 4.3.1 Cybersecurity and PHI Exposure Across Connected Transaction Networks

- 4.3.2 Legacy ERP, WMS, EHR, and Supplier-System Integration Cost

- 4.3.3 UDI and Unit-of-Measure Master-Data Mismatches

- 4.3.4 Minimum-Data-Set Alignment Challenges for Implant Orders

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Solutions / Software

- 5.1.2 Services

- 5.2 By Deployment and Connectivity Model

- 5.2.1 Cloud-based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.2.4 Multi-channel / API-enabled EDI

- 5.2.5 Portal / Mobile EDI

- 5.3 By Transaction Type

- 5.3.1 Procurement and Ordering

- 5.3.2 Logistics and Fulfillment

- 5.3.3 Commercial Settlement

- 5.3.4 Product and Contract Data Synchronization

- 5.4 By End User

- 5.4.1 Medical Device Manufacturers

- 5.4.2 Medical Device Distributors and Wholesalers

- 5.4.3 Group Purchasing Organizations and Exchanges

- 5.4.4 Hospitals and Integrated Delivery Networks

- 5.4.5 Ambulatory Surgical Centers and Specialty Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Celigo, Inc.

- 6.3.2 Cleo Communications US, LLC

- 6.3.3 Comarch SA

- 6.3.4 EDICOM CAPITAL, S.L.

- 6.3.5 Generix Group SAS

- 6.3.6 Global Healthcare Exchange, LLC

- 6.3.7 International Business Machines Corporation

- 6.3.8 MuleSoft, LLC

- 6.3.9 Open Text Corporation

- 6.3.10 Oracle America, Inc.

- 6.3.11 Reed Tech

- 6.3.12 SAP SE

- 6.3.13 SEEBURGER AG

- 6.3.14 SPS Commerce, Inc.

- 6.3.15 SupplyOn AG

- 6.3.16 Syndigo LLC

- 6.3.17 Tecsys Inc.

- 6.3.18 The Descartes Systems Group Inc.

- 6.3.19 TrueCommerce, Inc.

- 6.3.20 Veradigm Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment