|

시장보고서

상품코드

2065756

SaaS(Software As A Service) 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Software As A Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

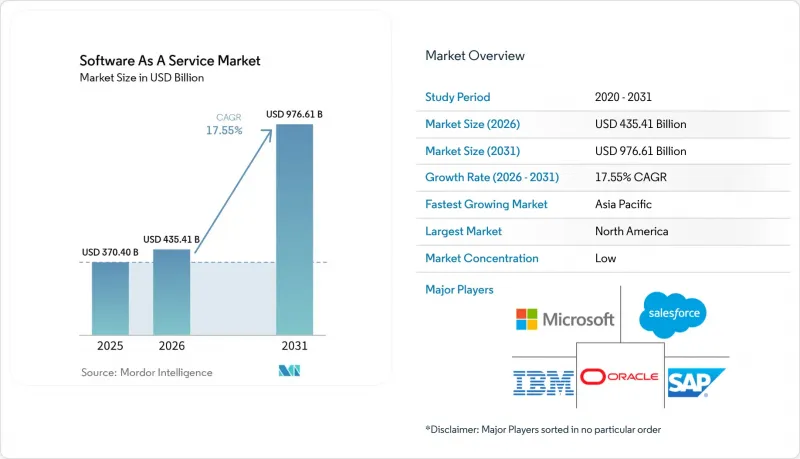

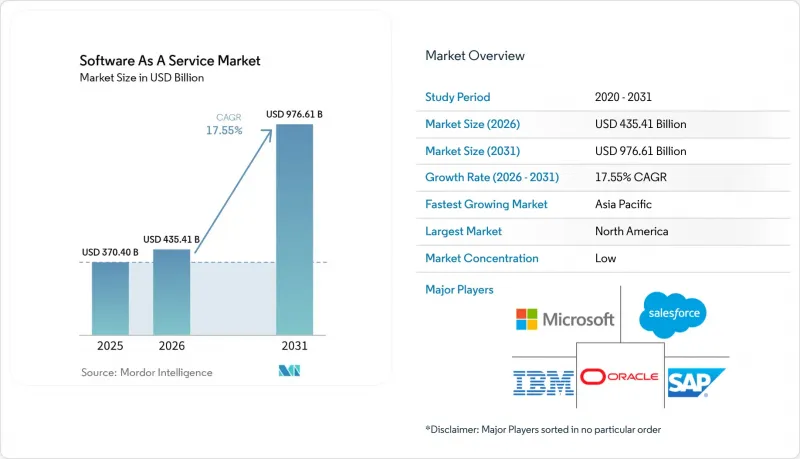

Mordor Intelligence에 의하면, 2026년 SaaS(Software As A Service) 시장 규모는 4,354억 1,000만 달러로 추정되고 있어 2025년 3,704억 달러에서 확대될 전망입니다.

또한, 2031년의 예측치는 9,766억 1,000만 달러이며, 2026년부터 2031년까지 연평균 성장률(CAGR) 17.55%로 성장할 것으로 전망됩니다.

본 보고서는 배포 방식(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 기업 규모(중소기업, 대기업), 최종 사용 산업(IT 및 통신, 금융 및 보험·증권, 소매, 의료, 제조, 기타 최종 사용자 업종), 지역(북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카)별로 분류되어 있습니다. 상기 모든 부문에 대해 시장 규모 및 전망은 금액(달러) 단위로 제시되어 있습니다.

세계 SaaS 시장 동향과 인사이트

클라우드 네이티브 아키텍처의 보급

클라우드 네이티브 접근 방식에서는 모놀리식 소프트웨어가 쿠버네티스를 통해 오케스트레이션되는 컨테이너화된 마이크로서비스로 대체되어, 지속적인 배포와 탄력적인 확장이 가능해집니다. 마이크로소프트의 2025 회계연도 3분기 클라우드 매출은 424억 달러(전년 동기 대비 20% 증가)에 달했으며, 이는 기업들이 ‘클라우드 우선’ 전략에 따른 재구성을 강력히 요구하고 있음을 뒷받침합니다. 하드웨어의 제약에서 벗어난 기업들은 단 몇 분 만에 새로운 환경을 구축함으로써 개발자의 생산성과 서비스의 복원력을 높이고 있습니다. 이러한 아키텍처의 전환은 하이퍼스케일러의 생태계에 원활하게 통합될 수 있는 틈새 시장 공급업체들의 진입 장벽을 낮춤으로써, SaaS 시장의 세분화도 초래하고 있습니다. 멀티클라우드 도구가 성숙해짐에 따라, 조직들은 집중 위험을 피하면서도 각 분야에서 최고의 혁신을 유지하기 위해 공급업체를 다양화하고 있습니다.

중소기업의 급속한 디지털화

팬데믹 이후, 중소기업들은 경쟁력을 유지하기 위해 프론트오피스와 백오피스 기능의 디지털화를 급속도로 추진하고 있습니다. OECD 조사에 따르면, 기업 규모나 업종에 따라 도입 격차가 확대되고 있는 반면, 지식집약형 중소기업이 도입을 주도하고 있습니다. 중국에서는 2023년 SaaS 지출이 581억 위안으로, 거시경제의 침체에도 불구하고 23.1% 증가했습니다. 합리적인 가격의 SaaS 구독 서비스는 중소기업이 자금적 제약을 피하는 데 도움이 되고 있으며, AI를 활용한 자체 설정 기능 덕분에 도입에 드는 노력도 줄어들고 있습니다. 자원 제약이 있는 경영자들이 편의성과 ROI를 우선시하는 가운데, 회계, 전자상거래, 마케팅을 통합 대시보드로 묶어 제공하는 벤더가 지지를 얻고 있습니다.

데이터 주권과 규정 준수의 장벽

GDPR(EU 개인정보보호규정) 및 각 성·자치구·직할시 차원에서 잇달아 제정되고 있는 개인정보 보호 관련 법규로 인해, 서비스 제공업체들은 데이터 현지화, 데이터 보호 책임자 임명, 그리고 엄격한 감사 통과를 피할 수 없게 되었습니다. 규정 준수 조치는 비용을 증가시켜 하이퍼스케일러의 설치 장소 선택의 폭을 좁히고 있습니다. 기업들은 기밀성이 높은 워크로드를 On-Premise나 프라이빗 클라우드에 보관하고, 지역별 호스팅 체계를 갖춘 공급업체를 선택함으로써 리스크를 분산하고 있습니다.

부문별 분석

퍼블릭 클라우드는 2025년에 89.42%의 점유율을 차지하며, 여전히 SaaS 시장을 주도하고 있습니다. 그러나 기업들이 규제 준수 및 지연 시간에 민감한 이용 사례를 추구함에 따라, 하이브리드 구성은 연평균 성장률(CAGR) 21.8%로 성장할 것으로 전망됩니다. 디스커버 파이낸셜 서비스는 AWS상의 Red Hat OpenShift를 활용하여 계절적 수요 급증에 대응하고, 워크로드를 자유롭게 이동시킴으로써 벤더 종속의 위험을 줄이고 있습니다. 엣지 노드가 제조업 및 금융 업계에서 실시간 분석을 가능하게 함에 따라, 하이브리드 솔루션의 SaaS 시장 규모는 확대될 전망입니다.

기업들은 비용과 관리의 균형을 맞추기 위해 퍼블릭, 프라이빗, 엣지 리소스를 조합하고 있습니다. IndiGo Airline은 18개월 이내에 업무의 80%를 Microsoft Azure와 Google Cloud에 걸친 멀티 클라우드 환경으로 이전했습니다. SaaS 시장은 이러한 다양성의 혜택을 누리고 있으며, 각 벤더들은 모든 환경에서 일관되게 작동하는 컨테이너 지원 버전의 제공을 촉진하고 있습니다.

2025년에는 전 세계 업무 프로세스를 간소화하는 통합 솔루션에 매력을 느낀 대기업들이 SaaS 시장의 58.05%를 차지했습니다. 그러나 연평균 성장률(CAGR) 19.2%를 나타낼 것으로 예측되는 중소기업이 다음 성장의 물결을 주도하고 있습니다. 이 부문에서는 구독형 과금, 안내형 온보딩, AI를 활용한 설정 기능 등을 통해 기술적 장벽이 해소됨에 따라 SaaS 시장 규모가 해마다 확대되고 있습니다.

중소기업은 회계, 영업, 인사 기능을 단일 인터페이스를 통해 제공하는 플랫폼을 선호합니다. OECD는 디지털 기술의 보급에 여전히 편차가 있음을 지적하고 있으며, 이에 따라 소규모 기업을 대상으로 한 정책적 지원이 추진되고 있습니다. 템플릿, 파트너 생태계, 커뮤니티 학습에 투자하는 벤더는 총 소유 비용(TCO)을 절감하고, 장기적인 고객 충성도를 확보하고 있습니다.

지역별 분석

북미는 2025년에 SaaS 시장의 42.60%를 차지해, 고밀도 클라우드 인프라, 견고한 사이버 보안 기준, 그리고 자본 접근성이라는 이점을 누리고 있습니다. 코카콜라사가 마이크로소프트와의 제휴를 11억 달러 규모로 확대한 사례는 멀티클라우드 SaaS 전략이 기업 차원에서 채택되고 있음을 보여줍니다. 미국 각 주마다 규정이 제각각인 탓에 규정 준수 부담이 커지고 있지만, 각 벤더사는 사용자 정의가 가능한 개인정보 보호 모듈과 지역별로 복제된 데이터 저장소를 제공함으로써 이에 대응하고 있습니다.

아시아태평양은 2031년까지 연평균 18.7%의 성장률을 보일 것으로 예측되며, SaaS 시장 확대의 중심지가 될 전망입니다. 인터넷 보급률의 상승, 모바일 우선 소비 동향, 그리고 정부의 디지털화 프로그램이 도입을 뒷받침하고 있습니다. 중국에서는 2023년에 581억 위안 규모의 SaaS 매출을 기록하며 23.1%의 성장률을 보였으며, 이는 제조업 및 소비자 서비스 분야에서 아직 개척되지 않은 수요가 있음을 여실히 보여주고 있습니다. 현지의 각 하이퍼스케일러 기업들은 언어에 최적화된 UI와 지역별 규정 준수 기능을 제공함으로써 전 세계의 기존 기업들과 경쟁하고 있습니다.

유럽에서는 꾸준하면서도 규정 준수를 중시하는 성장세가 나타나고 있습니다. GDPR(EU 개인정보보호규정) 및 각국의 데이터 보호법에 따라, 공급업체는 지역별 데이터센터를 운영하고 암호화 기술 혁신에 투자해야 합니다. 또한, 지속가능성 목표 역시 조달에 영향을 미치고 있으며, 기업들은 공급업체의 탄소 발자국을 평가하고 그린 클라우드에 관한 정보 공개를 요구하고 있습니다. 재생에너지를 활용하는 시설에 대한 인증을 취득하고, 투명성이 높은 보고를 수행하는 공급업체는 경쟁 우위를 확보할 수 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the software as a service (SaaS) market size in 2026 is estimated at USD 435.41 billion, growing from the 2025 value of USD 370.4 billion, with 2031 projections showing USD 976.61 billion, growing at 17.55% CAGR over 2026-2031.

This report is Segmented by Deployment (Public Cloud, Private Cloud, Hybrid Cloud), Enterprises (SMEs, Large Enterprises), End-User Verticals (IT and Telecom, BFSI, Retail, Healthcare, Manufacturing, Other End-User Verticals), Geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

Global Software As A Service Market Trends and Insights

Proliferation of Cloud-Native Architectures

Cloud-native approaches replace monolithic software with containerized microservices orchestrated by Kubernetes, enabling continuous delivery and elastic scaling. Microsoft's USD 42.4 billion Q3 FY2025 cloud revenue, up 20% year over year, underlines enterprise appetite for cloud-first rebuilding. Freed from hardware constraints, companies spin up new environments in minutes, boosting developer velocity and service resilience. This architectural shift also fragments the SaaS market by lowering entry barriers for niche vendors that plug seamlessly into hyperscaler ecosystems. As multi-cloud tools mature, organizations diversify providers to avoid concentration risk while preserving best-of-breed innovation.

Rapid SME Digitalization

Post-pandemic, SMEs race to digitize front- and back-office functions to remain competitive. OECD research points to widening adoption gaps by size and sector, yet knowledge-intensive SMEs lead uptake. In China, SaaS spending hit CNY 58.1 billion in 2023, rising 23.1% despite macro softness. Budget-friendly SaaS subscriptions help SMEs bypass capital constraints, while AI-infused self-configuration trims onboarding effort. Vendors that bundle accounting, e-commerce, and marketing into unified dashboards gain traction as resource-strapped owners prioritize simplicity and ROI.

Data-Sovereignty and Compliance Barriers

GDPR and a wave of state-level privacy laws compel providers to localize data, appoint Data Protection Officers, and pass rigorous audits. Compliance lifts costs and narrows hyperscaler location choices. Enterprises hedge by retaining sensitive workloads on-prem or in private clouds and selecting vendors with regional hosting frameworks.

Other drivers and restraints analyzed in the detailed report include:

- Lower Upfront Costs vs. On-Premises Licensing

- Vendor Lock-in and Switching Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public cloud continues to dominate the SaaS market with 89.42% share in 2025. Hybrid configurations, though, are projected to grow at 21.8% CAGR as firms pursue regulatory compliance and latency-sensitive use cases. Discover Financial Services uses Red Hat OpenShift on AWS to manage seasonal demand spikes and move workloads freely, mitigating vendor lock-in risk. The SaaS market size for hybrid solutions is set to widen as edge nodes enable real-time analytics in manufacturing and finance.

Enterprises blend public, private, and edge resources to balance cost against control. IndiGo Airline migrated 80% of operations to a multicloud estate spanning Microsoft Azure and Google Cloud within 18 months. The SaaS market benefits from this diversity, encouraging vendors to ship container-ready versions that run consistently across environments.

Large companies accounted for 58.05% of the SaaS market in 2025, attracted by unified suites that simplify global processes. Yet SMEs, forecast to expand at 19.2% CAGR, power the next growth wave. For this cohort the SaaS market size expands each year as subscription billing, guided onboarding, and AI-driven configuration remove technical barriers.

SMEs gravitate toward platforms offering accounting, sales, and HR in a single interface. OECD notes digital uptake remains uneven, prompting policy support for smaller firms. Vendors that invest in templates, partner ecosystems, and community learning lower the total cost of ownership and secure long-term loyalty.

Geography Analysis

North America held 42.60% of the SaaS market in 2025, benefitting from dense cloud infrastructure, robust cybersecurity standards, and capital access. Coca-Cola's USD 1.1 billion expansion of its Microsoft partnership illustrates enterprise-scale adoption of multi-cloud SaaS strategies. Regulatory fragmentation among US states does raise compliance overhead, but vendors respond with configurable privacy modules and regionally replicated data stores.

Asia-Pacific is projected to grow 18.7% annually to 2031, becoming the epicenter of SaaS market expansion. Rising internet penetration, mobile-first consumption, and government digitization programs drive adoption. China recorded CNY 58.1 billion SaaS sales in 2023 with 23.1% growth, underscoring untapped demand across manufacturing and consumer services. Local hyperscalers battle global incumbents by offering language-localized UI and region-specific compliance features.

Europe posts steady yet compliance-centric growth. GDPR and country-level data-protection acts compel vendors to maintain regional datacenters and invest in encryption innovations. Sustainability goals also influence procurement, with enterprises evaluating provider carbon footprints and requiring green-cloud disclosures. Vendors that certify renewable-powered facilities and transparent reporting gain competitive advantage.

- Microsoft

- Salesforce

- Oracle

- SAP

- IBM

- ServiceNow

- Atlassian

- Intuit

- Adobe

- Google (Alphabet)

- Workday

- Zoom Video Communications

- Dropbox

- HubSpot

- Shopify

- Zendesk

- Snowflake

- Alteryx

- ServiceTitan

- BambooHR

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of cloud-native architectures

- 4.2.2 Rapid SME digitalization post-COVID

- 4.2.3 Lower upfront costs vs. on-prem licensing

- 4.2.4 Generative-AI-enabled revenue extensions

- 4.2.5 Edge-delivered ultra-low-latency SaaS

- 4.2.6 Carbon-accounting compliance demand

- 4.3 Market Restraints

- 4.3.1 Data-sovereignty and compliance barriers

- 4.3.2 Vendor lock-in and switching costs

- 4.3.3 FinOps scrutiny curbing SaaS sprawl

- 4.3.4 Green-cloud mandates raising costs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis

- 4.8 Assessment of Macroeconomic Impact

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium-sized Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By Application Type

- 5.3.1 Customer Relationship Management (CRM)

- 5.3.2 Enterprise Resource Planning (ERP)

- 5.3.3 Human Capital Management (HCM/HRM)

- 5.3.4 Collaboration and Productivity

- 5.3.5 Business Intelligence and Analytics

- 5.3.6 Security and Compliance

- 5.3.7 Other Applications

- 5.4 By Pricing Model

- 5.4.1 Subscription-Based

- 5.4.2 Usage-Based / Pay-As-You-Go

- 5.4.3 Freemium and Tiered

- 5.5 By End-User Vertical

- 5.5.1 IT and Telecom

- 5.5.2 Banking, Financial Services and Insurance (BFSI)

- 5.5.3 Retail and E-Commerce

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Manufacturing

- 5.5.6 Other Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Colombia

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Israel

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Nigeria

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft

- 6.4.2 Salesforce

- 6.4.3 Oracle

- 6.4.4 SAP

- 6.4.5 IBM

- 6.4.6 ServiceNow

- 6.4.7 Atlassian

- 6.4.8 Intuit

- 6.4.9 Adobe

- 6.4.10 Google (Alphabet)

- 6.4.11 Workday

- 6.4.12 Zoom Video Communications

- 6.4.13 Dropbox

- 6.4.14 HubSpot

- 6.4.15 Shopify

- 6.4.16 Zendesk

- 6.4.17 Snowflake

- 6.4.18 Alteryx

- 6.4.19 ServiceTitan

- 6.4.20 BambooHR

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment