|

시장보고서

상품코드

2065788

미국의 의료용 디스플레이 모니터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2025-2031년)United States Medical Display Monitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

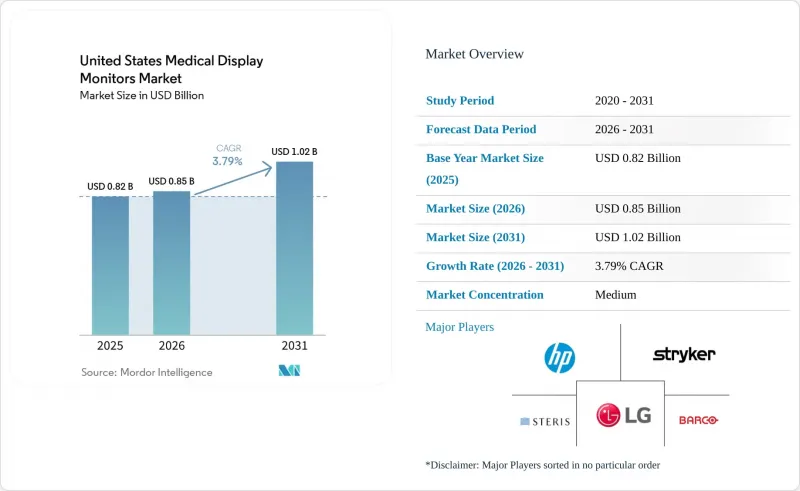

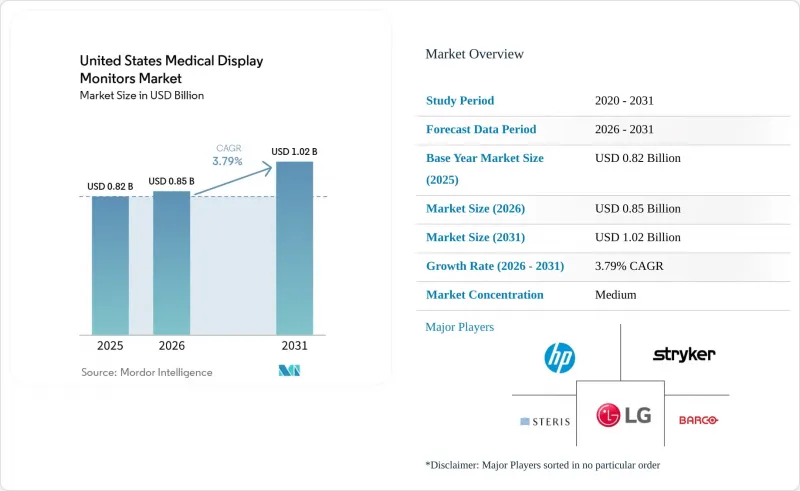

Mordor Intelligence에 의하면, 미국 의료용 디스플레이 모니터 시장 규모는 2025년에 8억 2,000만 달러, 2026년에 8억 5,000만 달러, 2031년까지 10억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 3.79%로 성장할 전망입니다.

본 보고서는 유형(그레이스케일, 컬러), 해상도(2 MP 이하, 2.1-4 MP, 4.1-8 MP, 8 MP 이상), 기술(LED 백라이트 장착 LCD, OLED, CCFL 백라이트 장착 LCD), 용도(일반 방사선 진단, 유방촬영술, 외과 수술 등), 최종 사용자(병원 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 본 보고서에서는 상기 각 부문 시장 규모(달러)를 제시하고 있습니다.

미국 의료용 디스플레이 모니터 시장 동향 및 분석

영상진단센터의 확장 및 판독실 현대화

외래 영상 진단은 미국 의료용 디스플레이 모니터 시장에서 단기적인 수요를 뒷받침하는 가장 뚜렷한 요인 중 하나로 계속해서 자리 잡고 있습니다. Lumexa Imaging사는 190곳 이상의 외래 센터를 운영하며, 2025년에는 400만 건의 검사를 실시했습니다. 또한, 2026년에는 Advocate Health 및 UPMC와의 합작 투자를 통해 4곳의 신규 센터를 개설할 예정이며, 연간 8-10곳의 신규 센터 개설을 목표로 하고 있습니다. 새로운 센터, 개보수된 시설, 또는 확장된 영상의학 판독실 각각은 1차 진단 스테이션, 2차 확인용 스크린, 백업 작업 구역 등에서 여러 대의 디스플레이를 구매할 기회를 창출합니다. 이러한 수요 효과는 신축 시설에만 국한되지 않습니다. 현대화 프로젝트로 인해, 시설 측은 기존 모든 회의실에 대한 보정 상태, 밝기의 일관성, 그리고 모니터의 사용 연한을 재평가할 수밖에 없게 되기 때문입니다. 미국의 의료용 디스플레이 모니터 시장에서 인증 기준에 부합하는 조달 활동은 중요합니다. 왜냐하면, 높은 진단 기준을 유지하고자 하는 기관은 모든 업무 흐름에서 일반적인 시판용 선별 검사에만 의존할 수는 없기 때문입니다. 이러한 추세는 수년에 걸쳐 인증된 품질 보증(QA) 생태계를 유지할 수 있는 공급업체에게 정기적인 교체, 재보정 및 서비스 수익을 뒷받침하는 요인이 됩니다.

4K 저침습 및 하이브리드 수술실의 업그레이드 주기

미국 의료용 디스플레이 모니터 시장의 수술 분야에서는 4K 및 Mini-LED로의 교체 주기가 점차 명확해지고 있습니다. 소니는 2025년 1월, VESA DisplayHDR 1000 인증을 획득한 최초의 의료용 모니터 ‘LMD-32M1MD’를 출시했으며, 이후 2025년 7월에는 더 폭넓은 수술 용도에 대응하기 위해 27인치 및 43인치 모델을 추가하여 제품 라인업을 확충했습니다. 또한, LG도 2025년 9월 4K 수술용 모니터 ‘32HS710S’에 대해 FDA의 510(k) 승인을 획득했습니다. 한편, EIZO는 최대 밝기 1,900 cd/m², 명암비 1,000,000:1을 갖춘 Mini-LED 모델 ‘CuratOR EX3245H’를 2026년 11월부터 출하하기 시작한다고 발표했습니다. 이러한 신제품 출시가 중요하게 여겨지는 이유는 2015년부터 2020년까지 도입된 4K 이전의 HD 디스플레이가 수술실이나 외래 진료 시설에서 권장 사용 기간을 거의 다 채우고 있기 때문입니다. 많은 구형 시스템은 비용 효율성을 중시하여 구입된 것으로, 형광 유도나 로봇 지원, 혹은 장시간에 걸친 수술 중 지속적인 하이 다이내믹 레인지 성능을 목적으로 한 것이 아니었습니다. 이러한 격차로 인해 미국 의료용 디스플레이 모니터 시장에서는 교체 수요가 증가하고 있으며, 병원 및 외래수술센터(ASC)가 수술실 시각화 시스템을 표준화해 나감에 따라 이러한 추세는 앞으로도 활발하게 이어질 것으로 전망됩니다.

고급 진단용 및 수술용 디스플레이의 높은 도입 비용

고사양 의료용 디스플레이 모니터는 여전히 가격이 비싸기 때문에 미국 의료용 디스플레이 모니터 시장의 일부에서는 도입 속도가 둔화되고 있습니다. EIZO는 2026년 4월, 명암비 2,200:1, 최대 휘도 2,500 cd/m²를 구현하는 ‘Instant Backlight Booster’를 탑재한 5 MP 흑백 유방촬영용 모니터 ‘RadiForce GX570’을 출시했습니다. 한편, Barco는 풀 해상도로 이미지를 확인할 수 있는 32 MP 유방 영상 진단용 디스플레이 ‘Coronis OneLook’을 선보였습니다. 인증된 의료용 디스플레이와 고성능 상용 모니터 간의 가격 차이는 대당 5,000-2만 달러에 달하기도 하여, 한 번에 여러 대의 워크스테이션이 필요한 소규모 시설의 경우 큰 부담이 됩니다. 많은 임상적으로 중요한 워크플로우에서 휘도 검증 및 DICOM 보정은 필수적이기 때문에 인증 기준은 여전히 수요의 하한선을 형성하고 있습니다. 그렇긴 하지만, 예산 압박은 지방 병원, 독립 영상진단 업체, 그리고 자본위원회가 모든 장비 교체를 엄격히 심사하는 검사 건수가 적은 전문 의료기관에서 가장 크게 가중되고 있습니다. 이 때문에 조달 과정이 체계적으로 관리되면서, 미국 의료용 디스플레이 모니터 시장이 최고 해상도와 최고 밝기를 갖춘 프리미엄 부문으로 완전히 전환되는 속도가 둔화되고 있습니다.

부문별 분석

2025년, 그레이스케일 디스플레이는 미국 의료용 디스플레이 모니터 시장 점유율의 61.78%를 차지하고 있으며, 이는 흑백 표시가 여전히 일상적인 방사선 진단 및 유방촬영술 판독 업무의 기반이 되고 있음을 뒷받침합니다. 한편, 병리학 및 외과 분야의 업무 흐름에서 조직 색조의 재현 정확도와 시각적 맥락의 폭이 더욱 중요해짐에 따라, 컬러 디스플레이 시장은 2031년까지 연평균 성장률(CAGR) 4.91%라는 더 빠른 성장세를 기록할 것으로 전망됩니다. 미국의 의료용 디스플레이 모니터 시장에서는 여전히 방대한 양의 진단 업무에서 그레이스케일에 의존하고 있습니다. 이는 DICOM GSDF 보정이 완료된 흑백 표시가 많은 방사선 진단 업무에서 여전히 임상 기준으로 자리 잡고 있기 때문입니다. 이러한 기존 인프라 덕분에, 새로운 이용 사례가 컬러로 전환되고 있는 상황에서도 그레이스케일은 교체 수요 측면에서 지속적인 우위를 유지하고 있습니다.

컬러에 대한 수요는 단순히 외관상의 선호도보다는 워크플로우상의 명확한 이유로 인해 확대되고 있습니다. FDA 승인을 받은 병리 시스템에서는 진단 설정의 일환으로 승인된 컬러 디스플레이를 참조하는 사례가 늘어나고 있으며, 이는 모니터 선정이 일반적인 IT 조달이 아닌 규제 대상 도입 계획의 일부로 이루어지게 되었음을 의미합니다. 또한, 외과 수술에서의 시각화 역시 본질적으로 색상에 의존하고 있습니다. 형광 유도, 관류 영상, 로봇 수술 등은 장시간에 걸친 수술 중에도 안정적인 렌더링이 요구되기 때문입니다. 한편, 미국의 의료용 디스플레이 모니터 업계는 여전히 그레이스케일 제품의 성능 향상에 투자를 이어가고 있으며, 그 한 예로 EIZO가 2026년 4월에 유방촬영용 ‘RadiForce GX570’을 출시한 것을 들 수 있습니다. 따라서 시장 구조는 두 개의 지속적인 수요층으로 분화되고 있습니다. 하나는 방사선 진단의 연속성을 중시하는 계층이고, 다른 하나는 색상이 극히 중요한 워크플로우의 확대를 중시하는 계층입니다. 이러한 균형으로 인해, 예측 기간 동안 그레이스케일 시장 규모는 유지되는 한편, 컬러 시장 점유율은 확대될 것으로 보입니다.

2025년, 2.1 MP-4 MP 대역은 미국 의료용 디스플레이 모니터 시장 규모의 32.16%를 차지했습니다. 이는 일반적인 영상 진단 및 영상 검토 환경 전반에서 널리 사용되고 있는 3 MP급 워크스테이션의 도입 대수가 매우 많다는 점을 반영하고 있습니다. 이 대역은 다양한 진단 업무를 아우르면서도, 예산이 제한된 시설에서도 부담 없이 구입할 수 있는 가격대이기 때문에 여전히 시장의 실질적인 중심을 차지하고 있습니다. 미국의 의료용 디스플레이 모니터 시장에서는 임상적 유용성과 조달 비용 사이에서 실용적인 균형을 제공함에 따라, 이 제품군이 광범위한 도입 과정에서 계속해서 지지를 받고 있습니다. 따라서 지역 병원과 많은 외래 진료 시설은 여전히 이 중가 대열에 속해 있습니다.

4.1 MP-8 MP 대역은 유방촬영술 및 전체 슬라이드 이미징을 통해 지속적인 고해상도 렌더링에 대한 수요가 증가하고 있는 만큼, 2031년까지 연평균 성장률(CAGR) 4.73%로 성장할 것으로 전망됩니다. 2024년 4월 USPSTF(미국 예방 서비스 태스크포스)의 유방암 검진 권고안에 따라 정기 검진 시작 연령이 40세로 낮아졌습니다. 이로 인해 장기적인 검진 대상자가 확대되면서, 인증을 받은 유방암 영상진단 시설의 장비 수요가 지속적으로 증가하고 있습니다. 하이엔드 제품 중에서는 Barco사의 ‘Coronis OneLook’이 유방암 영상 진단 판독에 32 MP의 성능을 제공하며, 대규모 프로그램에서 프리미엄 해상도가 처리량 향상에 어떻게 활용되고 있는지를 보여주고 있습니다. 따라서 미국의 의료용 디스플레이 모니터 업계에서는 완전한 전환이라기보다는 구조적 변화가 나타나고 있습니다. 이는 중해상도 제품이 여전히 주류를 이루고 있는 반면, 특정 임상 현장에서는 고해상도에 대한 수요가 확대되고 있기 때문입니다. 8 MP를 초과하는 부문은 여전히 틈새 시장에 머물러 있지만, 팬닝을 줄이고 전체 시야를 확인하는 것이 중요한 유방암 영상 진단, 고도의 외과 수술 용도, 그리고 전문적인 학술 환경에서 그 중요성은 점점 더 커지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the united states medical display monitors market size is projected to be USD 0.82 billion in 2025, USD 0.85 billion in 2026, and reach USD 1.02 billion by 2031, growing at a CAGR of 3.79% from 2026 to 2031.

This report is Segmented by Type (Greyscale, Color), Resolution (Up To 2 MP, 2. 1-4 MP, 4. 1-8 MP, Above 8 MP), Technology (LED-Backlit LCD, OLED, CCFL-Backlit LCD), Application (General Radiology, Mammography, Surgery, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Report Offers the Value (in USD) for the Above Segments.

United States Medical Display Monitors Market Trends and Insights

Imaging-Center Expansion and Reading-Room Modernization

Outpatient imaging remains one of the clearest near-term demand supports for the United States medical display monitors market. Lumexa Imaging operated more than 190 outpatient centers, completed 4 million procedures in 2025, and added 4 new centers in 2026 through joint ventures with Advocate Health and UPMC while targeting 8 to 10 de novo openings annually. Every new center, renovated site, or expanded reading room creates multiple display purchase points across primary diagnostic stations, secondary review screens, and backup work areas. The demand effect is not limited to new buildings because modernization projects also force facilities to reevaluate calibration status, luminance consistency, and monitor age across existing rooms. In the United States medical display monitors market, accreditation-linked procurement behavior matters because facilities that want to maintain high diagnostic standards cannot rely on general commercial screens for every workflow. That pattern supports recurring replacement, recalibration, and service revenue for vendors that can sustain certified QA ecosystems over several years.

4K Minimally Invasive and Hybrid OR Upgrade Cycle

The surgical side of the United States medical display monitors market is entering a more defined 4K and Mini-LED replacement cycle. Sony launched the LMD-32M1MD in January 2025 as the first medical monitor certified to VESA DisplayHDR 1000, and later expanded the lineup in July 2025 with additional 27-inch and 43-inch models for broader procedural use. LG also received FDA 510(k) clearance in September 2025 for the 32HS710S 4K surgical monitor, while EIZO stated that its CuratOR EX3245H Mini-LED model would begin shipping in November 2026 with 1,900 cd/m2 peak brightness and a 1,000,000:1 contrast ratio. These launches matter because a large installed base of pre-4K HD displays from 2015 to 2020 is aging out of its preferred service window in operating rooms and ambulatory settings. Many older systems were purchased for cost efficiency, not for fluorescence guidance, robotic assistance, or sustained high dynamic range performance during long procedures. That gap is creating a replacement wave in the United States medical display monitors market that should stay active as hospitals and ASCs standardize their OR visualization stacks.

High Acquisition Cost for Premium Diagnostic and Surgical Displays

High-end medical displays remain expensive enough to slow unit adoption in parts of the United States medical display monitors market. EIZO launched the RadiForce GX570 in April 2026 as a 5 MP monochrome mammography monitor with a 2,200:1 contrast ratio and an Instant Backlight Booster that reaches 2,500 cd/m2, while Barco positioned Coronis OneLook as a 32 MP breast imaging display for full-resolution review. The gap between a certified medical display and a high-performance commercial monitor can reach USD 5,000 to USD 20,000 per unit, which is significant for smaller facilities that need several stations at once. Accreditation standards still create a floor under demand, because luminance verification and DICOM calibration are not optional in many clinically sensitive workflows. Even so, budget pressure is strongest in rural hospitals, independent imaging operators, and lower-volume specialty settings where capital committees review every replacement closely. This keeps procurement disciplined and slows the speed at which the United States medical display monitors market can fully migrate to the highest resolution and brightest premium tiers.

Other drivers and restraints analyzed in the detailed report include:

- FDA-Cleared Digital Pathology Primary Diagnosis Adoption

- AI-Enabled Multi-Modality Workflow Complexity Favors Premium Diagnostic Displays

- Long Replacement Cycles and Lower-Cost Substitute Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Greyscale displays held 61.78% of the United States medical display monitors market share in 2025, which confirms that monochrome visualization still anchors routine radiology and mammography reading volumes. Color displays are projected to record the faster 4.91% CAGR through 2031 as pathology and surgical workflows demand stronger tissue hue fidelity and broader visual context. The United States medical display monitors market still relies on greyscale for high-volume diagnostic work because DICOM GSDF-calibrated monochrome rendering remains the clinical standard for many radiology tasks. That installed base gives greyscale an enduring advantage in replacement demand, even when new use cases are shifting toward color.

Color demand is expanding for clear workflow reasons rather than for cosmetic preference. FDA-cleared pathology systems increasingly reference approved color displays as part of the diagnostic setup, which means monitor selection now sits inside regulated deployment planning instead of general IT sourcing. Surgical visualization is also inherently color dependent because fluorescence guidance, perfusion imaging, and robotic procedures depend on stable rendering during long cases. At the same time, the United States medical display monitors industry is still investing in greyscale product performance, which is visible in EIZO's April 2026 launch of the RadiForce GX570 for mammography use. The type landscape is therefore splitting into 2 durable demand pools, one centered on radiology continuity and another centered on expanding color-critical workflows. That balance keeps greyscale large while allowing color to gain share over the forecast period.

The 2.1 MP to 4 MP band accounted for 32.16% of the United States medical display monitors market size in 2025, which reflects the deep installed base of 3 MP-class workstations used across general imaging and review environments. This band remains the practical center of the market because it covers many diagnostic tasks while staying more accessible to facilities with tighter capital budgets. The United States medical display monitors market continues to favor this range for broad deployment because it offers a workable balance between clinical utility and procurement cost. That is why community hospitals and many outpatient sites still fall within this mid-range tier.

The 4.1 MP to 8 MP band is forecast to grow at a 4.73% CAGR through 2031 as mammography and whole-slide imaging create stronger demand for sustained high-resolution rendering. The April 2024 USPSTF breast cancer screening recommendation lowered the starting age for routine screening to 40, which expands the long-term screening base and supports continued equipment demand in accredited breast imaging settings. At the top end, Barco's Coronis OneLook brings 32 MP capability to breast imaging review, showing how premium resolution is being used to improve throughput in high-volume programs. The United States medical display monitors industry is therefore seeing a reshaping effect rather than a full migration, because mid-range remains dominant while high-resolution demand expands in clinically specific settings. Segments above 8 MP stay niche, but their relevance is rising in breast imaging, advanced surgical applications, and specialized academic environments where panning reduction and full-field review matter.

List of Companies Covered in this Report:

- Advantech Co., Ltd.

- ASUS

- Barco NV

- Canvys (Richardson Electronics, Ltd.)

- Double Black Imaging Corporation

- EIZO Corporation

- FSN Medical Technologies

- FUJIFILM Healthcare Americas Corporation

- HP Development Company, L.P

- Image Diagnostics Inc.

- JVCKENWOOD Corporation

- Karl Storz

- LG Electronics Inc.

- Novanta Inc.

- Olympus America Inc.

- Rein Medical GmbH

- Reshin Monitors

- Sony Group

- Stryker

- STERIS

- WIDE USA

- Winmate Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Imaging-Center Expansion and Reading-Room Modernization

- 4.2.2 4K Minimally Invasive and Hybrid OR Upgrade Cycle

- 4.2.3 Higher Breast Imaging and Oncology Read Volumes

- 4.2.4 AI-Enabled Multi-Modality Workflow Complexity Favors Premium Diagnostic Displays

- 4.2.5 FDA-Cleared Digital Pathology Primary Diagnosis Adoption

- 4.2.6 Zero-Footprint Diagnostic Viewing Raising Remote QA Demand

- 4.3 Market Restraints

- 4.3.1 High Acquisition Cost for Premium Diagnostic and Surgical Displays

- 4.3.2 Long Replacement Cycles and Lower-Cost Substitute Pressure

- 4.3.3 2026 QMSR Compliance Burden for Device Makers

- 4.3.4 Web Viewer Adoption Deferring Some Dedicated Workstation Display Upgrades

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Greyscale

- 5.1.2 Color

- 5.2 By Resolution

- 5.2.1 Up to 2 MP

- 5.2.2 2.1 MP to 4 MP

- 5.2.3 4.1 MP to 8 MP

- 5.2.4 Above 8 MP

- 5.3 By Technology

- 5.3.1 LED-backlit LCD

- 5.3.2 OLED

- 5.3.3 CCFL-backlit LCD

- 5.4 By Application

- 5.4.1 General Radiology and Diagnostic Imaging

- 5.4.2 Mammography

- 5.4.3 Surgery and Interventional Imaging

- 5.4.4 Digital Pathology

- 5.4.5 Dentistry

- 5.4.6 Clinical Review, Education, and Telemedicine

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Imaging Centers and Diagnostic Laboratories

- 5.5.3 Specialty Clinics

- 5.5.4 Ambulatory Surgical Centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Advantech Co., Ltd.

- 6.3.2 ASUS

- 6.3.3 Barco NV

- 6.3.4 Canvys (Richardson Electronics, Ltd.)

- 6.3.5 Double Black Imaging Corporation

- 6.3.6 EIZO Corporation

- 6.3.7 FSN Medical Technologies

- 6.3.8 FUJIFILM Healthcare Americas Corporation

- 6.3.9 HP Development Company, L.P

- 6.3.10 Image Diagnostics Inc.

- 6.3.11 JVCKENWOOD Corporation

- 6.3.12 KARL STORZ SE & Co. KG

- 6.3.13 LG Electronics Inc.

- 6.3.14 Novanta Inc.

- 6.3.15 Olympus America Inc.

- 6.3.16 Rein Medical GmbH

- 6.3.17 Reshin Monitors

- 6.3.18 Sony Group Corporation

- 6.3.19 Stryker Corporation

- 6.3.20 Steris

- 6.3.21 WIDE USA

- 6.3.22 Winmate Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment