|

시장보고서

상품코드

2065789

바지선 운송 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Barge Transportation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

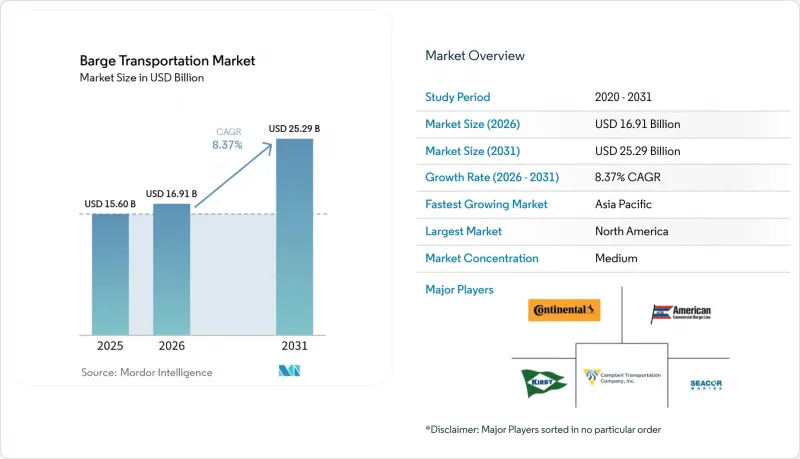

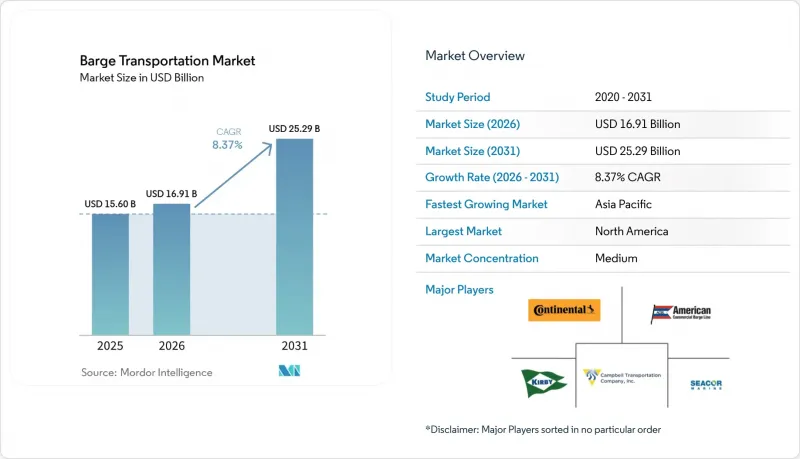

Mordor Intelligence에 의하면, 바지선 운송 시장 규모는 2025년에 156억 달러, 2026년에 169억 1,000만 달러, 2031년까지 252억 9,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 8.37%로 성장할 전망입니다.

본 보고서에서는 업계를 ‘바지선 선단의 유형’(건화물용 바지선, 액체화물용 바지선, 특수용도 바지선), ‘화물/최종 이용 산업’(농산물, 석탄·원유 제품, 화학제품·비료 등), ‘바지선 운송 활동’(내륙/국내, 연안/외해) 및 ‘지역’(북미 등)별로 분류하고 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 바지선 운송 시장 동향과 인사이트

세계 해상 무역의 확대가 내륙 수로 이용을 촉진

연안 항구의 화물 처리량은 꾸준히 증가하고 있으며, 이는 내륙 바지선 운송에 대한 ‘퍼스트 마일’ 및 ‘라스트 마일’ 수요를 뒷받침하고 있습니다. 바지선은 트럭에 비해 톤마일당 온실가스 배출량이 89% 적어, 화주사의 지속가능성 목표에 부합합니다. DP 월드 앤트워프 경영진에 따르면, 컨테이너의 35%는 이미 바지선을 통해 선적되어 터미널의 혼잡이 완화되고 있습니다. 멕시코만이나 양쯔강 삼각주 지역에서도 항만들이 내륙 지역의 물류를 수운으로 전환함으로써 처리량을 유지하려 하고 있어, 이와 유사한 움직임이 확대되고 있습니다. 각국 정부는 장기적인 인프라 계획에서 준설 및 수문 개보수를 우선시함으로써 이러한 전환을 뒷받침하고 있습니다. 항만 커뮤니티 시스템과 내륙 터미널 간의 지속적인 통합은 신뢰할 수 있는 일정 관리와 신속한 선박 회전율을 뒷받침하며, 바지선 운송 시장에 더욱 탄력을 불어넣고 있습니다.

연료 가격 변동 속에서 비용 면에서의 우위가 매력을 높이고 있습니다.

내륙 바지선의 연비는 갤런당 514톤마일에 달하며, 철도나 트럭과 같은 대체 수단을 훨씬 능가합니다. 15척의 바지선으로 구성된 1개의 예인 선단은 약 1,050대의 트럭에 해당하는 수송량을 담당할 수 있으며, 디젤 가격 변동이 지속되는 가운데 운임 절감으로 이어집니다. 프린스턴 TMX의 분석에 따르면, 화물을 도로 운송에서 수로 운송으로 전환함으로써 벌크 화물 운송업체의 총 착륙 비용을 20% 절감할 수 있는 것으로 나타났습니다. 에너지 시장의 변동이 지속되는 가운데, 계약 운송업체들은 예측 가능성을 확보하기 위해 수년에 걸친 바지선 운송 능력을 확보하고 있습니다. 이러한 비용 절감 효과는 공급망 전반으로 파급되어, 상품 생산자들이 효율적인 복합 운송의 거점인 하천 항구를 중심으로 물류 네트워크 재구축을 추진하도록 촉진하고 있습니다.

노후화된 인프라가 운항상의 병목 현상을 초래하고 있습니다.

미국 수문의 80% 이상이 당초 설계 수명인 50년을 초과하여, 잦은 폐쇄로 인해 항해 지연과 비용 증가를 초래하고 있습니다. 미시시피강의 제25수문에 대한 조사 결과, 30일간 가동이 중단될 경우 미국의 GDP가 31억 달러 감소할 우려가 있다고 경고하고 있습니다. ‘인프라 투자·고용법’에 따라 내륙 지역 건설에 29억 달러가 투입되고 있지만, 유지 관리 미해결 과제는 여전히 막대한 양에 달할 전망입니다. 유럽에서도 다뉴브강에서 유사한 문제에 직면해 있으며, 노후화된 구조물로 인해 수요가 최고조에 달할 때 선저 깊이가 제한되고 있습니다. 예기치 못한 운행 중단은 일정의 신뢰성을 떨어뜨리고, 일부 화주들이 철도 운송 계약을 통해 위험을 헤지하도록 유도하는 결과를 낳아, 바지선 운송 시장의 활기를 위축시키고 있습니다.

부문별 분석

2025년, 건화물 바지선은 벌크 화물 시장에서 가장 큰 점유율을 차지했으며, 바지선 운송 시장 점유율의 47.55%를 차지했습니다. 이 선박들은 적재 용량을 최적화할 수 있고, 단위당 운영 비용도 저렴하기 때문에 화물의 대부분은 곡물, 석탄, 금속 광석이 차지하고 있습니다. 선단에 대한 수요는 수확기나 에너지 주기와 연동되어 있으며, 운항 사업자들은 정기적인 유지보수를 통해 자산의 수명을 연장하고 있습니다. 특수 선박의 수는 급속히 증가하고 있으며, 조선소들이 새로운 틈새 시장에 대응하기 위해 LNG 벙커링 선박, 거주 구역을 갖춘 선박, 그리고 탄소 포집 기능을 갖춘 선체를 납품함에 따라 연평균 성장률(CAGR)은 8.92%로 전망됩니다. 2025년 5월에 승인된 텍사스 시티 선박 운하 최초의 LNG 급유 허브에는 선박 및 육상 시설에 최소 3억 달러가 투자될 예정입니다. 대체 연료에 관한 규제가 명확해진 데 더해, 전용으로 설계된 선박에 대한 높은 용선료가 바지선 운송 시장을 견인하는 장기적인 설비 발주를 뒷받침하고 있습니다.

화학제품 및 석유 전용 탱커 바지는 안전 기준 준수가 서비스의 차별화 요인으로 작용하고 있어, 계속해서 수익성을 유지하고 있습니다. 미국 선급협회(ABS)는 LNG 및 메탄올 연료 공급 시스템에 관한 엄격한 지침을 발표하여, 선주가 프리미엄 계약을 체결할 수 있도록 지원하고 있습니다. 이산화탄소 포집 실증 프로그램에서는 걸프 연안 내수로(Gulf Intracoastal Waterway)를 통해 액화 CO2를 수송하는 바지선의 운항이 계획되어 있어, 새로운 수요원의 출현을 시사하고 있습니다. 도료, 증기 제어 콘솔, 실시간 모니터링 시스템에 대한 지속적인 투자 덕분에 진입 장벽은 여전히 높게 유지되고 있으며, 바지선 운송 업계의 이 분야에서 가동률과 이익률은 안정적으로 유지되고 있습니다.

지역별 분석

북미는 미시시피강, 오하이오강, 일리노이강을 중심으로 2025년 매출의 41.60%를 차지했습니다. 내륙 수로 개선을 위해 연방 정부가 29억 달러의 예산을 배정함에 따라 수문의 신뢰성과 수심 활용도가 향상되었으며, 2022년 화물 처리량은 역사적인 저수위 상황에도 불구하고 2억 5,700만 톤을 넘어섰습니다. 잉그램 바지 컴퍼니(Ingram Barge Company)는 SEACOR사로부터 1,000척 이상의 바지를 추가로 도입하여 지속적인 수요에 부응하기 위해 네트워크를 확장하고 있습니다. Mythos AI가 시범 운영 중인 자율 조종 시스템은 미국 해안경비대의 원격 선박 조종 관련 규정이 마련되면 효율성을 한층 더 높일 가능성이 있습니다.

아시아태평양은 연평균 성장률(CAGR) 7.18%를 기록하며, 바지선 운송 시장에서 단기적으로 가장 견조한 성장 전망을 보이고 있습니다. 중국은 양쯔강의 수심 증설에 막대한 자원을 투입하고 있으며, 지방 자치 단체는 내륙 항구에서 바지선에서 트럭으로의 환적을 효율화하여 병목 현상을 해소하고자 하고 있습니다. 또한, ‘지역 종합적 경제 동반자 협정(RCEP)’은 지역 내 생산 거점의 이전을 촉진하고, 더 많은 중간재를 수로로 운송하도록 장려하고 있습니다. 동남아시아에서는 해상 화물 운송이 이미 무역액의 61%를 차지하고 있으며, 새로운 복합 운송 회랑을 통해 내륙 지방으로도 바지선의 운행 범위가 확대되고 있습니다.

유럽은 로테르담과 안트베르펜·브뤼헤가 합쳐서 연간 500억 유로의 부가가치를 창출하고 있다는 점을 바탕으로, 바지선 운송 시장에서 여전히 매우 중요한 위치를 차지하고 있습니다. NAIADES 프로그램은 2030년까지 내륙 운송량을 25% 늘리는 것을 목표로 하고 있으며, 이를 위해서는 무공해 선박과 스마트 교통 관리가 필수적입니다. 그러나 기후 변화로 인한 라인강의 수위 저하로 인해 화물이 정기적으로 철도로 우회되는 경우가 있어, 하천 수송의 취약성이 부각되고 있습니다. 따라서 수문의 심화 공사와 수위 예측 자동화에 대한 투자는 바지선 운송 시장을 보호하기 위한 정책적 우선순위가 됩니다.

남미는 농업 수출 강국으로 부상하고 있으며, 대두와 옥수수의 운송은 꾸준히 바지선으로 전환되고 있습니다. 2010년부터 2023년까지, 바지를 이용한 옥수수 수출 비중은 3%에서 16%로 증가했습니다. 이는 타파조스 강과 마데이라 강에서 운임 인하 효과가 반영된 것입니다. PALFINGER MARINE사의 브라질 철광석 운송 프로그램은 광업이 바지선 수요의 추가 확대를 주도하고 있음을 보여줍니다. 파라과이-파라나 수로 연안의 습지 보호를 둘러싼 논의는 환경 측면에서의 감시가 강화되고 있음을 보여주고 있으며, 이는 향후 프로젝트의 허가 취득 일정에 영향을 미칠 가능성이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the barge transportation market size is projected to be USD 15.60 billion in 2025, USD 16.91 billion in 2026, and reach USD 25.29 billion by 2031, growing at a CAGR of 8.37% from 2026 to 2031.

This report Segments the Industry Into by Barge Fleet Type (Dry Cargo Barges, Liquid Cargo Barges and Specialty Barges), by Cargo / End-Use Industry (Agricultural Products, Coal & Crude Petroleum Products, Chemicals & Fertilizers and More), by Barging Activity (Inland / Domestic and Coastal / Ocean-Going), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Barge Transportation Market Trends and Insights

Expansion of global seaborne trade driving inland waterway utilization

Cargo volumes handled at coastal ports continue to climb, propelling first- and last-mile demand for inland barge moves. Barges generate 89% lower greenhouse-gas emissions per ton-mile than trucks, which aligns with shipper sustainability targets. At DP World Antwerp, management reports that 35% of containers already depart by barge, reducing terminal congestion. Similar initiatives are expanding in the Gulf of Mexico and the Yangtze River Delta as ports look to preserve throughput by shifting hinterland flows onto water. Governments reinforce the shift by prioritizing dredging and lock upgrades in long-range infrastructure plans. Continuous integration of port community systems with inland terminals underpins reliable scheduling and quicker turnarounds, giving the barge transportation market further momentum.

Cost advantage amplifying appeal amid fuel price volatility

Inland barges achieve 514 ton-miles per gallon, far outperforming rail and truck alternatives. A single 15-barge tow displaces roughly 1,050 trucks, which lowers freight bills at a time when diesel prices are trending higher. Princeton TMX analysis shows the total landed cost for bulk shippers can fall by 20% when loads migrate from highway to waterways. As energy markets remain volatile, contract shippers lock in multiyear barge capacity to secure predictability. These savings cascade through supply chains, encouraging commodity producers to reconfigure distribution footprints around river ports that offer efficient multimodal interchange.

Aging infrastructure creating operational bottlenecks

More than 80% of United States locks have exceeded the original 50-year design horizon, triggering frequent closures that delay voyages and raise costs. A study on the Mississippi's Lock 25 warned that a 30-day outage could trim national GDP by USD 3.1 billion. Although the Infrastructure Investment and Jobs Act channels USD 2.9 billion into inland construction, the maintenance backlog remains large. Europe faces a comparable challenge on the Danube where aging structures restrict draft during peak demand. Unplanned downtime erodes schedule reliability and encourages some shippers to hedge with rail contracts, dampening the barge transportation market.

Other drivers and restraints analyzed in the detailed report include:

- Growing biofuel and chemical movements requiring specialized tank barges

- Digitalization and autonomous-navigation technologies boosting fleet productivity

- Climate variability disrupting navigation and service reliability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dry cargo barges moved the largest share of bulk goods in 2025 and held 47.55% of barge transportation market share. Grain, coal and metal ores dominate their manifests because these vessels optimize cubic capacity and incur low unit operating cost. Fleet demand tracks harvest and energy cycles, and operators stretch asset lives through standard maintenance. Specialty barges are rising quickly, posting a forecast 8.92% CAGR as shipyards deliver LNG bunkering, accommodation and carbon-capture hulls that serve new niches. The first LNG bunkering hub on the Texas City Ship Channel, approved in May 2025, will invest at least USD 300 million in vessels and shore facilities. Regulatory certainty on alternative fuels, plus higher charter rates for purpose-built units, underpins long-term equipment orders that lift the barge transportation market.

Tank barges dedicated to chemicals and petroleum remain profitable because safety compliance differentiates service. The American Bureau of Shipping issued strict guidelines on LNG and methanol fueling systems, enabling owners to qualify for premium contracts. Carbon-capture demonstration programs envision liquefied CO2 barges operating on the Gulf Intracoastal Waterway, hinting at fresh demand pools. Continuous investment in coatings, vapor-control consoles and real-time monitoring keeps barriers to entry high, preserving utilization and margins within this slice of the barge transportation industry.

Geography Analysis

North America generated 41.60% of 2025 revenue, anchored by the Mississippi, Ohio and Illinois rivers. Federal allocations of USD 2.9 billion for inland upgrades improve lock reliability and draft availability, and 2022 cargo throughput surpassed 257 million tons despite historic low water. Ingram Barge Company's addition of more than 1,000 barges from SEACOR scales its network to meet durable demand. Autonomous pilots, as tested by Mythos AI, could unlock further efficiency once United States Coast Guard rules on remote operations mature.

Asia-Pacific holds the strongest near-term growth outlook in the barge transportation market with an 7.18% CAGR. China pours resources into deepening the Yangtze, and local authorities streamline barge-truck transfers at inland ports to remove bottlenecks. The Regional Comprehensive Economic Partnership encourages regional production shifts that move more intermediate goods on waterways. In Southeast Asia, maritime freight already accounts for 61% of trade value, and new intermodal corridors extend barge reach into land-locked provinces.

Europe remains pivotal in the barge transportation market, underpinned by Rotterdam and Antwerp-Bruges which together add EUR 50 billion of value annually. The NAIADES programme seeks a 25% jump in inland volumes by 2030, requiring zero-emission vessels and smart traffic management. Yet climate-related low Rhine levels periodically divert freight to rail, showing the vulnerability of river transport. Investment in lock deepening and automated water-level forecasting is therefore a policy priority that safeguards the barge transportation market.

South America emerges as an agricultural export powerhouse with soy and corn flows shifting steadily toward barges. Corn exports that used barges rose from 3% to 16% between 2010 and 2023, reflecting freight savings on the Tapajos and Madeira rivers. PALFINGER MARINE's Brazilian iron-ore program demonstrates how mining drives additional barge demand. Debate over wetland protection along the Paraguay-Parana waterway shows environmental scrutiny is intensifying, which could shape permitting timelines for future projects.

- Kirby Corporation

- Ingram Marine Group

- American Commercial Barge Line (ACBL)

- SEACOR Holdings Inc.

- Campbell Transportation Company

- Canal Barge Company

- SCF Marine Inc.

- Blessey Marine Services

- Florida Marine Transporters

- PACC Offshore Services Holdings (POSH)

- PT Pelayaran Nasional Indonesia (PELNI)

- Rhenus Group

- Danube Shipping Management Service GmbH

- Imperial Logistics International

- VTG AG

- GAC Saudi Arabia

- Qinhuangdao Tianhang Shipping Co.

- Simatech Shipping LLC

- Mercuria Energy Group (Stema Shipping)

- Hvide Sande Supply (Esbjerg)*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of global seaborne trade shifting first/last-mile volumes to inland waterways

- 4.2.2 Cost advantage of barges over rail & trucking amid rising fuel prices

- 4.2.3 Growing biofuel and chemical movements requiring specialized tank barges

- 4.2.4 Digitalization and autonomous-navigation technologies boosting fleet productivity

- 4.2.5 International climate policies favoring low-emission waterborne freight

- 4.2.6 Rising global investment in dredging and lock modernization projects

- 4.3 Market Restraints

- 4.3.1 Aging inland waterway infrastructure causing congestion and downtime

- 4.3.2 Climate-driven water-level variability undermining service reliability

- 4.3.3 High capital cost of low-emission barge newbuilds and retrofits

- 4.3.4 Intensifying competition from upgraded rail freight corridors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Barge Fleet Type

- 5.1.1 Dry Cargo Barges

- 5.1.2 Liquid Cargo Barges

- 5.1.3 Specialty Barges

- 5.2 By Cargo / End-use Industry

- 5.2.1 Agricultural Products

- 5.2.2 Coal & Crude Petroleum Products

- 5.2.3 Chemicals & Fertilizers

- 5.2.4 Metal Ores & Alloys

- 5.2.5 Project & Oversized Cargo

- 5.2.6 Others

- 5.3 By Barging Activity

- 5.3.1 Inland / Domestic

- 5.3.2 Coastal / Ocean-going

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Asia Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Spain

- 5.4.4.5 Italy

- 5.4.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.4.8 Rest of Europe

- 5.4.5 Middle East And Africa

- 5.4.5.1 United Arab of Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East And Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Kirby Corporation

- 6.4.2 Ingram Marine Group

- 6.4.3 American Commercial Barge Line (ACBL)

- 6.4.4 SEACOR Holdings Inc.

- 6.4.5 Campbell Transportation Company

- 6.4.6 Canal Barge Company

- 6.4.7 SCF Marine Inc.

- 6.4.8 Blessey Marine Services

- 6.4.9 Florida Marine Transporters

- 6.4.10 PACC Offshore Services Holdings (POSH)

- 6.4.11 PT Pelayaran Nasional Indonesia (PELNI)

- 6.4.12 Rhenus Group

- 6.4.13 Danube Shipping Management Service GmbH

- 6.4.14 Imperial Logistics International

- 6.4.15 VTG AG

- 6.4.16 GAC Saudi Arabia

- 6.4.17 Qinhuangdao Tianhang Shipping Co.

- 6.4.18 Simatech Shipping LLC

- 6.4.19 Mercuria Energy Group (Stema Shipping)

- 6.4.20 Hvide Sande Supply (Esbjerg)*