|

시장보고서

상품코드

2066415

인도의 화물 및 물류 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

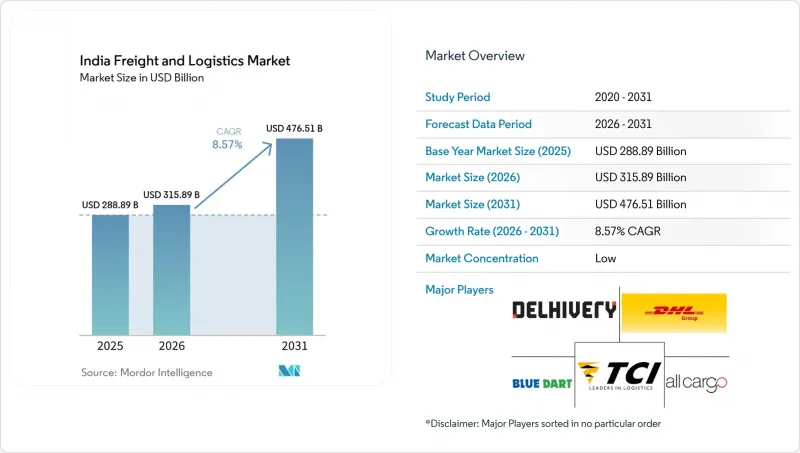

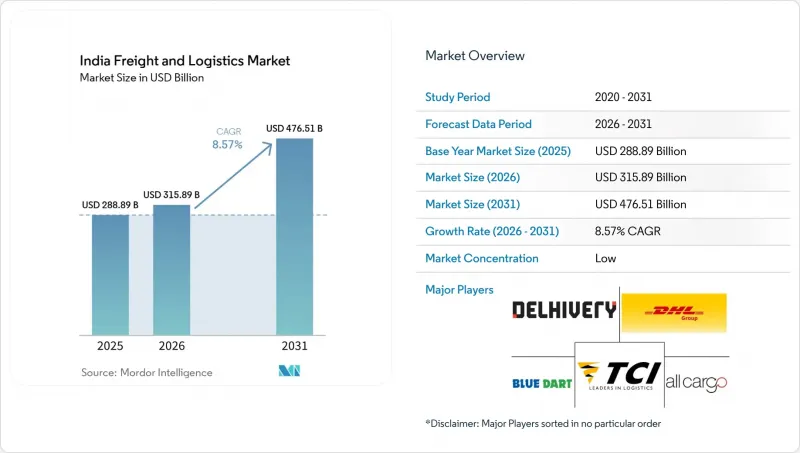

Mordor Intelligence에 의하면, 인도의 화물 및 물류 시장 규모는 2025년 2,888억 9,000만 달러로 평가되었습니다. 2026년에는 3,158억 9,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 8.57%로 성장을 지속하여, 2031년에는 4,765억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 최종 사용자 산업별(농업, 어업 및 임업, 건설, 제조업, 석유 및 가스, 광업·채석업, 도매·소매업, 기타) 및 물류 기능별(택배·특송·소포(CEP), 화물 포워딩, 화물 운송, 창고·보관, 기타 서비스)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 화물 및 물류 시장 동향 및 인사이트

옴니채널 및 D2C 주문 처리의 급증

D2C(소비자 직접 판매) 브랜드는 출하 규모를 세분화하고 있어, 소비 집적지 반경 15킬로미터 내에 위치한 마이크로 풀필먼트 센터에 대한 수요를 견인하고 있습니다. Flipkart는 2024년까지 네트워크를 1,400곳 이상의 물류 및 분류 센터로 확대하고, 1만 9,000개 우편번호 지역 전역에서 익일 배송을 보장하겠다고 밝혔습니다. 아마존 인도의 ‘I Have Space’는 2만 8,000곳의 키라나 매장을 라스트 마일 거점으로 등록하여 주문당 비용을 최대 22% 절감했습니다. 소규모 D2C 브랜드들은 다년간의 임대 계약 대신 6개월 단위의 창고 계약을 체결하고 있으며, 이로 인해 3PL 사업자들은 유연한 수용 능력을 구축해야 할 필요가 있습니다. Blinkit과 같은 퀵커머스 사업자들은 수요가 집중되는 지역으로부터 2킬로미터 반경 내에 도심형 다크스토어를 필요로 하고 있으며, 이는 구역 지정 개혁과 라스트마일 자동화를 촉진하고 있습니다. 전반적으로, D2C 매출 증가는 인도의 화물 및 물류 시장에서 키팅 및 당일 반품과 같은 부가가치 서비스의 확대를 뒷받침하고 있습니다.

실시간 시각화 및 예상 도착 시간(ETA)의 의무화

현재 기업 화주들은 일반적인 ‘운송 중’이라는 상태 표시가 아닌, 상세한 GPS 데이터와 머신러닝을 통한 ETA(예정 도착 시간) 업데이트를 기대하고 있습니다. Blue Dart사는 2024년, 1만 8,000대의 차량으로 구성된 자사 차량 전체에 IoT 추적기를 도입하여 고객 문의 건수를 31% 줄였습니다. 인도 컨테이너 공사(CCI)는 철도 운송을 FOIS 시스템과 통합하여, 60곳의 내륙 물류센터에 있는 컨테이너의 위치 정보를 수출업체에게 실시간으로 제공합니다. FASTag를 통한 통행료 징수가 의무화됨에 따라 현재 매월 12억 건의 경로 데이터가 생성되고 있으며, 이를 통해 화물 매칭 엔진이 빈차 주행 거리 감소를 실현하고 있습니다. 온도 관리가 이루어지는 차량군에서는 텔레매틱스를 활용하여 콜드체인에서의 상품 손실률을 4% 가까이 낮추고 있습니다. 이러한 시각화에 대한 투자는 인도의 화물 및 물류 시장에서 자산 활용도를 높이고, 화주의 충성도를 높이는 데 기여하고 있습니다.

운전기사 부족과 높은 이직률

2024년에는 필요한 상업용 운전기사 수와 실제 공급 수 사이에 22%의 격차가 발생하여, 배송 지연과 임금 상승을 악화시켰습니다. 장거리 운전기사들의 이직률은 가혹한 근무 일정과 도로변 시설의 미비로 인해 38%까지 상승했습니다. 피로가 트럭 관련 사고의 12%를 차지함에 따라, 보험사는 보험료를 인상했습니다. 팀 운전 모델에서는 인건비가 최대 50% 증가하기 때문에 이 모델의 도입은 고부가가치 화물로 제한되고 있습니다. 정부의 훈련 프로그램에서는 2024년에 목표인 10만 명 중 고작 4만 7,000명의 신규 운전자가만 자격을 취득했습니다. 강력한 기술 향상 인센티브가 없다면, 인력 부족이 인도의 화물 및 물류 시장의 성장세를 계속해서 저해할 것입니다.

부문별 분석

2025년에는 도매·소매업이 매출액의 33.52%를 차지했으며, 체계화된 소매망의 확대에 따라 2026년부터 2031년까지 연평균 성장률(CAGR) 9.20%로 성장할 것으로 전망됩니다. 릴라이언스 리테일의 8개 물류 센터에 도입된 자동 분류 시스템 덕분에 매장으로의 재고 보충 주기가 48시간으로 단축되었습니다.

제조업의 물류는 적시생산(JIT) 방식의 주문 관리에 의존하고 있으며, 타타 모터스는 공급업체 관리 재고(VMI) 프로그램을 통해 재고 일수를 2.8일로 단축했습니다. 농업 물자의 경우, 농촌 지역의 도로망이 미비하여 여전히 연간 최대 140억 달러에 달하는 수확 후 손실이라는 과제에 직면해 있습니다. 다양한 분야 수요에 힘입어, 인도의 화물 및 물류 시장의 수익원은 계속해서 다각화되고 있습니다.

2025년에는 화물 운송이 62.96%의 점유율을 차지하며 주도적인 위치를 차지했으나, 2024년에 전자상거래 출하량이 29% 증가한 데 힘입어 CEP 부문은 연평균 성장률(CAGR) 9.92%(2026-2031년)로 성장하고 있습니다. Delhivery사의 100개 분류 센터는 각 센터에서 하루 최대 10만 개의 소포를 처리하고 있으며, 이는 CEP 분야를 휩쓸고 있는 자동화의 물결을 여실히 보여주고 있습니다.

자산 집약형 화물 운송 사업자들은 저배출 가스 규제에 대응하기 위해 전기 배송 밴을 도입하고 있습니다. Blue Dart는 2024년에 320대를 도입하여, 1회 배송당 배출량을 18% 줄였습니다. 인도 우정공사의 ‘Speed Post Express’는 15만 5,000곳의 우체국을 활용해 3차 도시까지 배송을 진행하고 있으며, 이는 이 시장의 롱테일 부문에서 비즈니스 기회를 부각시키고 있습니다. 소포 물량이 증가하는 가운데, 통합형 창고 관리와 라스트 마일 최적화가 인도의 화물 및 물류 시장의 경쟁 우위를 확보하는 기반이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the india freight and logistics market size is expected to grow from USD 288.89 billion in 2025 to USD 315.89 billion in 2026 and is forecast to reach USD 476.51 billion by 2031 at 8.57% CAGR over 2026-2031.

This report is Segmented by End-User Industry (Agriculture, Fishing and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).

India Freight And Logistics Market Trends and Insights

Omnichannel and D2C Fulfilment Surge

Direct-to-consumer brands are fragmenting shipment sizes and driving demand for micro-fulfilment centers located within 15 kilometers of consumption clusters. Flipkart lifted its network to more than 1,400 fulfilment and sortation sites by 2024 to promise next-day delivery across 19,000 pin codes. Amazon India's "I Have Space" enlisted 28,000 kirana stores as last-mile nodes, lowering per-order costs up to 22%. Small D2C brands negotiate six-month warehousing contracts rather than multiyear leases, forcing 3PLs to build flexible capacity. Quick-commerce players such as Blinkit require urban dark stores within two kilometers of demand pockets, spurring zoning reforms and last-mile automation. Overall, rising D2C sales are propelling value-added services like kitting and same-day returns inside the India freight and logistics market .

Real-Time Visibility and Predictive ETA Mandate

Enterprise shippers now expect granular GPS feeds and machine-learning ETA updates instead of generic "in transit" statuses. Blue Dart connected IoT trackers across its 18,000-vehicle fleet in 2024, cutting customer queries by 31%. Container Corporation of India integrated its rail moves with the FOIS system, giving exporters real-time box locations at 60 inland depots. Mandatory FASTag tolling now produces 1.2 billion route data points each month, enabling load-matching engines to curb empty miles. Temperature-controlled fleets employ telematics to reduce cold-chain spoilage to near 4%. These visibility investments improve asset utilization and boost shipper loyalty within the India freight and logistics market .

Driver Shortage and High Attrition

A 22% gap between required and available commercial drivers in 2024 exacerbated delivery delays and wage inflation. Attrition among long-haul drivers rose to 38% because of arduous schedules and poor roadside amenities. Fatigue contributed to 12% of truck-related accidents, prompting insurers to raise premiums. Team-driving models lift labor costs by up to 50%, limiting viability to high-value cargo. Government training programs certified only 47,000 new drivers in 2024 against a target of 100,000. Without robust skilling incentives, personnel shortages will continue to suppress growth momentum in the India freight and logistics market .

Other drivers and restraints analyzed in the detailed report include:

- Flexible Delivery Windows and Anytime Returns

- Pharmaceutical Cold-Chain Integrity Demands

- Highly Fragmented Truck Ownership

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wholesale and retail trade contributed 33.52% of revenue in 2025 and is forecast to grow at a 9.20% CAGR (2026-2031) as organized retail footprints broaden. Reliance Retail's automated sortation in eight distribution centers cut store replenishment cycles to 48 hours.

Manufacturing logistics hinges on just-in-time sequencing; Tata Motors reduced inventory to 2.8 days via a vendor-managed inventory program. Agricultural freight remains challenged by post-harvest losses of up to USD 14 billion annually due to weak rural road connectivity. Diverse sectoral needs continue to diversify revenue streams inside the India freight and logistics market.

Freight transport dominated with a 62.96% share in 2025; however, the CEP segment is scaling at a 9.92% CAGR (2026-2031) as e-commerce shipments climbed 29% in 2024. Delhivery's 100 sortation centers, each processing up to 100,000 parcels daily, illustrate the automation wave gripping CEP.

Asset-heavy freight carriers are deploying electric delivery vans to meet low-emission mandates; Blue Dart introduced 320 units in 2024 and cut per-drop emissions by 18%. India Post's Speed Post Express leverages 155,000 post offices to reach tier-3 towns, underscoring the market's long-tail opportunity. As parcel density rises, integrated warehousing and last-mile orchestration underpin competitive advantage inside the India freight and logistics market.

List of Companies Covered in this Report:

- Adani Ports and SEZ

- Allcargo Logistics, Ltd. (Including Gati Express)

- Amazon

- Blue Dart Express, Ltd.

- Busybees Logistics Solutions Pvt. Ltd.

- Container Corporation of India, Ltd.

- Delhivery, Ltd.

- DHL Group

- DSV A/S (Including DB Schenker)

- DTDC Express, Ltd.

- Ecom Express, Ltd.

- FedEx

- Flipkart Logistics

- Kuehne+Nagel

- LEAP India Pvt. Ltd.

- Mahindra Logistics, Ltd

- Redington, Ltd.

- Safexpress Pvt. Ltd.

- Shadowfax

- Snowman Logistics Ltd.

- TCI (Transport Corporation of India Ltd.)

- TVS Supply Chain Solutions Ltd.

- United Parcel Service of America, Inc. (UPS)

- VRL Logistics Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Logistics Performance

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls and Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.22 Regulatory Framework (Sea and Air)

- 4.23 Value Chain and Distribution Channel Analysis

- 4.24 Market Drivers

- 4.24.1 Omnichannel and D2C Fulfilment Surge

- 4.24.2 Real-Time Visibility and Predictive ETA Mandate

- 4.24.3 Flexible Delivery Windows and "Anytime Returns"

- 4.24.4 Pharmaceutical Cold-Chain Integrity Demands

- 4.24.5 Defence and Aerospace Logistics Outsourcing Surge

- 4.24.6 Ultra-High Service-Level SLAs for Industrial OEMs

- 4.25 Market Restraints

- 4.25.1 Driver Shortage and High Attrition

- 4.25.2 Highly Fragmented Truck Ownership

- 4.25.3 Volatile Diesel and LNG Price Spread

- 4.25.4 Geopolitical Route Volatility (Red Sea / Panama)

- 4.26 Technological Outlook

- 4.27 Porter's Five Forces Analysis

- 4.27.1 Threat of New Entrants

- 4.27.2 Bargaining Power of Buyers

- 4.27.3 Bargaining Power of Suppliers

- 4.27.4 Threat of Substitutes

- 4.27.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value in USD)

- 5.1 By End-User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining, and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 By Logistics Function

- 5.2.1 Courier, Express and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature-Controlled

- 5.2.4.1.2 Temperature-Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express and Parcel (CEP)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Adani Ports and SEZ

- 6.4.2 Allcargo Logistics, Ltd. (Including Gati Express)

- 6.4.3 Amazon

- 6.4.4 Blue Dart Express, Ltd.

- 6.4.5 Busybees Logistics Solutions Pvt. Ltd.

- 6.4.6 Container Corporation of India, Ltd.

- 6.4.7 Delhivery, Ltd.

- 6.4.8 DHL Group

- 6.4.9 DSV A/S (Including DB Schenker)

- 6.4.10 DTDC Express, Ltd.

- 6.4.11 Ecom Express, Ltd.

- 6.4.12 FedEx

- 6.4.13 Flipkart Logistics

- 6.4.14 Kuehne+Nagel

- 6.4.15 LEAP India Pvt. Ltd.

- 6.4.16 Mahindra Logistics, Ltd

- 6.4.17 Redington, Ltd.

- 6.4.18 Safexpress Pvt. Ltd.

- 6.4.19 Shadowfax

- 6.4.20 Snowman Logistics Ltd.

- 6.4.21 TCI (Transport Corporation of India Ltd.)

- 6.4.22 TVS Supply Chain Solutions Ltd.

- 6.4.23 United Parcel Service of America, Inc. (UPS)

- 6.4.24 VRL Logistics Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment