|

시장보고서

상품코드

2066435

유럽의 에폭시 수지 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Epoxy Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

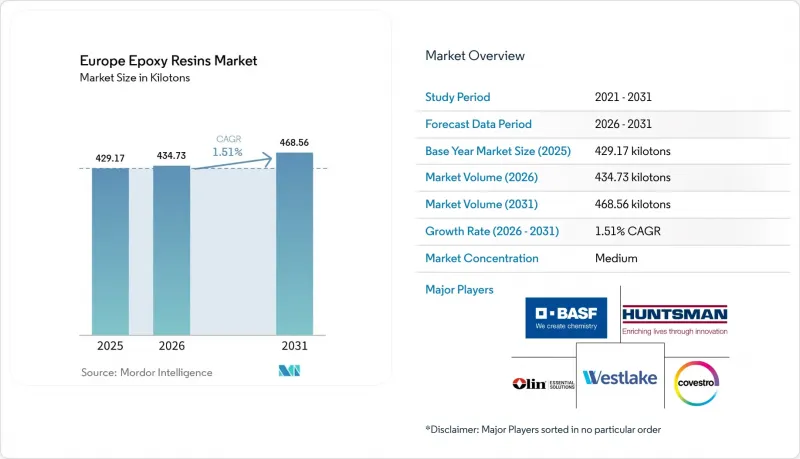

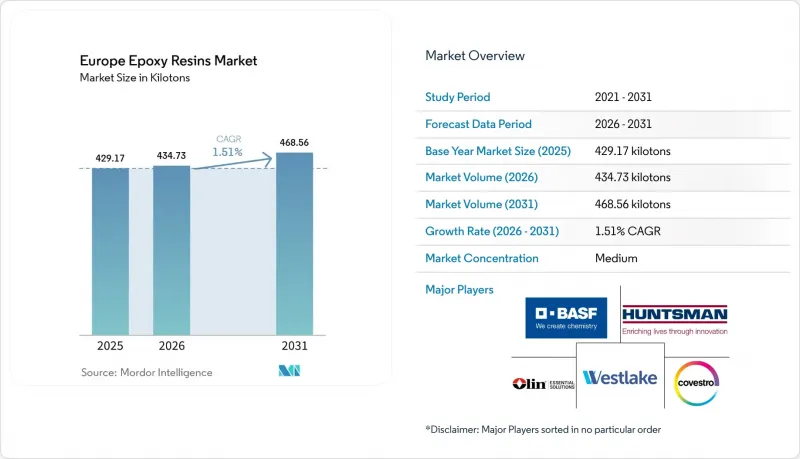

Mordor Intelligence에 의하면, 유럽의 에폭시 수지 시장 규모는 2025년 429.17 킬로톤으로 평가되었고, 2026년에는 434.73 킬로톤으로 추정되고, 2031년까지 468.56 킬로톤에 이를 것으로 예상되며, 2026-2031년 CAGR 1.51%로 성장할 전망입니다.

본 보고서는 원재료별(DGBEA, DGBEF, 노보락, 지방족, 글리시딜아민, 기타 원재료), 용도별(페인트 및 코팅, 접착제 및 실란트, 복합재료, 전기 및 전자기기, 풍력 터빈 등), 지역별(독일, 영국, 프랑스, 이탈리아, 스페인, 러시아, 북유럽 국가, 기타 유럽)로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

유럽의 에폭시 수지 시장 동향 및 분석

풍력 발전용 블레이드 수요의 급증

유럽은 2030년까지 풍력 발전 설비 용량 510 GW 달성을 목표로 하고 있지만, 국제에너지기구(IEA)의 예측에 따르면 유럽 전체에서 370 GW에 그칠 것으로 보이며, 이로 인해 28%의 격차가 발생하고 프로젝트 리드타임이 길어지고 있습니다. 블레이드 생산에는 멀티 MW급 발전기 1기당 최대 10톤의 에폭시 수지가 소비되기 때문에 베스타스(Vestas)와 지멘스 가메사(Siemens Gamesa)가 블레이드 공장을 운영하는 덴마크, 스페인, 이탈리아에서 수지 소비가 주도되고 있습니다. 베스타스는 2024년에 친환경 연구개발(R&D)에 5억 3,100만 유로를 배정했습니다. 이 중 2,050만 유로는 올린(Olin)과 스테나 리사이클링(Stena Recycling)으로 구성된 컨소시엄 ‘CETEC’에 배정되었으며, 이 컨소시엄은 2026년까지 수명이 다한 블레이드의 화학적 재활용 실증에 나설 계획입니다. 이것이 성공하면, 순환형 원료 풀이 형성되어 버진 수지에 대한 수요 압박이 완화될 것입니다. 홋카이도에서 해상 풍력 발전이 확대됨에 따라, 에폭시 화학에 의존하는 선박용 도료 및 해저 그라우트 용도에 대한 수요가 계속해서 증가하고 있습니다.

자동차용 경량 복합재료의 보급 확대

에어버스는 2024년에 A350의 월간 생산 대수를 10대로 늘렸는데, 이 기종의 구조 중 52%에는 에폭시 매트릭스 복합재가 사용되고 있습니다. 헥셀사는 이에 대응하여 프랑스와 오스트리아에 새로운 프리프레그 생산 라인을 신설함으로써, 2024년 4분기 매출을 12.5% 끌어올렸습니다. 자동차 분야에서는 배터리 팩 탑재로 인해 전기차의 중량이 400-500kg 증가함에 따라, 각 OEM 업체들은 강판에서 탄소섬유 에폭시 재질의 차체 패널로 전환을 추진하고 있으며, 이를 통해 최대 50%의 경량화를 달성하고 있습니다. 리카르도사는 2030년까지 유럽의 경차 시장에서 복합재료의 사용 비율이 증가할 것으로 전망하고 있으며, 도레이와 시엔스코사는 이러한 수요에 대응하기 위해 탄소섬유 생산 능력을 확대되고 있습니다.

BPA 및 ECH에 관한 규제 검토

규정 2024/3190에 따라 2025년부터 식품 접촉 재료에 비스페놀 A의 사용이 금지되며, 대형 저장 탱크 및 폴리설폰 막에 대해서는 극히 제한된 예외만 허용됩니다. 이와 병행하여 시행된 CLP 규정 개정에 따라, 일반적인 촉진제에 ‘발암성 물질 1B’ 및 ‘피부 감작성 물질 1A’ 표기가 추가됨에 따라, 중견 제조업체의 규정 준수 비용은 최대 12% 증가하게 될 것입니다. 또한, 새로운 라벨 표시로 인해 제품이 고객의 재인증을 받아야 할 필요가 생겨, 배합 변경에 소요되는 리드타임이 길어지고 있습니다. 이사회 규정 2024/745에 따른 제재 조치로 인해 특정 러시아 기업과의 데이터 공유가 더욱 제한되면서, 특수 등급에 관한 공동 연구 개발이 복잡해지고 있습니다.

부문별 분석

DGBEA는 2025년 유럽 에폭시 수지 시장에서 36.05%의 점유율을 유지했으며, 2031년까지 연평균 성장률(CAGR) 6.05%를 기록할 전망이지만, 비스페놀 A에 대한 의존도가 높기 때문에 배합 제조업체들은 규제 위험에 노출되어 있으며, 이로 인해 비스페놀 F나 노보락 계열 대체품으로의 전환이 촉진되고 있습니다. 노보락 수지는 DGBEA보다 30-40% 높은 가교 밀도를 실현하고 유리 전이 온도를 150°C 이상으로 높이기 때문에 2027년에 인텔의 마그데부르크 공장과 TSMC의 드레스덴 공장이 가동을 시작하면 반도체 봉지 재료로서 필수적인 소재가 될 것입니다. 따라서 유럽의 에폭시 수지 시장에서 노보락 등급 시장 규모는 기준치보다 빠르게 확대될 전망입니다. 글리시딜아민계 수지는 200°C를 초과하는 유리전이 온도를 가지며, 에어버스 A350의 운용 요건을 충족하기 때문에 항공우주용 프리프레그의 기준이 되고 있습니다. 한편, 시클로 알킬 및 알킬 등급은 장식용 마감 및 LED 봉지 공정에서 요구되는 자외선 안정성을 충족합니다. REACH 신청 수수료 및 데이터 공유 의무로 인해 업계 재편이 진행되고 있으며, 수직 통합형 대기업은 규정 준수 비용을 더 넓은 생산량에 분산할 수 있기 때문에 우위를 유지하고 있습니다.

또한, 원료 제조업체들은 글리세롤 유래의 바이오 에피클로로히드린에 대한 검증 작업도 진행하고 있습니다. 상업적 공급량은 제한적이지만, 규모 확대에 성공한다면 염소 사용량을 줄이고 탄소 발자국을 개선할 수 있을 것입니다. 현재 진행 중인 시험 결과, 바닥재와 전기용 포팅재의 성능 면에서 동등한 수준인 것으로 나타났으나, 비용 면에서 동등한 수준을 달성하기 위해서는 아시아에서의 생산 능력 확대나 유럽 내 전용 공장 건설이 필요합니다. 그동안 대부분의 제조업체는 기계적 성능과 가격의 균형을 맞추기 위해, 바이오 유래 성분과 기존 원료를 혼합함으로써 위험을 분산시켜 왔습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the europe epoxy resins market size is expected to increase from 429.17 kilotons in 2025 to 434.73 kilotons in 2026 and reach 468.56 kilotons by 2031, growing at a CAGR of 1.51% over 2026-2031.

This report is Segmented by Raw Material (DGBEA, DGBEF, Novolac, Aliphatic, Glycidylamine, and Other Raw Materials), Application (Paints and Coatings, Adhesives and Sealants, Composites, Electrical and Electronics, Wind Turbines, and More), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, Nordic Countries, and Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Tons).

Europe Epoxy Resins Market Trends and Insights

Surge in Wind-Energy Blade Demand

Europe aims to achieve 510 GW of installed wind capacity by 2030; however, the International Energy Agency forecasts the continent will reach only 370 GW, resulting in a 28% gap that is lengthening project lead times. Blade production consumes up to 10 tons of epoxy per multi-MW unit, driving resin consumption across Denmark, Spain, and Italy, where Vestas and Siemens Gamesa run blade plants. Vestas earmarked EUR 531 million for green R&D in 2024, with EUR 20.5 million allocated to CETEC, a consortium comprising Olin and Stena Recycling, which aims to demonstrate the chemical recycling of end-of-life blades by 2026. Success would create a circular feedstock pool and alleviate pressures on virgin resin demand. Offshore wind growth in the North Sea continues to drive demand for marine coatings and subsea grout applications, which also rely on epoxy chemistry.

Lightweight Automotive Composites Push

Airbus increased A350 output to 10 aircraft per month in 2024, and the model uses epoxy-matrix composites for 52% of its structure. Hexcel responded with new prepreg lines in France and Austria, supporting a 12.5% sales rise in Q4 2024. On the road, battery packs add 400-500 kg to electric vehicles, prompting OEMs to switch from steel to carbon-fiber epoxy body panels, which reduce mass by up to 50%. Ricardo projects rising composite content in European light vehicles through 2030, while Toray and Syensqo have expanded carbon-fiber capacity to meet demand.

BPA and ECH Regulatory Scrutiny

Regulation 2024/3190 bans bisphenol A in food-contact materials from 2025, leaving only narrow derogations for large storage tanks and polysulfone membranes. Parallel CLP amendments add Carcinogen 1B and Skin Sensitizer 1A tags to popular accelerators, raising compliance costs by up to 12% for mid-tier producers. The new labels also extend reformulation lead times as products pass customer requalification. Sanctions under Council Regulation 2024/745 further restrict data sharing with certain Russian entities, complicating joint research and development on specialty grades.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Electronics and Electricals Manufacturing

- Rebound in Protective Construction Coatings

- Crude-Linked Raw-Material Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DGBEA retained 36.05% of Europe epoxy resin market share in 2025 and is trending at a 6.05% CAGR to 2031, yet its reliance on bisphenol A exposes formulators to regulatory risk that is triggering a pivot toward bisphenol-F and novolac alternatives. Novolac resins deliver crosslink densities 30-40% above DGBEA, raising glass-transition temperatures beyond 150°C and making them indispensable for semiconductor encapsulation once Intel's Magdeburg and TSMC's Dresden lines commence operation in 2027. Europe epoxy resin market size for novolac grades is therefore set to expand more quickly than the baseline. Glycidylamine systems remain the benchmark for aerospace prepregs due to their glass-transition temperatures above 200°C, which meet Airbus A350 service requirements. Meanwhile, cycloaliphatic and aliphatic grades address ultraviolet stability in decorative finishes and LED encapsulation. REACH fees and data-sharing obligations have encouraged consolidation, giving vertically integrated majors an edge as they can amortize compliance costs across broader volumes.

Formulators are also validating bio-based epichlorohydrin from glycerol. While commercial supply is limited, a successful scale-up would reduce chlorine use and improve carbon footprints. Ongoing trials suggest performance parity in flooring and electrical potting, but cost parity requires larger Asian capacities or European on-purpose plants. Until then, most producers hedge by blending bio-content with conventional feedstocks to balance mechanical performance and pricing.

List of Companies Covered in this Report:

- 3M

- Aditya Birla Chemicals

- Arkema

- BASF

- Bitrez Ltd

- Covestro AG

- DIC Corporation

- DuPont

- Huntsman International LLC

- Leuna-Harze GmbH

- Olin Corporation

- POLYNT-REICHHOLD GROUP

- Sika AG

- Sir Industriale

- Solvay

- Spolchemie

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in wind-energy blade demand

- 4.2.2 Lightweight automotive composites push

- 4.2.3 Expansion of Electronics and Electricals manufacturing

- 4.2.4 Rebound in protective construction coatings

- 4.2.5 EU "Renovation Wave" subsidies for epoxy floors

- 4.3 Market Restraints

- 4.3.1 BPA and ECH regulatory scrutiny

- 4.3.2 Crude-linked raw-material price volatility

- 4.3.3 Bio-based resin substitution threat

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Raw Material

- 5.1.1 DGBEA (Bisphenol A and ECH)

- 5.1.2 DGBEF (Bisphenol F and ECH)

- 5.1.3 Novolac (Formaldehyde and Phenols)

- 5.1.4 Aliphatic (Aliphatic Alcohols)

- 5.1.5 Glycidylamine (Aromatic Amines and ECH)

- 5.1.6 Other Raw Materials

- 5.2 By Application

- 5.2.1 Paints and Coatings

- 5.2.2 Adhesives and Sealants

- 5.2.3 Composites

- 5.2.4 Electrical and Electronics

- 5.2.5 Wind Turbines

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 NORDIC Countries

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Aditya Birla Chemicals

- 6.4.3 Arkema

- 6.4.4 BASF

- 6.4.5 Bitrez Ltd

- 6.4.6 Covestro AG

- 6.4.7 DIC Corporation

- 6.4.8 DuPont

- 6.4.9 Huntsman International LLC

- 6.4.10 Leuna-Harze GmbH

- 6.4.11 Olin Corporation

- 6.4.12 POLYNT-REICHHOLD GROUP

- 6.4.13 Sika AG

- 6.4.14 Sir Industriale

- 6.4.15 Solvay

- 6.4.16 Spolchemie

- 6.4.17 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment