|

시장보고서

상품코드

2066439

무인항공기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Unmanned Aerial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

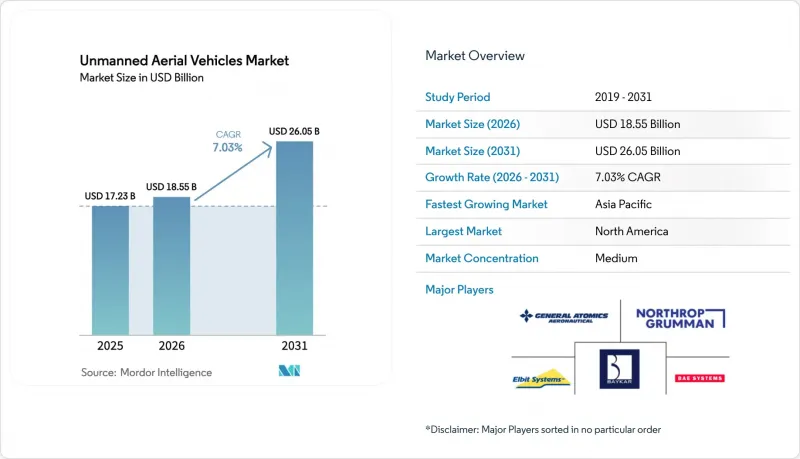

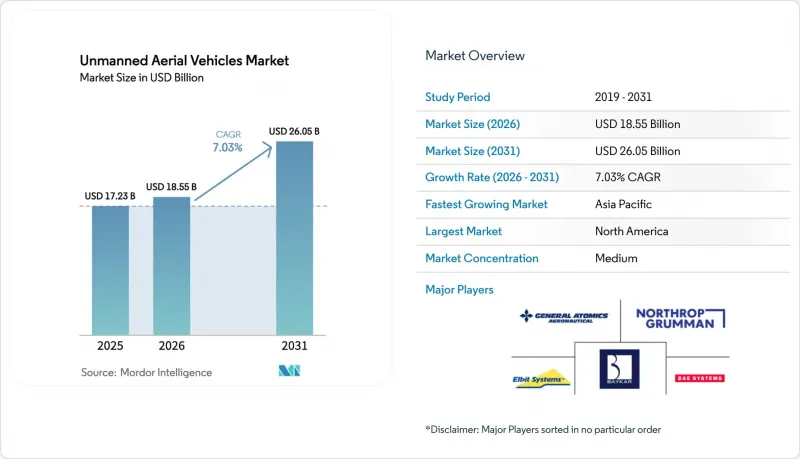

Mordor Intelligence에 의하면, 무인항공기(UAV) 시장은 2025년 172억 3,000만 달러로 평가되었고, 2026년에는 185억 5,000만 달러로 추정되고, 2026-2031년 CAGR 7.03%로 성장을 지속할 전망이며, 2031년에는 260억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 UAV 등급별(등급 I(150kg 미만), 등급 II(150-600kg), 등급 III(600kg 초과)), 플랫폼 유형별(고정익, 회전익, 하이브리드), 운용 모드별(원격 조종, 선택적 조종, 완전 자율), 용도별(전투, ISR, 배송, 로터링 탄약), 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 무인항공기(UAV) 시장 동향 및 인사이트

국방 예산 증액이 무인항공기(UAV) 편대의 확대를 뒷받침하고 있습니다.

전장에서의 실전 검증을 통해, 저렴한 드론으로도 기존에는 유인 자산으로만 달성할 수 있었던 성과를 거둘 수 있음이 밝혀짐에 따라, 각국의 국방부는 무인 항공기 조달을 확대되고 있습니다. 인도는 히말라야 지역의 감시 체제를 유지하기 위해 2027년까지 국산 플랫폼에 35억 달러의 예산을 승인했습니다. 이러한 예산 배분은 탁월한 생존성에서 수량 중시로 전환된 점을 여실히 보여주고 있으며, 저비용 드론이 장갑차를 대규모로 무력화시킨 우크라이나의 사례를 반영하고 있습니다. 다중 도메인 작전에서는 지속적인 정찰과 신속한 공격 주기가 요구되기 때문에 다른 예산 항목이 삭감되는 상황에서도 각국 의회는 무인항공기(UAV) 관련 지출을 계속해서 보호하고 있습니다. 그 결과, 안정적인 수주 기반이 구축되어 공급업체의 수익이 안정화되었을 뿐만 아니라, 차세대 시스템을 위한 연구 개발의 위험도 경감되고 있습니다.

실시간 및 전천후형 ISR에 대한 작전상 수요

지휘관들은 킬 체인을 몇 시간에서 몇 분으로 단축할 수 있는 24시간 감시 체제를 요구하고 있습니다. 미 공군의 MQ-9 리퍼 기단은 2024년 말까지 비행 시간이 300만 시간을 돌파했으며, 그 중 70%는 실전 임무가 아닌 ISR 출격에서 기록되었습니다. 이스라엘의 ‘헤르메스 900’ 운용은 주야를 가리지 않는 지속적인 감시 능력을 입증했으며, 기상 조건에 관계없이 센서에서 정보를 확보하는 것을 전제로 하는 현재의 작전 교리의 기반이 되고 있습니다. 합성 개구 레이더와 전기광학 페이로드는 구름을 뚫고 촬영한 영상을 제공하여, 적의 은폐 능력을 제한합니다. 동등한 수준의 경쟁 상대가 전력을 분산시키고 위장 전술을 구사하는 가운데, 실시간 영상 전송의 가치는 더욱 높아지고 있으며, 이에 따라 다중 센서를 탑재한 기체의 조달이 진행되고, 구형 기체의 탑재량 업그레이드가 촉진되고 있습니다.

엄격한 수출 관리 및 안보 관련 규제

미사일 기술 통제 체제(MTCR)는 사거리 300km를 초과하고 탑재 중량이 500kg을 넘는 시스템을 금지하고 있으며, 이로 인해 수요가 세분화되면서 일부 정부는 자국 공급업체로 눈을 돌리고 있습니다. 미국 연방조달규정(FAR) 40.2는 중국산 부품의 사용을 더욱 제한하고 있어, 시스템 통합사업자의 재설계 비용 부담이 증가하고 있습니다. 이스라엘의 사례별 라이선스 부여 방식은 해외로의 대규모 판매를 지연시키고 있으며, 정치적 제약이 적은 튀르키예공급업체들에게 호기를 제공합니다. 이러한 규제들이 복합적으로 작용하면서, 서유럽의 주요 제조업체들이 진출할 수 있는 무인 항공기 시장은 축소되고 판매 주기가 장기화됨에 따라, 자본은 신흥 경제국의 국내 프로그램으로 흘러들고 있습니다.

부문별 분석

중량 150kg 미만의 클래스 I 플랫폼은 2025년 매출의 44%를 차지했으며, 현재 대대 단위에서의 유기적 ISR(정보·감시·정찰)이 수요의 대부분을 차지하고 있음이 드러났습니다. 이 경량 기체들은 10만 미달러 미만이며, 시판 부품을 사용하고 활주로 없이도 이륙할 수 있기 때문에 예산이 제한된 군라도 수백 대를 배치할 수 있습니다. 금액 기준으로 볼 때, 클래스 I이 무인 항공기 시장에서 가장 큰 점유율을 차지하고 있지만, 많은 육군에서 초기 도입을 완료함에 따라 성장세는 둔화되고 있습니다. 중량이 150kg에서 600kg인 클래스 II 플랫폼은 연평균 성장률(CAGR) 7.55%로 시장 확대를 주도할 것으로 예상되며, 주머니에 들어갈 만한 크기의 쿼드콥터와 전략적 HALE(고고도 장거리) 시스템 사이의 공백을 메우는 역할을 할 것입니다. 이 부문은 12시간의 항속 시간과 멀티 센서 탑재라는 장점을 갖추고 있을 뿐만 아니라, C-130급 수송기에도 탑재가 가능하며, 이러한 기동성의 우위는 원정 부대의 요구 사항에 부합합니다. 중량이 600kg을 초과하는 클래스 III 플랫폼은 장거리 ISR(정보·감시·정찰) 및 공격 임무에서 전략적 중요성을 유지하고 있지만, 3,000만 달러를 넘는 단가가 광범위한 도입을 가로막고 있습니다.

우크라이나 측의 신속한 작전 피드백을 통해, 대형 드론만큼의 후방 지원 부담을 수반하지 않으면서 정밀 공격을 수행한 ‘바이락탈 TB2’의 클래스 II에서의 영향력이 입증되었습니다. 제너럴 아토믹스사의 ‘모하비’ STOL(단거리 이착륙)형은 이 부문을 목표로 하고 있으며, 일반 도로에서의 운용 및 기존 ‘리퍼’와의 탑재량 공통화를 약속하고 있습니다. 한편, 로터링 탄약은 클래스 I 조달이 활발히 이루어지고 있으며, ‘스위치블레이드 600’과 ‘할롭’의 각 변형 모델이 최경량급에 대장갑 능력을 더하고 있습니다. 결국, 무인항공기(UAV) 시장은 대량 발주되는 클래스 I과 가성비가 뛰어난 클래스 II 계약 간의 균형을 유지하고 있으며, 클래스 III 프로그램의 경우 고가라는 점으로 인한 충격을 완화하기 위해 서비스 계약을 함께 제공하는 사례가 늘고 있습니다.

2025년 매출액 중 고정익 항공기가 74.78%를 차지했으며, 이는 타의 추종을 불허하는 항속 시간과 적재량 대 중량 비율을 반영한 것입니다. 전략적 ISR(정보·감시·정찰)의 경우, 20시간의 체공 시간과 1,500km의 항속 거리가 활주로나 착함 장치에 대한 투자를 정당화하는 요인이 되고 있습니다. 회전익 드론은 호버링이 필수적인 도시 지역이나 산악 지대에서 특별한 역할을 수행하지만, 그 비행 시간은 보통 4시간에 그칩니다. 수직 이륙 후 날개를 이용한 순항 단계로 전환되는 하이브리드 VTOL 모델 시장은 연평균 성장률(CAGR) 9.25%로 확대될 것으로 예상되며, 이는 모든 플랫폼 유형 중 가장 빠른 성장률입니다. 해군이 이러한 기체를 중시하는 이유는 대부분의 함정 갑판에 캐터펄트가 설치되어 있지 않기 때문입니다. 벨사의 틸트로터기 ‘V-247 비질란트’는 2016년에 갑판 시험을 완료하며 이 개념의 실현 가능성을 입증했습니다.

하이브리드 플랫폼은 현재 무인항공기(UAV) 시장에서 신규 건조 지출에서 차지하는 비중을 확대하고 있으며, 배터리 밀도 향상과 경량 복합재 로터의 이점을 누리고 있습니다. 노스롭 그루먼사의 중단된 ‘Tern’ 프로젝트는 그럼에도 불구하고 테일 시팅의 공기역학적 특성을 입증했으며, 몇몇 신생 기업들이 그 인사이트를 소형 보급기에 응용하고 있습니다. 고정익 항공기 제조업체들은 캐터펄트가 필요 없는 탈부착식 부스터 포드와 자동 착륙 알고리즘을 통해 이에 대응하고 있어, 기종 간의 경계가 점차 모호해지고 있습니다. 회전익기 제조업체들은 근접 정찰용으로 센서 마스트를 통합하고, 거의 소음이 없는 전동 로터 개발에 주력하고 있습니다. 고정익기 모델이 여전히 수익의 주축을 이루고 있는 반면, 하이브리드 VTOL 모델의 성장은 유연한 배치와 해상 작전으로의 장기적인 전환을 시사하고 있습니다.

지역별 분석

북미는 2025년 매출의 40.12%를 차지했으며, 이는 미국의 무인 시스템에 대한 연간 지출이 120억 달러를 초과함에 따라 뒷받침되고 있습니다. '협동 전투기(CCA)' 등의 프로그램은 금세기 내에 1,000대의 자율형 호위기 도입을 목표로 하고 있으며, 국내 주요 제조업체들에게 안정적인 수주 잔고를 확보해 주고 있습니다. 캐나다가 북극권 감시를 위해 ‘스카이 가디언’ 드론을 발주한 것은 주권 유지 임무의 다각화를 보여주는 반면, 멕시코의 ‘헤르메스 900’ 기단은 마약 카르텔 단속에 대응하고 있어, 동등한 적과의 전쟁이라는 가정을 넘어선 지역적 수요를 확대시키고 있습니다. 강력한 벤처 자금 조달 덕분에 지적 재산권과 관련된 장벽은 여전히 낮아, 수십 개의 소프트웨어 스타트업이 공급망에 진입할 수 있게 되었습니다.

아시아태평양은 연평균 성장률(CAGR) 8.29%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 중국은 ‘윙 룬’과 ‘CH’ 시리즈 드론을 양산하여, MTCR의 제약을 받지 않는 중동의 구매자들에게 수출하고 있습니다. 인도의 ‘CATS Warrior’ 프로젝트는 2028년까지 200대를 도입하는 것을 목표로 하고 있으며, 이를 통해 이스라엘산 장비 수입에 대한 의존도를 낮출 수 있게 될 것입니다. 호주의 MQ-4C 트리톤 도입은 광대한 배타적 경제수역(EEZ) 전역에 걸친 해양 상황 인식을 강화하는 것이며, 일본의 시 가디언 도입 역시 동중국해에서 이와 유사한 우선 과제를 시사하고 있습니다. 대만과 남중국해를 둘러싼 지역적 긴장이 조달을 촉진하는 한편, 한국과 인도네시아의 주요 기업들은 인접한 동남아시아 시장 확보를 놓고 경쟁을 벌이고 있습니다.

유럽, 중동 및 아프리카가 나머지 시장 기회를 형성하고 있습니다. 유럽의 NATO 회원국들은 2022년 러시아의 우크라이나 침공을 계기로 구매를 가속화했습니다. 독일은 MQ-4C ‘트리톤’을 발주했고, 프랑스는 ‘리퍼’의 운용 기간을 연장했습니다. 튀르키예는 수출 규제를 완화하고 TB2 및 아크운지 드론을 판매함으로써 현 상황을 타개하고, 중앙아시아와 북아프리카에 발판을 마련했습니다. 중동에서는 이스라엘, 아랍에미리트, 사우디아라비아가 멀티센서 페이로드를 활용해 항공기 편대의 업그레이드를 추진하고 있지만, 예산과 유가 변동이 여전히 그 시기에 영향을 미치고 있습니다. 아프리카는 아직 발전의 초기 단계에 있습니다. 남아프리카의 파라마운트 그룹과 케냐의 초기 단계에 있는 프로그램은 회복의 조짐을 보이고 있지만, 인프라와 자금 부족이 확산을 저해하고 있습니다. 남미는 재정적 제약으로 인해 뒤처져 있지만, 브라질의 엠브라에르(Embraer)사가 제작한 RQ-900은 국경 감시가 전략적 필수 과제가 될 경우, 국내 산업이 부상할 수 있음을 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the unmanned aerial vehicles market is expected to grow from USD 17.23 billion in 2025 to USD 18.55 billion in 2026, and is forecasted to reach USD 26.05 billion by 2031 at a 7.03% CAGR over 2026-2031.

This report is Segmented by UAV Class (Class I (Below 150 Kg), Class II (150-600 Kg), Class III (Above 600 Kg)), Platform Type (Fixed-Wing, Rotary-Wing, Hybrid), Mode of Operation (Remotely Piloted, Optionally Piloted, Fully Autonomous), Application (Combat, ISR, Delivery, Loitering Munition), and Geography (North America, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Unmanned Aerial Vehicles Market Trends and Insights

Rising Defense Budgets Fueling UAV Fleet Expansion

Defense ministries have increased the procurement of unmanned aerial vehicles after battlefield evidence demonstrated that inexpensive drones can deliver results previously achievable only with manned assets. India approved USD 3.5 billion for indigenous platforms through 2027 to sustain Himalayan surveillance. These allocations underscore a shift from exquisite survivability to quantity, mirroring Ukraine's experience, where low-cost drones neutralized armor at scale. As multi-domain operations demand persistent sensing and rapid strike cycles, legislatures continue to ring-fence UAV spending even where other line items decline. The outcome is a steady baseline of orders that stabilizes supplier revenue and de-risks R&D for next-generation systems.

Operational Demand for Real-Time, All-Weather ISR

Commanders seek 24-hour coverage that compresses kill chains from hours to minutes. The US Air Force's MQ-9 Reaper fleet exceeded 3 million flight hours by late 2024, with 70% logged in ISR sorties rather than kinetic missions. Israeli Hermes 900 operations demonstrated actual day-night persistence, informing doctrine that now expects sensor feeds regardless of weather. Synthetic-aperture radar and electro-optical payloads deliver cloud-penetrating imaging, limiting adversaries' ability to mask movements. As peer competitors disperse assets and employ camouflage, real-time feeds become more valuable, reinforcing procurement of multi-sensor airframes and driving payload upgrades to legacy fleets.

Stringent Export-Control and Security-Prohibition Regimes

The Missile Technology Control Regime (MTCR) bars systems with a range beyond 300 km and a payload over 500 kg, fragmenting demand and steering some governments toward indigenous suppliers. US FAR 40.2 further restricts the use of components of Chinese origin, adding redesign costs for integrators. Case-by-case licensing in Israel delays large foreign sales, creating an opportunity for Turkish vendors that face fewer political constraints. Cumulatively, these rules shrink the accessible unmanned aerial vehicles market for Western primes and elongate sales cycles, diverting capital toward domestic programs in emerging economies.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Advances in Onboard Autonomy and AI-Driven Mission Systems

- Manned-Unmanned Teaming Concepts Entering Procurement Cycles

- High Acquisition and Life-Cycle Cost of HALE/MALE Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class I platforms, which weigh under 150 kg, accounted for 44% of 2025 revenue, underscoring that organic ISR at the battalion level currently dominates demand. These lightweight airframes cost under USD 100,000, utilize commercial parts, and launch without runways, allowing budget-constrained forces to field hundreds of units. In dollar terms, Class I accounted for the largest share of the unmanned aerial vehicles market; however, growth moderates as many armies complete their initial rollouts. Class II platforms, weighing between 150 kg and 600 kg, are forecast to lead the expansion at a 7.55% CAGR, bridging the gap between pocket-sized quadcopters and strategic HALE systems. The segment benefits from 12-hour endurance and multi-sensor payloads yet still fits on C-130-class transports, a mobility advantage that resonates with expeditionary forces. Class III platforms weighing more than 600 kg maintain strategic relevance for long-range ISR and strike, but unit costs exceeding USD 30 million discourage widespread adoption.

Rapid operational feedback from Ukraine validated the Class II impact of the Bayraktar TB2, which delivered precision strikes without the logistics footprint of larger drones. General Atomics' Mojave STOL variant targets this category, promising highway operations and payload commonality with legacy Reapers. Meanwhile, loitering munitions keep Class I procurement lively, as Switchblade 600 and Harop variants add anti-armor punch to the lowest weight class. Ultimately, the UAV market balances high-volume Class I orders with value-dense Class II contracts, while Class III programs increasingly bundle service contracts to ease sticker shock.

Fixed-wing airframes accounted for 74.78% of 2025 revenue, reflecting their unmatched endurance and payload-to-weight ratios. For strategic ISR, 20-hour loiter times and 1,500 km range justify investments in runways and arresting gear. Rotary-wing drones serve specialized roles in urban or mountainous terrain, where hovering is essential, but their endurance typically lasts only four hours. Hybrid VTOL models that take off vertically then transition to wing-borne cruise are forecast to expand at a 9.25% CAGR, the fastest clip across the platform-type continuum. Navies prize such airframes because most ship decks lack catapults; Bell's V-247 Vigilant tilt-rotor completed deck trials in 2016, proving the concept viable.

Hybrid platforms now capture new-build spending in the UAV market, benefiting from improved battery density and lightweight composite rotors. Northrop Grumman's canceled Tern project nevertheless validated tail-sitting aerodynamics, and several startups apply those lessons to smaller resupply craft. Fixed-wing manufacturers respond with detachable booster pods and autoland algorithms to avoid catapults, blurring the lines between categories. Rotary-wing suppliers focus on sensor-mast integration and near-silent electric rotors for close-quarters reconnaissance. While fixed-wing models remain the revenue anchor, the growth of hybrid VTOL models signals a long-term pivot toward flexible basing and maritime operations.

Geography Analysis

North America generated 40.12% of 2025 revenue, sustained by US outlays exceeding USD 12 billion annually for unmanned systems. Programs such as the Collaborative Combat Aircraft aim to achieve 1,000 autonomous escorts by this decade, ensuring a steady backlog for domestic primes. Canada's Arctic-domain surveillance orders for SkyGuardian drones illustrate diversification into sovereignty missions, while Mexico's Hermes 900 fleet addresses cartel interdiction, broadening regional demand beyond peer-war contingencies. Intellectual-property barriers remain low due to strong venture financing, enabling dozens of software startups to enter the supply chain.

The Asia-Pacific region is the fastest-growing theater, with an 8.29% CAGR. China mass-produces Wing Loong and CH-series drones and exports them to Middle Eastern buyers unconstrained by MTCR. India's CATS Warrior project aims to procure 200 units by 2028, thereby reducing its reliance on Israeli imports. Australia's MQ-4C Triton deals strengthen maritime domain awareness across vast Exclusive Economic Zones, and Japan's SeaGuardian acquisition signals similar priorities in the East China Sea. Regional tensions over Taiwan and the South China Sea catalyze procurement, while domestic champions in South Korea and Indonesia vie to capture adjacent Southeast Asian markets.

Europe, the Middle East, and Africa form the remaining opportunity set. European NATO members accelerated purchases after Russia's 2022 invasion of Ukraine; Germany ordered MQ-4C Tritons and France lengthened Reaper operations. Turkey disrupted the status quo by selling TB2 and Akinci drones under fewer export constraints, gaining footholds in Central Asia and North Africa. In the Middle East, Israel, the UAE, and Saudi Arabia are upgrading their fleets with multi-sensor payloads, although budgetary and oil-price fluctuations still influence the timing. Africa remains nascent; South Africa's Paramount Group and Kenya's embryonic programs indicate green shoots, but infrastructure and funding gaps temper uptake. South America lags due to fiscal constraints, yet Brazil's Embraer RQ-900 demonstrates that an indigenous industry can emerge when border surveillance is a strategic imperative.

List of Companies Covered in this Report:

- AeroVironment

- Airbus SE

- BAE Systems plc

- BAYKAR A.S.

- The Boeing Company

- Elbit Systems Ltd.

- General Atomics

- Israel Aerospace Industries Ltd.

- Kratos Defense & Security Solutions, Inc.

- Leonardo S.p.A

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Saab AB

- Textron Systems Corporation

- Turkish Aerospace Industries (TAI)

- QinetiQ Group

- Hindustan Aeronautics Limited

- Korean Aerospace Industries (KAI)

- Griffon Aerospace, Inc.

- Teledyne Technologies Incorporated

- Griffon Aerospace, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising defense budgets fueling UAV fleet expansion

- 4.2.2 Operational demand for real-time, all-weather ISR

- 4.2.3 Rapid advances in onboard autonomy and AI-driven mission systems

- 4.2.4 Manned-unmanned teaming ("loyal wingman") concepts entering procurement cycles

- 4.2.5 Attritable-drone doctrine lowering cost threshold for mass deployment

- 4.2.6 Satellite-mesh networking enabling resilient BVLOS comms in GPS-contested theaters

- 4.3 Market Restraints

- 4.3.1 Stringent export-control and security-prohibition regimes (e.g., MTCR, FAR 40.2)

- 4.3.2 High acquisition and life-cycle cost of HALE/MALE platforms

- 4.3.3 Escalating electronic-warfare/counter-UAS threat environment

- 4.3.4 Supply-chain security restrictions driving component scarcity and cost inflation

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By UAV Class

- 5.1.1 Class I (Below 150 kg)

- 5.1.2 Class II (150-600 kg)

- 5.1.3 Class III (Above 600 kg)

- 5.2 By Platform Type

- 5.2.1 Fixed-wing

- 5.2.2 Rotary-wing

- 5.2.3 Hybrid

- 5.3 By Mode of Operation

- 5.3.1 Remotely Piloted

- 5.3.2 Optionally Piloted

- 5.3.3 Fully Autonomous

- 5.4 By Application

- 5.4.1 Combat

- 5.4.2 Intelligence, Surveillance & Reconnaissance (ISR)

- 5.4.3 Delivery

- 5.4.4 Loitering Munition

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 France

- 5.5.3.3 Germany

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AeroVironment

- 6.4.2 Airbus SE

- 6.4.3 BAE Systems plc

- 6.4.4 BAYKAR A.S.

- 6.4.5 The Boeing Company

- 6.4.6 Elbit Systems Ltd.

- 6.4.7 General Atomics

- 6.4.8 Israel Aerospace Industries Ltd.

- 6.4.9 Kratos Defense & Security Solutions, Inc.

- 6.4.10 Leonardo S.p.A

- 6.4.11 Lockheed Martin Corporation

- 6.4.12 Northrop Grumman Corporation

- 6.4.13 Saab AB

- 6.4.14 Textron Systems Corporation

- 6.4.15 Turkish Aerospace Industries (TAI)

- 6.4.16 QinetiQ Group

- 6.4.17 Hindustan Aeronautics Limited

- 6.4.18 Korean Aerospace Industries (KAI)

- 6.4.19 Griffon Aerospace, Inc.

- 6.4.20 Teledyne Technologies Incorporated

- 6.4.21 Griffon Aerospace, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment