|

시장보고서

상품코드

2066464

지열 에너지 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Geothermal Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

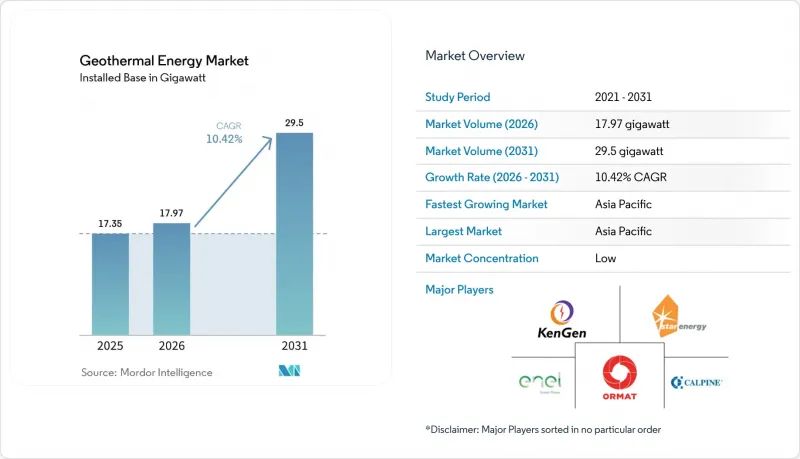

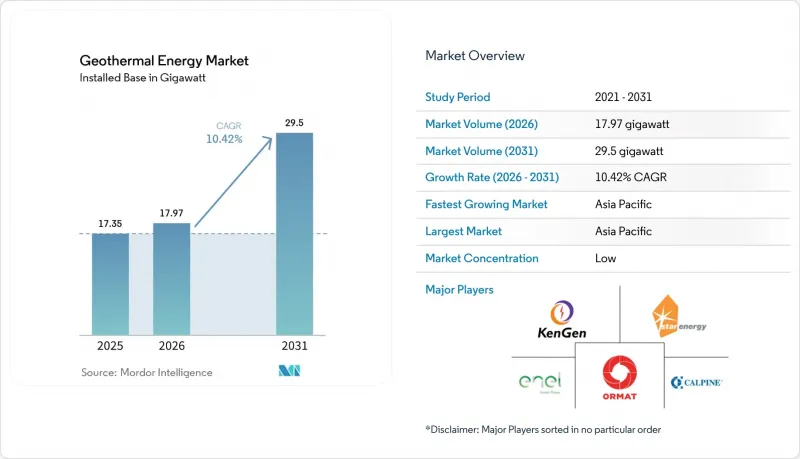

Mordor Intelligence에 의하면, 지열 에너지 시장 규모(설치용량 기반)는 2025년 17.35기가와트로 평가되었습니다. 2026년 17.97기가와트에서 2031년까지 29.5기가와트로 확대될 것으로 예측되며, 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.42%를 나타낼 전망입니다.

본 보고서는 플랜트 유형(건식 증기 플랜트, 플래시 증기 플랜트, 바이너리 사이클 플랜트, 복합 사이클/하이브리드 플랜트 및 강화 지열 시스템), 용도(발전, 지역 냉난방, 산업용 열 이용), 그리고 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다.

세계의 지열 에너지 시장 동향 및 인사이트

기초 부하 재생에너지에 대한 정부의 인센티브 및 고정가격임베디드제도(FIT)의 확대

고정가격 임베디드 제도(FIT)와 용량 지급 제도는 탐사 위험을 상쇄할 수 있는 수익원을 확보함으로써 프로젝트의 경제성을 재구축하고 있습니다. 인도네시아는 2025년에 지열 전력 임베디드 가격을 1kWh당 1,450루피아로 인상했으며, 이 12%의 프리미엄 덕분에 수마트라섬과 술라웨시섬에서의 시추 및 현장 작업이 가속화되었습니다. 튀르키예는 임베디드 가격 보장을 2030년까지 연장했으며, 이에 따라 총 320MW 규모의 신규 바이너리 사이클 발전소 8곳의 건설이 촉진되었습니다. 케냐는 우물 손실의 최대 70%를 보상하는 국가 보증 시추 보험을 도입하여, 민간 자금 조달의 가장 큰 장벽을 직접 해결했습니다. 유럽연합(EU)은 지열 발전 허가 취득 기간을 18개월 미만으로 단축함으로써, 프로젝트의 리드타임과 은행 대출 승인 가능성을 높였습니다. 이러한 움직임으로 인해, 태양광 및 풍력 발전 제한률이 이미 15%를 넘어선 시장에서 투기성 광구가 투자 가능한 자산으로 전환되고 있습니다.

지열 히트펌프 도입 확대

지열 히트펌프의 설치는 발전과는 별개로 병행적인 수요 경로를 창출하고 있습니다. 미국에서는 30%의 연방 세금 공제 덕분에 2025년 추운 지역의 주에서 주택용 시스템 도입이 전년 대비 41% 증가했습니다. 독일에서는 ‘건축물 에너지법’에 따라 가스 보일러가 단계적으로 폐지되는 가운데, 8만 7,000건의 신규 허가가 발급되었습니다. 스웨덴에서는 지역 난방 시설에 대규모 히트펌프를 도입하여 개보수를 실시함으로써, 운영 비용을 35% 절감하는 동시에 계절별 성능 계수를 개선했습니다. 일본은 2028년까지 건축물에서의 화석 연료 사용량을 20% 감축하는 것을 목표로, 상업시설 개보수를 위해 180억 엔의 보조금을 편성했습니다. 시추 깊이가 얕은 경우 심부 지층의 불확실성을 피할 수 있기 때문에 도급업체들은 이 분야를 수익률은 높고 위험은 낮은 것으로 보고 있습니다.

초기 단계의 높은 시추 위험과 설비 투자

미개척 분지에서 탐사정의 성공률은 55%-65%에 그치며, 빈 우물이 될 경우 비용이 최대 800만 달러에 달하기 때문에 자금 조달이 어렵습니다. 시추 비용은 총 설비 투자액의 40%-50%를 차지하며, 투수성이 낮은 경우 단 한 개의 시추 실패만으로도 20MW 규모의 프로젝트가 좌초될 가능성이 있습니다. 케냐의 메넨가이 유전에서는 성공률이 고작 38%에 그쳐, 4,700만 달러의 감손 처리와 18개월의 지연을 초래했습니다. 인도네시아의 살라 프로젝트는 예상치 못한 저류층 구획화로 인해 예산을 23% 초과하여 종료되었습니다. 위험 완화 기금이 손실의 일부를 보전해 주지만, 개발업체들은 여전히 저류층 성능에 대한 불확실성에 노출되어 있어, 지질 데이터가 확인된 개보수 공사에 자본을 투입하고 있습니다.

부문별 분석

2025년에는 플래시 증기 발전소가 발전 용량의 47.50%를 차지했습니다. 이는 인도네시아와 필리핀의 고엔탈피 지역에서 다년간 쌓아온 실적을 반영한 것입니다. 이 부문은 확립된 공급망과 검증된 저류층 관리 기법의 혜택을 받고 있어, 시추 위험은 중간 수준으로 억제되고 있습니다. 그러나 셰일 자극 기술을 통해 기존에는 경제성이 없었던 고온 건조 암층에 저류층이 형성됨에 따라, 강화형 지열 시스템(EGS) 세계 시장 규모는 2031년까지 연평균 성장률(CAGR) 18.80%로 확대될 것으로 예측됩니다. 네바다주와 유타주에서 진행된 시범 사업의 성공을 통해 1MW당 약 420만 달러라는 비용 기준이 입증되었으며, 이는 저온 지열전에서 운영되는 바이너리 발전소와 동등한 수준입니다. '더 가이저스'와 같은 기존 방식의 사이트에서는 여전히 건식 증기 방식이 채택되고 있지만, 증기가 주성분인 지열전의 고갈에 따라 그 이용은 점차 줄어들고 있습니다. 바이너리 사이클 기술은 유럽의 저엔탈피 시장에서 계속해서 활용되고 있으며, 유기 랭킨 터빈을 통해 물 사용량을 85% 줄임으로써 전 세계 지열 에너지 산업의 기반을 강화하고 있습니다.

EGS(강화 지열 시스템)의 성장세는 공급망의 역학을 변화시키고 있습니다. 수평 시추에 대한 전문 지식을 갖춘 서비스 기업들이 시장에 진출함에 따라, 케이싱, 프로판트 및 자극 작업 팀을 둘러싼 경쟁이 치열해지고 있습니다. 장비 공급업체들은 건설 기간을 단축하는 모듈식 지상 플랜트를 통해 이에 대응하고 있습니다. 격리 수준이 높은 지역에서는 태양열 집열기와 지열 우물을 같은 장소에 배치하는 복합 사이클 하이브리드 시스템이 등장하고 있으며, 새로운 터빈을 설치하지 않고도 낮 시간대의 발전량을 늘려 전 세계 지열 에너지 시장을 통합형 재생에너지 허브로 이끌고 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 지열 에너지 시장 점유율의 44.27%를 차지했으며, 인도네시아의 3.3 GW 신규 발전 용량 가동 계획과 필리핀의 허가 절차 간소화에 힘입어 2031년까지 연평균 성장률(CAGR) 11.9%로 성장할 것으로 전망됩니다. 인도네시아의 페르타미나 지열 에너지는 2025년, 수마트라 섬의 3개 유전에서 총 165 MW를 증설했으며, 스타 에너지는 살락에서 110 MW 규모의 확장 공사를 완료하여 저류층의 수명을 18년 연장했습니다. 일본에서는 온천 리조트 주변의 시추 제한이 철폐되어 420 km²에 걸쳐 탐사가 가능해졌습니다. 이에 따라 미쓰비시 파워는 2027년 가동을 목표로 벳푸에 30MW 규모의 발전소를 건설할 계획을 제안했습니다. 중국은 계속해서 직접 이용 방식의 난방에 주력하고 있으며, 현재 화북 평원의 얕은 대수층에서 공급되는 주택용 열은 석탄 보일러 비용의 3분의 1 수준에 이용되고 있습니다.

북미에서는 미국 토지관리국이 2025년에 7만 8,000에이커에 달하는 47건의 임대 계약을 체결하고, 2008년 이후 최고치인 1억 4,200만 달러의 보너스 입찰금을 모음으로써 부활의 조짐을 보이고 있습니다. 오마트 테크놀로지스는 과거 수익성이 낮다고 여겨졌던 155°C의 유체를 이용하는 바이너리 사이클을 통해 스팀보트 콤플렉스를 18MW 규모로 확장했습니다. 캐나다의 5,000만 캐나다 달러 규모의 탐사 기금은 고갈된 가스정의 개량을 목표로 하고 있지만, 멕시코 연방전력위원회(CFE)는 963 MW를 유지하고 있음에도 불구하고 2015년 예산 삭감 이후 신규 프로젝트가 부족한 실정입니다.

유럽, 중동 및 아프리카에서는 대조적인 추세가 나타나고 있습니다. 튀르키예는 10년간의 요금 보장 조건 하에 2025년에 95 MW 규모의 바이너리 사이클 발전 설비를 추가하여, 총 발전 용량이 1.7 GW에 달했습니다. 아이슬란드의 설비 용량은 755 MW로 안정적이며, 개발 사업자는 현재 지열 전기분해를 통해 생산된 재생 가능 수소를 수출하고 있습니다. 케냐는 오르카리아 V에서 35 MW급 발전기 2기를 완공하여 설비 용량을 985 MW로 확대했습니다. 또한, 2027년까지 오르카리아 I에서 140 MW 규모의 증설이 계획되어 있습니다. 에티오피아의 투루 모예 프로젝트는 2029년까지 520 MW를 달성하기 위해 8억 달러의 자금을 확보했습니다. 한편, 칠레에서는 안데스 산맥의 송전 비용이 높기 때문에 현재 가동 중인 발전소는 48 MW 규모의 세로 파벨리온 단 한 곳뿐입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the geothermal energy market size in terms of installed base is projected to expand from 17.35 gigawatt in 2025 and 17.97 gigawatt in 2026 to 29.5 gigawatt by 2031, registering a CAGR of 10.42% between 2026 to 2031.

This report is Segmented by Plant Type (Dry Steam Plants, Flash Steam Plants, Binary Cycle Plants, Combined Cycle/Hybrid Plants, and Enhanced Geothermal Systems), Application (Electricity Generation, District Heating and Cooling, and Industrial Process Heat), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Global Geothermal Energy Market Trends and Insights

Rising Government Incentives & FiTs for Baseload Renewables

Feed-in tariffs and capacity payments are reshaping project economics by locking in revenue streams that neutralize exploration risk. Indonesia lifted its geothermal tariff to IDR 1,450 per kWh in 2025, a 12% premium that accelerated well-field work in Sumatra and Sulawesi. Turkey extended its tariff guarantee to 2030, triggering eight new binary-cycle plants totaling 320 MW. Kenya introduced sovereign drilling insurance that now covers up to 70% of well losses, directly addressing the single largest barrier to private finance. The European Union shortened geothermal permitting to below 18 months, improving project lead times and bankability. These moves convert speculative acreage into investable assets in markets where solar and wind curtailment already exceeds 15%.

Growing Deployment of Geothermal Heat Pumps

Ground-source heat-pump installations are creating a parallel demand channel that is independent of electricity generation. A 30% U.S. federal tax credit drove a 41% year-on-year jump in residential systems during 2025 in cold-climate states. Germany issued 87,000 new permits as gas boilers are phased out under the Building Energy Act. Sweden retrofitted district-heating plants with large-scale pumps that cut operating costs by 35% and improved seasonal performance ratios. Japan earmarked JPY 18 billion in subsidies for commercial retrofits, pursuing a 20% fossil-fuel reduction in buildings by 2028. Contractors see this segment as high margin and low risk because shallow drilling avoids deep subsurface uncertainty.

High Upfront Drilling Risk & Capex

Exploration wells succeed only 55%-65% of the time in frontier basins, with dry-hole costs up to USD 8 million, making financing difficult. Drilling consumes 40%-50% of total capex, and one failed well can sink a 20 MW project if permeability is poor. Kenya's Menengai field saw only a 38% success rate, causing USD 47 million in write-offs and 18-month delays. Indonesia's Sarulla project ended 23% over budget due to unexpected reservoir compartmentalization. Risk-mitigation funds cover part of the loss, but developers remain exposed to reservoir performance uncertainty, steering capital toward retrofits with known subsurface data.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Energy-Security Needs for 24/7 Green Power

- Repurposing Idle Oil & Gas Wells for Closed-Loop Geothermal

- Cost-Competitive Pressure from Solar & Wind

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flash-steam plants represented 47.50% of capacity in 2025, reflecting their long track record in high-enthalpy zones across Indonesia and the Philippines. The segment benefits from established supply chains and proven reservoir management practices, keeping drilling risk moderate. However, the global geothermal energy market size for Enhanced Geothermal Systems is projected to expand at an 18.80% CAGR to 2031 as shale-style stimulation creates reservoirs in previously uneconomic hot-dry-rock formations. Pilot successes in Nevada and Utah validated cost benchmarks near USD 4.2 million per MW, on par with binary plants in lower-temperature fields. Dry-steam configurations persist at legacy sites like The Geysers but face a gradual decline as vapor-dominated fields deplete. Binary-cycle technology continues to serve low-enthalpy markets in Europe, where organic Rankine turbines cut water use by 85%, strengthening the global geothermal energy industry mix.

EGS momentum is altering supply-chain dynamics. Service companies with horizontal-drilling expertise are entering the market, increasing competition for casing, proppant, and stimulation crews. Equipment vendors respond with modular surface plants that shorten construction timelines. Combined-cycle hybrids that co-locate solar collectors with geothermal wells are emerging in regions with strong isolation, adding daytime output without new turbines and nudging the global geothermal energy market toward integrated renewable hubs.

Geography Analysis

Asia-Pacific held a 44.27% global geothermal energy market share in 2025 and is projected to grow at an 11.9% CAGR through 2031, supported by Indonesia's plan to commission 3.3 GW of new capacity and the Philippines' streamlined permitting framework. Indonesia's Pertamina Geothermal Energy added 165 MW across three Sumatra fields in 2025, and Star Energy completed a 110 MW expansion at Salak to prolong reservoir life by 18 years. Japan removed drilling limits near onsen resorts, opening 420 km2 for exploration and prompting Mitsubishi Power to propose a 30 MW plant in Beppu slated for 2027. China continues to focus on direct-use heating; shallow aquifers in the North China Plain now supply residential heat at one-third the cost of coal boilers.

North America is experiencing a resurgence as the U.S. Bureau of Land Management issued 47 leases covering 78 000 acres in 2025, attracting USD 142 million in bonus bids, the highest since 2008. Ormat Technologies expanded the Steamboat complex by 18 MW using binary cycles that tap 155 °C fluids formerly deemed sub-economic. Canada's CAD 50 million exploration fund targets retrofits in depleted gas wells, while Mexico's Comision Federal de Electricidad maintains 963 MW but lacks fresh projects after 2015 budget cuts.

Europe, the Middle East, and Africa reveal contrasting trajectories. Turkey reached 1.7 GW after adding 95 MW of binary-cycle capacity in 2025 under a 10-year tariff guarantee. Iceland's installed base is steady at 755 MW, with developers now exporting renewable hydrogen from geothermal electrolysis. Kenya lifted its capacity to 985 MW after completing two 35 MW units at Olkaria V, and a further 140 MW is planned at Olkaria I by 2027. Ethiopia's Tulu Moye project secured a USD 800 million package to target 520 MW by 2029, while Chile's only operating plant remains Cerro Pabellon at 48 MW amid high Andean transmission costs.

- Ormat Technologies Inc.

- Enel Green Power

- Calpine Corporation

- Toshiba Energy Systems & Solutions

- Mitsubishi Power Ltd.

- Fuji Electric Co. Ltd.

- Ansaldo Energia SpA

- Baker Hughes Company

- Turboden

- PT Pertamina Geothermal Energy

- Star Energy Geothermal

- KenGen (Kenya Electricity Generating Co.)

- ENGIE SA

- Aboitiz Power Corporation

- First Gen Corporation

- Sosian Energy Ltd.

- Tetra Tech Inc.

- Alterra Power Corp.

- Contact Energy

- Fervo Energy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising government incentives & FiTs for baseload renewables

- 4.2.2 Growing deployment of geothermal heat pumps

- 4.2.3 Heightened energy-security needs for 24/7 green power

- 4.2.4 Repurposing idle oil & gas wells for closed-loop geothermal

- 4.2.5 Emerging geothermal-to-hydrogen production hubs

- 4.3 Market Restraints

- 4.3.1 High upfront drilling risk & capex

- 4.3.2 Cost-competitive pressure from solar & wind

- 4.3.3 Global shortage of specialised geothermal drill crews

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Existing and Key Upcoming Projects

- 4.8 Investment & Financing Analysis

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitute Products & Services

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Plant Type

- 5.1.1 Dry Steam Plants

- 5.1.2 Flash Steam Plants

- 5.1.3 Binary Cycle Plants

- 5.1.4 Combined Cycle/Hybrid Plants

- 5.1.5 Enhanced Geothermal Systems (EGS)

- 5.2 By Application

- 5.2.1 Electricity Generation

- 5.2.2 District Heating and Cooling

- 5.2.3 Industrial Process Heat

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 NORDIC Countries

- 5.3.2.6 Turkey

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Indonesia

- 5.3.3.6 Philippines

- 5.3.3.7 Australia

- 5.3.3.8 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Kenya

- 5.3.5.4 Nigeria

- 5.3.5.5 South Africa

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Ormat Technologies Inc.

- 6.4.2 Enel Green Power

- 6.4.3 Calpine Corporation

- 6.4.4 Toshiba Energy Systems & Solutions

- 6.4.5 Mitsubishi Power Ltd.

- 6.4.6 Fuji Electric Co. Ltd.

- 6.4.7 Ansaldo Energia SpA

- 6.4.8 Baker Hughes Company

- 6.4.9 Turboden

- 6.4.10 PT Pertamina Geothermal Energy

- 6.4.11 Star Energy Geothermal

- 6.4.12 KenGen (Kenya Electricity Generating Co.)

- 6.4.13 ENGIE SA

- 6.4.14 Aboitiz Power Corporation

- 6.4.15 First Gen Corporation

- 6.4.16 Sosian Energy Ltd.

- 6.4.17 Tetra Tech Inc.

- 6.4.18 Alterra Power Corp.

- 6.4.19 Contact Energy

- 6.4.20 Fervo Energy

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment