|

시장보고서

상품코드

2066503

가구 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Furniture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

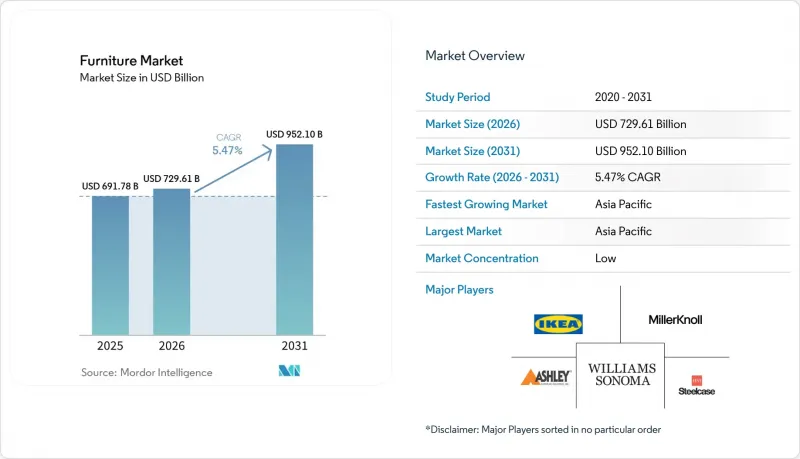

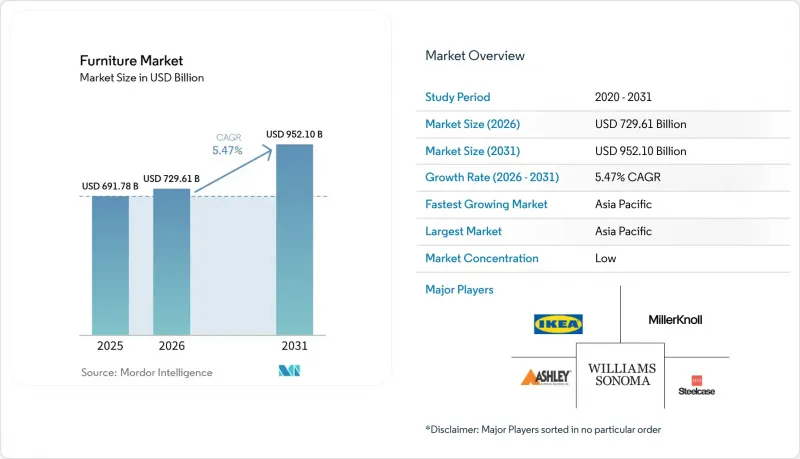

Mordor Intelligence에 의하면, 가구 시장 규모는 2025년 6,917억 8,000만 달러로 평가되었고, 2026년에는 7,296억 1,000만 달러로 추정되고, 2026-2031년 CAGR 5.47%로 성장을 지속할 전망이며, 2031년에는 9,521억 달러에 이를 것으로 예측됩니다.

본 보고서는 용도별(가정용 가구, 사무용 가구, 호텔 및 레스토랑용 가구, 교육용 가구 등), 소재별(목재, 금속, 플라스틱·폴리머 등), 가격대별(이코노미, 미드레인지, 프리미엄), 유통 채널별(B2C 및 소매, B2B 및 프로젝트), 지역별(북미, 남미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 가구 시장 동향 및 인사이트

밀레니얼 세대의 주택 리모델링이 다기능 가구 수요를 견인하고 있습니다.

2026년의 리모델링 열풍이 가구 시장을 견인하고 있습니다. 프로젝트의 범위가 단순한 외관 개편에 그치지 않고 공간 계획이나 여러 방의 리모델링으로 확대되면서, 인체공학에 기반한 기능과 수납 기능을 갖춘 모듈식 가구가 선호되고 있기 때문입니다. 하버드 대학의 주택 리모델링 선행 지표에 따르면, 2025년 미국의 주택 리모델링 지출은 5,090억 달러에 달할 것으로 예상되며, 이는 각 가구가 생산성, 웰빙, 그리고 하이브리드 생활 방식을 뒷받침하는 유연한 공간 구성을 우선시함에 따라 2026년에도 수요가 지속될 것임을 시사합니다. 시공 업체의 피드백에 따르면, 2023-2025년 대규모 프로젝트와 구조적 재설계가 증가하고 있으며, 이러한 추세로 인해 수요는 단기적인 리뉴얼이 아닌, 장기적인 교체 판단의 대상이 되는 내구성이 뛰어나고 다기능적인 가구로 이동하고 있습니다. 도시 지역의 공간적 제약으로 인해, 모듈형 소파, 벽걸이 침대, 중첩형 테이블, 유연한 수납용품에 대한 구매가 더욱 집중되고 있습니다. 이는 수십 년에 걸쳐 도시 지역의 1인당 건축 면적이 인구 증가율을 웃도는 속도로 확대되면서, 많은 가구에서 이용 가능한 공간이 부족해졌기 때문입니다. 리모델링 후, 대다수의 주택 소유자는 자택에 대한 애착이 더 깊어졌습니다고 보고하고 있으며, 이로 인해 주택 교체 주기가 길어지면서, 단순히 가격만을 중시하는 선택보다는 쾌적성, 수리 용이성, 다기능성을 중시하는 ‘그레이드 업’ 선택이 촉진되고 있습니다. 이러한 추세는 가구 시장에 안정적인 호재를 가져오고 있으며, 모듈식 제품 라인업과 공간에 대한 적합성을 명확히 제시하는 가이드를 갖춘 브랜드들이 온라인 및 오프라인 채널 모두에서 높은 계약 성사율을 달성하고 있습니다.

급속한 도시화가 공간 절약형 모듈러 가구의 판매를 촉진하고 있습니다.

급속한 도시화는 공간 절약형 및 모듈식 가구에 대한 수요를 견인하는 주요 구조적 요인입니다. 2025-2050년, 주로 아시아태평양 지역과 아프리카에서 5억 명 이상의 인구가 도시 지역으로 이주할 것으로 예측됩니다. 이러한 인구 유입으로 인해 이미 제한적인 도시 지역의 주거 공간, 특히 고밀도 임대 주택이나 소규모 주거 단위에 가해지는 압박이 더욱 심화되고 있으며, 구매 경향은 콤팩트하고 적층이 가능하며 벽걸이형인 가구 솔루션으로 전환되고 있습니다. 도시 주민 1인당 평균 연면적에 대한 제약은 사하라 이남 아프리카의 일부 지역에서 특히 두드러지며, 단일 설치 면적 내에서 업무, 돌봄, 사교 기능을 겸비한 모듈식 옷장, 로프트 침대, 다기능 소파의 도입이 확대되고 있습니다. 인도는 정부 주도의 주택 프로그램을 통해 보조금이 지원되는 도시 주택공급이 가속화되고 있으며, 인구 밀도가 높은 도시에서 공간을 최적화한 가구 형태에 대한 수요가 유도되고 있어, 큰 판매 기회를 내포하고 있습니다. 중국에서는 도시 지역의 주택 교체 수요가 증가함에 따라, 가구가 현대적인 주거 공간으로 업그레이드되는 과정에서 더 콤팩트하고 효율적인 평면 구조에 맞추어 설계된 가구의 판매가 늘어나고 있습니다. 도시 지역의 고령화 추세도 이러한 요인을 더욱 부추기고 있어, 접근성을 고려한 디자인, 내구성이 뛰어난 소재, 관리가 간편하고 항균 처리가 된 의료용 가구가 주택 및 지역 사회 공간에서 그 중요성이 커지고 있습니다. 이러한 요인들이 복합적으로 작용함에 따라, 급속한 도시화는 소매 및 프로젝트 채널 모두에서 모듈식 다기능 가구의 보급을 지속적인 원동력으로 자리매김하고 있습니다.

EU의 확대 생산자 책임(EPR) 규정에 따라 수출업체의 규정 준수 비용이 증가

EU에서 조만간 시행될 ‘지속 가능한 제품을 위한 에코디자인 규정’에 따르면, 2026년부터 해당 지역에서 판매되는 가구에 대해 내구성, 수리 가능성, 최소 재활용 소재 함유율 및 디지털 제품 여권을 의무화하는 ‘제조부터 폐기까지의 전체 수명 주기’를 포괄하는 체계가 도입됩니다. 이러한 규제 변경으로 인해, 규정 준수 기준을 충족하기 위해 추적성 시스템, 시험 프로토콜, 데이터 보고를 이행해야 하는 비EU 공급업체의 진입 비용이 증가하고 있습니다. 그 결과, 인증을 취득하고 감사에 대응할 수 있는 벤더와 규정 준수 기준을 충족하지 못하는 공급업체 사이에 뚜렷한 격차가 발생하고 있으며, 후자의 경우 기관 투자자나 주요 소매 플랫폼에 대한 접근이 제한되고 있습니다. 특히 아시아·태평양 지역의 수출업체들은 EU 규정을 준수하기 위해 제품 설계와 재료 성분 표기를 조정하고 있는 반면, 선도 기업들은 이러한 변화를 활용하여 유사한 지속가능성 요건을 갖춘 다른 지역에서 우위를 점하려고 하고 있습니다. 전반적으로, 규정 준수는 세계 가구 시장에서 필수적인 역량이 되었으며, 국제 시장 진출을 유지하려는 공급업체의 경우 업무의 복잡성과 비용이 증가하고 있습니다.

부문별 분석

2025년에는 거실 및 침실 가구 교체 수요가 계속해서 견조한 수요를 이끌며, 가정용 가구가 시장 점유율에서 가장 큰 비중을 차지해 62.76%를 나타낸 것으로 평가되었습니다. 그러나 재택 생활이 장기화되면서 초기에 급증했던 수주 동향은 점차 안정화되고 있습니다. 사무용 가구 시장은 2026-2031년 연평균 성장률(CAGR) 7.24%를 기록하며 가장 빠른 성장세를 보일 것으로 예측됩니다. 이는 인체공학에 기반한 의자, 높이 조절이 가능한 책상, 협업형 업무 공간 솔루션에 대한 수요를 높이는 하이브리드 근무 모델에 힘입은 결과입니다. 유연한 기업 사무실 이용 방침은 쾌적성, 음향적 사생활 보호, 직원의 웰빙을 향상시키고, 번아웃을 완화하는 데 기여하는 고성능 제품에 대한 투자를 촉진하고 있습니다. 호스피탈리티 및 교육 분야는 계속해서 호황을 누리고 있으며, 호텔과 학교에서는 유동 인구가 많은 구역을 위해 내구성이 뛰어나고 유지보수가 간편한 가구가 우선적으로 선택되고 있습니다. 한편, 의료 분야에서는 임상 수준에서 내구성과 쾌적성의 균형이 요구되고 있어, 닦아낼 수 있는 표면, 항균성이 있는 원단, 이동의 편의성을 고려한 디자인의 도입이 확대되고 있습니다.

수명 주기와 관련된 고려 사항은 용도에 따라 다르며, 구매 결정 및 총 소유 비용에 영향을 미칩니다. 주거용 가구는 일반적으로 7-10년의 교체 주기를 따르지만, 상업용 및 공공시설용 제품은 더 긴 보증 기간이 설정되어 있고 엄격한 사양 기준을 충족하고 있기 때문에 사후 서비스 및 부품 확보 가능성을 통해 기존 공급업체의 경쟁력이 강화되고 있습니다. ESG 기준도 중요한 역할을 하고 있으며, 구매자들은 규제 및 기업의 지속가능성 요건을 충족하기 위해 저탄소 소재, 인증된 목재, 수리가 용이한 디자인을 점점 더 많이 지정하고 있습니다. 전반적으로, 주택 부문에서는 여전히 판매량이 시장의 성장 동력으로 작용하고 있는 반면, 사무실, 의료, 교육 분야에서는 성능과 규정 준수가 시장의 성장 동력으로 작용하고 있으며, 이러한 분야에서는 내구성, 웰니스, 규제 준수성이 예측 기간 동안 프리미엄 포지셔닝을 뒷받침하고 있습니다.

목재는 여전히 가구 시장을 독점하고 있으며, 2025년에는 시장 규모의 51.76%를 차지한 것으로 평가되었지만, 금속은 2031년까지 연평균 성장률(CAGR)이 7.63%를 나타낼 것으로 전망되어 가장 빠르게 성장하는 소재로 부상하고 있습니다. 상업 부문의 구매자들은 재활용 가능성, 내구성, 장기적인 성능을 점점 더 중요하게 여기게 되면서, 장기간에 걸친 가혹한 사용 조건에도 견딜 수 있는 금속 프레임 및 수납 솔루션으로 소재 선택을 전환하고 있습니다. 목재 산업은 원자재 가격 변동, 조달 규제 강화, 여러 지역에 걸친 규정 준수 요건 등의 과제에 직면해 있으며, 이로 인해 수명이 긴 용도에서 금속의 매력이 높아지고 있습니다. 플라스틱 및 폴리머 소재는 실외용 및 가격에 민감한 부문에서 여전히 중요한 위치를 차지하고 있지만, 재활용 소재의 함유율 및 폐기물 감축에 대한 규제적 기대가 주요 시장의 배합 방식을 형성하고 있습니다. 유리나 가죽 등 특수 소재는 특히 질감, 미관, 투명성이 부가가치를 창출하는 호스피탈리티 업계나 고급 주택 분야에서 틈새 프리미엄 부문을 대상으로 계속해서 활용되고 있습니다. 제품 수명 종료 시의 고려 사항이 설계에 점점 더 큰 영향을 미치고 있으며, 탈부착이 가능한 고정 장치와 모듈식 구성 요소를 통해 개조 및 재활용이 용이해지고 있습니다.

가구 업계도 순환형 경제와 관련된 우려에 대응하기 위해 인증 및 추적성 시스템 도입에 주력하고 있으며, 이케아가 2024 회계연도에 사용한 목재의 97%가 FSC 인증을 받았거나 재활용 목재였습니다고 보고한 것이 그 한 예입니다. 상업 공간에서 금속의 사용 확대는 수명 주기 경제성을 반영하고 있습니다. 내구성과 교체 빈도가 낮다는 점이 사무실, 학교, 의료시설에서의 재정적·운영적 의사결정을 뒷받침하고 있습니다. EU의 ‘디지털 제품 여권’ 요건을 포함한 정책 동향은 검증·문서화·감사가 가능한 소재와 디자인을 장려하고 있으며, 견고한 규정 준수 프로그램을 갖춘 공급업체를 선정하는 데 영향을 미치고 있습니다. 디자인 팀은 초기 단계부터 수리 용이성, 유지보수성, 모듈성을 반영하여 미관과 기능성, 그리고 규제 요건 간의 균형을 맞추고 있습니다. 시장 전반에 걸쳐 의사결정은 순수한 시각적 매력보다는 제품 수명 주기 전반에 걸친 성능, 내구성, 그리고 ESG 기준 준수 여부에 따라 점점 더 좌우되고 있습니다. 이러한 변화들이 복합적으로 작용하여, 금속의 성능적 장점과 목재의 인증된 지속가능성 자격이 공존함으로써, 진화하는 시장과 정책의 기대에 부응하는 소재 환경이 강화되고 있습니다.

지역별 분석

아시아태평양은 2025년에 47.76%의 점유율을 차지했으며, 세계 가구 시장을 주도하고 있으며, 2031년까지 연평균 성장률(CAGR) 7.44%로 가장 빠른 성장세를 보일 것으로 전망됩니다. 이 지역에서는 인도의 성장이 두드러지고 있으며, 소형 주택 프로그램과 도시의 고밀화 추세가 뒷받침되면서 신규 구매와 교체 구매 주기 모두에서 모듈식이며 다기능적인 가구가 선호되고 있습니다. 중국에서는 도시 지역의 아파트 시장에서 주택 교체 수요가 계속해서 주도적인 역할을 하고 있으며, 도시 차원의 인프라 확충과 소매 매출 증가가 콤팩트하고 변형이 가능한 가구에 대한 수요를 뒷받침하고 있습니다. 2025년에 도입된 저배출 가구 기준 등의 규제 조치가 해당 지역공급업체들이 소재와 마감재를 선택하는 데 영향을 미치고 있습니다. 또한, 동남아시아의 제조 거점은 여전히 중요하며, 브랜드가 조달처를 다각화하면서도 인건비와 물류 비용의 균형을 맞출 수 있게 되었습니다.

북미는 미국을 중심으로 한 제2의 지역 시장으로, 주택 착공 건수와 리모델링 활동이 가구 수요의 안정적인 기반이 되고 있습니다. 2025년 초, 미국의 주택 착공 건수는 연율 환산으로 150만 호에 달한 것으로 평가되었으며, 5,090억 달러 규모로 전망되는 리모델링 활동은 주거 환경의 수준 향상과 재택근무 환경 조성을 뒷받침하고 있습니다. 캐나다는 하이브리드 근무 환경 구축과 주택 교체 주기를 통해 시장에 기여하고 있으며, 멕시코는 니어쇼어링과 미국 수출을 위한 생산 능력 확대에 힘입어 해당 지역에서 가장 빠른 성장세를 보이고 있습니다. 주요 옴니채널 소매업체와 순수 전자상거래 플랫폼은 배송 속도와 대량 주문 성사율을 최적화하기 위해 매장 네트워크와 디지털 자산을 지속적으로 연계하고 있습니다. 해당 지역 전체에서 수요는 인체공학적 개선, 신속한 주문 처리, ESG 기준을 충족하는 인증된 소재의 영향을 점점 더 크게 받고 있습니다.

유럽은 여전히 중요한 시장이며, 규제 체계가 제품 설계, 문서화 및 사용 후 제품 처리 계획을 규정하고 있습니다. 디지털 제품 여권을 포함한 EU의 ‘지속 가능한 제품을 위한 에코디자인 규정’에 따라 규정 준수 요건이 강화됨에 따라, 가구 제품 라인업은 수리 가능성과 재활용 가능성을 중시하는 방향으로 변화하고 있습니다. 유럽에 뿌리를 둔 세계 브랜드들은 비용 효율성을 유지하고 배송 속도를 높이기 위해 자동화 및 네트워크 확장에 투자하고 있습니다. 중동 및 아프리카에서는 사우디아라비아의 ‘비전 2030’에 기반한 주택 및 호텔·관광 프로젝트가 성장의 원동력이 되고 있는 반면, 아프리카의 도시화에 따라 공식적인 고성장 대도시권과 비공식적인 저가 부문으로 양극화된 시장이 형성되고 있습니다. 이 지역 전체에서 2026년에도 에너지 비용, 물류의 신뢰성, 정책 동향이 원자재 선정, 가격 책정, 유통 전략을 계속해서 좌우하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the furniture market size is expected to grow from USD 691.78 billion in 2025 to USD 729.61 billion in 2026 and is forecast to reach USD 952.10 billion by 2031 at a 5.47% CAGR over 2026-2031.

This report is Segmented by Application (Home Furniture, Office Furniture, Hospitality Furniture, Educational Furniture, and More), Material (Wood, Metal, Plastic & Polymer, and More), Price Range (Economy, Mid-Range, Premium), Distribution Channel (B2C/Retail, and B2B/Project), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Furniture Market Trends and Insights

Millennial Home Remodeling Driving Multi-Functional Furniture Demand

Remodeling activity in 2026 supports the furniture market as project scopes widen beyond cosmetic updates into space planning and multi-room upgrades that favor modular pieces with ergonomic and storage features. Harvard's Leading Indicator of Remodeling Activity projected United States home improvement spending at USD 509 billion for 2025, which signaled sustained demand entering 2026 as households prioritize productivity, well-being, and adaptable layouts that support hybrid routines. Contractor feedback points to larger projects and more structural reimagination across 2023-2025, a pattern that channels demand toward durable, multifunctional furniture that serves as a long-horizon replacement decision rather than a short-cycle refresh. Urban space constraints further concentrate purchases into modular sofas, wall-beds, nesting tables, and flexible storage as built-up area per capita in cities has grown faster than population over multi-decade windows, tightening usable space for many households. After remodeling, a majority of homeowners report stronger attachment to their homes, which extends replacement cycles and supports trade-up choices that emphasize comfort, repairability, and multi-function over purely price-driven options. These dynamics provide a steady tailwind in the furniture market as brands with modular assortments and clear fit-for-space guidance win higher conversion in both digital and store channels.

Rapid Urbanization Boosting Space-Saving Modular Furniture Sales

Rapid urbanization is a key structural driver of space-saving and modular furniture demand, with more than 500 million additional people expected to move into cities between 2025 and 2050, primarily across Asia-Pacific and Africa. This influx is intensifying pressure on already limited urban living space, particularly in high-density rental housing and small residential units, shifting purchasing preferences toward compact, stackable, and wall-mounted furniture solutions. Constraints on average built-up area per urban resident are especially pronounced in parts of Sub-Saharan Africa, increasing the adoption of modular wardrobes, loft beds, and convertible seating that can serve work, caregiving, and social functions within a single footprint. India represents a major volume opportunity as government-led housing programs have accelerated the delivery of subsidized urban homes, channeling demand toward space-optimized furniture formats in dense cities. In China, rising replacement purchases in urban centers are supporting sales of furniture designed for smaller, more efficient layouts as households upgrade to modernized living spaces. Urban aging trends further reinforce this driver, as healthcare-oriented furnishings with accessible designs, durable materials, and easy-clean, antimicrobial finishes gain relevance in residential and community settings. Collectively, these factors position rapid urbanization as a sustained catalyst for modular, multifunctional furniture adoption across both retail and project channels.

EU Extended Producer Responsibility (EPR) Rules Increasing Compliance Costs for Exporters

The upcoming Ecodesign for Sustainable Products Regulation in the EU introduces a cradle-to-grave framework requiring durability, repairability, minimum recycled content, and Digital Product Passports for furniture sold in the region, starting in 2026. This regulatory shift is increasing entry costs for non-EU suppliers, who must implement traceability systems, testing protocols, and data reporting to meet compliance standards. As a result, a clear divide is emerging between certified, audit-ready vendors and non-compliant suppliers, with limited access to institutional buyers and major retail platforms for the latter. Exporters, particularly in Asia-Pacific, are adjusting product design and material declarations to meet EU rules, while early movers are leveraging these changes to gain advantages in other regions with similar sustainability requirements. Overall, compliance has become a critical capability in the global furniture market, elevating operational complexity and costs for suppliers seeking to maintain international market access.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Digital-First D2C Brands Increasing Online Furniture Penetration

- Corporate ESG Mandates Encouraging Use of Recycled and Bio-Based Materials

- High Cross-Border Logistics Costs and Damage Risks Limiting E-Commerce Furniture Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, home furniture accounts for the largest share of the market, representing 62.76% as living room and bedroom replacements continue to drive steady demand. However, order trends are stabilizing after the earlier surge associated with extended home nesting. Office furniture is expected to register the fastest growth at a 7.24% CAGR from 2026 to 2031, fueled by hybrid work models that increase demand for ergonomic seating, adjustable desks, and collaborative workspace solutions. Flexible corporate occupancy policies support investments in high-spec products that enhance comfort, acoustic privacy, and employee well-being, helping reduce burnout. Hospitality and education sectors remain active, with hotels and schools prioritizing durable, low-maintenance furniture for high-traffic areas, while healthcare applications require a balance of clinical-grade durability and comfort, driving adoption of wipeable surfaces, antimicrobial fabrics, and mobility-friendly designs.

Lifecycle considerations differ across applications, influencing purchasing decisions and total cost of ownership. Residential furniture typically follows 7-10 year replacement cycles, whereas commercial and institutional products carry longer warranties and meet rigorous specification standards, reinforcing vendor incumbency through after-sales service and parts availability. ESG criteria also play a significant role, with buyers increasingly specifying low-emission materials, certified wood, and repair-friendly designs to meet regulatory and corporate sustainability requirements. Overall, the market remains volume-driven in residential segments while being performance- and compliance-driven in office, healthcare, and education, where durability, wellness, and regulatory alignment support premium positioning during the forecast period.

Wood continues to dominate the furniture market, accounting for 51.76% share of the market size in 2025, but metal is emerging as the fastest-growing material with a projected 7.63% CAGR through 2031. Commercial buyers are increasingly prioritizing recyclability, durability, and long-term performance, shifting material selection toward metal frames and storage solutions that can withstand heavy use over extended periods. Wood faces challenges from input cost volatility, tighter sourcing regulations, and compliance requirements across multiple regions, reinforcing the appeal of metal for long-life applications. Plastic and polymer materials maintain relevance in outdoor and budget-sensitive segments, though regulatory expectations for recycled content and waste reduction are shaping formulations in major markets. Specialty materials like glass and leather continue to serve niche premium segments, particularly in hospitality and luxury residential settings where texture, aesthetics, and transparency add value. End-of-life considerations are increasingly influencing design, with reversible fasteners and modular components enabling easier refurbishment and recycling.

The furniture industry is also leaning into certification and traceability to address circularity concerns, as highlighted by IKEA reporting that 97% of its wood in FY24 was FSC-certified or recycled. Metal's growing adoption in commercial spaces reflects lifecycle economics, where durability and lower replacement frequency support financial and operational decisions in offices, schools, and healthcare facilities. Policy trends, including the EU's Digital Product Passport requirements, favor materials and designs that can be verified, documented, and audited, influencing vendor selection toward suppliers with robust compliance programs. Design teams are integrating repairability, serviceability, and modularity from the start, balancing aesthetics with functionality and regulatory demands. Across the market, decisions are increasingly guided by lifecycle performance, durability, and ESG alignment, rather than purely visual appeal. Together, these shifts reinforce a material landscape where metal's performance advantages and wood's certified sustainability credentials coexist to meet evolving market and policy expectations.

Geography Analysis

Asia-Pacific dominates the global furniture market with a 47.76% share in 2025 and is projected to record the fastest growth at a 7.44% CAGR through 2031. India's growth in the region stands out, supported by compact-footprint housing programs and urban densification that favor modular and multifunctional furniture for both new and replacement cycles. China continues to drive replacement demand in urban apartments, with city-level upgrades and retail sales growth supporting compact and convertible furniture formats. Regulatory initiatives, such as low-emission furniture standards introduced in 2025, are shaping material and finish choices for suppliers in the region. Southeast Asia's manufacturing base also remains critical, enabling brands to diversify sourcing while balancing labor and logistics costs.

North America is the second-largest regional market, anchored by the United States, where housing starts and remodeling activity provide a steady base for furniture demand. United States housing starts reached 1.50 million annualized units in early 2025, while remodeling activity, projected at USD 509 billion, supports upgrades and home office improvements. Canada contributes through hybrid work upgrades and residential replacement cycles, and Mexico records the fastest regional growth, driven by nearshoring and expanded manufacturing capacity for United States-bound exports. Leading omnichannel retailers and pure-play e-commerce platforms continue to align store footprints with digital assets to optimize delivery speed and conversion on larger orders. Across the region, demand is increasingly influenced by ergonomic upgrades, faster fulfillment, and certified materials that meet ESG criteria.

Europe remains a significant market, with regulatory frameworks shaping product design, documentation, and end-of-life planning. The EU Ecodesign for Sustainable Products Regulation, including Digital Product Passports, is increasing compliance requirements and influencing furniture assortments toward repairability and recyclability. European-rooted global brands are investing in automation and network expansion to maintain cost efficiency and faster delivery. In the Middle East and Africa, growth is driven by Saudi Arabia's Vision 2030 housing and hospitality projects, while African urbanization creates a two-tier market of formal high-growth metros and informal budget segments. Across these regions, energy costs, logistics reliability, and policy developments continue to shape material selection, pricing, and distribution strategies in 2026.

- IKEA

- Ashley Furniture Industries Inc.

- Steelcase Inc.

- MillerKnoll, Inc.

- HNI Corporation

- Williams-Sonoma Inc.

- La-Z-Boy Incorporated

- Hooker Furniture Corp.

- Kimball International Inc.

- Haworth Inc.

- Wayfair LLC

- Godrej Interio

- Durian Industries Ltd.

- Foshan Huasheng Furniture

- KOKUYO Co. Ltd.

- Shanghai UE Furniture

- Leggett & Platt Inc.

- Okamura Corporation

- Nitori Holdings Co. Ltd.

- KUKA Home

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Home-Remodel Spend By Millennials Powering Multi-Functional Furniture Demand

- 4.1.2 Rapid Urbanization Is Driving Space-Saving Modular Furniture Sales

- 4.1.3 Expansion of Digital-First D2C Furniture Brands Boosting Online Penetration

- 4.1.4 Corporate ESG mandates spurring adoption of recycled & bio-based furniture materials

- 4.1.5 Remote and Hybrid Work Driving Home Office Furniture Demand

- 4.1.6 Rising Middle-Class Income Supporting Premium and Customized Furniture Purchases

- 4.2 Market Restraints

- 4.2.1 EU Extended Producer Responsibility (EPR) Rules Raising Compliance Costs For Exporters

- 4.2.2 High Cross-Border Logistics Costs & Damage Rates Curbing Bulky E-Commerce Furniture Margins

- 4.2.3 Volatility in raw material prices is increasing manufacturing costs

- 4.2.4 Trade tariffs and import duties limit cross-border market access

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Bargaining Power of Buyers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

- 4.5 Insights into the Latest Trends and Innovations in the Market

- 4.6 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

- 4.7 Insights on Regulatory Framework and Industry Standards for the Furniture Industry in Key Geographies

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Home Furniture

- 5.1.1.1 Chairs

- 5.1.1.2 Tables (side tables, coffee tables, dressing tables, etc.)

- 5.1.1.3 Beds

- 5.1.1.4 Wardrobes

- 5.1.1.5 Sofas

- 5.1.1.6 Dining Tables/Dining Sets

- 5.1.1.7 Kitchen Cabinets

- 5.1.1.8 Other Home Furniture (bathroom furniture, outdoor furniture, etc.)

- 5.1.2 Office Furniture

- 5.1.2.1 Chairs

- 5.1.2.2 Tables

- 5.1.2.3 Storage Cabinets

- 5.1.2.4 Desks

- 5.1.2.5 Sofas and Other Soft Seating

- 5.1.2.6 Other Office Furniture

- 5.1.3 Hospitality Furniture

- 5.1.4 Educational Furniture

- 5.1.5 Healthcare Furniture

- 5.1.6 Other Applications (public places, retail malls, government offices, etc.)

- 5.1.1 Home Furniture

- 5.2 By Material

- 5.2.1 Wood

- 5.2.2 Metal

- 5.2.3 Plastic & Polymer

- 5.2.4 Other Materials

- 5.3 By Price Range

- 5.3.1 Economy

- 5.3.2 Mid-Range

- 5.3.3 Premium

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail

- 5.4.1.1 Home Centers

- 5.4.1.2 Specialty Furniture Stores

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B /Project

- 5.4.1 B2C/Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 Sweden

- 5.5.3.8 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.9 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East And Africa

- 5.5.5.1 United Arab of Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 IKEA

- 6.3.2 Ashley Furniture Industries Inc.

- 6.3.3 Steelcase Inc.

- 6.3.4 MillerKnoll, Inc.

- 6.3.5 HNI Corporation

- 6.3.6 Williams-Sonoma Inc.

- 6.3.7 La-Z-Boy Incorporated

- 6.3.8 Hooker Furniture Corp.

- 6.3.9 Kimball International Inc.

- 6.3.10 Haworth Inc.

- 6.3.11 Wayfair LLC

- 6.3.12 Godrej Interio

- 6.3.13 Durian Industries Ltd.

- 6.3.14 Foshan Huasheng Furniture

- 6.3.15 KOKUYO Co. Ltd.

- 6.3.16 Shanghai UE Furniture

- 6.3.17 Leggett & Platt Inc.

- 6.3.18 Okamura Corporation

- 6.3.19 Nitori Holdings Co. Ltd.

- 6.3.20 KUKA Home

7 Market Opportunities & Future Outlook

- 7.1 Shift Toward Sustainable and Eco-Conscious Furniture

- 7.2 Evolving E-commerce and Immersive Digital Experiences