|

시장보고서

상품코드

2066529

드론 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

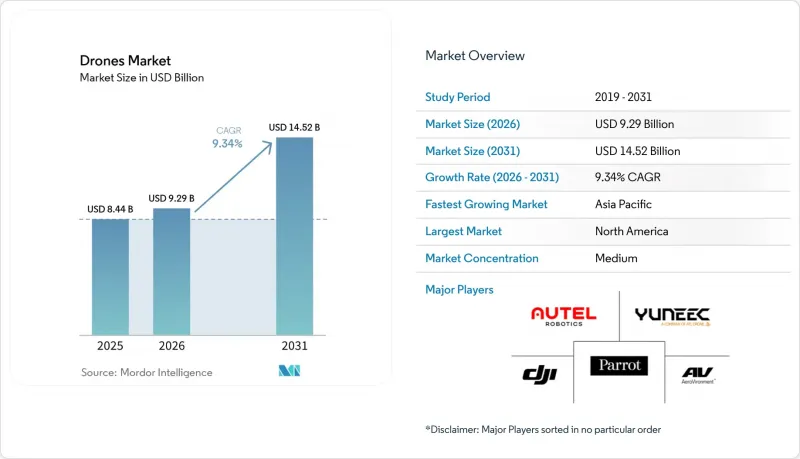

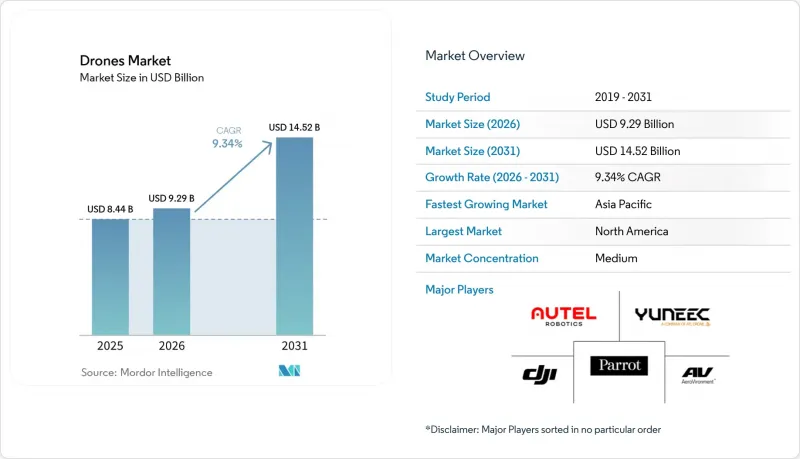

Mordor Intelligence에 의하면, 드론 시장 규모는 2025년 84억 4,000만 달러에서 2026년에는 92억 9,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 9.34%로 성장을 지속하여, 2031년에는 145억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 용도별(건설, 농업, 에너지, 엔터테인먼트 등), 유형별(고정익, 회전익 등), 중량 등급별(나노/마이크로, 소형, 중형, 대형), 운용 모드별(원격 조종, 옵션 조종 등), 최종 사용자(상업용·민간용 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 드론 시장 동향과 인사이트

드론 스타트업에 대한 투자 및 벤처 자금 조달 증가

2024년부터 2026년까지 드론 시장에서 자금 조달 및 사업 확장 움직임이 활발해지면서, 반복 가능한 운영과 규제 대응 체계를 입증할 수 있는 운영사 및 플랫폼 제공업체로 유입되는 자본이 증가했습니다. 배송 업체들은 상업용 소포 서비스를 위한 파트 135 인가를 취득함으로써 사업을 발전시켰으며, 체계적인 규제 체제 하에서 일관된 비행 운영을 이미 입증한 기업들에 대한 투자자들의 관심을 끌었습니다. Terra Drone사가 미국에서 처리된 LAANC 승인의 대부분을 차지하는 FAA 인증 UTM 제공업체인 Aloft Technologies사의 잔여 지분을 인수한 것은 확장 가능한 인프라 및 교통 관리 솔루션에 대한 투자가 확대되고 있음을 여실히 보여주고 있습니다. 전반적으로 드론 시장에서는 지속적인 운영 능력과 규정 준수 관련 전문 지식, 그리고 견고한 기술을 모두 갖춘 기업에 막대한 투자가 몰리고 있으며, 시범 프로젝트에서 대규모 확대로의 전환이 가속화되고 있습니다.

DIAB의 확대와 완전 자율형 운영 모델의 보급

도킹 시스템, 통합 센서 및 인증된 항공 적합성 기능이 양산 단계에 접어들면서, 조종사 주도의 운용에서 자율 비행 기체로 전환되는 속도가 빨라지고 있습니다. DJI를 비롯한 기업용 벤더 각사는 광대한 부지 내 인프라의 보안 확보 및 점검을 위해, 상시 감시 및 예정된 임무를 지원하는 도킹 기능을 갖춘 원격 조종을 추진하고 있습니다. 규제 대상인 여객 운항 분야에서도 자율화가 진행되고 있으며, EHang의 운항 사업자는 조종사 없이 승객을 수송하는 비행에 대해 중국민용항공국(CAAC)으로부터 항공운송사업허가증을 취득했습니다. 이는 인증을 받은 UAM이 정의된 비행 경로 및 절차에 따라 운항을 시작할 수 있음을 나타냅니다. 유럽의 U-space 규정은 공통된 절차와 데이터 교환을 통해 자율 비행을 조정하는 분산형 교통 서비스를 뒷받침하며, ‘Drone-in-a-Box’와 같은 모델을 지원하는 동시에 항공기 간 간격 및 예기치 못한 상황에 대한 대응도 관리하고 있습니다. 오토파일럿 기술의 발전은 기업용 드론 군에도 영향을 미치고 있으며, Parrot과 같이 보안을 중시하는 플랫폼에서는 기밀성이 높은 임무에서 개인정보 보호 및 규정 준수 요건을 충족하기 위해 보안 요소, 암호화된 데이터 파이프라인, 온보드 처리가 중요시되고 있습니다.

리튬 이온 배터리 셀 공급 부족으로 소형 드론의 BOM 비용이 상승

주요 배터리 부품공급 제약으로 인해, 가격에 민감한 플랫폼, 특히 생산 대수에 따라 비용이 변동하기 쉬운 소형 드론 부문에서 부품 원가(BOM)에 대한 민감도가 더욱 높아지고 있습니다. 각 제조업체는 특정 부품공급 지연이 발생하더라도 기체의 납기를 준수할 수 있도록, 공급의 지속성과 ‘가용성을 고려한 설계(Design-for-Availability)’를 우선시하고 있습니다. 안정적인 배터리 및 모터 공급에 의존하는 각 공급업체들은 안전성 요건이나 주행 거리를 저해하지 않는 범위 내에서 조달 계획을 세밀하게 조정하고 부품 대체를 지속적으로 추진하고 있습니다. 일부 제조업체들은 기밀성이 높은 분야에서 확실한 조달 체제가 자사의 가치 제안의 핵심을 이룬다는 점을 공개적으로 강조하고 있으며, 이는 부품의 출처와 최종 제품의 규정 준수 중요성을 다시금 부각시키고 있습니다. 이러한 요인으로 인해 일시적인 비용 상승이 발생하고 있으며, 드론 시장은 공급업체와의 관계를 다각화하고, 성능 목표를 충족하는 검증된 대체품을 확보하고 있는 공급업체로 점차 전환되고 있습니다.

부문별 분석

2025년에는 기타 용도가 33.23%의 점유율을 차지했으나, 농업 분야는 2031년까지 연평균 성장률(CAGR) 10.28%로 성장할 것으로 전망됩니다. 드론 시장에서는 공공 안전, 측량, 미디어 관련 등 다양한 분야에서 광범위한 활용이 확대되고 있습니다. 그러나 비행 시간이 경작 면적 확대 및 투입 자재 절감과 직결되기 때문에 농업 분야가 가장 높은 투자 수익률(ROI)을 가져다주고 있습니다. 각 OEM 업체의 로드맵은 적재량과 처리 능력 향상에 중점을 두고 있으며, XAG사의 P150 Max와 같은 플랫폼은 더 큰 탱크, 더 넓은 살포 범위, 그리고 고속 충전을 지원하도록 설계되었습니다. 이를 통해 서비스 제공업체는 성수기 동안 작업 주기를 단축할 수 있게 됩니다. 통합된 농업 소프트웨어는 이러한 기능을 보완하여, 드론을 지도 합성, 변동성 분석, 그리고 현장에서 가변 시비율을 통해 성능을 향상시키는 처방전 작성을 수행하는 용도과 연동합니다. 이러한 요소들 덕분에 농업은 플랫폼 개선이 일상적인 생산성의 뚜렷한 향상으로 이어지는 대규모 수직 시장으로서의 입지를 공고히 하고 있습니다.

농업 분야의 유닛 경제학은 일회성 건설 측량이나 비정기적인 미디어 촬영과 같이, 비행 시간이 반복적인 프로그램을 뒷받침하기 어려운 저밀도 용도와는 크게 다릅니다. 또한 UAM(도심항공모빌리티(UAM))도 업계의 한 축을 차지하고 있으며, 중국에서는 지정된 항공 노선에서 무인 여객 서비스가 운항되고 있습니다. 이러한 추세는 인증된 기체의 수가 늘어남에 따라 새로운 부문이 등장할 가능성을 시사하고 있습니다. 많은 기업에게 있어 도입의 주요 장애물은 더 이상 기기의 성능이 아니라, 하류 시스템과의 통합 품질에 있습니다. 이 통합의 질에 따라 드론 데이터가 일관된 업무 개선으로 이어질지 여부가 결정되기 때문입니다. 통합 과정이 진행됨에 따라 드론 시장은 빈번한 임무와 측정 가능한 성과를 특징으로 하는 분야에 초점을 맞출 것으로 예측됩니다.

2025년에는 회전익 플랫폼이 70.25%의 시장 점유율을 차지해, 2031년까지 연평균 성장률(CAGR) 9.92%로 성장할 것으로 전망됩니다. 좁은 공간에서의 다용도성, 조종사의 작업 부담 경감, 신속한 설치 덕분에 20분에서 40분 정도의 임무 시간으로 충분한 건설, 공공 안전 및 다양한 점검 업무 분야에서 멀티로터가 표준적인 선택지로 자리 잡고 있습니다. 고정익 및 하이브리드형 플랫폼은 항속 거리와 체공 시간 측면에서 성능상의 우위를 유지하고 있으며, 임무 특성상 발사 및 회수 인프라의 설치가 타당화되는 장거리 점검이나 대규모 매핑에 적합합니다. UAM(도심항공모빌리티(UAM))은 또 다른 차원을 더하며, 인증을 받은 eVTOL(전동 수직 이착륙기) 설계는 도시 회랑 내에서의 수직 이착륙과 승객의 안전을 보장하고, VTOL(수직 이착륙)의 장점을 규제된 비행 적합성 및 지정 노선과 결합하고 있습니다.

가격대나 물류 측면도 회전익형과 고정익형의 구성 비율에 영향을 미치고 있습니다. 일상적인 업무에 통합된 멀티로터는 배치 및 재배치가 용이하기 때문에 빈번하고 단시간에 끝나는 임무가 많은 업계에서는 가동률을 높게 유지할 수 있습니다. 반면, 고정익 플랫폼의 경우 훈련을 받은 팀과 현장 절차가 필요하기 때문에 프로젝트가 대규모로 진행되지 않는 한 많은 상업 운영업체에게는 경제성이 떨어질 수 있습니다. 민간 시장 전체를 보면, 드론 시장에서 회전익기가 주도적인 위치를 유지하는 한편, 고정익기는 장거리·장시간 비행 임무와 같은 틈새 분야에서 우위를 유지할 것으로 전망됩니다.

지역별 분석

2025년 기준으로 북미는 시장의 37.86%를 차지했습니다. 해당 지역의 정책 환경은 BVLOS(시야 밖) 운항이 일상화되는 방향으로 나아가고 있으며, FAA(연방항공청)가 제안한 규정의 최종 결정이 예정되어 있습니다. 미국에서는 인증된 운송업체가 파트 135 절차에 따라 운항하는 체계 속에서 배송 사업이 지속적으로 확대되고 있으며, 안전성 및 비행 적합성 기준을 충족하는 업체에 투자가 집중되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.88%를 나타낼 것으로 전망됩니다. 중국의 저고도 경제는 주요 도시에서 무인 여객 운항을 가능하게 한 국내 규제 체제 하에서 발전하고 있으며, 이 지역은 상업용 UAM의 선구자로서의 위상을 확립하고 있습니다. 농업 분야에서의 도입은 여러 농업 중심지에서 확대되고 있으며, 항공 살포의 경제성이 입증되어 서비스 네트워크가 뒷받침되고 있습니다. 지역 내 각 OEM 기업들은 특히 농업 분야에서 생산 능력과 플랫폼 기능을 확대하고 있으며, 적재량과 급속 충전을 통해 더 긴 가동 주기와 성수기의 처리 능력을 뒷받침하고 있습니다.

유럽에서는 개인정보 보호 및 데이터 보호 요건을 준수하면서 자율 비행을 지원하는 통합 공역 관리 시스템의 개발이 계속되고 있습니다. 'U-space'의 조화를 통해 회원국 전체에 걸쳐 무인항공기(UAS) 교통 관리를 위한 공통 서비스와 절차가 제공되고 있으며, 이는 국경을 초월한 서비스 및 자율 비행 편대의 통합에 필수적입니다. 데이터 보안과 개인정보 보호는 여전히 조달 과정에서 결정적인 요소로 작용하고 있으며, 암호화 및 안전한 데이터 흐름을 입증하는 공급업체에 대한 수요를 높이고 있습니다. 라틴아메리카에서는 농업 현대화 프로그램과 기업 주도의 자금 조달 이니셔티브가, 보다 광범위한 생산성 목표 및 농촌 지역 서비스 네트워크와 연계된 항공 살포 도입을 뒷받침하고 있습니다. 이러한 지역별 특유 요인들이 도입 양상을 형성하고 있으며, 정책 준비 상황과 부문별 우선순위에 따라 드론 시장이 어디에서 가장 빠르게 성장할 수 있을지가 결정됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the drones market size is expected to grow from USD 8.44 billion in 2025 to USD 9.29 billion in 2026 and is forecasted to reach USD 14.52 billion by 2031 at 9.34% CAGR over 2026-2031.

This report is Segmented by Application (Construction, Agriculture, Energy, Entertainment, and More), Type (Fixed-Wing, Rotary-Wing, and More), Weight Class (Nano/Micro, Small, Medium, and Large), Mode of Operation (Remotely Piloted, Optionally Piloted, and More), End User (Commercial and Consumer, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Drones Market Trends and Insights

Increasing Investment and Venture Funding in Drone Startups

Funding and scale-up activity in the drones market intensified from 2024 to 2026, with capital increasingly directed to operators and platform providers that can demonstrate repeatable operations and regulatory readiness. Delivery operators advanced by obtaining Part 135 authorizations for commercial package services, aligning investor interest with businesses already demonstrating consistent flight operations under a structured regulatory regime. Terra Drone's acquisition of the remaining stake in Aloft Technologies, an FAA-certified UTM provider with a significant share of LAANC authorizations processed in the United States, highlights growing investments in scalable infrastructure and traffic management solutions. Overall, the drones market is attracting significant investments in companies that combine recurring operational capabilities with compliance expertise and robust technology, facilitating the transition from pilot projects to scaled deployments.

Expansion of DIAB and Fully Autonomous Operational Models

The shift from pilot-operated missions to autonomous fleets is accelerating as docking systems, integrated sensors, and certified airworthiness features move into production. DJI and other enterprise vendors promote dock-enabled remote operations that support always-on monitoring and scheduled missions for infrastructure security and inspections across large sites. Autonomy is also advancing in regulated passenger operations, with EHang operators obtaining Air Operator Certificates from the CAAC for pilotless human-carrying flights, which demonstrates that certified UAM can launch under defined corridors and procedures. European U-space rules underpin distributed traffic services that coordinate automated flights with common procedures and data exchange, supporting models like Drone-in-a-Box while managing separation and contingencies. Autopilot advancements are moving into enterprise fleets as well, where security-focused platforms like Parrot emphasize secure elements, encrypted data pipelines, and onboard processing that fit privacy and compliance requirements for sensitive missions.

Li-ion Cell Supply Crunch Inflating Small-Drone BOM Costs

Supply constraints on key battery inputs have heightened sensitivity to bill-of-material costs for price-sensitive platforms, most notably in small drone categories that scale with unit volume. Manufacturers have prioritized continuity of supply and design-for-availability approaches so that airframes can maintain delivery schedules when specific components are delayed. Vendors that rely on consistent battery and motor inflows continue to refine sourcing plans and component substitutions where this can be achieved without compromising safety cases or endurance. Some makers have publicly emphasized that secure sourcing is a core part of their value proposition in sensitive categories, reinforcing the importance of component provenance and end-product compliance. These factors create a temporary cost overhang, pushing the drones market toward vendors with diversified supplier relationships and tested substitutions that meet performance targets.

Other drivers and restraints analyzed in the detailed report include:

- Progressive BVLOS and U-space/UTM Regulatory Advancements

- Scaling of Precision Agriculture and Rural Drone Service Networks

- Government Policies and Airspace Regulations Hampering the Usage of Drones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Other applications accounted for a 33.23% share in 2025, while agriculture is projected to grow at a 10.28% CAGR through 2031. The drones market is seeing widespread use across diverse public-safety, surveying, and media missions. Yet, agriculture delivers the highest return on investment because flight hours directly translate into treated acreage and reduced inputs. OEM roadmaps have focused on increasing payload and throughput, with platforms such as XAG's P150 Max designed to handle larger tanks, broader spread rates, and fast recharging so service providers can compress turnaround times during peak windows. Integrated agronomy software complements these capabilities, linking drones to applications that stitch maps, analyze variability, and produce prescriptions that drive variable-rate performance in the field. These elements reinforce agriculture as a high-volume vertical where platform improvements translate into clear daily productivity gains.

The unit economics of agriculture differ significantly from those of lower-density applications, such as one-off construction surveys or occasional media capture, where flight hours are less likely to support repeatable programs. UAM is also becoming part of the landscape, with pilotless passenger services operating in designated corridors in China. This development indicates the potential emergence of new segments as certified fleets expand. For many enterprises, the primary barrier to adoption is no longer the airframe's capability but rather the quality of integration with downstream systems, which determines whether drone data translates into consistent operational improvements. As integration processes advance, the drones market is expected to focus on verticals characterized by frequent missions and measurable outcomes.

Rotary-wing platforms held a 70.25% share in 2025 and are projected to grow at a 9.92% CAGR through 2031. Versatility in confined spaces, reduced pilot workload, and rapid setup make multirotors the default for construction, public safety, and many inspection tasks where 20- to 40-minute missions suffice. Fixed-wing and hybrid platforms maintain a performance edge on range and endurance, which suits long-line inspection and mapping at scale, where mission profiles justify launch and recovery infrastructure. UAM adds another layer, where certificated eVTOL designs offer vertical takeoff and passenger safety cases for city corridors, tying VTOL benefits to regulated airworthiness and designated routes.

Price points and logistics also shape the mix between rotary and fixed-wing types. Multirotors that slot into everyday jobs are easier to stage and redeploy, which keeps utilization high in industries with frequent, short missions. Fixed-wing platforms, on the other hand, require trained teams and field procedures that many commercial operators cannot justify unless projects run at scale. Across civilian markets, the drones market will likely maintain rotary-wing leadership, while fixed-wing types retain niche dominance in long-range and high-endurance missions.

Geography Analysis

North America accounted for 37.86% of the market in 2025. The region's policy environment is moving toward normalized BVLOS operations, with the FAA's proposed rule scheduled for final determination. US delivery continues to expand within a framework in which certificated carriers operate under Part 135 procedures, channeling investment into operators that meet safety and airworthiness thresholds.

Asia-Pacific is projected to post a 9.88% CAGR through 2031. China's low-altitude economy is advancing under a domestic regulatory system that has enabled pilotless passenger flights in major cities, positioning the region as a first mover in commercial UAM. Agricultural adoption has scaled across several farming centers, validating the economics of aerial application and supporting service networks. Regional OEMs are expanding capacity and platform capabilities, particularly in agriculture, where payload and rapid charging support longer duty cycles and peak-season throughput.

Europe continues to develop an integrated airspace management system that supports automated operations while aligning with privacy and data protection requirements. U-space harmonization provides common services and procedures for UAS traffic management across member states, which are essential for cross-border services and the integration of autonomous fleets. Data security and privacy remain decisive factors in procurement, bolstering demand for vendors demonstrating encryption and secure data flows. In Latin America, agricultural modernization programs and company-led financing initiatives support the adoption of aerial application, tied to broader productivity goals and rural service networks. These region-specific factors shape adoption patterns, with policy readiness and sector priorities determining where the drones market can scale fastest.

- SZ DJI Technology Co., Ltd.

- Parrot Drones SAS

- AeroVironment, Inc.

- Skydio, Inc.

- Wisk Aero LLC (The Boeing Company)

- Yuneec (ATL Drone)

- Terra Drone Corporation

- Delair SAS

- Autel Robotics Co., Ltd.

- EHang Holdings Limited

- EagleNXT

- Garuda Aerospace Pvt. Ltd.

- Guangzhou XAG Co., Ltd.

- ideaForge Technology Limited

- Aerosense Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing investment and venture funding in drone startups

- 4.2.2 Expansion of DIAB and fully autonomous operational models

- 4.2.3 Progressive BVLOS and U-space/UTM regulatory advancements

- 4.2.4 Scaling of precision agriculture and rural drone service networks

- 4.2.5 Integration of drones with enterprise digital-twin and AI ecosystems

- 4.2.6 Rapid maturation of battery, hybrid, and fast charging technologies

- 4.3 Market Restraints

- 4.3.1 Li-ion cell supply crunch inflating small-drone BOM costs

- 4.3.2 Government policies and airspace regulations hampering the usage of drones

- 4.3.3 Privacy-by-design rules in the EU slowing urban adoption

- 4.3.4 Operational integration complexity and ambiguous ROI in some use cases

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Construction

- 5.1.2 Agriculture

- 5.1.3 Energy

- 5.1.4 Entertainment

- 5.1.5 Law Enforcement

- 5.1.6 Other Applications

- 5.2 By Type

- 5.2.1 Fixed-Wing Drones

- 5.2.2 Rotary-Wing Drones

- 5.2.3 Hybrid/VTOL Drones

- 5.3 By Weight Class

- 5.3.1 Nano/Micro (Less than 2 kg)

- 5.3.2 Small (2 to 25 kg)

- 5.3.3 Medium (25 to 150 kg)

- 5.3.4 Large (Greater than 150 kg)

- 5.4 By Mode of Operation

- 5.4.1 Remotely Piloted

- 5.4.2 Optionally Piloted

- 5.4.3 Fully Autonomous

- 5.5 By End User

- 5.5.1 Commercial and Consumer

- 5.5.2 Government and Civil

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share Analysis

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 SZ DJI Technology Co., Ltd.

- 6.3.2 Parrot Drones SAS

- 6.3.3 AeroVironment, Inc.

- 6.3.4 Skydio, Inc.

- 6.3.5 Wisk Aero LLC (The Boeing Company)

- 6.3.6 Yuneec (ATL Drone)

- 6.3.7 Terra Drone Corporation

- 6.3.8 Delair SAS

- 6.3.9 Autel Robotics Co., Ltd.

- 6.3.10 EHang Holdings Limited

- 6.3.11 EagleNXT

- 6.3.12 Garuda Aerospace Pvt. Ltd.

- 6.3.13 Guangzhou XAG Co., Ltd.

- 6.3.14 ideaForge Technology Limited

- 6.3.15 Aerosense Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment