|

시장보고서

상품코드

2066536

기판형 PCB : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Substrate-Like Printed Circuit Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

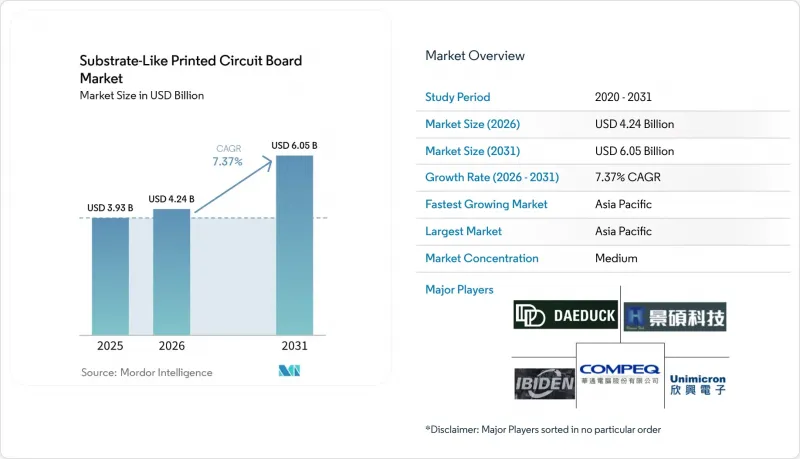

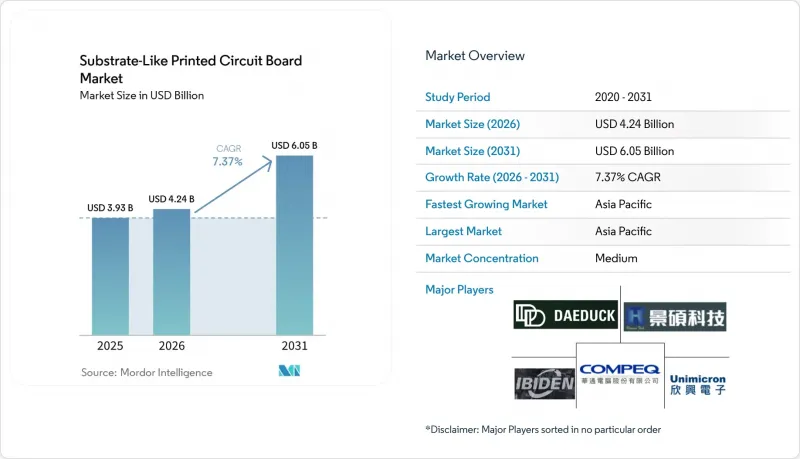

Mordor Intelligence에 의하면, 2026년 기판형 PCB 시장 규모는 42억 4,000만 달러에 달할 것으로 예상됩니다. 2025년 39억 3,000만 달러에서 확대해, 2026년부터 2031년에 걸쳐 CAGR 7.37%로 성장하여 60억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 기판 소재(유리 에폭시 FR-4, 고속·저손실, 폴리이미드 등), 최종 사용자 산업(소비자용 전자기기, 컴퓨팅 및 데이터센터, 통신 및 5G, 자동차 및 전기자동차, 헬스케어/의료, 항공우주 및 방위 등), 지역(북미, 유럽 등)별로 세분화되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 기판형 PCB 시장 동향 및 인사이트

고밀도 상호 연결에 대한 스마트폰 OEM 제조업체 수요 급증

각 스마트폰 제조업체들은 애플리케이션 프로세서, RF 프런트엔드 및 전원 관리 IC를 단일 기판형 PCB(SLP) 위에 집적함으로써, 기존의 다층 설계에 비해 면적을 30% 줄였습니다. 대만의 제조업체에 따르면, 2025년에는 SLP 매출의 35% 이상을 모바일 애플리케이션가 차지할 것으로 예상되며, 비아 직경이 50µm 미만인 20µm 미만 라인에 대한 수요가 증가하고 있음이 두드러지게 나타나고 있습니다. 더 많은 공장이 이 미세 구조 제조 기술을 습득함에 따라, 수율이 결정적인 차별화 요소로 부상하고 있으며, 공급업체들은 고정밀 레이저 직접 노광 기술과 패턴 전사 편차를 조기에 감지하는 예측 분석을 결합해야 하는 압박을 받고 있습니다.

5G 통신 모듈 수요 증가

mm파 주파수 대역에서 작동하는 독립형 5G 네트워크의 경우, 30GHz에서 0.5 dB-in.의 삽입 손실 상한이 적용되지만, FR-4는 실용적인 두께에서는 이 요건을 충족할 수 없습니다. 따라서 기지국 OEM 제조업체들은 고속 PTFE 및 액정 폴리머 적층 기판을 지정하고 있으며, 이로 인해 층 수가 8층을 초과함에 따라 결함 발생률을 50 PPM 이하로 억제하기 위한 자동 광학 검사(AOI)에 대한 기판형 PCB(SLP) 시장의 설비 투자가 촉진되고 있습니다. 휴대폰 제조업체들도 비슷한 추세를 보이고 있으며, 듀얼 밴드 지원 단말기의 경우 고밀도로 집적된 SLP 모듈 위에 여러 개의 전력 증폭기와 안테나 튜너가 집적됨에 따라, 단말기 1대당 소재 매출액이 증가하고 있습니다.

SLP 생산 라인의 막대한 설비 투자

25µm 라인을 지원할 수 있는 신규 공장의 경우, 레이저 직접 노광, 순차 적층 및 인라인 X선 검사 클러스터 도입에 1억 5,000만-3억 달러가 필요합니다. 가동률이 80%를 넘지 않는 한 투자 회수에 5년 이상이 소요되므로, 신규 진입을 가로막고 통신, 민생, 자동차 분야의 계약을 통해 자산을 상각하는 기존 기업을 중심으로 기판형 PCB 시장이 재편되고 있습니다.

부문별 분석

2025년에는 고속·저손실 라미네이트가 기판형 PCB 시장의 40.94% 점유율을 차지했으며, 2031년까지 연평균 성장률(CAGR) 7.64%로 확대될 것으로 전망됩니다. 이는 5G 무선 헤드 및 400-GbE 스위치 패브릭에서 PTFE, 액정 고분자, 탄화수소 세라믹 계열 소재가 유리 에폭시를 대체하기 때문입니다. 배선 길이가 단축되더라도 10GHz에서의 삽입 손실은 0.5 dB-in. 미만으로 억제되어, 이를 통해 스펙트럼 효율을 향상시킬 수 있으며, 이는 캐리어 용량 증가로 직접 이어집니다. 유리 에폭시 FR-4는 원료 시트의 비용이 PTFE 복합재료의 3분의 1 수준이기 때문에 중저가 스마트폰이나 산업용 제어 기기에서는 여전히 주류를 이루고 있습니다. 그러나 휴대전화 제조업체들이 적층 카메라 어레이의 공차 기준을 더욱 엄격하게 적용함에 따라, 기판형 PCB 시장에서의 그 규모는 축소되기 시작하고 있습니다.

고속 소재는 데이터센터의 가속기 보드에도 널리 사용되고 있으며, 이곳에서는 112 Gbps의 PAM4 신호 전송을 통해 아이 다이어그램의 클로즈 감도가 향상되었습니다. 각 공급업체들은 유전율을 저하시키지 않으면서 유리전이온도를 높이기 위해 ABF 수지에 탄화수소계 세라믹를 배합하기 시작했습니다. 폴리이미드는 자동차 및 항공 전자 기기의 플렉스-리지드 구조 분야에서 틈새 시장을 차지하고 있지만, 레이저 드릴링에 소요되는 시간과 화학 약품 취급으로 인해 공정 비용이 증가하기 때문에 시장 점유율은 10% 미만에 그치고 있습니다. 열유속이 10 W cm?²를 초과하는 경우, 소켓 수준의 전력 전자 분야에서는 금속 코어 및 세라믹 충전 구조가 채택되고 있습니다. 이는 높은 이익률을 가져다주지만 생산량은 적은 마이크로 부문입니다.

지역별 분석

2025년, 아시아태평양은 기판형 PCB 시장 매출의 83.64%를 차지했으며, 대만, 중국, 한국, 일본이 이를 주도했습니다. 대만에서는 2024년 3분기에 205억 달러 규모의 PCB 생산액을 기록했습니다. 이는 빌드업 적층판 공급업체, 레이저 장비 제조업체, 그리고 며칠 만에 시제품을 제작할 수 있는 설계 회사로 구성된 생태계를 반영한 것입니다. 중국 본토는 지정학적으로 불안정한 수입에 의존하지 않도록 국내 생산 능력 확충을 추진하고 있으며, 심난 서킷(Shennan Circuits)은 국가 보조금(SCC)을 지원받아 ABF 생산 라인을 확장하고 있습니다. 한국의 재벌들은 자동차 업계의 인증을 받은 수직 통합형 사업을 활용해 전기자동차 모듈 시장에 진출하고 있는 반면, 일본은 초박형 유리 코어 분야의 공정 기술 리더십을 유지하고 있습니다. 5G의 밀집화, 클라우드 데이터센터 건설, 그리고 전기자동차 배터리 팩의 현지 생산을 원동력으로 삼아, 2031년까지 해당 지역 전체의 성장률은 8.77%를 나타낼 것으로 전망됩니다.

북미와 유럽을 합쳐도 시장 점유율은 15% 미만에 그치고 있으며, 높은 인건비와 원자재 공급망의 취약성이 제약 요인으로 작용하고 있습니다. 2022년 ‘CHIPS and Science Act’에서는 반도체 분야에 390억 달러가 배정되었으나, 기판 제조 시설은 투자 세액 공제 대상에서 제외됨에 따라 단기적인 리쇼어링의 기세가 주춤하고 있습니다. 2026년, 뉴욕과 오스트리아 등에서 진행 중인 몇 건의 그린필드형 시범 프로젝트는 여전히 입지 선정 단계에 있습니다. 세계 기타 지역에서 수요는 주로 동남아시아의 가전제품 최종 조립 및 멕시코의 자동차용 케이블 하네스 공장에서 발생하고 있지만, 현지 기판 생산 능력은 극히 미미하기 때문에 대만과 한국에서의 수입이 주를 이루고 있습니다.

지정학적 리스크로 인해 다국적 OEM 기업들은 듀얼 소싱으로 방향을 전환하고 있습니다. 유니마이크론의 태국 공장은 2025년에 양산을 시작하여, 동남아시아국가연합(ASEAN) 시장에 관세 없이 진출할 수 있는 기회를 제공하는 동시에, 대만 해협을 둘러싼 리스크에 대한 의존도를 낮추고 있습니다. 대만 지진으로 인한 공급 차질을 우려하는 유럽의 자동차 제조업체들은 800V 배터리 팩용 기판형 PCB(SLPCB) 시장의 지속성을 확보하기 위해 한국 및 일본공급업체들과 다년간의 조달 협정을 체결했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the substrate-Like printed circuit board market size in 2026 is estimated at USD 4.24 billion, growing from 2025 value of USD 3.93 billion with projections showing USD 6.05 billion, growing at 7.37% CAGR over 2026-2031.

This report is Segmented by Substrate Material (Glass Epoxy FR-4, High-Speed/Low-Loss, Polyimide, and More), End-User Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Healthcare / Medical, Aerospace and Defense, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Substrate-Like Printed Circuit Board Market Trends and Insights

Surging Smartphone OEM Demand for High-Density Interconnects

Smartphone brands have consolidated application processors, RF front ends, and power-management ICs onto single Substrate-Like PCB market boards, cutting occupied area by 30% relative to conventional multilayer designs. Taiwanese fabricators disclosed that mobile use accounted for over 35% of SLP revenue in 2025, underscoring the volume pull for sub-20 µm lines with via diameters below 50 µm. Yield has become the decisive differentiator as more plants master the geometry, pushing suppliers to couple high-accuracy laser direct imaging with predictive analytics that spot pattern-transfer deviations early.

Rising Demand for 5G Communication Modules

Standalone 5G networks operating at millimeter-wave frequencies impose insertion-loss ceilings of 0.5 dB-in. at 30 GHz that FR-4 can meet only at impractical thicknesses. Base-station OEMs therefore specify high-speed PTFE or liquid-crystal polymer stacks, lifting layer counts beyond eight and driving Substrate-Like PCB market capital spending on automated optical inspection to hold defect escape below 50 PPM. Handset makers mirror the trend; dual-band phones integrate multiple power amplifiers and antenna tuners on densified SLP modules, boosting material revenue per device.

High CAPEX for SLP Production Lines

Greenfield plants capable of 25 µm lines demand USD 150-300 million for laser direct-imaging, sequential lamination and inline X-ray inspection clusters. Payback stretches beyond five years unless utilizations exceed 80%, which deters newcomers and consolidates the Substrate-Like PCB market around incumbents that amortize assets across telecom, consumer and automotive contracts.

Other drivers and restraints analyzed in the detailed report include:

- Automotive ADAS and EV Electronics Escalating Complexity

- Flip-Chip on SLP Enabling Heterogeneous Integration

- Supply Risk of ABF Resin Due to Limited Vendors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-speed and low-loss laminates captured 40.94% of substrate-like printed circuit board market share in 2025, expanding at a 7.64% CAGR through 2031 as PTFE, liquid-crystal polymer, and hydrocarbon-ceramic systems replace glass-epoxy in 5G radio heads and 400-GbE switch fabrics. Insertion loss stays under 0.5 dB-in. at 10 GHz, even as routing lengths shrink, enabling spectral efficiency gains that directly convert into carrier capacity. Glass-epoxy FR-4 still prevails in mid-range smartphones and industrial controls because its raw sheet cost is one-third that of PTFE composites. However, its Substrate-Like PCB market size has begun to taper as handset OEMs chase tighter tolerances for stacked camera arrays.

High-speed materials also spread to data-center accelerator boards, where 112 Gbps PAM4 signaling raises eye-diagram closure sensitivity. Suppliers have started blending hydrocarbon ceramics into ABF resin to lift the glass-transition temperature without sacrificing the dielectric constant. Polyimide retains a niche for flex-rigid builds in automotive and avionics, but share stays below 10% because laser-drilling time and chemistry handling raise process cost. Metal-core and ceramic-filled builds win socket-level power electronics when heat flux exceeds 10 W cm-2, a micro-segment that offers high margins but modest volume.

Geography Analysis

Asia-Pacific accounted for 83.64% of the Substrate-Like Printed Circuit Board market revenue in 2025, led by Taiwan, China, South Korea, and Japan. Taiwan recorded USD 20.5 billion PCB output in Q3-2024, reflecting an ecosystem of build-up laminate suppliers, laser-equipment firms, and design houses that can prototype within days. Mainland China advances domestic capacity to escape geopolitically fraught imports, with Shennan Circuits expanding ABF lines under state subsidies SCC. South Korea's conglomerates leverage auto-qualified verticals to enter the EV module market, while Japan maintains process leadership in ultra-thin glass cores. Overall regional growth is projected at 8.77% through 2031, fueled by 5G densification, cloud data-center builds, and EV battery-pack localization

North America and Europe together hold under 15% of the market, constrained by higher labor costs and a thinner material supply chain. The 2022 CHIPS and Science Act earmarked USD 39 billion for semiconductors but excluded substrate facilities from investment tax credits, muting near-term reshoring momentum. A few greenfield pilots, including one in New York and another in Austria, remain in site-selection stages as of early 2026. Rest-of-world demand arises mainly from consumer-electronics final assembly in Southeast Asia and automotive cable-harness plants in Mexico, yet local substrate capacity is negligible, so imports from Taiwan and South Korea dominate.

Geopolitical risk is steering multinational OEMs toward dual-sourcing. Unimicron's plant in Thailand entered mass production in 2025, offering duty-free access to Association of Southeast Asian Nations markets while dampening cross-strait exposure. European automakers, wary of Taiwanese earthquake disruptions, have entered multi-year sourcing pacts with Korean and Japanese suppliers to secure Substrate-Like Printed Circuit Board market continuity for 800-V battery packs.

- Kinsus Interconnect Technology Corp

- Ibiden Co., Ltd.

- Compeq Manufacturing Co., Ltd.

- Daeduck Electronics Co., Ltd.

- Unimicron Technology Corp.

- Zhen Ding Technology Holding

- TTM Technologies

- Meiko Electronics Co., Ltd.

- AT&S AG

- Korea Circuit Co., Ltd.

- LG Innotek Co., Ltd.

- Samsung Electro-Mechanics

- Shennan Circuits Co., Ltd.

- Tripod Technology

- Fujitsu Interconnect

- Wus Printed Circuit

- HannStar Board Corp.

- Nippon Mektron Ltd.

- NCAB Group AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ultra-Thin Glass Core Adoption for Optical Integration

- 4.2.2 On-Device Generative AI Raising SLP Layer Counts

- 4.2.3 In-Package RF Front-End Convergence (SiP + SLP)

- 4.2.4 Battery-Free Wearables Using Energy-Harvest SLP Boards

- 4.2.5 Government Chiplets Grants for Advanced Substrates

- 4.2.6 Rapid Build-Up Film Capacity Expansion in Vietnam

- 4.3 Market Restraints

- 4.3.1 ABF Resin Oligopoly Driving Price Volatility

- 4.3.2 Yield Losses from mSAP Copper Over-Etch Below 20 µm

- 4.3.3 Scarcity of Skilled mSAP Process Engineers

- 4.3.4 Carbon-Footprint Regulations on High-Energy Plasma Desmear

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Substrate Material

- 5.1.1 Glass Epoxy (FR-4)

- 5.1.2 High-Speed / Low-Loss

- 5.1.3 Polyimide (PI)

- 5.1.4 Other Substrate Materials

- 5.2 By End-user Industry

- 5.2.1 Consumer Electronics

- 5.2.2 Computing and Data Centers

- 5.2.3 Telecommunications and 5G

- 5.2.4 Automotive and EV

- 5.2.5 Healthcare / Medical

- 5.2.6 Aerospace and Defense

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Netherlands

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Taiwan

- 5.3.3.3 Japan

- 5.3.3.4 India

- 5.3.3.5 South Korea

- 5.3.3.6 Southeast Asia

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 Rest of World

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Kinsus Interconnect Technology Corp

- 6.4.2 Ibiden Co., Ltd.

- 6.4.3 Compeq Manufacturing Co., Ltd.

- 6.4.4 Daeduck Electronics Co., Ltd.

- 6.4.5 Unimicron Technology Corp.

- 6.4.6 Zhen Ding Technology Holding

- 6.4.7 TTM Technologies

- 6.4.8 Meiko Electronics Co., Ltd.

- 6.4.9 AT&S AG

- 6.4.10 Korea Circuit Co., Ltd.

- 6.4.11 LG Innotek Co., Ltd.

- 6.4.12 Samsung Electro-Mechanics

- 6.4.13 Shennan Circuits Co., Ltd.

- 6.4.14 Tripod Technology

- 6.4.15 Fujitsu Interconnect

- 6.4.16 Wus Printed Circuit

- 6.4.17 HannStar Board Corp.

- 6.4.18 Nippon Mektron Ltd.

- 6.4.19 NCAB Group AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment