|

시장보고서

상품코드

2066596

중국의 SSD 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)China Solid-State Drive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

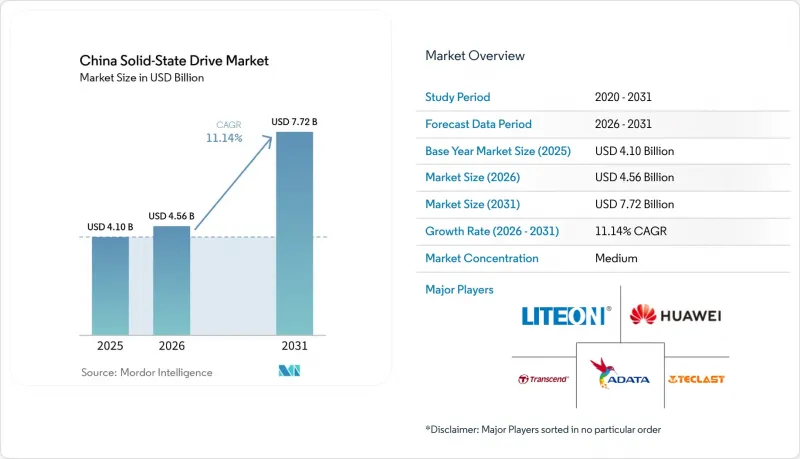

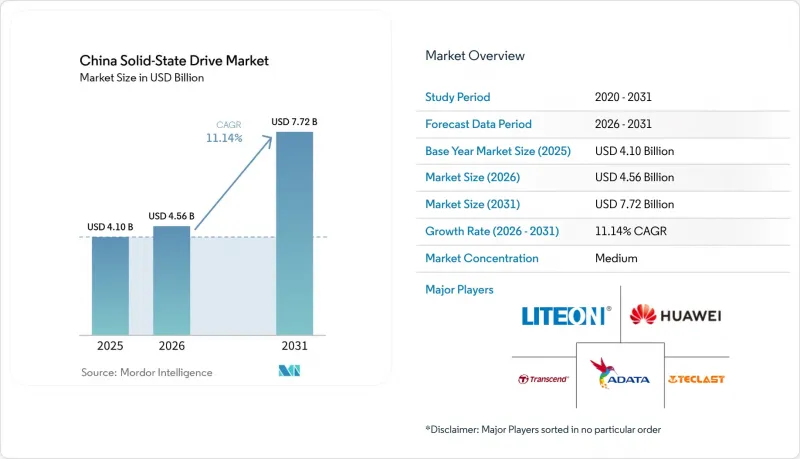

Mordor Intelligence에 의하면, 중국 SSD 시장 규모는 2025년 41억 달러에서 2026년에는 45억 6,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 11.14%로 성장을 지속하여, 2031년에는 77억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 인터페이스(시리얼 ATA(SATA), PCI Express(PCIe/NVMe) 등), 폼 팩터(2.5인치 드라이브, M.2 모듈 등), NAND 기술(SLC/MLC, TLC 등), 용도(엔터프라이즈, 클라이언트), 최종 사용 산업(클라우드 서비스 제공업체, 하이퍼스케일 및 코로케이션 데이터센터 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국 SSD 시장 동향과 인사이트

AI 워크로드를 위한 데이터센터 확장

중국의 AI 컴퓨팅 처리 능력은 2025년까지 300 엑사플롭스를 넘어설 것으로 예상되며, 이에 따라 모델 훈련 서버의 SSD 용량 요구 사항은 현재의 30 TB에서 10년 말까지 100 TB로 증가할 것으로 전망됩니다. Solidigm의 QLC 장치를 기반으로 하는 Kingsoft Cloud의 ‘KS3 Extreme Speed’ 도입 환경은 이미 1페타바이트당 1Tbps의 처리 속도를 유지하고 있으며, 이는 동급 HDD 어레이에 비해 100배 더 빠릅니다. 추론 워크로드는 더욱 빠르게 증가하고 있으며, 스토리지 수요는 2030년까지 447 엑사바이트에 달할 것으로 예측됩니다. 각 클라우드 제공업체들은 수출 규제 하에서도 안정적인 공급을 확보하기 위해, 국내에서 패키지화된 PCIe 5.0 NVMe SSD로의 전환을 추진하고 있습니다. 그 결과, 중국의 SSD 시장은 AI 서버 1랙이 증설될 때마다 판매량이 직접적으로 증가하는 혜택을 누리고 있습니다.

소비자용 기기에서 HDD에서 SSD로의 전환

컨텐츠 제작 업무량이 4K 및 8K 형식으로 전환됨에 따라, SSD가 탑재된 노트북 및 데스크톱 PC의 소비자 채택이 가속화되고 있습니다. 삼성의 시안 공장은 2024년에 가동률이 70%까지 회복되면서, 스마트폰 OEM 제조업체를 위한 현지 NAND 공급이 안정화되었습니다. 일본 제조업체인 UNIS는 현재 전송 속도 14.9 GB/s의 PCIe 5.0 드라이브를 출하하고 있으며, 해외 제품과의 성능 격차를 줄이는 동시에 판매 파트너에게 비용 면에서 이점을 제공합니다. 팬데믹 기간 동안 PC 시장의 침체로 인해 소매 가격은 억제되었으나, 생산 일정 관리가 순조롭게 진행되고 있어 2025년 하반기에는 시장 상황이 호전될 것으로 예상되며, 중국 SSD 시장의 소비자 채널은 지속적인 성장이 전망됩니다.

NAND 가격 사이클의 변동

2024년에는 노트북 수요가 부진한 데다 키오크시아와 웨스턴디지털의 팹 가동률이 높은 수준을 유지하면서, 현물 가격이 급격히 변동했습니다. 중국의 2선 SSD 브랜드들은 이익률 압박에 직면하면서 컨트롤러 업그레이드를 연기하고, 판촉 예산을 축소할 수밖에 없게 되었습니다. YMTC와의 선물 계약이 헤지 수단으로 부상하고 있지만, 재고 불일치 문제가 여전히 중국 SSD 시장 전체의 단기 판매량을 저해할 가능성이 있습니다.

부문별 분석

2025년, 중국 SSD 시장 규모 중 PCIe/NVMe 장치가 61.35%를 차지하며, 저지연 처리량이 필요한 AI 클러스터에 힘입어 연평균 성장률(CAGR) 14.32%의 속도로 확대되고 있습니다. 기업 사용자들은 트랜스포머 모델의 학습 시간을 단축하기 위해 PCIe 4.0 및 5.0 레인을 선호하고 있으며, 이로 인해 국내 공급업체의 평균 판매 가격(ASP)이 상승하고 있습니다. SATA는 보급형 노트북 시장에서 일정한 점유율을 유지하고 있지만, 소비자들이 PCIe 기반 노트북으로 전환함에 따라 그 점유율은 분기마다 감소하고 있습니다. SAS는 순수한 속도보다는 듀얼 포트의 신뢰성이 더 중요시되는 기존의 미션 크리티컬 어레이에서 여전히 채택되고 있습니다. 따라서 인터페이스 업그레이드는 중국 SSD 시장에서 제품 차별화의 핵심 요소로 자리 잡고 있습니다.

Innogrit 및 Maxio의 2세대 PCIe 5.0 컨트롤러에는 드라이브 내 AI 캐싱을 위한 코프로세싱 블록이 추가되었습니다. ODM 업체들이 클라우드 규모로 이러한 칩의 인증을 추진함에 따라, 중국의 SSD 업계는 전력 소비 제약을 감수하지 않으면서도 새로운 성능 수준을 개척하고 있습니다. PCIe 6.0 로드맵에 따르면 두 자릿수의 효율 향상이 예상되며, 이는 데이터센터의 배출량을 억제하겠다는 국가 목표와 부합합니다. 이러한 발전은 스토리지 밸류체인을 한 단계 끌어올리는 동시에, 국산 IP 블록의 수출 가능성을 확대하려는 중국의 야망을 뒷받침하고 있습니다.

2025년, M.2 모듈은 중국 SSD 시장 점유율의 47.20%를 차지하며, 슬림하고 가벼운 설계를 추구하는 각 OEM 업체들로부터 지지를 받았습니다. 그러나 각 하이퍼스케일러 기업들이 AI 랙의 유지보수성과 기류를 우선시함에 따라, U.2/E1.S 카테고리는 2031년까지 연평균 15.55%의 성장률을 보일 것으로 전망됩니다. E1.S 드라이브는 25W의 전력 소비 한도를 지원하며, PCIe 5.0 환경에서 발생하는 열로 인한 성능 저하를 완화합니다. 또한, 핫스왑 기능이 제공하는 편의성 덕분에 클라우드 SLA의 중요한 지표인 장애 복구가 신속해집니다.

알리바바의 장베이 캠퍼스에서는 2.5인치 베이를 EDSFF 트레이로 전환하는 작업이 진행 중이며, 이는 기존 시설(브라운필드)에서의 전환 경로를 시사하고 있습니다. 한편, 애드인 카드형 SSD는 대역폭 포화가 밀도 문제를 상회하는 특수한 가속기 노드에서 틈새 시장을 유지하고 있습니다. 전반적으로 볼 때, 이러한 폼 팩터의 전환은 랙 수준의 설계 선택이 중국 SSD 시장의 전체 공급망에 파급되는 양상을 여실히 보여주고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the china solid-state drive market size is expected to grow from USD 4.10 billion in 2025 to USD 4.56 billion in 2026 and is forecast to reach USD 7.72 billion by 2031 at 11.14% CAGR over 2026-2031.

This report is Segmented by Interface (Serial ATA (SATA), PCI Express (PCIe/NVMe) and More), Form Factor (2. 5-Inch Drives. M. 2 Modules, and More), NAND Technology (SLC / MLC, TLC, and More), Application (Enterprise, Client), End-User Industry (Cloud Service Providers, Hyperscale and Colocation Data Centres, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Solid-State Drive Market Trends and Insights

Data-centre Expansion for AI Workloads

China's AI computing footprint is on track to exceed 300 exaflops by 2025, lifting SSD capacity requirements for model training servers from 30 TB today to 100 TB by decade-end. Kingsoft Cloud's KS3 Extreme Speed deployment, built on Solidigm QLC devices, already sustains 1 Tbps per petabyte-100X faster than comparable HDD arrays. Inference workloads are expanding even faster, with storage demand forecast to reach 447 exabytes by 2030. Cloud providers are switching to domestically packaged PCIe 5.0 NVMe SSDs to secure supply amid export controls. As a result, the China solid-state drive market enjoys a direct volume lift from every incremental rack of AI servers commissioned.

Shift from HDD to SSD in Consumer Devices

Consumer adoption of SSD-equipped laptops and desktops is accelerating as content-creation workloads move to 4K and 8K formats. Samsung's Xi'an plant rebounded to 70% utilization in 2024, stabilizing local NAND supply for smartphone OEMs. Domestic player UNIS now ships PCIe 5.0 drives at 14.9 GB/s, narrowing the performance gap with international alternatives while offering cost relief to channel partners. Though pandemic-era PC weakness tempered retail pricing, controlled production schedules signal firmer conditions in late 2025, sustaining the China solid-state drive market's consumer channel.

NAND Price-cycle Volatility

Spot prices swung sharply in 2024 as weak laptop demand met elevated fab utilization at Kioxia and Western Digital. Chinese tier-2 SSD brands faced squeezed margins, delaying controller upgrades and tightening promotional budgets. Forward contracts with YMTC are emerging as a hedge, but inventory misalignment can still hinder near-term sell-in volumes across the China solid-state drive market.

Other drivers and restraints analyzed in the detailed report include:

- East-Data-West-Compute" Government Build-out

- Localization of NAND Supply Chain

- Export-control Limits on Advanced Tools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PCIe/NVMe devices accounted for 61.35% of the China solid-state drive market size in 2025 and are on pace for a 14.32% CAGR, propelled by AI clusters that demand low-latency throughput. Enterprise buyers favour PCIe 4.0 and 5.0 lanes to cut training time on transformer models, lifting blended ASPs for domestic suppliers. SATA maintains a toehold in entry-level notebooks, but its share slides each quarter as consumers migrate to PCIe-based laptops. SAS continues in legacy mission-critical arrays where dual-port reliability trumps raw speed. Interface upgrades therefore remain a centerpiece of product differentiation across the China solid-state drive market.

Second-generation PCIe 5.0 controllers from Innogrit and Maxio add co-processing blocks for on-drive AI caching. As ODMs qualify these chips at cloud scale, the China solid-state drive industry unlocks fresh performance tiers without sacrificing power budgets. PCIe 6.0 roadmaps promise double-digit efficiency gains, aligning with the national goal of curbing data-center emissions. These advances reinforce China's ambition to climb the storage value chain while enlarging export potential for indigenous IP blocks.

M.2 modules held 47.20% of the China solid-state drive market share in 2025, favoured by OEMs for thin-and-light designs. Yet the U.2/E1.S category is forecast to grow 15.55% annually through 2031 as hyperscalers prioritize serviceability and airflow in AI racks. E1.S drives support 25 W envelopes, easing thermal throttling in PCIe 5.0 deployments. Their hot-swap convenience accelerates failure recovery, a key metric in cloud SLAs.

Converters from 2.5-inch bays to EDSFF trays are underway at Alibaba's Zhangbei campus, signalling a migration path for brownfield sites. Meanwhile, add-in-card SSDs retain a niche in specialized accelerator nodes where bandwidth saturation overrides density concerns. Collectively, the form-factor shift exemplifies how rack-level design choices ripple across the China solid-state drive market supply chain.

List of Companies Covered in this Report:

- Samsung Electronics Co., Ltd.

- Yangtze Memory Technologies Co., Ltd. (YMTC)

- Western Digital Corporation

- Kingston Technology Company, Inc.

- SK Hynix Inc.

- Huawei Technologies Co., Ltd.

- ADATA Technology Co., Ltd.

- Transcend Information Inc.

- Lenovo Group Limited

- Memblaze Technology Co., Ltd.

- Shenzhen Longsys Electronics Co., Ltd.

- Dapu Microelectronics Co., Ltd.

- Kimtigo Technology Co., Ltd.

- BIWIN Storage Technology Co., Ltd.

- Kioxia Holdings Corporation

- Micron Technology Inc.

- Intel Corporation (Solidigm)

- Seagate Technology Holdings plc

- LITE-ON Technology Corporation

- Maxiotek Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Data-centre expansion for AI workloads

- 4.2.2 Shift from HDD to SSD in consumer devices

- 4.2.3 East-Data-West-Compute government build-out

- 4.2.4 Localization of NAND supply chain

- 4.2.5 Edge and in-storage processing for IIoT

- 4.3 Market Restraints

- 4.3.1 NAND price-cycle volatility

- 4.3.2 Export-control limits on advanced tools

- 4.3.3 Power-supply caps for hyperscale DCs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Interface

- 5.1.1 Serial ATA (SATA)

- 5.1.2 PCI Express (PCIe/NVMe)

- 5.1.3 Serial-Attached SCSI (SAS)

- 5.1.4 USB/Other Embedded

- 5.2 By Form Factor

- 5.2.1 2.5-inch Drives

- 5.2.2 M.2 Modules

- 5.2.3 U.2 / E1.S

- 5.2.4 Add-in Cards

- 5.3 By NAND Technology

- 5.3.1 SLC / MLC

- 5.3.2 TLC

- 5.3.3 QLC

- 5.3.4 PLC (Prototype)

- 5.4 By Application

- 5.4.1 Enterprise

- 5.4.2 Client

- 5.5 By End-User Industry

- 5.5.1 Cloud Service Providers

- 5.5.2 Hyperscale & Colocation Data Centres

- 5.5.3 Consumer Electronics OEMs

- 5.5.4 Industrial & Manufacturing

- 5.5.5 Automotive & Transportation

- 5.5.6 Aerospace & Defence

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Yangtze Memory Technologies Co., Ltd. (YMTC)

- 6.4.3 Western Digital Corporation

- 6.4.4 Kingston Technology Company, Inc.

- 6.4.5 SK Hynix Inc.

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 ADATA Technology Co., Ltd.

- 6.4.8 Transcend Information Inc.

- 6.4.9 Lenovo Group Limited

- 6.4.10 Memblaze Technology Co., Ltd.

- 6.4.11 Shenzhen Longsys Electronics Co., Ltd.

- 6.4.12 Dapu Microelectronics Co., Ltd.

- 6.4.13 Kimtigo Technology Co., Ltd.

- 6.4.14 BIWIN Storage Technology Co., Ltd.

- 6.4.15 Kioxia Holdings Corporation

- 6.4.16 Micron Technology Inc.

- 6.4.17 Intel Corporation (Solidigm)

- 6.4.18 Seagate Technology Holdings plc

- 6.4.19 LITE-ON Technology Corporation

- 6.4.20 Maxiotek Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis