|

시장보고서

상품코드

2066656

북미의 납축전지 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America Lead Acid Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

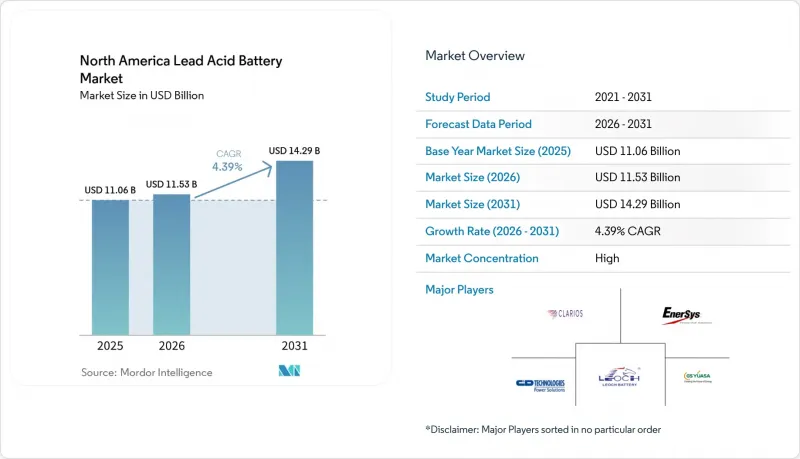

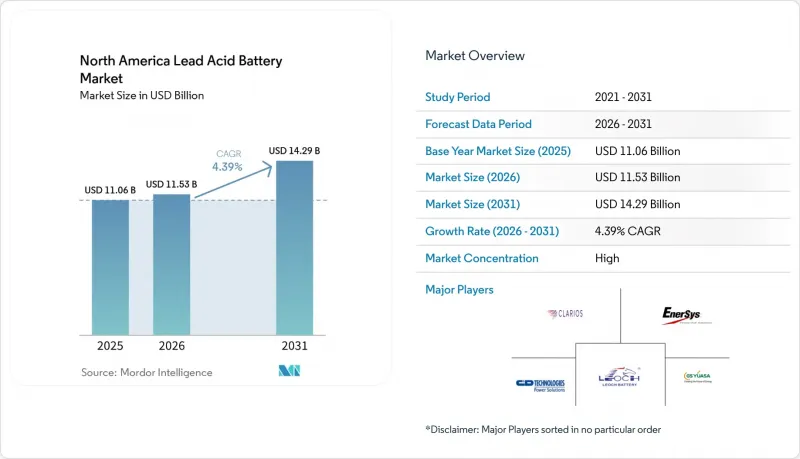

Mordor Intelligence에 의하면, 북미 납축전지 시장 규모는 2025년 110억 6,000만 달러에서 2026년에는 115억 3,000만 달러로 확대되어 2031년까지 142억 9,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 4.39%로 성장할 전망입니다.

본 보고서는 구조 방식(액체식, VRLA), 용도(시동·조명·점화(SLI), 고정형, 동력·견인용(지게차, 골프 카트), 휴대용, 기타) 및 지역(미국, 캐나다, 멕시코)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미 납축전지 시장 동향과 인사이트

노후화된 내연기관(ICE) 차량을 차량군에서 교체해야 할 필요성

미국 차량의 평균 사용 연수가 사상 최고치인 12.6년에 달하면서, 구조적인 교체 수요의 물결을 뒷받침하고 있습니다. 이는 11년 이상 경과한 차량의 배터리 교체율이 연간 37%에 달하기 때문입니다. 배터리 카운슬 인터내셔널(BCI)의 조사에 따르면, 2024년 납축전지 출하량은 1억 5,900만 개에 달했으나, 그 대부분은 공장 출고 시 기본 장착분이 아닌 교체 수요에 의한 것이었습니다. 스타트-스톱 기술 및 주행 보조 기능으로 인한 전력 부하 증가로 인해, 액체형 배터리에서 흡수 유리 매트(AGM)형 VRLA 설계로의 전환이 가속화되고 있으며, S&P;Global은 2027년까지 애프터마켓에 설치된 전체 대수의 19%를 나타낼 것으로 예측했습니다. O'Reilly Auto Parts사는 East Penn사를 2025년도 ‘올해공급업체’로 선정했습니다. 이는 해당 공급업체가 가동 중인 차량의 40% 이상을 커버할 수 있는 DIN 규격 AGM 배터리의 생산 규모를 확대한 점이 높이 평가받았기 때문입니다. 중요한 점은 내연기관 차량을 더 오랫동안 보유하는 지방이나 저소득층 구매자들이 전기차에 의한 시장 잠식을 늦추고, 북미 납축전지 시장의 수명을 연장하고 있다는 것입니다.

데이터센터 및 통신 분야의 UPS 확대 열풍

인공지능(AI) 워크로드를 처리하기 위한 하이퍼스케일 인프라 구축으로 인해, 전 세계 데이터센터의 전력 수요는 2022년 460 TWh에서 2030년까지 945 TWh로 증가할 것으로 전망됩니다. 2025년 시점에서도 VRLA 배터리, 특히 AGM 유형은 43억 3,000만 달러 규모의 세계 UPS 배터리 시장에서 여전히 58%의 점유율을 차지하고 있었습니다. 2024년 텍사스주 상원 법안 제6호(SB 6)에서는 현장 백업이 의무화되어 있으며, 이로 인해 기존 시설의 개보수에 따른 구매가 촉진되고 있습니다. 반면, 신규 프로젝트에서는 고밀도화의 장점 때문에 리튬 이온 배터리가 선택되고 있습니다. 마찬가지로, 5G 기지국 구축에 있어서도 외딴 지역에서는 밀폐형 무정비 VRLA 배터리가 채택되어, 유지보수 방문 횟수를 줄이고 있습니다. 리튬 이온 배터리는 10년간의 총 소유 비용(TCO)이 39% 더 낮지만, 설비 투자 예산과 확립된 재활용 채널 덕분에 VRLA 배터리는 방대한 도입 규모에서 여전히 중요한 위치를 차지하고 있습니다.

리튬 이온 배터리 팩의 급격한 원가 하락

미국 에너지부(DOE)의 자료에 따르면, 리튬 이온 배터리 팩의 가격은 2022년 1kWh당 150달러에서 2024년에는 128-133달러로 하락하여, 2014년 수준에 비해 85% 하락했습니다. 무정전 전원 장치(UPS) 분야에서는 8-15년의 수명과 3,000-5,000회의 충방전 주기를 통해 VRLA에 비해 10년간의 총 소유 비용(TCO)이 39% 절감됩니다. 지게차 차량군에서도 비슷한 변화가 나타납니다. 리튬 이온 배터리는 1-2시간 만에 충전이 완료되며, 최대 4,000회의 충방전 주기가 가능하기 때문에 배터리 교체실 및 예비 배터리 재고 비용을 절감할 수 있습니다. 전동 지게차에 사용되는 리튬 이온 배터리의 전 세계 보급률은 2024년 32%에서 2034년까지 70% 이상으로 급증할 가능성이 있습니다. 한편, 미국에서는 시설의 50-60%가 여전히 고액의 전기 설비 개보수가 필요하기 때문에 보급이 늦어질 전망입니다. 그렇긴 하지만, 초기 비용의 균형이 이루어지면 납축전지는 높은 가동률을 보이는 부문에서 시장 점유율을 지키기 위해 안전성과 순환형 경제에 기여한다는 이미지에 의존할 수밖에 없게 될 것입니다.

부문별 분석

VRLA(밀폐형 납축전지)는 2025년에 북미 납축전지 시장의 64.3%를 차지해, 2031년까지 연평균 5.7%의 복합 성장률을 기록하며 기존 전해액형 납축전지를 앞지를 것으로 전망됩니다. 이러한 장점은 물 보충의 번거로움을 덜어주고, 가스 배출을 줄이며, OSHA(미국 직업안전보건청)의 실내 공기 규정을 준수하기 쉽게 해주는 밀폐형 구조에서 비롯됩니다. VRLA 중에서도 AGM 유형이 점점 더 인기를 얻고 있습니다. 이는 충전 속도가 빠르기 때문에 연간 수백 회에 달하는 충방전을 반복하는 배송용 밴이나 카셰어링 차량의 가동 중단 시간을 대폭 단축할 수 있기 때문입니다. EnerSys사는 2025년, 사우스캐롤라이나주 섬터에 670만 달러를 투자하여 박판 순납(TPPL) 및 AGM 제품의 생산 라인을 확장했습니다. 이 제품들은 액체형 배터리의 경쟁 제품이 3-5년인 데 비해, 8-10년의 수명을 보장합니다.

액체형 배터리는 여전히 비용을 중시하는 애프터마켓 분야나, 딥 사이클의 내구성과 저렴한 가격을 중시하는 대형 운송 트럭 등에서 사용되고 있습니다. 음극판에 탄소를 함유시켜 부분 충전 상태에서의 성능을 향상시키는 납·탄소 하이브리드 배터리를 통해 점진적인 기술 혁신이 이루어지고 있습니다. 캐나다 북극권의 마이크로그리드에서 진행된 시범 프로젝트를 통해, 외부 히터 없이도 주변 온도 -40°C를 견딜 수 있는 이 화학 조성의 성능이 입증되었습니다. 규제 기준 또한 밀폐형 유닛에 대해 보다 간소화된 VRLA UL 1989 인증을 미묘하게 뒷받침하고 있으며, VRLA의 누액 방지 쉘은 데이터센터 개보수 공사를 감독하는 점점 더 엄격해지는 각 지역 소방 당국의 요건을 충족하고 있습니다. 이러한 요인들이 복합적으로 작용하여, 전해액형 납축전지의 판매가 감소 추세를 보이고 있음에도 불구하고, 북미 납축전지 시장에서 VRLA의 역할은 계속해서 확대되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the north america lead acid battery market size is expected to increase from USD 11.06 billion in 2025 to USD 11.53 billion in 2026 and reach USD 14.29 billion by 2031, growing at a CAGR of 4.39% over 2026-2031.

This report is Segmented by Construction Method (Flooded, VRLA), Application (Starting-Lighting-Ignition (SLI), Stationary, Motive/Traction (Forklifts, Golf-Carts), Portable and Others), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Lead Acid Battery Market Trends and Insights

Replacement Demand from Aging ICE-Vehicle Fleet

The U.S. fleet's record 12.6-year average age underpins a structural replacement wave because vehicles 11 years or older post a 37% annual battery swap rate. Battery Council International tracked 159 million lead acid units shipped in 2024, the bulk tied to replacement rather than factory-install volume. Growing electrical loads from start-stop technology and driver-assistance features hasten the shift from flooded batteries to absorbed-glass-mat (AGM) VRLA designs, which S&P Global projects will reach 19% of all aftermarket installs by 2027. O'Reilly Auto Parts named East Penn its 2025 Supplier of the Year after the vendor scaled DIN-size AGM output that could cover over 40% of vehicles in operation. Crucially, rural and lower-income buyers who retain internal-combustion vehicles longer slow EV cannibalization, extending the tail of the North America lead acid battery market.

Data-Center & Telecom UPS Expansion Boom

Hyperscale builds to serve artificial-intelligence workloads are lifting global data-center electricity demand toward 945 TWh by 2030, up from 460 TWh in 2022. VRLA batteries, especially AGM variants, still held 58% of the USD 4.33 billion global UPS battery segment in 2025. Texas Senate Bill 6 of 2024 requires on-site backup, which is spurring retrofit purchases even while greenfield projects choose lithium-ion for densification advantages. 5G tower roll-outs likewise favor VRLA at remote sites where sealed, maintenance-free units cut service visits. Although lithium-ion offers a 39% lower 10-year TCO, capital budgets and well-established recycling channels preserve VRLA relevance across a large installed base.

Rapid Cost Decline of Lithium-Ion Packs

DOE data show lithium-ion pack prices fell to USD 128-133 per kWh in 2024 from USD 150 per kWh in 2022, an 85% drop versus 2014 levels. In UPS service, that translates to a 39% lower 10-year TCO relative to VRLA, thanks to 8-15 year service life and 3,000-5,000 charge cycles. Forklift fleets mirror the shift: lithium-ion units recharge in 1-2 hours and deliver up to 4,000 cycles, saving on battery-swap rooms and spare-pack inventory. Global lithium-ion penetration in electric forklifts could jump from 32% in 2024 to over 70% by 2034, with the U.S. lagging because 50-60% of facilities still need costly electrical upgrades. Nonetheless, once upfront cost parity is crossed, lead acid must lean on its safety and circular-economy image to defend share in high-utilization segments.

Other drivers and restraints analyzed in the detailed report include:

- 48 V Mild-Hybrid Auxiliary Battery Adoption

- Closed-Loop Recycling Mandates Accelerating Supply Security

- Environmental & Health Concerns over Lead Toxicity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

VRLA units captured 64.3% of the North America lead acid battery market in 2025 and are expected to compound at 5.7% annually through 2031, outpacing conventional flooded cells. This leadership stems from sealed architectures that eliminate watering labor, reduce gas emissions, and simplify compliance with OSHA indoor-air rules. Within VRLA, AGM variants command momentum because faster charge acceptance slashes turnaround time for delivery vans and ride-hail vehicles that cycle hundreds of times per year. EnerSys invested USD 6.7 million in Sumter, South Carolina, during 2025 to expand thin-plate-pure-lead (TPPL) and AGM lines that promise 8-10 year life versus 3-5 years for flooded rivals.

Flooded batteries still serve cost-sensitive aftermarket channels and heavy-duty haul trucks where buyers prize deep-cycle robustness and lower list prices. Incremental innovation is emerging through lead-carbon hybrids that embed carbon in negative plates to boost partial-state-of-charge performance; pilot projects in Canadian Arctic micro-grids illustrate the chemistry's tolerance of -40 °C ambient temperatures without external heaters. Regulatory codes also tilt subtly toward VRLA UL 1989 certification, which is simpler for sealed units, and VRLA's spill-proof shell satisfies increasingly stringent local fire marshals overseeing data-center retrofit work. These factors collectively sustain VRLA's expanding role inside the North America lead acid battery market size even as flooded sales taper.

List of Companies Covered in this Report:

- Clarios

- East Penn Manufacturing

- EnerSys

- Exide Technologies

- C&D Technologies

- GS Yuasa Corporation

- Leoch International

- Power-Sonic Corporation

- Panasonic Holdings Corp

- Crown Battery Manufacturing

- Trojan Battery Company

- NorthStar Battery Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Replacement demand from aging ICE-vehicle fleet

- 4.2.2 Data-center & telecom UPS expansion boom

- 4.2.3 Cost competitiveness vs. lithium alternatives in SLI use-cases

- 4.2.4 48 V mild-hybrid auxiliary battery adoption

- 4.2.5 Lead-carbon batteries for remote micro-grids (Canada Arctic, off-grid mining)

- 4.2.6 Closed-loop recycling mandates accelerating domestic supply security

- 4.3 Market Restraints

- 4.3.1 Rapid cost decline of lithium-ion packs

- 4.3.2 Environmental & health concerns over lead toxicity

- 4.3.3 Impending tighter U.S. EPA ambient-lead limits

- 4.3.4 Recycled-lead supply volatility from scrap-export flows

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Construction Method

- 5.1.1 Flooded

- 5.1.2 VRLA

- 5.2 By Application

- 5.2.1 Starting-Lighting-Ignition (SLI)

- 5.2.2 Stationary

- 5.2.3 Motive/Traction (Forklifts, Golf-carts)

- 5.2.4 Portable and Others

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Clarios

- 6.4.2 East Penn Manufacturing

- 6.4.3 EnerSys

- 6.4.4 Exide Technologies

- 6.4.5 C&D Technologies

- 6.4.6 GS Yuasa Corporation

- 6.4.7 Leoch International

- 6.4.8 Power-Sonic Corporation

- 6.4.9 Panasonic Holdings Corp

- 6.4.10 Crown Battery Manufacturing

- 6.4.11 Trojan Battery Company

- 6.4.12 NorthStar Battery Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment