|

시장보고서

상품코드

2066670

아시아태평양의 자동차용 접착제 및 실란트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Automotive Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

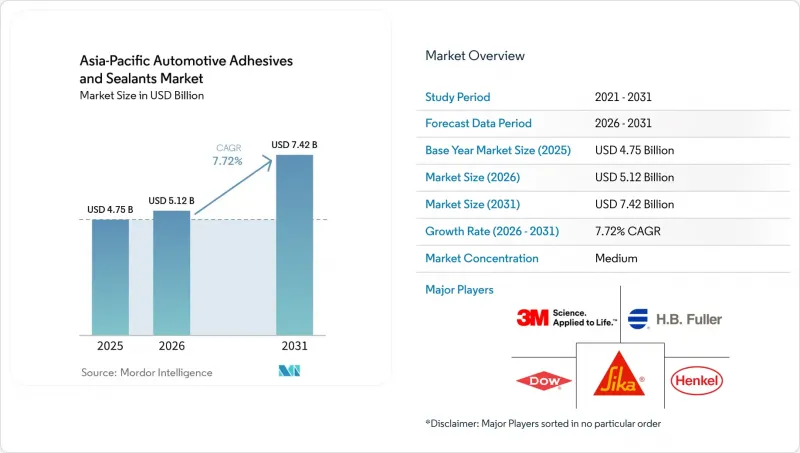

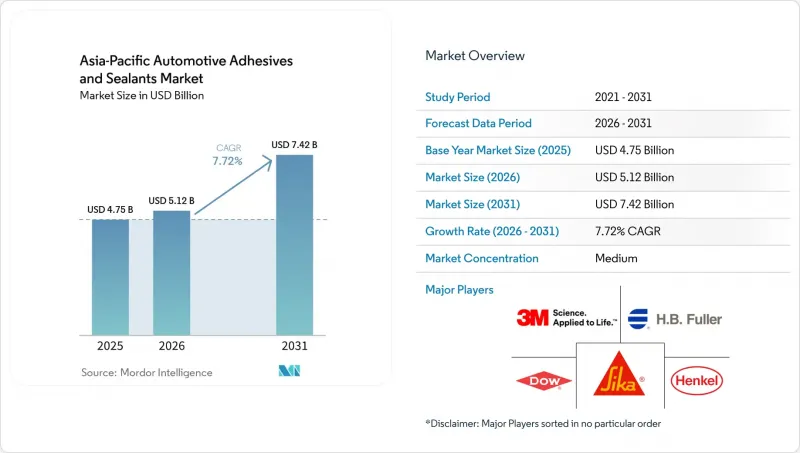

Mordor Intelligence에 의하면, 아시아태평양의 자동차용 접착제 및 실란트 시장 규모는 2025년에 47억 5,000만 달러로 평가되었습니다. 2026년에 51억 2,000만 달러에 달하고, 2031년까지 74억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 7.72%로 성장할 전망입니다.

본 보고서는 수지별(아크릴, 시아노아크릴레이트, 에폭시, 폴리우레탄, 실리콘, VAE/EVA, 기타 수지), 기술별(핫멜트, 반응형, 실란트, 용제계 등), 지역별(호주, 중국, 인도, 인도네시아, 일본, 말레이시아, 싱가포르, 한국, 태국 및 기타 아시아태평양)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 자동차용 접착제 및 실란트 시장 동향 및 인사이트

OEM을 통한 다중 소재 차체(Body-in-White) 설계로의 전환

이 지역의 자동차 제조업체들은 차량 총중량을 8-12% 줄이기 위해 단일 구조 내에 강철, 알루미늄, 마그네슘 및 탄소섬유 강화 플라스틱을 통합하고 있습니다. 이러한 변화로 인해 차량 1대당 접착제 사용량은 약 15Kg에서 25Kg 이상으로 증가했습니다. 아르셀로미탈이 중국산 세단에 적용하고 있는 다단계 통합 공정에서는 초고장력강과 알루미늄 도어 패널을 조합하고 있지만, 이러한 조합은 갈바닉 부식의 위험이 있어 저항 스폿 용접에는 적합하지 않습니다. 2025년, 세레스사는 마그네슘 다이캐스팅 서브프레임을 채택하고, 표면 전처리가 필요 없이 10메가파스칼(MPa)을 초과하는 랩 전단 강도를 실현하는 에폭시계 구조용 접착제를 지정했습니다. 일본의 Tier 1 공급업체에 따르면, 실온에서 경화되는 실릴 개질 폴리머계 실란트는 소성로가 필요하지 않기 때문에 사이클 타임을 단축할 수 있다고 합니다. 이러한 발전 덕분에 2027년부터 2030년에 걸쳐 출시될 예정인 대량 생산 플랫폼에서 접착제 사용이 더욱 보편화되고 있습니다.

중국 VI 및 CAFE 기준에 따른 경량화 요건

2026년 1월 중국에서 ‘중국 VI B’ 기준이 시행되면서, 미세먼지 허용치가 30%, 질소산화물(NOx) 허용치가 50% 각각 하향 조정되며, 실제 주행 배기가스 시험 도입을 통해 규제 집행이 강화되었습니다. 또한, 자동차 제조업체(OEM)는 2030년까지 차종 평균 연비를 100킬로미터당 3.3리터(L/100 km)로 달성해야 하며, 이에 따라 에너지 소비가 많은 열처리 공정을 생략할 수 있는 접착제로 접합된 알루미늄이나 복합 소재로 강재를 대체하는 움직임이 활발해지고 있습니다. 현대와 기아도 이와 유사한 방식을 채택하고 있으며, 테일게이트와 보닛에 반응성 핫멜트를 사용함으로써 개폐부 하나당 3-5kg의 경량화를 실현하고 있습니다. 2026년에 시행될 일본의 스테이지 4 규제에 따라 경량화 요건이 밴과 소형 트럭으로 확대됨에 따라, 이미 인증을 받은 1액형 폴리우레탄에 대한 공급업체 수요가 증가하고 있습니다.

이소시아네이트 및 에폭시 원료 가격 변동

메틸렌디페닐디이소시아네이트(MDI)의 예상치 못한 공급 중단과 원유 가격 변동으로 인해 2025년 한 해 동안 현물 시장에 변동이 발생했으며, 아세안 지역의 소규모 배합 제조업체들의 이익률은 200-300 베이시스 포인트 감소했습니다. 2026년 초, 에폭시 시장은 침체세를 보였고, 일부 공급업체들은 연구개발 및 생산 능력 확대 계획을 연기할 수밖에 없게 되었습니다. 국내 공급을 확보하기 위해 보조금을 지원받은 DIC의 치바 신 에폭시 공장은 원자재 리스크를 관리하기 위해 막대한 설비 투자가 필요하다는 점을 여실히 보여주고 있습니다. 시릴 변성 폴리머를 이용한 대체재는 이소시아네이트에 대한 의존도를 낮추는 데 도움이 되지만, 120°C를 초과하는 온도에서 발생하는 열노화라는 제약으로 인해 그 용도는 여전히 제한적입니다.

부문별 분석

폴리우레탄은 400%의 성장률과 습기 경화성을 갖추고 있어 이종 기재의 접합에 적합하기 때문에 2025년에는 아시아태평양의 자동차용 접착제 및 실란트 시장 점유율의 27.25%를 차지했습니다. 헨켈사의 열전도성 폴리우레탄 등급은 1.2-3.4 와트/미터·켈빈(W/m·K)의 열전도율을 갖추고 있으며, 전기자동차(EV) 모듈의 접착에 널리 사용되고 있습니다. 에폭시계 접착제는 최대 180°C까지의 내열성이 요구되는 보닛 내부 용도로 사용되고 있는 반면, 실리콘계 접착제는 절연 내력이 10킬로볼트/mm(kV/mm)를 초과하기 때문에 고전압 배터리 팩에 주로 채택되고 있습니다.

비닐아세테이트·에틸렌/에틸렌비닐아세테이트(VAE/EVA) 계열 수성 시스템은 현재 시장 점유율은 작지만, 2031년까지 연평균 성장률(CAGR) 6.55%를 나타낼 것으로 예측됩니다. 뛰어난 가성비와 휘발성 유기 화합물(VOC) 규제 준수 덕분에, 인도에서 헤드라이너나 도어 패널 등의 용도로 사용하기에 적합합니다. 이러한 접착제는 OEM(원청 브랜드 제조업체)이 자외선(UV) 램프에 투자할 필요 없이, 일본이 정한 차량 실내 포름알데히드 농도 상한치인 1입방미터당 100마이크로그램(µg/m3)을 충족하는 데 도움이 됩니다. VAE/EVA 계열 접착제 시장은 국내 공급업체들의 지역별 생산 능력 확충에 힘입어 대폭 확대될 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the asia-Pacific automotive adhesives and Sealants Market size is projected to be USD 4.75 billion in 2025, USD 5.12 billion in 2026, and reach USD 7.42 billion by 2031, growing at a CAGR of 7.72% from 2026 to 2031.

This report is Segmented by Resin (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, Other Resins), Technology (Hot Melt, Reactive, Sealants, Solvent-Borne, and More), and Geography (Australia, China, India, Indonesia, Japan, Malaysia, Singapore, South Korea, Thailand, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Automotive Adhesives And Sealants Market Trends and Insights

OEM Preference for Multi-Material Body-in-White Designs

Automakers in the region are integrating steel, aluminum, magnesium, and carbon-fiber-reinforced polymers within single structures to reduce curb weight by 8-12%. This change has increased adhesive usage from approximately 15 kilograms to over 25 kilograms per vehicle. ArcelorMittal's multi-phase integration process for Chinese sedans combines ultra-high-strength steel with aluminum closures, a pairing unsuitable for resistance spot-welding due to the risk of galvanic corrosion. In 2025, Seres adopted magnesium die-cast subframes, specifying epoxy structural adhesives that achieve lap-shear strength exceeding 10 megapascals (MPa) without requiring surface pretreatment. Japanese tier-one suppliers report that silyl-modified-polymer sealants, which cure at ambient temperatures, reduce cycle times by eliminating the need for bake ovens. These advancements are embedding adhesives more deeply into high-volume platforms scheduled for launch between 2027 and 2030.

Weight-Reduction Mandates Under China VI and CAFE Norms

China's implementation of China VI B standards in January 2026 will reduce particulate matter thresholds by 30% and nitrogen oxide (NOx) limits by 50%, while real-driving-emissions testing will enhance enforcement. Additionally, original equipment manufacturers (OEMs) must achieve a fleet average of 3.3 liters per 100 kilometers (L/100 km) by 2030, driving the substitution of steel with adhesive-bonded aluminum and composites that eliminate the need for energy-intensive heat tunnels. Hyundai and Kia are following a similar approach, using reactive hot-melts on tailgates and hoods to reduce weight by 3-5 kilograms per closure. Japan's Stage 4 regulations, effective in 2026, extend lightweighting requirements to vans and mini-trucks, increasing supplier demand for qualified one-component polyurethanes.

Volatility in Isocyanate and Epoxy Feedstock Prices

Unplanned methylene diphenyl diisocyanate (MDI) outages and fluctuations in crude oil prices caused spot-market variations through 2025, reducing the margins of smaller ASEAN formulators by 200-300 basis points. The epoxy market weakened in early 2026, leading some suppliers to delay research and development initiatives and capacity expansion plans. DIC's new Chiba epoxy unit, subsidized to ensure domestic supply, highlights the significant capital investment required to manage raw material risks. While silyl-modified polymer alternatives help reduce isocyanate exposure, they remain limited by thermal-aging constraints above 120°C.

Other drivers and restraints analyzed in the detailed report include:

- Uptick in EV Battery-Pack Gasketing Demand

- Start-Ups Commercializing Bio-Based Polyurethane Chemistries

- OEM Push Toward Mechanical Fastening for Ease of Repair

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane is expected to account for 27.25% of the Asia-Pacific Automotive Adhesives & Sealants market share in 2025, driven by its 400% elongation and moisture-curing properties, which are suitable for mixed-substrate joints. Henkel's thermal-conductive polyurethane grades, offering thermal conductivity of 1.2-3.4 watts per meter-kelvin (W/m*K), are widely used in bonding electric vehicle (EV) modules. Epoxy adhesives are utilized in under-hood applications requiring resistance to temperatures up to 180°C, while silicone adhesives are preferred for high-voltage battery packs due to their dielectric strength exceeding 10 kilovolts per millimeter (kV/mm).

Vinyl acetate ethylene/ethylene vinyl acetate (VAE/EVA) water-borne systems, though currently smaller in market share, are projected to grow at a compound annual growth rate (CAGR) of 6.55% through 2031. Their cost-effectiveness and compliance with volatile organic compound (VOC) regulations make them suitable for applications such as headliners and door panels in India. These adhesives help original equipment manufacturers (OEMs) meet Japan's in-cabin formaldehyde limit of 100 micrograms per cubic meter (µg/m3) without requiring ultraviolet (UV) lamp investments. The market for VAE/EVA adhesives is expected to expand significantly, supported by increased regional production capacity from domestic suppliers.

List of Companies Covered in this Report:

- 3M

- Arkema

- Ashland

- DIC Corporation

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International

- ITW Performance Polymers

- Jowat SE

- PARKER HANNIFIN CORP

- Permabond LLC

- Pidilite Industries Ltd.

- PPG Industries, Inc.

- Shanghai Huitian New Material Co., Ltd

- SHINSUNG PETROCHEMICAL

- Sika AG

- THREEBOND INTERNATIONAL, INC

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OEM preference for multi-material body-in-white designs

- 4.2.2 Weight-reduction mandates under China VI and CAFE norms

- 4.2.3 Uptick in EV battery pack gasketing demand

- 4.2.4 Start-ups commercialising bio-based polyurethane chemistries

- 4.2.5 Emergence of low-surface-energy composite adhesives

- 4.3 Market Restraints

- 4.3.1 Volatility in isocyanate and epoxy feedstock prices

- 4.3.2 OEM push toward mechanical fastening for ease-of-repair

- 4.3.3 Stringent VOC caps in Japan and South Korea

- 4.3.4 Skill-gap in robot-dispensing programming at Tier-2 plants

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV-Cured Adhesives

- 5.2.6 Water-borne

- 5.3 By Geography

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/(%)Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 DIC Corporation

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International

- 6.4.9 ITW Performance Polymers

- 6.4.10 Jowat SE

- 6.4.11 PARKER HANNIFIN CORP

- 6.4.12 Permabond LLC

- 6.4.13 Pidilite Industries Ltd.

- 6.4.14 PPG Industries, Inc.

- 6.4.15 Shanghai Huitian New Material Co., Ltd

- 6.4.16 SHINSUNG PETROCHEMICAL

- 6.4.17 Sika AG

- 6.4.18 THREEBOND INTERNATIONAL, INC

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment