|

시장보고서

상품코드

2066728

독일의 의약품 콜드체인 물류 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Germany Pharmaceutical Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

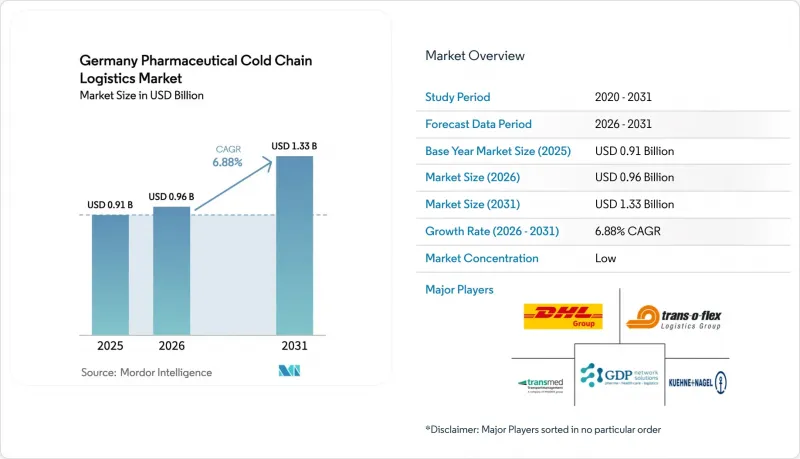

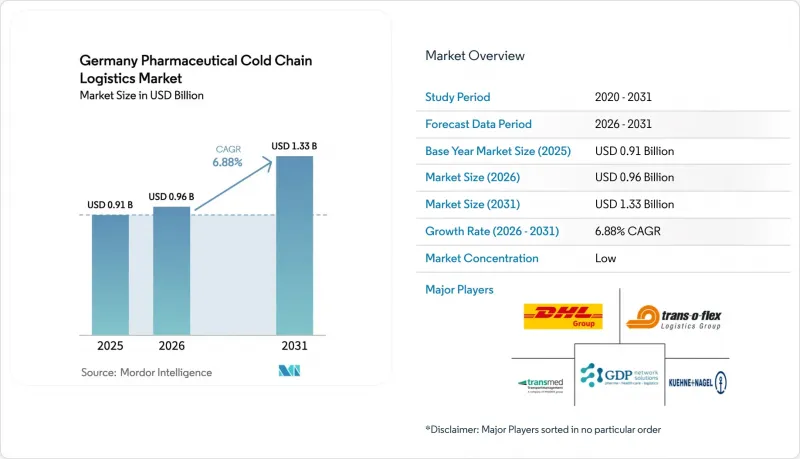

Mordor Intelligence에 의하면, 독일의 의약품 콜드체인 물류 시장 규모는 2025년 9억 1,000만 달러로 평가되었고, 2026년에는 9억 6,000만 달러로 추정되고, 2026-2031년 CAGR 6.88%로 성장을 지속할 전망이며, 2031년까지 13억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 서비스 유형별(운송(육상, 항공, 해상, 철도), 창고·유통, 부가가치 서비스), 온도별(냉장, 냉동, 상온), 제품별(제네릭 의약품, 브랜드 의약품) 및 용도별(바이오 의약품, 화학 의약품, 특수 의약품)별로 분류되어 있습니다. 시장 전망은 금액(10억 달러) 기준으로 제시되어 있습니다.

독일의 의약품 콜드체인 물류 시장 동향 및 인사이트

바이에른주 및 바덴뷔르템베르크주에서의 바이오의약품 생산 확대

2027년까지 가동을 시작할 예정인 일라이 릴리(Eli Lilly)의 23억 유로(25억 달러) 규모 ‘알레이(Aley)’ 공장은 서부 및 남부 물류 회랑에서 충전 및 마무리부터 조제까지 2-8°C의 프로토콜 하에서 운송되는 바이오의약품 및 인크레틴 치료제의 생산이 확대되고 있음을 여실히 보여주고 있습니다. 로슈의 독일 내 지속적인 자본 투자는 바덴뷔르템베르크주와 인접 주 전체에 새로운 활력을 불어넣고 있으며, 규제 대응의 신속성과 전문 인력을 중시하는 세계 기업들이 밀집해 있는 클러스터를 강화하고 있습니다. 이러한 클러스터화를 통해 시설 간 운송 시간이 단축되고, 역물류 순환 체계가 강화되는 동시에 여러 물류 센터가 밀집된 환경이 조성됩니다. 이를 통해 GDP 인증을 취득한 운송업체는 효율적인 밀크런 및 풀트럭 적재 운송 노선으로 전환할 수 있게 됩니다. 프랑크푸르트나 슈투트가르트와 같은 복합운송 거점과의 근접성은 노선 관리를 개선하고, 고부가가치 바이오의약품 환적 시 발생하는 환경적 위험을 줄여줍니다. 그 결과, 남부 및 서부 지역의 출하 흐름이 더욱 통합되어 운송업체의 자산 활용률이 향상될 뿐만 아니라, 독일 의약품 콜드체인 물류 시장의 서비스 수준이 안정화될 것입니다.

중부 유럽의 의약품 유통 허브로서의 독일

플로르슈타트에 위치한 DHL의 확장된 생명과학 및 헬스케어 캠퍼스는 GDP 기준을 충족하는 공간 10만 제곱미터와 다양한 온도 구역에 걸쳐 있는 팔레트 보관 공간 14만 개 이상을 추가함으로써, 프랑크푸르트 공항을 거점으로 하는 중부 유럽의 의약품 허브로서 독일의 위상을 강화하고 있습니다. 이 시설은 GMP 조건 하에서 API, 위험물, 원자재의 취급을 지원하며, 이 지역의 생명과학 분야 고객을 대상으로 하는 엄격한 유럽 및 국제 기준을 준수하고 있습니다. 라인-마인-도나우 회랑과 고속철도를 포함한 독일의 복합 운송망은 북해의 관문과 알프스 산맥 주변의 제조 거점을 연결하여 의약품 물류를 효율화하는 데 기여하고 있습니다. 24시간 이내 배송과 신원 추적 체인 관리가 필요한 전문 치료제의 경우, 독일의 허브 앤 스포크(hub-and-spoke) 구조를 통해 전날 밤까지 수거하고, 다음 날 이른 아침에 병원이나 재택 간호 시설로 배송할 수 있습니다. 이러한 통합된 네트워크 효과는 독일의 의약품 콜드체인 물류 시장을 장기적으로 뒷받침하는 구조적 강점으로 작용하고 있습니다.

급등하는 에너지 비용이 냉장 물류의 경제성에 미치는 영향

냉장 창고와 능동형 냉장 운송은 에너지 집약적 시스템에 의존하고 있기 때문에 가격 변동은 이익률을 압박하고, 급증하는 수요에 대응하기 위한 운송 능력을 신속하게 확충하는 데 제약을 가합니다. 생산자 물가의 변동은 독일 제조업의 높은 비용 민감도를 여실히 보여주고 있으며, 이는 온도 관리 업무 및 관련 서비스의 비용 구조에 영향을 미치고 있습니다. 항만에 인접한 창고 등 냉장 설비 밀도가 높은 거점에서는 계절적 수요가 정점에 달할 때 피크 부하 문제에 직면하게 되며, 이로 인해 긴급 대응 비용이 증가합니다. 운송업체들은 노선 및 화물 통합을 통해 대응하고 있지만, 전용 운송 능력이 필요한 화물이나 단기간 내에 조치가 필요한 화물의 경우 여전히 위험 요소가 남아 있습니다. 이러한 압박은 -20°C 및 -70°C 인프라의 업그레이드를 지연시킬 가능성이 있으며, 결과적으로 독일 의약품 콜드체인 물류 시장의 서비스 범위에 영향을 미칠 것입니다.

부문별 분석

2025년에는 운송 부문이 부문 총 가치의 41.78%를 차지했으며, 부가가치 서비스가 2031년까지 6.87%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있음에도 불구하고, 현재 구성 비율의 기반을 이루고 있습니다. 도로 운송은 바이에른주, 노르트라인-베스트팔렌주, 헤센주의 각 생산 거점 간 국내 물류의 중추 역할을 계속하고 있습니다. 한편, 항공 화물은 프랑크푸르트를 경유하여 시간적 제약이 엄격한 바이오 의약품 및 임상용 자재를 운송하는 가교 역할을 하고 있습니다. 해상 운송과 철도 운송은 국내 운송에서는 비교적 작은 역할을 담당하고 있지만, 수출입 회랑 및 업스트림 공정에서의 API(원료의약품) 집약화에 기여하고 있습니다. 창고·유통 부문은 다온도대 대응 GDP(적정 보관 기준) 시설, 검증 절차를 마친 냉장실, 그리고 많은 제약 기업이 외부에 위탁하고 있는 지속적인 모니터링을 통해 시장 점유율을 확대되고 있습니다. DHL의 플로르슈타트 캠퍼스는 2-8°C, -20°C, 나아가 -70°C까지의 온도 구역을 갖춘 통합형 창고가 바이오의약품 및 임상 연구 고객에게 어떻게 더 광범위한 서비스 범위를 뒷받침하고 있는지 보여줍니다. 함부르크에서 GEODIS가 획득한 해상 운송용 GDP 인증은 선박에서 GDP 창고에 이르는 복합 운송의 연속성을 강화하고, 입고 및 환적 과정에서 발생할 수 있는 인계 위험을 줄여줍니다. 운송업체가 운송, 보관 및 규정 준수 대응이 요구되는 부가 서비스를 단일 계약으로 통합하여 화주의 감사 부담을 줄일 수 있다면, 독일의 의약품 콜드체인 물류 시장은 그 혜택을 누릴 수 있을 것입니다.

부가가치 서비스가 확대되는 가운데, 운송은 계속해서 핵심적인 역할을 수행할 것입니다. 이는 제조업체가 인계 횟수를 줄이면서도 보다 철저한 규정 준수 대응을 요구하고 있기 때문입니다. 이러한 경향은 핵심 운송과 밀접하게 관련된 온도 편차 관리, 통제된 반품, 임상 검체 취급 분야에서 가장 두드러지게 나타납니다. Eurotranspharma사의 이중 온도대 물류 시스템은 차량 수준의 설계를 통해 하나의 경로 계획 내에서 혼합 화물을 처리할 수 있음을 보여주고 있으며, 이를 통해 개별 소포마다 패시브 포장을 적용해야 할 필요성이 줄어듭니다. 계약 범위가 엔드투엔드로 확대됨에 따라, 보관, 라벨링, 재라벨링 및 배치 인증 키팅 서비스를 통합하는 운송업체들이 독일 의약품 콜드체인 물류 업계에서 입지를 강화하고 있습니다. 이러한 변화로 인해, 감사를 마친 IT 시스템과 원격 측정 기능을 갖추고, GDP(적정 유통 기준) 준수를 실시간으로 입증할 수 있는 사업자가 유리한 입장에 서게 됩니다. 이러한 특징들은 독일 의약품 콜드체인 물류 시장에서 저가 입찰에 대응할 수 있는 가격 경쟁력의 기반이 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 전망

제8장 부록

AJYAccording to Mordor Intelligence, the germany pharmaceutical cold chain logistics market size is expected to grow from USD 0.91 billion in 2025 to USD 0.96 billion in 2026 and is forecast to reach USD 1.33 billion by 2031 at 6.88% CAGR over 2026-2031.

This report is Segmented by Service Type (Transportation [Road, Air, Sea, Rail], Warehousing & Distribution, and Value-Added Services), by Temperature Type (Chilled, Frozen, and Ambient), by Product (Generic Drugs, and Branded Drugs), and by Application (Biopharma, Chemical Pharma, and Specialized Pharma). The Market Forecasts are Provided in Terms of Value (USD Billion).

Germany Pharmaceutical Cold Chain Logistics Market Trends and Insights

Expansion of Biopharma Manufacturing in Bavaria and Baden-Wurttemberg

Eli Lilly's EUR 2.3 billion (USD 2.5 billion) plant in Aley, operational by 2027, underscores how western and southern corridors are scaling biologics and incretin therapy output that moves under 2-8°C protocols from fill-finish to dispensing. Roche's continued capital commitment in Germany adds further momentum across Baden-Wurttemberg and adjacent states, reinforcing a dense cluster of global players that value regulatory speed and specialized labor. This clustering reduces inter-facility transfer time, strengthens reverse-logistics loops, and creates multi-depot density that GDP-certified carriers convert into efficient milk runs and full-truckload lanes. Proximity to Frankfurt and Stuttgart intermodal gateways improves route control and reduces ambient risk during transshipment for high-value biologics. The result is a more consolidated outbound flow from the south and west that improves asset utilization for carriers and stabilizes service-level performance in the Germany pharmaceutical cold chain logistics market.

Germany as a Central European Pharmaceutical Distribution Hub

DHL's expanded Life Sciences & Healthcare campus in Florstadt adds 100,000 square meters of GDP-compliant space and more than 140,000 pallet positions across multi-temperature zones, which strengthens Germany's position as a central European pharma hub served by Frankfurt Airport. The site supports APIs, hazardous materials, and raw materials within GMP conditions, aligning with strict European and international standards for life sciences customers across the region. Germany's multimodal backbone, including the Rhine-Main-Danube corridor and high-speed rail, links North Sea gateways to Alpine manufacturing and helps consolidate pharmaceutical flows. For specialized therapies that need sub-24-hour delivery and chain-of-identity controls, Germany's hub-and-spoke architecture enables overnight staging and same-morning hospital or home-care dispatch. This integrated network effect is a structural advantage that sustains the Germany pharmaceutical cold chain logistics market over the long term.

High Energy Costs Impacting Refrigeration Economics

Cold storage and active refrigerated transport depend on energy-intensive systems, so price volatility tightens margins and limits the ability to add surge capacity quickly. Producer price movements underscore cost sensitivity within German manufacturing, which influences the cost base for temperature-controlled operations and related services. Sites with high refrigeration density, such as port-adjacent warehouses, face peak-load challenges during seasonal extremes that raise contingency costs. Carriers respond with route and load consolidation, but residual exposure persists for shipments that require dedicated capacity or short-notice dispatch. These pressures can delay upgrades to -20°C and -70°C infrastructure, which in turn affects service breadth in the Germany pharmaceutical cold chain logistics market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Direct-to-Patient Home Delivery Programs

- Increasing Clinical Trial Activity for Cell and Gene Therapies

- Driver Shortage for GDP-Certified Cold Chain Transportation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 41.78% of segment value in 2025, which anchors the current mix even as value-added services post the fastest 6.87% CAGR through 2031. Road distribution remains the backbone for domestic flows across production nodes in Bavaria, North Rhine-Westphalia, and Hesse, while air freight bridges time-critical biologics and clinical materials through Frankfurt. Ocean and rail have a smaller role for domestic movements, yet they contribute to import-export corridors and upstream API consolidation. Warehousing and distribution absorb a growing share due to multi-zone GDP facilities, validated cold rooms, and continuous monitoring that many pharma clients outsource. DHL's Florstadt campus illustrates how integrated warehousing with 2-8°C, -20°C, and down to -70°C zones supports a wider service envelope for biopharma and clinical research customers. GEODIS's GDP certification for ocean freight in Hamburg strengthens multimodal continuity from vessel to GDP warehouse, which reduces handoff risk for inbound or transshipment flows. The Germany pharmaceutical cold chain logistics market benefits when carriers can wrap transport, storage, and compliance-heavy add-ons into single contracts that reduce audit overhead for shippers.

Transportation will remain central as value-added services scale because manufacturers want fewer handoffs with richer compliance coverage. This is most visible in temperature excursion management, controlled returns, and clinical sample handling that sit adjacent to core transport. Eurotranspharma's bi-temperature distribution shows how fleet-level design can support mixed consignments in one route plan, which reduces the need for passive packaging on every parcel. As more contracts expand to end-to-end scope, carriers that integrate storage, labeling, relabeling, and batch-certified kitting gain traction in the Germany pharmaceutical cold chain logistics industry. The shift favors operators with audited IT systems and telemetry that demonstrate GDP adherence in real time. These attributes underpin price resilience against low-cost bids in the Germany pharmaceutical cold chain logistics market.

List of Companies Covered in this Report:

- Trans-o-flex (ThermoMed)

- DHL

- Transmed Transport GmbH

- GDP Network Solutions GmbH

- Kuehne + Nagel

- Biotech and Pharma Logistics

- Rhenus Logistics

- Ceva Logistics

- DB Schenker

- Pfenning Logistics

- FedEx Logistics

- MSK Pharma Logistics

- Eurotranspharma

- NextPharma Logistics GmbH

- B+S GmbH Logistik und Dienstleistungen

- SK Pharma Logistics GmbH

- Logistics4Pharma

- BPL - Biotech & Pharma Logistics GmbH

- FIEGE Logistics

- Logwin AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Biopharma Manufacturing in Bavaria and Baden-Wurttemberg

- 4.2.2 Germany as Central European Pharmaceutical Distribution Hub

- 4.2.3 Growing Direct-to-Patient Home Delivery Programs

- 4.2.4 Increasing Clinical Trial Activity for Cell and Gene Therapies

- 4.2.5 Premium Pricing Tolerance for Temperature-Assured Logistics

- 4.2.6 Rising mRNA Vaccine Production Following Pandemic Infrastructure

- 4.3 Market Restraints

- 4.3.1 High Energy Costs Impacting Refrigeration Economics

- 4.3.2 Driver Shortage for GDP-Certified Cold Chain Transportation

- 4.3.3 Infrastructure Limitations in Former East German Regions

- 4.3.4 Intense Price Competition from Eastern European Logistics Providers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geo-Politics Events on the Market

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea

- 5.1.1.4 Rail

- 5.1.2 Warehousing & Distribution

- 5.1.3 Value-Added Services

- 5.1.1 Transportation

- 5.2 By Temperature Type

- 5.2.1 Chilled

- 5.2.2 Frozen

- 5.2.3 Ambient

- 5.3 By Product

- 5.3.1 Generic Drugs

- 5.3.2 Branded Drugs

- 5.4 By Application

- 5.4.1 Biopharma

- 5.4.2 Chemical Pharma

- 5.4.3 Specialized Pharma

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Trans-o-flex (ThermoMed)

- 6.4.2 DHL

- 6.4.3 Transmed Transport GmbH

- 6.4.4 GDP Network Solutions GmbH

- 6.4.5 Kuehne + Nagel

- 6.4.6 Biotech and Pharma Logistics

- 6.4.7 Rhenus Logistics

- 6.4.8 Ceva Logistics

- 6.4.9 DB Schenker

- 6.4.10 Pfenning Logistics

- 6.4.11 FedEx Logistics

- 6.4.12 MSK Pharma Logistics

- 6.4.13 Eurotranspharma

- 6.4.14 NextPharma Logistics GmbH

- 6.4.15 B+S GmbH Logistik und Dienstleistungen

- 6.4.16 SK Pharma Logistics GmbH

- 6.4.17 Logistics4Pharma

- 6.4.18 BPL - Biotech & Pharma Logistics GmbH

- 6.4.19 FIEGE Logistics

- 6.4.20 Logwin AG

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 External Trade Statistics - Exports and Imports by Product and by Country of Destination/Origin