|

시장보고서

상품코드

2066743

박막 배터리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Thin Film Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

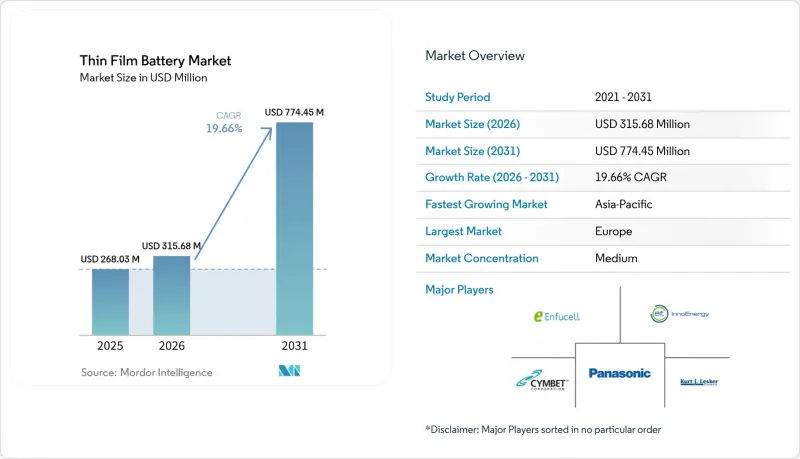

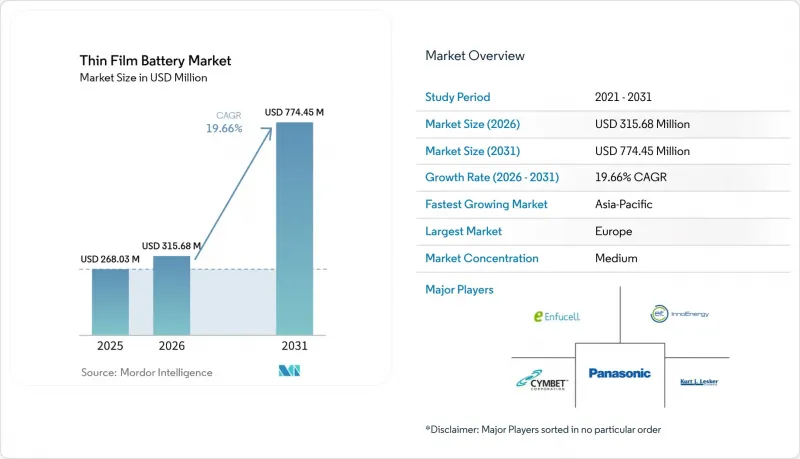

Mordor Intelligence에 의하면, 박막 배터리 시장 규모는 2025년 2억 6,803만 달러로 평가되었습니다. 2026년 3억 1,568만 달러에서 2031년까지 7억 7,445만 달러에 이를 것으로 예상되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 19.66%를 나타낼 전망입니다.

본 보고서는 배터리 유형(충전식, 비충전식), 기술(프린트 배터리, 세라믹 배터리, 기타 기술), 용도(소비자용 전자기기, 의료기기, 웨어러블 기술, 스마트카드, RFID, 기타) 및 지역(북미, 유럽, 아시아·태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 박막 배터리 시장 동향 및 인사이트

웨어러블 및 IoT 기기의 생산 급증

스마트 워치, 이어폰, 서비스 로봇, 산업용 센서의 전 세계 출하량 증가에 따라 1 Ah 미만의 평판형 배터리에 대한 수요가 지속적으로 증가하고 있습니다. TDK가 진정한 무선 스테레오 이어폰을 위해 도입한 박막 인덕터는 1㎥ 단위의 공간이 중요한 장치에서 기존의 코인형 배터리를 더 이상 필요로 하지 않게 합니다. 이를 통해 25분 이내에 90%까지 충전할 수 있게 되어, 부피가 큰 케이스 없이도 일상적으로 착용할 수 있는 기기를 지원합니다. 삼성SDI는 로봇 수요가 2025년 50만 대에서 2030년에는 204만 대로 증가할 것으로 전망하며, 이러한 수요 증가에 대응하기 위해 고체 파우치형 배터리를 발표했습니다. Dracula Technologies사의 LayerVault OPV 시트 등 에너지 수확 모듈은 물류 센서에 필요한 간헐적인 전력을 보완하며, 소비자용 및 산업용 두 가지 이용 사례 모두에서 박막 배터리 시장 규모를 확대되고 있습니다. 환경광 하베스터와 플렉서블 마이크로셀의 시너지 효과로 인해, 온도 로거나 자산 태그에 사용되는 CR2032 배터리를 대체하는 추세가 확산되고 있습니다.

소비자용 전자기기의 소형화 동향

각 기기 제조업체들은 스마트 카드, AR 안경, 생체 인증 태그의 경우 본체 두께를 5mm 미만으로 줄이겠다는 목표를 세우고 있으며, 이에 따라 평평한 형태의 배터리로의 전환이 시급해지고 있습니다. BTRY사의 1S4P 셀은 두께가 불과 0.1mm에 불과하면서도 1분간 충전으로 50mAh를 공급하여, ID 카드 내에서 능동적인 보안 인증을 가능하게 하는 혁신의 대표적인 사례입니다. 평면형 셀은 플렉서블 회로 기판에 직접 라미네이트되며, 와이어 본딩 지그를 생략함으로써 조립 시간을 단축하고, 체적 에너지 밀도가 18650 규격을 하회하는 경우에도 OEM 제조업체에 매력적인 총소유비용(TCO)을 실현합니다. 이러한 설계의 유연성 덕분에, 기기의 강성을 유지하면서도 곡선형 스마트 워치 뒷면이나 베젤리스 디스플레이를 구현할 수 있습니다. 사용 패턴이 연속적이지 않고 간헐적이기 때문에 소비자들은 웨어러블 기기의 경량화를 위해 매일 재충전을 감수하고 있으며, 이는 박막 배터리 시장 전반에 걸쳐 재주문을 촉진하고 있습니다.

대용량 리튬 이온 배터리와 비교한 에너지 밀도의 한계

박막 배터리의 에너지 밀도는 100-200 Wh/L로, 현재 320 Wh/kg에 육박하고 있는 첨단 2만 1,700 원통형 전지의 약 3분의 1 수준에 그치고 있습니다. LiPON의 이온 전도도는 10-6 S/cm 수준에 그치고 있어, 방전율에 상한이 발생하기 때문에 전동 공구에 적용하기는 어렵습니다. EV용 배터리 팩에 실리콘·흑연 음극재가 채택됨에 따라 성능 격차는 더욱 벌어지고 있으며, 박막 배터리 시장이 장시간 구동이나 높은 방전 전류가 요구되는 분야에서 시장 점유율을 확보하기는 어려워지고 있습니다. 며칠 동안 연속 작동을 목표로 하는 스마트 워치 제조업체 중에는 코인형 배터리로 되돌아가는 경우도 있으며, AR 헤드셋 OEM 제조업체들은 보조 전원으로 소형 리튬 폴리머 파우치 배터리를 함께 사용하고 있습니다. 복합 전해질의 연구 개발을 통해 전도도가 2배로 높아질 가능성은 있지만, 2027년 이후의 상용화 단계에서는 현재의 예측 기간 내에 개선이 이루어질 것으로 기대하기 어렵습니다.

부문별 분석

2025년 매출액 중 충전식 박막 배터리가 73.57%를 차지했으며, 연평균 성장률(CAGR) 20.69%를 나타낼 것으로 예측되어, 박막 배터리 시장에서 그 우위를 더욱 공고히 할 전망입니다. 이 부문은 수천 회의 충전 주기가 필요한 스마트 워치, 휴머노이드 로봇, 의료용 임플란트 등의 용도로부터 혜택을 보고 있습니다. 삼성SDI의 ‘SolidStack’ 프로토타입은 서비스 로봇에서 8시간의 가동 주기를 실현하며, 교대 시 신속한 충전을 가능하게 합니다. 일회용 스마트 패키징의 경우, 단위당 비용이 라벨 1장당 몇 센트에 불과하다는 경제성 덕분에 여전히 비충전식 1차 전지가 사용되고 있지만, IoT 기기 운영 사업자들이 충전식 전지의 수명 주기 비용 측면에서의 이점을 높이 평가함에 따라 박막 배터리 시장에서의 점유율은 감소하는 추세입니다.

ISO/IEC 7810 내구성 시험 및 UN 38.3 운송 인증이 연구 개발 로드맵을 형성하고 있으며, 각 공급업체에 1,000사이클을 초과하는 열 안정성과 5년을 초과하는 보관 기간에 대한 검증을 요구하고 있습니다. 방위 물류 분야에서도 STUB 규격이 충전식 형식을 채택하여 현장으로의 배터리 출하량을 대폭 줄임으로써 더욱 탄력을 받고 있습니다. 그 결과, 박막 배터리 업계는 LiPON 기술의 개선과 음극이 없는 스택 설계를 통한 사이클 수명 연장에 연구개발 예산을 집중하고 있으며, 2차 전지 화학 계열 시장 점유율 우위를 더욱 공고히 하고 있습니다.

지역별 분석

2025년, 유럽은 박막 태양전지 시장 매출의 52.11%를 차지했습니다. 이는 2027년부터 탄소 발자국 공개와 배터리 패스포트 도입을 의무화하는 EU 배터리 규정(2023/1542)에 근거한 것입니다. 스위스의 BTRY사는 용매를 사용하지 않는 롤-투-롤 방식의 고체 전지 산업화를 위해 570만 달러를 조달하며, 해당 지역의 딥테크 분야의 활력을 보여주고 있습니다. 프랑스의 ITEN과 영국의 배터리 산업화 센터(Battery Industrialisation Centre)는 Ilika사의 ‘Goliath’ 프로토타입에 대한 파일럿 라인의 수율을 93%까지 끌어올려 공급 안정성을 확보했습니다. 북유럽 제조업체들은 저탄소성을 내세우기 위해 수력 발전에서 생산된 전력을 강조하고 있지만, 리튬과 코발트의 채굴 허가가 여전히 걸림돌로 작용하고 있습니다.

아시아태평양은 성장의 원동력이 되어 연평균 성장률(CAGR) 22.35%로 확대되며, 박막 배터리 시장의 판도를 새롭게 바꾸고 있습니다. 삼성SDI는 ‘InterBattery 2026’에서 휴머노이드 로봇용 파우치형 전고체 배터리 시제품을 공개했으며, 약 1,100건의 특허를 보유함으로써 자사의 경쟁 우위를 강화하고 있습니다. 중국은 ‘중국 제조 2025’ 보조금 제도에 따라 커넥티드 패키징용 인쇄형 배터리 생산을 확대하고 있는 반면, 일본의 TDK는 산업용 전자기기용 세라믹형 배터리를 상용화하고 있습니다. 베트남과 태국은 중국으로부터의 생산 거점 분산이 가속화되는 가운데 조립 능력 유치를 추진하고 있지만, 업스트림 원자재는 여전히 동북아시아에 집중되어 있습니다.

북미는 박막 배터리 시장에서 방위 및 의료 기술 분야의 틈새 시장을 장악하고 있습니다. DARPA의 자금 지원과 실리콘밸리의 스타트업들이 안정적인 수요를 창출하고 있는 반면, NDAA(국방수권법)에 따라 Amprius사가 건설 중인 실리콘 음극 제조 시설은 박막 배터리가 성숙 단계에 접어들었을 때 국내 생산으로의 회귀가 가져올 시너지 효과를 시사하고 있습니다. 남미에서 진행 중인 브라질의 스마트 농업 시범 프로젝트나 중동의 유전에서의 IoT 도입 사례에서는 고온 내성을 갖춘 세라믹 박막 배터리가 채택되고 있습니다. 아프리카는 아직 발전의 초기 단계이지만, 재생에너지를 활용한 마이크로그리드가 향후 센서 수요를 창출하여 유연성이 높은 마이크로 배터리 수요 증가로 이어질 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the thin film battery market size is projected to expand from USD 268.03 million in 2025 and USD 315.68 million in 2026 to USD 774.45 million by 2031, registering a CAGR of 19.66% between 2026 and 2031.

This report is Segmented by Battery Type (Rechargeable, Non-Rechargeable), Technology (Printed Battery, Ceramic Battery, Other Technologies), Application (Consumer Electronics, Medical Devices, Wearable Technology, Smart Cards, RFID, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Thin Film Battery Market Trends and Insights

Surge in Wearable & IoT Device Production

Global shipments of smartwatches, earbuds, service robots, and industrial sensors are creating sustained pull for sub-1 Ah planar cells. TDK's thin-film inductors introduced for true-wireless-stereo earbuds make mechanical coin cells obsolete in devices where every cubic millimeter counts. Ensure batteries reach 90% charge in under 25 minutes, supporting daily-wear gadgets without bulky housings. Samsung SDI forecasts robot demand rising from 500,000 units in 2025 to 2.04 million by 2030, and it unveiled a solid-state pouch cell to serve that wave. Energy-harvesting modules such as Dracula Technologies' LayerVault OPV sheets buffer intermittent power for logistics sensors, lifting thin film battery market volumes across consumer and industrial use cases. The synergy between ambient-light harvesters and flexible micro-cells underpins the replacement of CR2032 batteries in temperature loggers and asset tags.

Miniaturization Trend in Consumer Electronics

Device makers are setting chassis thickness targets below 5 mm for smart cards, AR glasses, and biometric tags, forcing a pivot to flat battery geometries. BTRY's 1S4P cell, barely 0.1 mm thick yet delivering 50 mAh in one-minute charges, exemplifies innovation that unlocks active security authentication inside ID cards. Planar cells laminate directly onto flex circuits, skip wire-bond fixtures, and cut assembly time, giving OEMs a compelling cost-of-ownership story even when volumetric energy is lower than 18650 standards. The design freedom enables curved smartwatch backs and bezel-less displays while maintaining device rigidity. Because the operating profile is intermittent rather than continuous, consumers accept daily re-charging in exchange for lighter wearables, driving repeat orders across the thin film battery market.

Limited Energy Density Versus Bulk Li-ion Batteries

Thin-film cells provide 100-200 Wh/L, about one-third of advanced 21700 cylindrical formats now touching 320 Wh/kg. Ionic conductivity in LiPON remains at the 10-6 S/cm level, capping discharge rates and precluding use in power tools. As EV-grade packs adopt silicon-graphite anodes, the performance contrast widens, making it harder for the thin film battery market to win long-duration or high-drain slots. Smartwatch makers chasing multiday runtimes sometimes revert to coin cells, and AR headset OEMs blend small lithium-polymer pouches for auxiliary loads. Composite electrolyte R&D could double conductivity, yet commercialization after 2027 offers no relief during the current forecast window.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Solid-State Micro-Batteries in Medical Implants

- Roll-to-Roll PVD Scale-Ups Reducing Per-Unit Costs

- High CAPEX for Vacuum Deposition Tooling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rechargeable thin-film cells accounted for 73.57% of 2025 revenue and are forecast to grow at 20.69% CAGR, reinforcing their dominance in the thin film battery market. This cohort benefits from smartwatch, humanoid-robot, and medical-implant workloads that demand thousands of charge cycles. Samsung SDI's SolidStack prototypes deliver eight-hour duty cycles in service robots and promise fast top-ups during shift changes. Non-rechargeable primary cells still power disposable smart packaging where unit economics dictate pennies per label, yet their share in the thin film battery market is shrinking as IoT device operators calculate life-cycle cost advantages of rechargeability.

ISO/IEC 7810 durability tests and UN 38.3 transport certification shape R&D roadmaps, pushing vendors to validate thermal stability above 1,000 cycles and shelf life beyond five years. Defense logistics add momentum as the STUB standard adopts rechargeable formats to slash field battery shipments. Consequently, the thin film battery industry is funneling R&D budgets toward cycle-life extension through LiPON refinement and anode-free stack designs, reinforcing the share supremacy of secondary chemistries.

Geography Analysis

Europe generated 52.11% of thin film battery market revenue in 2025, underpinned by the EU Batteries Regulation (2023/1542) that enforces carbon-footprint disclosure and battery passports from 2027. Switzerland's BTRY raised USD 5.7 million to industrialize solvent-free roll-to-roll solid-state cells, showing deep-tech vigor in the region. France's ITEN and the UK's Battery Industrialisation Centre pushed Ilika's Goliath prototypes toward 93% pilot-line yield, anchoring supply resilience. Nordic producers tout hydropower-sourced electricity for low-carbon credentials, but mining permits for lithium and cobalt remain a bottleneck.

Asia-Pacific is the momentum engine, expanding at 22.35% CAGR and reshaping the thin film battery market landscape. Samsung SDI presented a pouch-type all-solid-state prototype for humanoid robots at InterBattery 2026 and owns about 1,100 patents, fortifying its moat. China scales printed-battery output for connected packaging under Made in China 2025 subsidies, while Japan's TDK commercializes ceramic variants for industrial electronics. Vietnam and Thailand lure assembly capacity as diversification away from China accelerates, although upstream materials remain concentrated in Northeast Asia.

North America captures defense and med-tech niches within the thin film battery market. DARPA funding and Silicon Valley start-ups provide steady demand, while Amprius' silicon-anode facility under NDAA alignment hints at onshoring synergies should thin-film versions mature. South America's pilot projects in Brazilian smart agriculture and the Middle East's oil-field IoT deployments use ceramic thin-film batteries for high-temperature resilience. Africa remains embryonic, though renewable-energy micro-grids may later seed sensor demand that benefits flexible micro-batteries.

- STMicroelectronics

- Panasonic Corporation

- Samsung SDI Co., Ltd.

- Cymbet Corporation

- BrightVolt Inc.

- Ilika plc

- Imprint Energy, Inc.

- Enfucell Oy

- Kurt J. Lesker Company

- Blue Spark Technologies

- Front Edge Technology

- Thinfilm Electronics ASA

- BASQUEVOLT

- EIT InnoEnergy SE

- The Batteries Sp. z o. o.

- Renata SA

- Power Paper Ltd.

- VARTA AG

- EnerVenue Inc.

- NEO Battery Materials Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in wearable & IoT device production

- 4.2.2 Miniaturization trend in consumer electronics

- 4.2.3 Rising demand for solid-state micro-batteries in medical implants

- 4.2.4 Roll-to-roll PVD scale-ups reducing per-unit costs

- 4.2.5 Integration with energy-harvesting IIoT sensors

- 4.2.6 Defense funding for soldier-worn power sources & smart munitions

- 4.3 Market Restraints

- 4.3.1 Availability of alternative battery chemistries

- 4.3.2 Limited energy density versus bulk Li-ion batteries

- 4.3.3 High CAPEX for vacuum deposition tooling

- 4.3.4 LiPON electrolyte patent bottlenecks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Rechargeable

- 5.1.2 Non-Rechargeable (Primary)

- 5.2 By Technology

- 5.2.1 Printed Battery

- 5.2.2 Ceramic Battery

- 5.2.3 Lithium-Polymer Battery

- 5.2.4 Solid-State Chip Battery

- 5.2.5 Other Technologies

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Medical Devices

- 5.3.3 Wearable Technology

- 5.3.4 Smart Cards

- 5.3.5 RFID

- 5.3.6 IoT Sensors

- 5.3.7 Military & Defense

- 5.3.8 Smart Packaging

- 5.3.9 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Nordic Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JV, Funding)

- 6.3 Market Ranking/Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 STMicroelectronics

- 6.4.2 Panasonic Corporation

- 6.4.3 Samsung SDI Co., Ltd.

- 6.4.4 Cymbet Corporation

- 6.4.5 BrightVolt Inc.

- 6.4.6 Ilika plc

- 6.4.7 Imprint Energy, Inc.

- 6.4.8 Enfucell Oy

- 6.4.9 Kurt J. Lesker Company

- 6.4.10 Blue Spark Technologies

- 6.4.11 Front Edge Technology

- 6.4.12 Thinfilm Electronics ASA

- 6.4.13 BASQUEVOLT

- 6.4.14 EIT InnoEnergy SE

- 6.4.15 The Batteries Sp. z o. o.

- 6.4.16 Renata SA

- 6.4.17 Power Paper Ltd.

- 6.4.18 VARTA AG

- 6.4.19 EnerVenue Inc.

- 6.4.20 NEO Battery Materials Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment