|

시장보고서

상품코드

2066752

미국의 지붕재 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

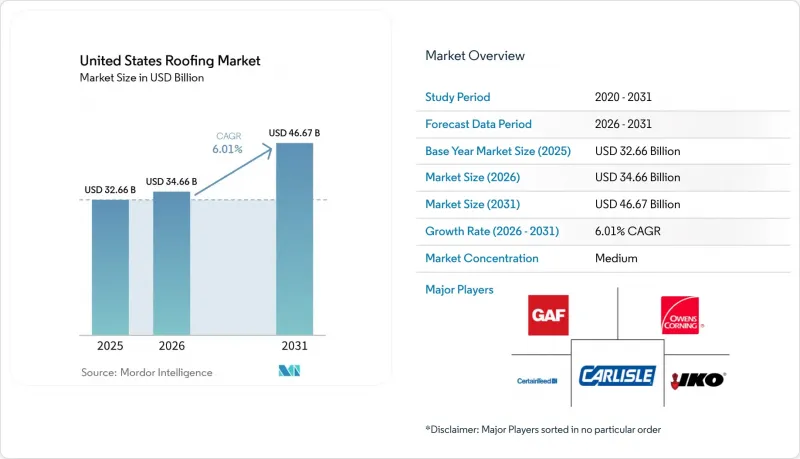

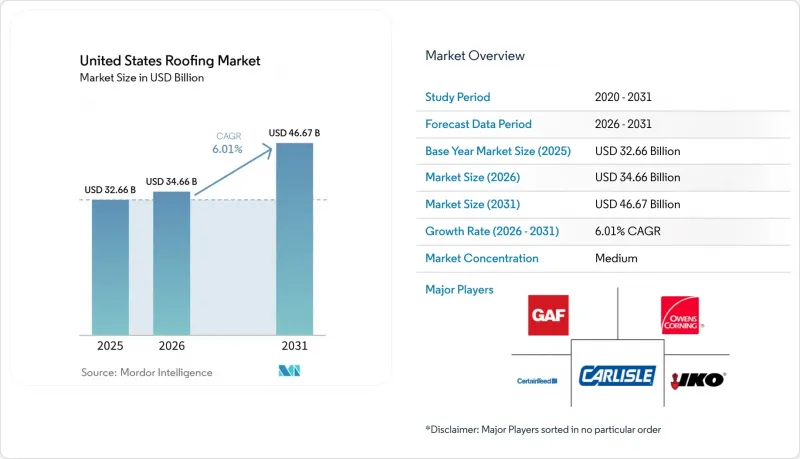

Mordor Intelligence에 의하면, 미국의 지붕재 시장 규모는 2025년 326억 6,000만 달러로 평가되었고, 2026년에는 346억 6,000만 달러로 추정되고, 2026-2031년 CAGR 6.01%로 성장을 지속할 전망이며, 2031년에는 466억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 자재 유형별(아스팔트 슁글, 점토·콘크리트 기와 등), 시공 유형별(신축, 지붕 재시공, 교체), 용도별(주거용, 상업시설, 산업 시설, 공공시설, 기타) 및 지역별(북동부, 중서부, 남동부, 서부, 남서부)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 지붕재 시장 동향과 인사이트

노후된 지붕재 재고와 교체 주기의 장기화가 지붕 재시공 수요를 뒷받침하고 있습니다.

미국 내 자가 소유 주택의 3분의 1 이상이 2000년 이전에 지어졌으며, 2025년에는 지붕의 평균 사용 연수가 17년을 넘어 수백만 채의 지붕이 정상적인 수명을 초과하게 되었습니다. 이러한 인구 동향의 변화로 인해 주택 착공 건수가 둔화되더라도, 업체들은 일정 수준의 기본적인 업무량을 확보할 수 있습니다. 주택 소유주들은 지붕 철거 공사 시 적층 싱글이나 금속 지붕으로 교체하는 경우가 많으며, 이로 인해 공사 비용이 두 자릿수 증가세를 보이고 있습니다. 또한, 보험사는 현재 지은 지 15년 이상 된 주택의 보험 계약 갱신 시 지붕 점검을 의무화하고 있어, 지붕 파손 발생 시 대응까지 걸리는 시간이 단축되고 있습니다. 그 결과, 꾸준한 지붕 교체 수요가 미국 지붕재 시장의 기반을 지탱하고 있습니다.

폭풍우와 우박 피해로 인해 보험을 통한 지붕 공사가 증가

2024-2025년 텍사스주, 오클라호마주, 아이오와주에서는 격렬한 대류성 폭풍으로 인해 지붕 관련 보험 청구액이 150억 달러 이상에 달했습니다. 이에 대해 각 보험사는 고위험 지역에서 UL 2218 클래스 4 인증을 받은 내충격성 지붕재의 사용을 의무화함으로써 대응했습니다. 이러한 고급 제품의 가격은 약 18% 더 비싸지만, 주택 소유자에게는 상당한 금액의 보험료 할인이 적용되기 때문에 지출은 수익성이 높은 자재로 향하고 있습니다. 또한, 허리케인 ‘이안’ 이후 플로리다주의 풍력 내력 기준 개정으로 인해, 기준을 충족하지 못하는 지붕을 조기에 교체해야 하는 상황이 되었습니다. 이러한 요인들이 복합적으로 작용하여 지붕 교체 주기가 빨라지고, 1제곱미터당 가치가 상승하고 있습니다.

숙련된 노동자의 부족으로 인해 도급업체의 수주 능력이 제한되고, 비용이 상승하고 있습니다.

지붕 공사 업체에서는 시급을 28달러로 인상했음에도 불구하고, 2025년 인력 공백률은 12%를 기록했습니다. 인력 부족이 가장 심각한 곳은 한랭 지역으로, 고령화되는 노동력을 대체할 인력이 부족합니다. 시공업체들은 인력 부족을 메우기 위해 로봇 시공 장비와 자재 리프트를 도입하고 있지만, 설비 비용 증가로 인해 간접비가 상승하고 있습니다. 8-12주에 달하는 납기 연장으로 인해 일부 소유주들은 공사를 연기할 수밖에 없게 되었고, 그 결과 단기적인 공사량이 감소하면서 미국 지붕 공사 시장의 성장세가 둔화되고 있습니다.

부문별 분석

2025년, 아스팔트 슁글은 미국 지붕재 시장에서 58.6%의 점유율을 차지했으며, 모든 소재 중에서 확고한 1위 자리를 지켰습니다. 이러한 규모는 광범위한 시공업체 네트워크, 익숙한 시공 방식, 주택용 유통망의 강점, 그리고 여전히 지붕 타일 교체에 크게 의존하고 있는 지붕 재시공 주기를 반영하고 있습니다. 오웬스 코닝사에 따르면, 2024년 미국 아스팔트 슁글 시장은 총 1억 6,000만 스퀘어에 달했으며, 이 중 1억 3,500만 스퀘어는 지붕 교체 및 보수 공사에서 비롯된 것이었습니다. 이는 시장 규모의 상당 부분이 신축이 아닌 정기적인 재시공 공사에 의존하고 있음을 보여줍니다. 또한 오웬스 코닝사는 2025년 라미네이트 제품이 싱글 제품 수요의 95%를 차지했다고 지적하며, 미국 지붕재 시장이 이미 표준적인 3탭 제품에서 부가가치가 높은 라미네이트 시스템으로 전환되고 있음을 보여주고 있습니다. 이 구성 비율이 중요한 이유는 라미네이트 제품이 판매 가격이 더 높고 내충격 성능이 뛰어나며, 우박 피해가 잦은 주에서 보험사가 요구하는 요건에도 더 잘 부합하기 때문입니다.

미국의 싱글플라이 멤브레인 지붕재 시장은 2031년까지 연평균 성장률(CAGR) 7.69%를 나타낼 것으로 예측되며, 이 부문은 가장 빠르게 성장하는 건축자재 부문이 될 전망입니다. 이러한 확대는 경사가 완만한 상업용 건축물에서 건축 기준을 충족하는 수준이 높아지고 있음을 반영한 것으로, 반사형 열가소성 폴리올레핀(TPO), 에틸렌·프로파일렌·디엔·모노머(EPDM), 그리고 폴리염화비닐(PVC) 시스템이 많은 기존 대체재보다 효율성과 유지보수 요건을 더 적절히 충족시키고 있기 때문입니다. 캘리포니아주의 현재 건축 기준 방향성과 연방 효율 기준은 특히 소유주가 동일한 프로젝트 내에서 규정 준수와 냉방 부하 감소를 동시에 추구할 경우, 지붕 재시공 사양을 이러한 시스템으로 전환하는 데 도움이 되고 있습니다. 2024년 9월 생산을 시작한 조지아주 발도스타에 위치한 GAF사의 425,000제곱피트 규모의 열가소성 폴리올레핀(TPO) 공장은 제조업체가 이러한 변화에 대응하여 실질적인 생산 능력을 확대하고 있음을 보여줍니다. 금속, 개질 아스팔트, 타일, 목재 및 기타 자재는 특정 지역의 틈새 시장에서 여전히 중요한 위치를 차지하고 있습니다. 그러나 미국의 지붕재 시장에서는 판매량 측면에서 여전히 아스팔트 슁글에 의존하고 있으며, 향후 가장 강력한 성장이 예상되는 것은 방수 시트입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트 및 시장 역학

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the united states roofing market size is expected to grow from USD 32.66 billion in 2025 to USD 34.66 billion in 2026 and is forecast to reach USD 46.67 billion by 2031 at 6.01% CAGR over 2026-2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, and More), by Construction Type (New Construction, Reroofing, and Replacement), by Application (Residential, Commercial, Industrial, Institutional, Others), and by Geography (North East, Mid West, South East, West, South West). The Market Forecasts are Provided in Terms of Value (USD).

United States Roofing Market Trends and Insights

Aging Roof Stock and Higher Replacement Cycles Sustaining Reroofing Demand

More than one-third of U.S. owner-occupied homes were built before 2000, and the median roof age exceeded 17 years in 2025, moving millions of coverings beyond their typical service life. This demographic swell assures baseline work for contractors even when housing starts slow. Homeowners often upgrade to laminated shingles or metal during tear-offs, lifting ticket values by double digits. Insurers now request roof inspections when policies renew on homes older than 15 years, shortening the lag between failure and action. As a result, consistent replacement volume underpins the United States roofing market .

Storm and Hail Events Increasing Insurance-Funded Roofing Activity

Severe convective storms generated more than USD 15 billion in roof-related claims across Texas, Oklahoma, and Iowa during 2024-2025. Carriers responded by insisting on impact-resistant shingles certified to UL 2218 Class 4 in high-risk zones. These premium products cost around 18% more but earn homeowners sizable premium credits, directing spend toward higher-margin materials. Florida's revised wind codes after Hurricane Ian are also forcing early replacements of non-compliant roofs. Collectively, these conditions accelerate reroof cycles and elevate value per square.

Skilled Labor Shortages Limiting Contractor Capacity and Raising Costs

Roofing firms recorded vacancy rates of 12% in 2025 despite wage hikes to USD 28 per hour. Scarcity is sharpest in colder regions where an aging workforce lacks replacements. Contractors are buying robotic applicators and material lifts to offset head-count gaps, but equipment costs raise overhead. Extended lead times of eight to twelve weeks push some owners to defer projects, trimming near-term volume and tempering growth for the United States roofing market.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Upgrades Boosting Demand for Cool Roofs and Better Insulation Systems

- Growth in Logistics Warehouses and Data Centers Expanding Commercial Roofing Installations

- Volatility in Asphalt, Metal, and Insulation Input Prices Pressuring Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Asphalt shingles held 58.6% of the United States roofing market share in 2025, keeping them firmly in the lead across materials. Their scale reflects a wide installer network, familiar installation methods, strong residential distribution, and a reroofing cycle that still leans heavily toward shingle replacement. Owens Corning stated that the U.S. asphalt shingle market totaled 160 million squares in 2024, with 135 million squares from reroof and repair activity, indicating how much of the material base is tied to recurring replacement work rather than new construction. Owens Corning also noted in 2025 that laminate products accounted for 95% of shingle demand, indicating that the United States roofing market has already shifted away from standard 3-tab products toward higher-value laminated systems. That mix matters because laminates support better selling prices, stronger impact ratings, and better alignment with insurer preferences in hail-prone states.

The United States roofing market for single-ply membranes is forecast to grow at a 7.69% CAGR through 2031, making that group the fastest-growing material category. This expansion reflects stronger code alignment in low-slope commercial work, where reflective Thermoplastic Polyolefin, Ethylene Propylene Diene Monomer, and Polyvinyl Chloride systems better meet efficiency and maintenance requirements than many legacy alternatives. California's current code direction and federal efficiency standards are helping move reroof specifications toward those systems, especially where owners want compliance and lower cooling loads in the same project. GAF's 425,000-square-foot Thermoplastic Polyolefin plant in Valdosta, Georgia, which began production in September 2024, demonstrates that manufacturers are adding real capacity to this shift. Metal, modified bitumen, tile, wood, and other materials remain important in specific regional niches. However, the United States roofing market still relies on asphalt shingles for volume and on membranes for the strongest forward growth.

List of Companies Covered in this Report:

- GAF Materials Corporation

- Owens Corning

- CertainTeed Corporation

- Carlisle Companies Inc.

- IKO Industries Ltd.

- Tamko Building Products

- Johns Manville

- Firestone Building Products (Holcim)

- Sika AG

- Soprema Group

- Atlas Roofing Corporation

- Beacon Building Products

- CentiMark Corporation

- Tecta America

- Flynn Group of Companies

- Baker Roofing Company

- Nations Roof

- IronHead Roofing

- Malarkey Roofing Products

- Best Contracting Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights & Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging roof stock and higher replacement cycles sustaining reroofing demand

- 4.2.2 Storm and hail events increasing insurance-funded repairs and re-roof activity

- 4.2.3 Energy-efficiency upgrades boosting demand for cool roofs and better insulation systems

- 4.2.4 Growth in logistics warehouses and data centers expanding commercial roofing installations

- 4.2.5 Adoption of solar-ready and rooftop PV-integrated roofing increasing upgrade spending

- 4.3 Market Restraints

- 4.3.1 Skilled labor shortages limiting contractor capacity and raising installation costs

- 4.3.2 Volatility in asphalt shingles, metal, and insulation input prices pressuring margins

- 4.3.3 Permitting, insurance, and warranty requirements extending project timeline

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North East

- 5.4.2 Mid West

- 5.4.3 South East

- 5.4.4 West

- 5.4.5 South West

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 GAF Materials Corporation

- 6.3.2 Owens Corning

- 6.3.3 CertainTeed Corporation

- 6.3.4 Carlisle Companies Inc.

- 6.3.5 IKO Industries Ltd.

- 6.3.6 Tamko Building Products

- 6.3.7 Johns Manville

- 6.3.8 Firestone Building Products (Holcim)

- 6.3.9 Sika AG

- 6.3.10 Soprema Group

- 6.3.11 Atlas Roofing Corporation

- 6.3.12 Beacon Building Products

- 6.3.13 CentiMark Corporation

- 6.3.14 Tecta America

- 6.3.15 Flynn Group of Companies

- 6.3.16 Baker Roofing Company

- 6.3.17 Nations Roof

- 6.3.18 IronHead Roofing

- 6.3.19 Malarkey Roofing Products

- 6.3.20 Best Contracting Services

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment