|

시장보고서

상품코드

2066763

하이브리드 전기자동차 배터리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

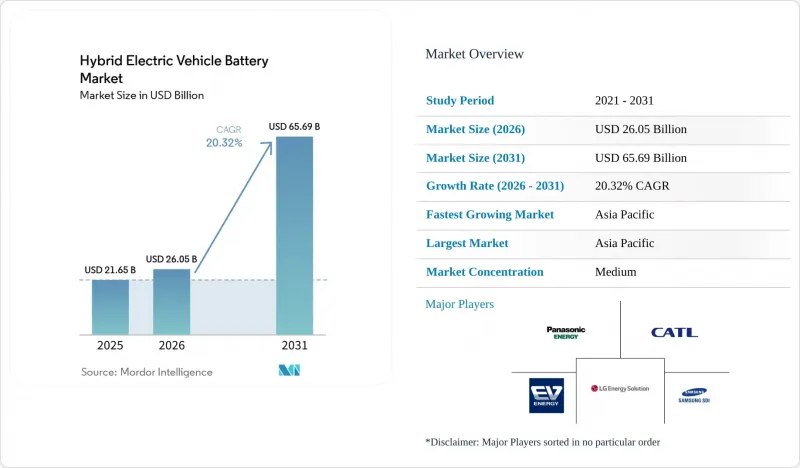

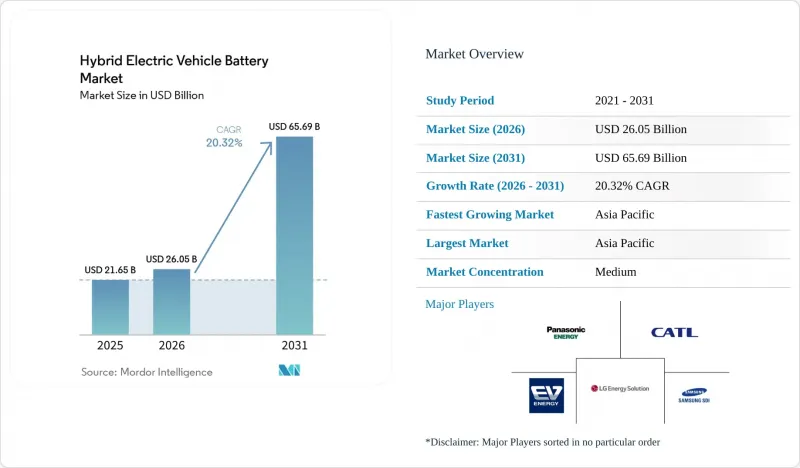

Mordor Intelligence에 의하면, 2026년 하이브리드 전기자동차 배터리 시장 규모는 260억 5,000만 달러에 달할 것으로 예상됩니다. 2025년 216억 5,000만 달러에서 확대해, 2031년에는 656억 9,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 20.32%로 성장할 것으로 전망됩니다.

본 보고서는 배터리의 화학 조성(리튬 이온, 니켈 수소, 납산 등), 하이브리드화 정도(마일드 하이브리드, 풀 하이브리드 등), 전압 등급(60V 이하, 60-200V, 200-400V, 400V 이상), 차량 등급(승용차, 상용차, 이륜차·삼륜차 등), 지역(북미, 유럽, 아시아태평양, 남미 등)별로 분류되어 있습니다.

세계의 하이브리드 전기자동차 배터리 시장 동향 및 인사이트

CO2 규제 하에서 확대되는 HEV 생산 대수

유럽연합(EU), 중국, 캘리포니아주의 이산화탄소 규제로 인해 자동차 제조업체들은 판매 대수의 100%를 무공해 차량으로 전환한다는 목표 달성을 위해 부족한 부분을 메우기 위해 하이브리드 차량의 생산 규모를 확대되고 있습니다. 차량 1대당 CO2 배출량이 규제치를 초과할 경우, 1그램당 95유로의 벌금이 부과되므로 하이브리드 차량에는 분명한 경제적 이점이 있습니다. 도요타가 파나소닉과 체결한 40GWh 규모의 리튬 이온 배터리 조달 계약, 스텔란티스의 120만 대 규모의 하이브리드 생산 능력은 이러한 추세를 상징하는 사례입니다. 중국의 이중 크레딧 제도는 장거리 주행이 가능한 플러그인 하이브리드 차량에 더 많은 혜택을 부여하고 있어, 각 OEM 업체들이 배터리 팩을 대형화하도록 유도하고 있습니다. 이러한 정책들의 시너지 효과로 인해, 주요 브랜드 대다수에서 하이브리드 차량 출시 속도가 빨라지고 있습니다.

리튬 이온 배터리의 $/kWh 단가 급락과 에너지 밀도 향상

호주와 칠레에서 새로운 채굴 능력이 확대됨에 따라 탄산리튬 공급 부족이 완화됨에 따라, 2024년 리튬 이온 배터리 팩 가격은 전년 대비 20% 하락하여 1kWh당 115달러를 기록했습니다. 이는 2017년 이후 가장 급격한 하락입니다. 비용 학습 곡선에 따르면, 누적 생산량이 2배가 될 때마다 가격은 약 25% 하락하는 것으로 나타났습니다. CATL의 ‘Qilin’ 설계(셀-투-팩 방식)를 통해 에너지 밀도가 255 Wh/kg로 향상되었으며, 배터리 팩을 과도하게 설계하지 않고도 플러그인 하이브리드 차량에서 100 km의 순수 전기 주행 거리를 실현하고 있습니다. 중국에서는 LFP 셀 가격이 kWh당 100달러 아래로 떨어지면서, 그동안 납산 배터리가 독점해 온 마일드 하이브리드 차량 및 이륜차 시장으로의 진출 기회가 확대되고 있습니다.

BEV 경쟁 환경에서의 주요 금속 공급 리스크

리튬 수요는 2030년까지 330만 톤에 달할 가능성이 있으며, 이는 2022년 사용량의 6배에 해당합니다. 또한, BEV는 하이브리드 차량에 비해 차량 1대당 리튬 소비량이 3-5배 더 많습니다. 코발트 공급은 여전히 콩고민주공화국(DRC)에 집중되어 있는 반면, 니켈 가공은 인도네시아가 주도하고 있습니다. 가격 변동은 장기 공급 계약을 복잡하게 만들고 있습니다. 리튬 탄산염 가격은 2022년 톤당 8만 달러에서 2024년 말에는 1만 달러로 급락하여 신규 광산 투자를 저해했습니다. 하이브리드 차량의 배터리 팩이 소형화됨에 따라 절대적인 위험은 줄어들었지만, BEV 제조업체가 다년 계약을 체결한 경우 현물 가격 변동의 영향을 피할 수는 없습니다.

부문별 분석

2025년 하이브리드 전기자동차용 배터리 시장에서 리튬이온 기술이 매출의 75.12%를 차지했으나, 고체 배터리 및 나트륨이온 배터리는 2031년까지 연평균 34.1%의 성장률을 보일 것으로 전망됩니다. 각 리튬 이온 배터리 제조업체들은 NMC 및 LFP의 배합을 지속적으로 개선하여 코발트 사용량을 줄이는 동시에 체적 효율을 높이고 있습니다. 도요타와 닛산은 2028년까지 전고체 배터리의 상용화를 시작할 계획이며, 배터리 팩의 크기를 늘리지 않고도 순수 전기 주행 거리를 2배로 늘릴 수 있는 500 Wh/kg의 셀 개발을 목표로 하고 있습니다. CATL의 나트륨 이온 배터리 시제품은 이미 160 Wh/kg의 에너지 밀도와 저온 환경에서의 뛰어난 성능 유지 능력을 실현해냈으며, 한랭 지역에서 보급형 하이브리드 차량에 적용될 것으로 기대되고 있습니다. 니켈-수소 전지는 주로 동남아시아 등, 에너지 밀도보다 가성비와 열적 안정성이 더 중요하게 여겨지는 지역에서 여전히 사용되고 있습니다. 납산 배터리는 보조용 12V 시스템으로만 사용됩니다. 리튬 이온 배터리에 기반한 하이브리드 전기자동차용 배터리 시장 규모는 2031년까지 468억 달러에 육박할 것으로 예상되는 반면, 신흥 화학계 배터리는 같은 해 총 73억 5,000만 달러를 넘어설 것으로 전망됩니다.

치열한 특허 환경이 경쟁의 양상을 형성하고 있습니다. 도요타는 1,300건 이상의 전고체 배터리 관련 특허를 보유하고 있는 반면, CATL과 BYD는 셀에서 팩에 이르는 주요 설계를 장악하고 있습니다. 소송을 피하고자 하는 후발 기업들에게 라이선싱은 현실적인 대안이 되어가고 있습니다. 전반적으로, 하이브리드 전기자동차용 배터리 업계에서는 여러 화학 계열이 공존하는 상황이 예상됩니다. 리튬 이온 배터리는 수량 면에서 주도권을 유지할 것이지만, 전고체 배터리의 규모가 확대되면 이익률 면에서의 주도권은 전고체 배터리에 넘어가게 될 것입니다.

2025년에는 마일드 하이브리드 차량이 판매 대수의 43.12%를 차지하며, CO₂ 배출 목표를 신속히 달성해야 하는 차량 운영 업체들에게 가장 비용 효율적인 규제 대응 수단이 되었습니다. 마일드 하이브리드로 인해 창출되는 하이브리드 전기자동차용 배터리 시장 규모는 2031년에는 222억 4,000만 달러를 넘어설 것으로 예상되며, 연평균 성장률(CAGR) 22.6%로 확대될 것으로 전망됩니다. 풀 하이브리드는 20년에 걸친 신뢰성 데이터를 바탕으로 일본과 북미에서 여전히 큰 인기를 끌고 있습니다. 플러그인 하이브리드 차량은 유럽에서는 기업용 차량 함대에 대한 세제 혜택의 수혜를 받고 있지만, 급속 충전 네트워크가 제대로 구축되지 않은 신흥 시장에서는 어려움을 겪고 있습니다. 레인지 익스텐더 방식은 Li Auto를 필두로 주로 중국에서 활발히 채택되고 있지만, 이 방식의 세계적 전망은 배출권 처리 방식에 따라 달라질 것입니다. 자동차 제조업체들은 규모의 경제를 확보하기 위해 하이브리드 차종 간에 동일한 셀 형식을 채택하고 있지만, 소프트웨어 캘리브레이션에는 현저한 차이가 있어 이로 인해 엔지니어링의 복잡성이 증가하고, 수직 통합형 공급업체가 유리한 입장에 있습니다.

PHEV의 성장은 규제 당국이 다음 단계의 기준에서도 저탄소 배출량에 대한 시험 주기 평가치를 계속 인정할지 여부에 따라 좌우될 것입니다. 독일에서는 2024년에 구매 보조금이 단계적으로 폐지됨에 따라 PHEV 등록 대수가 절반으로 줄어들었으며, 이는 정책 변화에 대한 민감성을 보여주었습니다. 신흥국에서는 충전이 필요 없고 kWh 용량이 작은 배터리 팩을 탑재한 기존 하이브리드 차량이 여전히 실용적인 전동화로 나아가는 첫걸음이 되고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 47.35%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 22.3%를 나타낼 것으로 전망됩니다. 이는 중국이 배터리 생산 점유율의 75%를 차지하고, CATL이 공급업체 점유율의 37.5%를 차지하고 있다는 점이 원동력이 되고 있습니다. 한국 및 일본공급업체들은 지정학적 장벽을 피하기 위해 미국과 유럽에서 현지 생산을 확대하고 있지만, 고부가가치 전극 및 분리막에 대해서는 계속해서 국내 공장에서 출하하고 있습니다. 인도의 급성장하는 이륜차 부문은 수입에 의존하고 있으며, 24억 달러 규모의 생산 연계형 인센티브 제도를 통해 그 공급 격차를 해소하는 것을 목표로 하고 있습니다.

2025년 매출액에서 유럽이 차지하는 비중은 28.15%였습니다. 보조금 중단은 플러그인 차량 수요에 타격을 주었지만, 법인용 차량의 경우 여전히 세제상의 우대 조치 덕분에 PHEV가 선호되고 있습니다. EU의 배터리 규제에 따라 탄소 발자국 공개와 재활용 기준이 의무화됨에 따라, 기가팩토리 운영 사업자들은 폐쇄형 모델로의 전환을 요구받고 있습니다. 노스볼트의 파산은 아시아산 수입으로 인한 비용 압박을 여실히 드러내고 있지만, LG에너지솔루션과 삼성SDI는 해당 지역공급을 유지하기 위해 폴란드와 헝가리에서 대규모 프로젝트를 추진하고 있습니다.

북미는 2025년 매출의 17.65%를 차지했습니다. '인플레이션 억제법'의 부품 원산지 규정에 따라 LG 에너지솔루션, 삼성SDI, 파나소닉이 총 115억 달러 규모의 배터리 투자 계획을 발표했습니다. 멕시코는 누에보레온주에서 관세 면제 혜택을 받는 배터리 팩 조립을 추진함으로써, 니어쇼어링의 대체 거점으로서의 입지를 확립하고자 하고 있습니다. 남미와 중동 및 아프리카를 합친 점유율은 6.85%였습니다. 브라질의 에탄올 하이브리드차 도입 노력과 UAE의 전기 버스 도입은 지역별 다양한 전략을 여실히 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, hybrid electric vehicle battery market size in 2026 is estimated at USD 26.05 billion, growing from 2025 value of USD 21.65 billion with 2031 projections showing USD 65.69 billion, growing at 20.32% CAGR over 2026-2031.

This report is Segmented by Battery Chemistry (Lithium-Ion, Nickel-Metal Hydride, Lead-Acid, and More), Degree of Hybridization (Mild Hybrid, Full Hybrid, and More), Voltage Class (Up To 60V, 60 To 200V, 200 To 400V, and Above 400V), Vehicle Class (Passenger Cars, Commercial Vehicles, Two-/Three-Wheelers, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More).

Global Hybrid Electric Vehicle Battery Market Trends and Insights

Escalating HEV Production Volumes Under CO2 Mandates

CO2 regulations in the European Union, China, and California are prompting automakers to scale hybrid output to bridge the gap to 100% zero-emission sales targets. Non-compliance fines that hit EUR 95 per gram of CO2 overshoot per vehicle create a clear economic case for hybrids. Toyota's 40 GWh lithium-ion sourcing deal with Panasonic and Stellantis's 1.2 million-unit hybrid capacity are emblematic responses. China's dual-credit regime further rewards long-range plug-in hybrids, nudging OEMs to enlarge battery packs. These converging policies have raised hybrid launch velocity at most mainstream brands.

Rapid Fall in Li-ion $/kWh & Higher Energy Density

Lithium-ion pack prices fell 20% year over year to USD 115 per kWh in 2024, the sharpest decline since 2017, as new mining capacity in Australia and Chile relieved lithium carbonate shortages. Cost learning curves show that each doubling of cumulative output trims prices by roughly 25%. CATL's cell-to-pack Qilin design lifts energy density to 255 Wh/kg and demonstrates 100 km electric-only range in plug-in hybrids without oversizing the pack. LFP cells have slipped below USD 100 per kWh in China, opening mild-hybrid and two-wheeler opportunities previously reserved for lead-acid units.

Critical-Metal Supply Risk Amid BEV Competition

Lithium demand could hit 3.3 million t by 2030, six times 2022 usage, and BEVs consume three to five times more per vehicle than hybrids. Cobalt remains heavily concentrated in the DRC, while Indonesia dominates nickel processing. Price volatility complicates long-term supply deals; lithium carbonate plunged from USD 80,000/t in 2022 to USD 10,000/t in late 2024, deterring fresh mine investment. Smaller hybrid packs reduce absolute exposure but do not escape spot-price swings when BEV makers lock in multi-year contracts.

Other drivers and restraints analyzed in the detailed report include:

- OEM Migration From NiMH to Li-ion Chemistries

- 48 V Micro-Hybrid Boom Creating Low-Cost Li-ion Demand

- Sparse PHEV Fast-Charge Infrastructure in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion technologies captured 75.12% of 2025 revenue for the hybrid electric vehicle battery market, yet solid-state and sodium-ion batteries are forecast to grow 34.1% annually to 2031. Lithium-ion vendors continue to refine NMC and LFP blends, cutting cobalt usage and improving volumetric efficiency. Toyota and Nissan plan solid-state commercial launches before 2028, targeting 500 Wh/kg cells that could double electric-only range without enlarging packs. Sodium-ion prototypes from CATL already deliver 160 Wh/kg and superior cold-weather retention, positioning the chemistry for entry-level hybrids in colder climates. Nickel-metal hydride endures where affordability and thermal stability trump energy density, chiefly in Southeast Asia. Lead-acid is relegated to auxiliary 12 V systems. The hybrid electric vehicle battery market size attributable to lithium-ion is expected to approach USD 46.8 billion by 2031, while emerging chemistries will jointly exceed USD 7.35 billion that year.

A tightening patent landscape is shaping competitive behavior. Toyota holds more than 1,300 solid-state-related patents, whereas CATL and BYD control key cell-to-pack designs. Licensing is becoming a realistic path for latecomers wishing to avoid litigation. Overall, the hybrid electric vehicle battery industry anticipates a multi-chemistry coexistence, with lithium-ion retaining volume leadership but ceding margin leadership to solid-state once scale materializes.

Mild hybrids achieved 43.12% unit volume in 2025, delivering the lowest-cost compliance option for fleets that must hit CO2 targets quickly. The hybrid electric vehicle battery market size generated by mild hybrids is projected to surpass USD 22.24 billion in 2031, rising at a 22.6% CAGR. Full hybrids remain popular in Japan and North America thanks to two decades of reliability data. Plug-in hybrids enjoy corporate-fleet tax benefits in Europe but struggle in emerging markets that lack fast-charging networks. Range-extender architectures thrive mainly in China, led by Li Auto, though their global prospects hinge on emissions-credit treatment. Automakers are bundling identical cell formats across hybrid types to secure scale economies, yet software calibration differs markedly, increasing engineering complexity and favoring vertically integrated suppliers.

PHEV growth will depend on whether regulators continue to count their low CO2 test-cycle ratings in the next phase of standards. Germany's phase-out of purchase rebates in 2024 cut PHEV registrations by half, showing sensitivity to policy shifts. In emerging economies, conventional hybrids with no charging requirement and low-kWh packs remain the practical electrification entry point.

Geography Analysis

Asia-Pacific accounted for 47.35% of 2025 revenue and is forecast to register a 22.3% CAGR through 2031, propelled by China's 75% cell-production share and CATL's 37.5% vendor position. Korean and Japanese suppliers are localizing output in the United States and Europe to evade geopolitical barriers, yet they continue to ship high-value electrodes and separators from domestic plants. India's fast-growing two-wheeler segment relies on imported cells, and its USD 2.4 billion production-linked incentive scheme seeks to fill that supply gap.

Europe held 28.15% of 2025 revenue. Subsidy withdrawals hurt plug-in demand, but corporate fleets still favor PHEVs for tax advantages. The EU Battery Regulation now obliges carbon-footprint declarations and recycling thresholds, pushing gigafactory operators into closed-loop models. Northvolt's insolvency underlines cost pressure from Asian imports, while LG Energy Solution and Samsung SDI advance large projects in Poland and Hungary to maintain regional supply.

North America generated 17.65% of 2025 sales. The Inflation Reduction Act's component-origin rules are drawing USD 11.5 billion of announced battery investment from LG Energy Solution, Samsung SDI, and Panasonic. Mexico is positioning itself as a near-shoring alternative by promoting duty-free pack assembly in Nuevo Leon. South America and the Middle East-Africa combined held 6.85% share; Brazil's ethanol-hybrid initiatives and the UAE's electric-bus rollouts illustrate diverse regional strategies.

- Primearth EV Energy (PEVE)

- Panasonic Energy Co.

- LG Energy Solution

- Contemporary Amperex Technology (CATL)

- Samsung SDI

- BYD Company Ltd

- AESC (Envision)

- Gotion High-Tech

- SK On

- EnerSys

- Saft Groupe SA

- Exide Industries

- East Penn Manufacturing

- Hitachi Astemo

- Amperex Technology Ltd (ATL)

- Amte Power

- Clarios

- Microvast

- Farasis Energy

- Romeo Power

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating HEV production volumes under CO2 mandates

- 4.2.2 Rapid fall in Li-ion $/kWh & higher energy density

- 4.2.3 OEM migration from NiMH to Li-ion chemistries

- 4.2.4 48 V micro-hybrid boom creating low-cost Li-ion demand

- 4.2.5 Recycling-mandate-driven secondary metals supply

- 4.2.6 AI-enabled cloud BMS extending battery warranties

- 4.3 Market Restraints

- 4.3.1 Critical-metal supply risk amid BEV competition

- 4.3.2 Sparse PHEV fast-charge infrastructure in EMs

- 4.3.3 Thermal-runaway design concerns in compact packs

- 4.3.4 Geopolitical scrutiny of Chinese battery IP

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (NMC, NCA, LFP, LTO)

- 5.1.2 Nickel-Metal Hydride (NiMH)

- 5.1.3 Lead-acid

- 5.1.4 Emerging Solid-State/Sodium-ion

- 5.2 By Degree of Hybridization

- 5.2.1 Mild Hybrid (48 V MHEV)

- 5.2.2 Full Hybrid (HEV)

- 5.2.3 Plug-in Hybrid (PHEV)

- 5.2.4 Range-Extender Hybrid

- 5.3 By Voltage Class

- 5.3.1 Up to 60 V

- 5.3.2 60 to 200 V

- 5.3.3 200 to 400 V

- 5.3.4 Above 400 V

- 5.4 By Vehicle Class

- 5.4.1 Passenger Cars

- 5.4.2 Commercial Vehicles

- 5.4.3 Two-/Three-Wheelers

- 5.4.4 Off-Highway and Specialty

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Norway

- 5.5.2.8 Russia

- 5.5.2.9 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Australia and New Zealand

- 5.5.3.7 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Primearth EV Energy (PEVE)

- 6.4.2 Panasonic Energy Co.

- 6.4.3 LG Energy Solution

- 6.4.4 Contemporary Amperex Technology (CATL)

- 6.4.5 Samsung SDI

- 6.4.6 BYD Company Ltd

- 6.4.7 AESC (Envision)

- 6.4.8 Gotion High-Tech

- 6.4.9 SK On

- 6.4.10 EnerSys

- 6.4.11 Saft Groupe SA

- 6.4.12 Exide Industries

- 6.4.13 East Penn Manufacturing

- 6.4.14 Hitachi Astemo

- 6.4.15 Amperex Technology Ltd (ATL)

- 6.4.16 Amte Power

- 6.4.17 Clarios

- 6.4.18 Microvast

- 6.4.19 Farasis Energy

- 6.4.20 Romeo Power

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment