|

시장보고서

상품코드

2066773

유럽의 하이브리드 전기자동차 배터리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

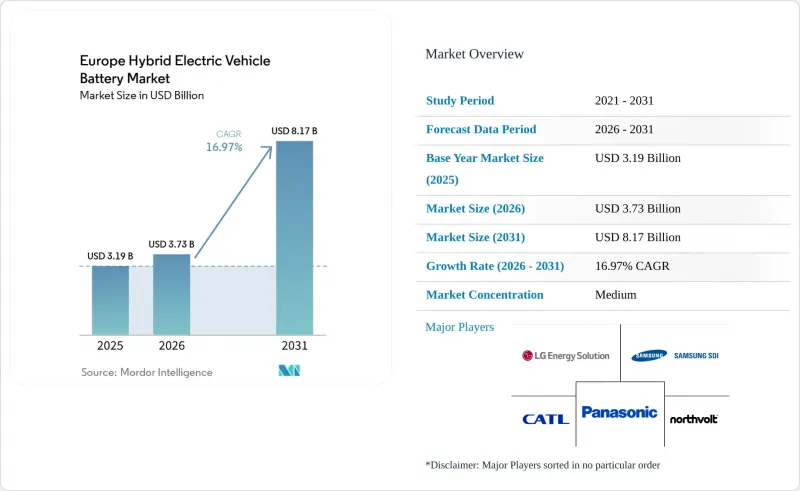

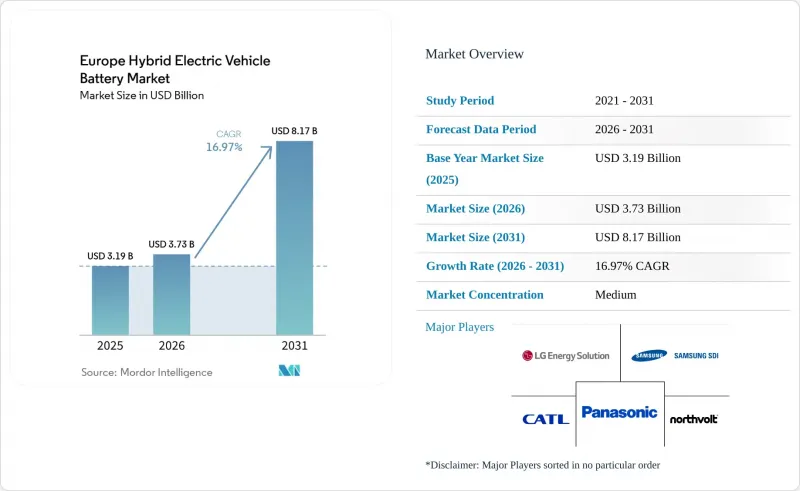

Mordor Intelligence에 의하면, 유럽의 하이브리드 전기자동차 배터리 시장 규모는 2025년 31억 9,000만 달러로 평가되었습니다. 2026년에는 37억 3,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 16.97%로 성장을 지속하여, 2031년까지 81억 7,000만 달러에 이를 것으로 예측됩니다.

(1) 유럽연합 집행위원회, "CO2 배출 성능 기준에 관한 제안', ec.europa.eu 마일드 하이브리드의 보급률은 풀 하이브리드나 플러그인 하이브리드를 웃돌며 상승하고 있습니다. 이는 이 기술이 풀 하이브리드 시스템 비용의 약 3분의 1 수준에서 10-15%의 연비 향상을 실현하고, 고가의 충전 인프라 구축을 피하면서도 이익률을 유지할 수 있기 때문입니다.(2) 스텔란티스, “2024년 전동화 전략”, stellantis.com. 배터리 제조업체들이 원자재 비용 절감과 공급망 회복탄력성 강화를 추구하는 가운데, 2025년에는 리튬 이온 배터리가 판매 대수의 78.2%를 차지하며 시장을 휩쓸었습니다. 본 보고서는 배터리의 화학 조성(리튬 이온, 니켈 수소, 납산 등), 하이브리드화 정도(마일드 하이브리드, 풀 하이브리드 등), 전압 등급(60V 이하, 60-200V, 200-400V, 400V 이상), 차량 등급(승용차, 상용차, 이륜차·삼륜차 등), 지역(독일, 영국, 스페인, 네덜란드 등)별로 분류되어 있습니다.

유럽의 하이브리드 전기자동차 배터리 시장 동향 및 인사이트

EU의 CO2 배출량 목표에 부합하는 HEV 생산 대수 증가

자동차 제조업체들은 2021년 115.1 g/km에서 하향 조정된 2025년 차량군 평균 배출량 상한선인 93.6 g/km를 달성해야 하며, 이를 초과할 경우 판매 대수 1대당 초과분 1그램당 95유로를 납부해야 합니다. 이에 따라 각 브랜드는 판매 대수가 많은 B부문 및 C부문 모델에서 하이브리드 파워트레인의 표준화를 추진하고 있습니다. 스텔란티스, 르노, 폭스바겐은 2024년에 48볼트 차량 라인업을 확대했습니다. 각 업체 모두 벨트식 스타터-제너레이터 시스템을 채택하여, 1,000유로 미만의 추가 비용으로 형식 인증 배출량을 약 12 g/km 줄이고 있습니다. 제로 배출 차량 및 저배출 가스 차량에 대한 슈퍼 크레딧은 2025년까지 적용 가능하므로, 현재 하이브리드 차량을 생산함으로써 BEV 인프라가 구축될 때까지 규제 준수를 위한 여유를 확보할 수 있습니다. 따라서, 이러한 규제 체계에 따라 적어도 2027년까지는 리튬 이온 배터리에 대한 기초적인 수요가 확보될 것이며, 그 이후에는 더욱 엄격해진 2030년 목표에 따라 전동화에 대한 압박이 더욱 커지게 될 것입니다.

중동부 유럽의 기가팩토리 투자 및 공급망 현지화

2024년에는 헝가리, 폴란드, 슬로바키아에 건설된 새로운 배터리 공장에 150억 유로 이상이 투자되었습니다. 그 중심에는 CATL의 데브레첸 공장(100 GWh)과 LG 에너지 솔루션의 브로츠와프 공장(70 GWh로 확장)이 있습니다. 서유럽에 비해 15-20% 낮은 인건비에 더해, 독일 조립 거점과의 적시(JIT) 공급이 가능한 근접성 덕분에 팩의 리드타임이 24시간 미만으로 단축되었습니다. ‘유럽 배터리 얼라이언스(European Battery Alliance)’의 공동 자금 지원을 통해 아시아산 원자재를 대체할 업스트림 공정의 양극 전구체 및 분리막 프로젝트가 가속화되고 있으며, 동시에 kWh당 내재된 CO2 배출량도 감소하고 있습니다. 탄소 발자국 공시가 의무화됨에 따라, 현지 공급망은 전략적 우위를 확보하고 있습니다.

중요 광물의 가격 변동

리튬 탄산염 가격은 2022년 말 톤당 8만 달러에서 2024년 12월까지 톤당 1만 달러 가까이 급락했습니다. 한편, 황산니켈 가격은 불과 1년 만에 톤당 7,000달러나 등락을 보였습니다. 이러한 가격의 급등락은 특히 수직 통합 체제가 없는 유럽의 중소 진출기업들에게 고정 가격 공급 계약의 이익률을 압박하고 있습니다. 현재 투자자들은 생산 능력 확대를 위한 자금 지원에 있어 가격 조정 조항이나 업스트림 광산에 대한 지분 확보를 요구하고 있으며, 그 결과 일부 기가팩토리의 가동 일정이 지연되고 있습니다.

부문별 분석

2025년 수요 중 리튬 이온 배터리가 77.60%를 차지하며, 고니켈 NMC 계열 배터리는 250-280 Wh/kg의 에너지 밀도가 필요한 플러그인 하이브리드 차량의 동력원으로 사용되었습니다. LFP는 3,000회 사이클의 내구성과 코발트가 포함되지 않은 공급망을 바탕으로 마일드 하이브리드 차량 시장에서의 점유율을 확대했습니다. 이는 스텔란티스사의 모델에서 시스템 비용을 30% 절감한 BYD의 ‘블레이드 팩’을 통해 입증된 성과입니다. 신기술인 나트륨 이온 전지와 전고체 전지는 연평균 30.90%의 성장률이 예상되지만, 2026년 이후 스웨덴의 노스볼트(Northvolt)사의 시범 생산 라인이 보급형 하이브리드 차량용 양산을 시작할 때까지는 규모가 제한된 상태가 지속될 전망입니다. 니켈수소 전지 시장 점유율은 7.60%로 떨어졌습니다. 이는 도요타가 유럽 시장용 신차 모델에서 리튬 이온 배터리로의 전환을 추진했기 때문입니다. 유럽의 하이브리드 전기자동차용 배터리 시장에서는 화학 성분의 양극화가 나타나고 있습니다. 비용 효율을 중시하는 마일드 하이브리드 차량은 LFP나 나트륨 이온 배터리를 주로 채택하는 반면, 성능을 중시하는 PHEV는 고니켈 NMC 배터리를 유지하고 있으며, 초고급 차종에서는 전고체 배터리가 시범 도입되고 있습니다.

첨단 배터리 기술의 도입으로 인해 재활용 과정이 더욱 복잡해지고 있습니다. 황화물 전해질을 사용한 전고체 배터리 팩의 경우, 새로운 해체 및 회수 공정이 필요하지만, 유럽의 재활용 업체 중 이를 대규모로 수행할 준비가 되어 있는 기업은 거의 없습니다. 동시에, 코발트가 포함되지 않은 배터리 방식은 규정 2023/1542에 따른 규제 부담을 줄여주며, 각 OEM 업체는 코발트 함량이 높은 배터리에 부과되는 50-80유로/kWh의 규정 준수 비용을 절감할 수 있습니다. 이러한 변화에 대응하기 위해 기가팩토리는 장기간의 가동 중단을 수반하지 않으면서도 화학 성분을 전환할 수 있는 유연한 생산 라인을 설계해야 합니다. 이는 아시아의 기존 대기업들이 이미 입증한 역량이며, 유럽의 신규 진출기업들도 이를 신속하게 따라잡아야 합니다.

유럽의 하이브리드 전기자동차용 배터리 시장에서는 2025년에 마일드 하이브리드가 매출의 46.70%를 차지했으며, 이 부문은 2031년까지 연평균 18.64%의 성장률을 보일 것으로 전망됩니다. 시스템 비용이 800유로로 저렴하기 때문에 폭스바겐 골프나 르노 클리오와 같은 모델에서 48볼트 시스템이 규제 대응의 주요 수단이 되고 있습니다. 도요타의 e-CVT 시스템으로 대표되는 풀 하이브리드는 28.40%의 시장 점유율을 차지하고 있지만, 유럽의 각 브랜드가 개발 예산 배분을 재검토하고 있는 탓에 연평균 성장률(CAGR)은 10.60%로 다소 낮은 수준에 머물고 있습니다. 플러그인 하이브리드는 매출의 22.00%를 차지하고 있지만, 독일과 영국이 구매 인센티브를 폐지함에 따라 BEV와의 총 소유 비용(TCO) 측면에서 경쟁력이 약화되어 취약한 입장에 놓여 있습니다.

실제 주행 데이터도 이러한 압력을 더욱 강화하고 있습니다. 2024년 ‘Transport &Environment’의 조사에 따르면, 차량 함대용 PHEV는 주행 거리의 절반 이하만 전기 모드로 주행하고 있는 것으로 나타났으며, 이에 따라 정책 입안자들은 더 엄격한 이용률 계수를 기반으로 한 시험 도입을 검토하고 있습니다. 세제 혜택이 없는 상황에서 충전 인프라가 확충됨에 따라 구매자들은 저비용의 마일드 하이브리드나 BEV 중 하나를 선택하는 경향이 있습니다. 레인지 익스텐더 방식은 패키징이 복잡하다는 점 때문에 시장 점유율이 2.90% 미만에 그치고 있어, 2031년까지는 보급이 어려울 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the europe hybrid electric vehicle battery market size is expected to grow from USD 3.19 billion in 2025 to USD 3.73 billion in 2026 and is forecast to reach USD 8.17 billion by 2031 at 16.97% CAGR over 2026-2031.

[1] European Commission, "Proposal for CO2 Emission Performance Standards," ec.europa.eu Mild-hybrid penetration is climbing ahead of full and plug-in variants because the technology delivers 10-15% fuel-economy gains at roughly one-third the system cost of a full hybrid, preserving margin while avoiding expensive charging infrastructure build-outs. [2] Stellantis, "2024 Electrification Strategy," stellantis.com Li-ion chemistries dominated in 2025 with 78.2% volume, as cell makers chase lower material cost and supply-chain resilience. This report is Segmented by Battery Chemistry (Lithium-Ion, Nickel-Metal Hydride, Lead-Acid, and More), Degree of Hybridization (Mild Hybrid, Full Hybrid, and More), Voltage Class (Up To 60V, 60 To 200V, 200 To 400V, and Above 400V), Vehicle Class (Passenger Cars, Commercial Vehicles, Two-/Three-Wheelers, and More), and Geography (Germany, United Kingdom, Spain, Netherlands, and More).

Europe Hybrid Electric Vehicle Battery Market Trends and Insights

Rising HEV Production Volumes Aligned With EU CO2 Fleet Targets

Automakers must meet the 2025 fleet-average ceiling of 93.6 g/km, reduced from 115.1 g/km in 2021, or pay EUR 95 for every excess gram per vehicle sold, pushing brands to standardize hybrid powertrains across high-volume B- and C-segment models. Stellantis, Renault, and Volkswagen expanded 48-volt offerings in 2024, each leveraging belt-starter-generator systems that shave roughly 12 g/km from type-approval emissions for less than a EUR 1,000 cost premium. Because super-credits for zero and low-emission vehicles can still be applied through 2025, building hybrids today generates compliance headroom while BEV infrastructure scales. This rule architecture therefore locks in baseline demand for lithium-ion cells through at least 2027, after which the stricter 2030 targets will intensify electrification pressure.

Gigafactory Investments in CEE Region Localizing Supply Chains

Over EUR 15 billion was committed to new cell plants in Hungary, Poland, and Slovakia during 2024, led by CATL's 100 GWh Debrecen facility and LG Energy Solution's Wroclaw expansion to 70 GWh. The labor arbitrage of 15-20% versus Western Europe, plus just-in-time proximity to German assembly hubs, trims pack lead times to under 24 hours. European Battery Alliance co-financing is accelerating upstream cathode precursor and separator projects that substitute Asia-origin inputs, simultaneously lowering embedded CO2 per kWh. As carbon-footprint declarations become mandatory, local supply chains gain a strategic advantage.

Critical Mineral Cost Volatility

Lithium carbonate prices collapsed from USD 80,000/t in late 2022 to near USD 10,000/t by December 2024, while nickel sulfate swung USD 7,000/t inside a single year. Such turbulence compresses margins on fixed-price supply deals, particularly for smaller European entrants lacking vertical integration. Investors now demand price-adjustment clauses or equity stakes in upstream mines before funding capacity expansions, delaying several gigafactory timelines.

Other drivers and restraints analyzed in the detailed report include:

- Surge in 48-V Mild-Hybrid Architectures

- EU Sustainable-Battery Regulation Incentives

- OEM Cap-ex Shift Toward Full-BEV Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion held 77.60% of 2025 demand, with high-nickel NMC variants powering plug-in hybrids that require 250-280 Wh/kg energy density. LFP gained share in mild-hybrids owing to 3,000-cycle durability and cobalt-free supply chains, a feat demonstrated by BYD's Blade pack that cut system cost 30% for Stellantis models. Emerging sodium-ion and solid-state formats should grow 30.90% annually yet remain sub-scale until after 2026, when Northvolt's pilot line in Sweden starts series output for entry-level hybrids. Nickel-metal-hydride slipped to 7.60% share as Toyota transitioned to new European releases to lithium-ion. The European hybrid electric vehicle battery market sees chemistry bifurcation: cost-sensitive mild hybrids gravitate to LFP and sodium-ion, performance-oriented PHEVs keep high-nickel NMC, and ultra-premium variants pilot solid-state cells.

Advanced chemistries introduce recycling complexity. Solid-state packs using sulfide electrolytes demand novel dismantling and recovery steps that few European recyclers are ready to scale. Simultaneously, cobalt-free formats lighten obligations under Regulation 2023/1542, saving OEMs the EUR 50-80/kWh compliance premium attached to high cobalt content cells. These shifts require gigafactories to design flexible lines capable of chemistry switching without extended downtime, a capability that entrenched Asian incumbents already demonstrate, and new European players must replicate quickly.

The European hybrid electric vehicle battery market recorded 46.70% revenue from mild hybrids in 2025, and this cohort will compound 18.64% annually to 2031. System costs as low as EUR 800 make 48-volt the dominant compliance lever for models such as the Volkswagen Golf and Renault Clio. Full hybrids, typified by Toyota's e-CVT system, held a 28.40% share yet face a slower 10.60% CAGR as European brands redirect engineering budgets. Plug-in hybrids claimed 22.00% revenue but are vulnerable after Germany and the UK scrapped purchase incentives, eroding total-cost-of-ownership parity with BEVs.

Real-world usage data compounds the pressure. A 2024 Transport & Environment study found fleet PHEVs drive less than half their kilometers in electric mode, prompting policymakers to consider tougher utility-factor testing. Absent tax breaks, buyers gravitate either to lower-cost mild hybrids or to BEVs as charging networks improve. Range-extender designs remain below 2.90% share due to packaging complexity and are unlikely to scale before 2031.

List of Companies Covered in this Report:

- BYD Company Ltd

- LG Energy Solution

- Panasonic Holdings Corporation

- Samsung SDI Co., Ltd.

- SK On Co., Ltd.

- EnerSys

- Clarios

- Gotion High-Tech Co Ltd

- Northvolt AB

- Automotive Cells Company (ACC)

- VARTA AG

- CATL Europe

- AESC Envision

- InoBat Auto

- Verkor

- FREYR Battery

- SVOLT Energy Technology

- Saft Groupe S.A.

- Leclanche SA

- E4V

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising HEV production volumes aligned with EU CO? fleet targets

- 4.2.2 Gigafactory investments in CEE region localizing supply chains

- 4.2.3 Declining lithium-ion pack prices in Europe

- 4.2.4 EU sustainable-battery regulation incentives

- 4.2.5 Surge in 48-V mild-hybrid architectures

- 4.2.6 Emergence of sodium-ion batteries for low-cost hybrids

- 4.3 Market Restraints

- 4.3.1 Critical mineral cost volatility

- 4.3.2 OEM cap-ex shift toward full-BEV platforms

- 4.3.3 Cross-border battery-transport regulatory complexity

- 4.3.4 Rise of hydrogen ICE hybrids diverting investment

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 Market Size & Growth Forecasts

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (NMC, NCA, LFP, LTO)

- 5.1.2 Nickel-Metal Hydride (NiMH)

- 5.1.3 Lead-acid

- 5.1.4 Emerging Solid-State/Sodium-ion

- 5.2 By Degree of Hybridization

- 5.2.1 Mild Hybrid (48 V MHEV)

- 5.2.2 Full Hybrid (HEV)

- 5.2.3 Plug-in Hybrid (PHEV)

- 5.2.4 Range-Extender Hybrid

- 5.3 By Voltage Class

- 5.3.1 Up to 60 V

- 5.3.2 60 to 200 V

- 5.3.3 200 to 400 V

- 5.3.4 Above 400 V

- 5.4 By Vehicle Class

- 5.4.1 Passenger Cars

- 5.4.2 Commercial Vehicles

- 5.4.3 Two-/Three-Wheelers

- 5.4.4 Off-Highway and Specialty

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Norway

- 5.5.8 Russia

- 5.5.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 BYD Company Ltd

- 6.4.2 LG Energy Solution

- 6.4.3 Panasonic Holdings Corporation

- 6.4.4 Samsung SDI Co., Ltd.

- 6.4.5 SK On Co., Ltd.

- 6.4.6 EnerSys

- 6.4.7 Clarios

- 6.4.8 Gotion High-Tech Co Ltd

- 6.4.9 Northvolt AB

- 6.4.10 Automotive Cells Company (ACC)

- 6.4.11 VARTA AG

- 6.4.12 CATL Europe

- 6.4.13 AESC Envision

- 6.4.14 InoBat Auto

- 6.4.15 Verkor

- 6.4.16 FREYR Battery

- 6.4.17 SVOLT Energy Technology

- 6.4.18 Saft Groupe S.A.

- 6.4.19 Leclanche SA

- 6.4.20 E4V

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment