|

시장보고서

상품코드

2066770

이탈리아의 SLI 배터리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Italy SLI Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

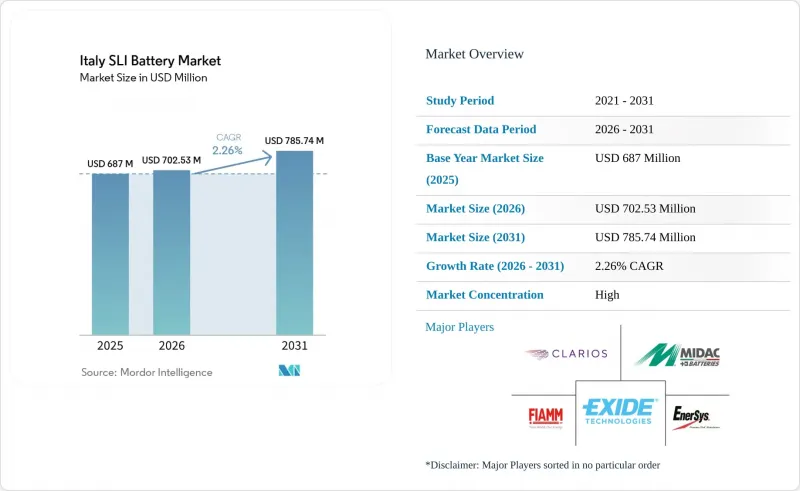

Mordor Intelligence에 의하면, 이탈리아의 SLI 배터리 시장 규모는 2025년 6억 8,700만 달러로 평가되었습니다. 2026년에는 7억 253만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 2.26%로 성장을 지속하여, 2031년에는 7억 8,574만 달러에 이를 것으로 예측됩니다.

본 보고서는 배터리 유형(액체형, 개량형 액체형, AGM(흡수성 유리 매트), 젤 셀 VRLA), 배터리 전압(12V 이하, 12V, 48V, 60V 이상), 용도(승용차, 소형 상용차, 대형 상용차, 이륜·삼륜차, 농업용 및 오프로드 차량, 산업용 동력, 대기/백업)별로 분류되어 있습니다.

이탈리아의 SLI 배터리 시장 동향 및 분석

증가하는 차량 보유 대수와 교체 수요

이탈리아의 4,100만 대에 달하는 차량 보유 대수(평균 차령 13년)는 수명이 다해가는 배터리의 방대한 공급원이 되고 있습니다. 차량 교체 주기가 느리고, 신규 등록 대수가 총 보유 대수의 불과 3-4%에 그치고 있기 때문에 2015년 이전에 장착된 액체형 배터리는 현재 2차 또는 3차 교체 시기를 맞이하고 있습니다. 이 수요 부문의 안정성 덕분에, 전기자동차 보급이 북유럽 국가들에 비해 뒤처져 있음에도 불구하고 이탈리아의 SLI 배터리 시장은 판매량 급감으로부터 보호받고 있습니다. 5년 이상 경과한 배터리의 경우, 겨울철 저온 시동 불량이 급증하고 있어 소매업체들은 진단 점검 및 계절 한정 할인을 적극적으로 추진하고 있습니다.

스타트-스톱 차량에 AGM/EFB 배터리 채택 확대

2024년까지 유럽 내 스타트-스톱 시스템 보급률은 68%를 넘어섰으며, 이탈리아의 각 OEM 업체들은 신형 마이크로 하이브리드 플랫폼에 AGM 또는 EFB 배터리를 탑재하도록 의무화하고 있습니다. 이러한 차량이 노후화됨에 따라 애프터마켓에서의 교체 수요가 가속화될 것으로 예상되며, 심방전에 강한 AGM 배터리가 선호되는 추세입니다. 엑사이드사의 듀얼 터미널 AGM ‘B24’ 시리즈는 호환 차종을 최대 100만 대까지 확대함으로써, 제조업체가 범용성을 중시하고 있음을 여실히 보여주었습니다. 따라서 유통업체은 수익 증대를 확실히 실현하기 위해 AGM 배터리의 재고 확보, 새로운 랙 설비 도입 및 직원 교육에 투자해야 합니다.

리튬이온 12V 보조 배터리 시장 점유율 확대

EUROBAT는 ADAS 및 인포테인먼트의 부하가 급증하는 가운데, 2030년까지 12V 보조 배터리 시장에서 납축전지와 리튬이온전지 시장 점유율이 50 대 50이 될 것으로 예측했습니다. 리튬 이온 배터리는 충전 속도가 빠르고 가볍지만, 납축전지는 60-70%의 비용 경쟁력을 갖추고 있으며, 영하의 기온에서도 뛰어난 저온 시동 성능을 발휘합니다. 이탈리아의 각 제조업체들은 이 중요한 틈새 시장에서 입지를 유지하기 위해, 박판 순수 납(Thin-Plate Pure Lead) 및 탄소 강화형 배터리의 도입을 서두르고 있습니다.

부문별 분석

AGM 배터리는 이미 스타트-스톱 기능이 탑재된 차량의 대부분에 채택되어 있으며, 이탈리아의 SLI 배터리 시장 전체의 성장률 2.26%에 비해 연평균 성장률(CAGR) 6.31%로 확대될 것으로 전망됩니다. 2015년 이전에 제조된 차량용 교체용 배터리 시장에서는 여전히 액체형 배터리가 주류를 이루고 있지만, AGM 배터리로의 교체가 보편화됨에 따라 그 점유율은 점차 감소할 것으로 전망됩니다. EFB 배터리는 액체형 배터리에서는 얻을 수 없는 높은 사이클 수명이 필요한 반면, 풀 AGM 배터리의 가격을 부담스럽게 여기는 차량 대여 업체에게 중가대의 대안이 됩니다.

이탈리아의 SLI 배터리 시장에서 AGM 제품 시장 규모는 스타트-스톱 기능의 보급이 확대됨에 따라, 2025년 2억 2,700만 달러에서 2031년까지 3억 2,770만 달러 가까이까지 확대될 것으로 전망됩니다. 엑사이드사의 M3 규격 대응 AGM B24 출시 소식은 제조업체가 유통업체의 SKU 수를 줄이기 위해 단자 옵션의 폭을 넓히고 있음을 보여줍니다. 한편, 비용 부담이 큰 남부 지역에서는 기존의 액체식 설계가 계속 채택될 것으로 보이지만, AGM의 장점에 대한 소비자의 이해가 깊어짐에 따라 전국적으로는 그 시장 점유율이 감소할 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the italy sLI battery market size is expected to grow from USD 687 million in 2025 to USD 702.53 million in 2026 and is forecast to reach USD 785.74 million by 2031 at 2.26% CAGR over 2026-2031.

This report is Segmented by Battery Type (Flooded, Enhanced Flooded, Absorbent Glass Mat, and Gel Cell VRLA), Battery Voltage (Up To 12V, 12V, 48V, and Above 60V), Application (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two-/Three-Wheelers, Agricultural and Off-Highway Vehicles, Industrial Motive Power, and Stand-by/Backup).

Italy SLI Battery Market Trends and Insights

Growing vehicle-parc & replacement demand

Italy's 41 million-unit parc, averaging 13 years in age, generates a deep pool of batteries nearing end-of-life. Slow fleet turnover, new registrations equal only 3-4% of total parc, means flooded batteries installed before 2015 are now cycling through second or third replacements. The stability of this demand segment shields the Italy SLI battery market from abrupt volume declines even as EV adoption lags Northern Europe. Winter cold-cranking failures rise sharply in batteries older than five years, prompting retailers to promote diagnostic checks and seasonal discounts.

Rising AGM/EFB adoption in start-stop cars

Start-stop systems topped 68% penetration in Europe by 2024, and Italian OEMs mandate AGM or EFB fitment on new micro-hybrid platforms. As these vehicles age, aftermarket replacements are set to accelerate, favoring AGM chemistry that tolerates deep cycling. Exide's dual-terminal AGM B24 series widened fitment coverage by up to 1 million units, underscoring the priority manufacturers place on versatility. Distributors must therefore invest in AGM stocking, new racking, and staff training to capture the revenue upswing.

Li-ion 12 V auxiliaries gaining share

EUROBAT projects a 50/50 split between lead-acid and lithium-ion in 12 V auxiliary batteries by 2030 as ADAS and infotainment loads soar. Lithium-ion offers faster recharge and lighter weight, but lead-acid holds a 60-70% cost edge and better cold-cranking at sub-zero temperatures. Italian manufacturers are racing to introduce Thin-Plate Pure Lead and carbon-enhanced variants to hold ground in this critical niche.

Other drivers and restraints analyzed in the detailed report include:

- Micro-hybrid retrofit boom in urban fleets

- EU circular-economy push for lead recycling

- Shrinking ICE production under 2030 targets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AGM already serves the majority of start-stop cars and is forecast to expand at a 6.31% CAGR, compared with the Italy SLI battery market's overall 2.26% growth. Flooded batteries still dominate replacement sales for vehicles built before 2015, but their share will erode as the AGM replacement wave matures. EFB provides a mid-price option for fleet operators who need higher cycle life than flooded units can provide, yet balk at full-AGM pricing.

The Italy SLI battery market size for AGM units is projected to rise from USD 227 million in 2025 to nearly USD 327.7 million by 2031 as start-stop penetration deepens. Exide's M3-rated AGM B24 launch shows how manufacturers are broadening terminal options to trim SKU counts for distributors. Meanwhile, flooded designs will persist in cost-pressured Southern regions but decline nationally as consumer education on AGM benefits increases.

List of Companies Covered in this Report:

- FIAMM Energy Technology S.p.A.

- Clarios (Johnson Controls)

- Exide Technologies

- Midac SpA

- Sunlight Group

- EnerSys

- GS Yuasa Corporation

- Banner GmbH

- C&D Technologies Inc.

- Leoch International Tech. Ltd.

- Accumulatori Ariete S.R.L.

- Trojan Battery Company

- NorthStar Battery

- Bosch (Battery Division)

- Varta AG

- Yuasa Battery (Europe) Ltd.

- East Penn Mfg. (Deka)

- TAB Batteries

- Moll Batterien GmbH

- VoltA Batteries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing vehicle-parc & replacement demand

- 4.2.2 Rising AGM/EFB adoption in start-stop cars

- 4.2.3 Micro-hybrid retrofit boom in urban fleets

- 4.2.4 EU circular-economy push for lead recycling

- 4.2.5 Carbon-footprint labelling favours local supply

- 4.2.6 Expansion of automotive aftermarket e-commerce

- 4.3 Market Restraints

- 4.3.1 Li-ion 12 V auxiliaries gaining share

- 4.3.2 Shrinking ICE production under 2030 targets

- 4.3.3 Battery-passport compliance cost for SMEs

- 4.3.4 Lead-scrap price volatility & export curbs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Flooded (Conventional)

- 5.1.2 Enhanced Flooded (EFB)

- 5.1.3 Absorbent Glass Mat (AGM)

- 5.1.4 Gel Cell VRLA

- 5.2 By Battery Voltage

- 5.2.1 Up to 12 V

- 5.2.2 12 V

- 5.2.3 48 V

- 5.2.4 Above 60 V

- 5.3 By Application

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Two-/Three-Wheelers

- 5.3.5 Agricultural and Off-Highway Vehicles

- 5.3.6 Industrial Motive Power (Forklifts, Material-Handling)

- 5.3.7 Stand-by/Backup (Telecom, UPS)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 FIAMM Energy Technology S.p.A.

- 6.4.2 Clarios (Johnson Controls)

- 6.4.3 Exide Technologies

- 6.4.4 Midac SpA

- 6.4.5 Sunlight Group

- 6.4.6 EnerSys

- 6.4.7 GS Yuasa Corporation

- 6.4.8 Banner GmbH

- 6.4.9 C&D Technologies Inc.

- 6.4.10 Leoch International Tech. Ltd.

- 6.4.11 Accumulatori Ariete S.R.L.

- 6.4.12 Trojan Battery Company

- 6.4.13 NorthStar Battery

- 6.4.14 Bosch (Battery Division)

- 6.4.15 Varta AG

- 6.4.16 Yuasa Battery (Europe) Ltd.

- 6.4.17 East Penn Mfg. (Deka)

- 6.4.18 TAB Batteries

- 6.4.19 Moll Batterien GmbH

- 6.4.20 VoltA Batteries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment