|

시장보고서

상품코드

2072466

이탈리아의 재생에너지 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Italy Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

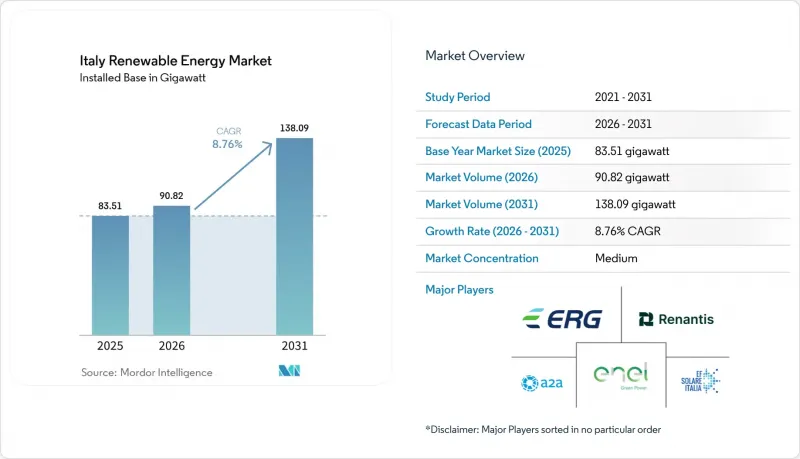

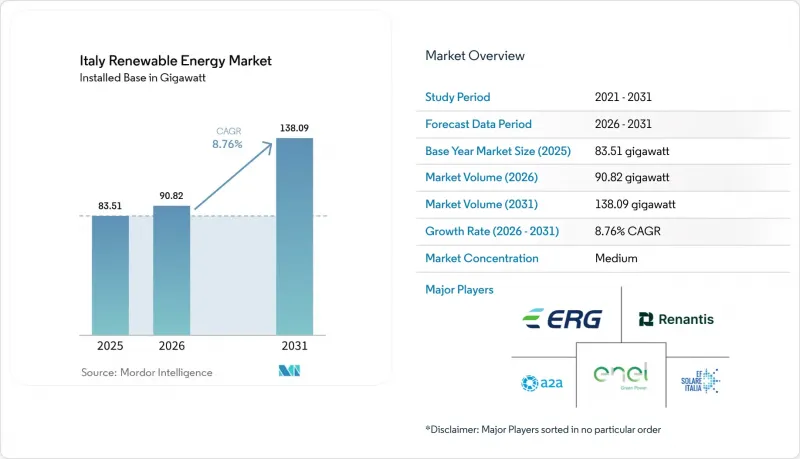

Mordor Intelligence에 의하면, 2026년 이탈리아의 재생에너지 시장 규모는 90.82기가와트에 이를 것으로 추정됩니다. 2025년 83.51기가와트에서 확대해, 2031년에는 138.09기가와트에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 8.76%로 성장할 것으로 전망됩니다.

본 보고서는 기술별(태양광 발전, 풍력 발전, 수력 발전, 바이오에너지, 지열 발전, 해양 에너지) 및 최종 사용자별(전력 회사, 상업 및 산업용, 주거용)로 분류되어 있습니다. 시장 규모 및 전망은 설치 용량(GW) 단위로 표시되어 있습니다.

이탈리아의 재생에너지 시장 동향 및 인사이트

NRRP를 통한 자금 지원 확대

NRRP는 에너지 전환 프로젝트에 253억 6,000만 유로를 직접 배정하고 있으며, 경쟁 입찰 및 우대 보조금을 통해 자금을 지원함으로써 신규 프로젝트의 가중평균자본비용을 낮추고 있습니다. 2023년 12월 REPowerEU 보충안에 따라 29억 유로가 추가로 배정되어, 송전망의 디지털화 및 대규모 재생에너지 사업에 투입되었습니다. 지금까지 NRRP 총 자금의 22%에 해당하는 430억 유로가 프로젝트 주관 기관에 배분되었으며, 인허가 제도 개혁으로 인해 지연되었던 사업들이 해결됨에 따라 2026년 기한까지 지출이 가속화될 것으로 예측됩니다. 역사적인 투자 부족으로 인해 송전망의 공백이 발생했으며, 이 공백이 현재 이탈리아에서 일사량이 가장 많은 지역과 겹치기 때문에 남부 주와 섬들이 우선적으로 선정되고 있습니다. 따라서 경제 발전이 제한된 지역에 자산을 배치할 경우, 프로젝트 개발자는 경매에서 우대 평가를 받을 수 있습니다.

EU의 ‘Fit-for-55’ 지침

'Fit-for-55' 패키지에서는 이탈리아에 2030년까지 최종 에너지 소비량에서 재생에너지의 비중을 40.5%로 높일 것을 요구하고 있습니다. 이는 약 131 GW의 발전 용량에 해당하며, 그중 80 GW가 태양광 발전(PV)이므로 태양광 발전의 성장세가 더욱 강화될 것입니다. 법적 구속력이 있는 마일스톤에 따라 투자 기간이 일반적인 프로젝트 파이낸싱 기간보다 연장되며, 목표를 달성하지 못할 경우 벌금이 부과되므로 적극적인 건설 일정이 확보되고 있습니다. 재생에너지 전력은 냉난방 및 운송 분야의 탈탄소화를 촉진하기 위해, 발전 사업자는 여러 부문에 걸쳐 원산지 보증 및 탄소 가격을 통해 수익을 창출할 수 있습니다. 2024년에는 이미 재생에너지 전력이 국내 수요의 41%를 차지했으며, 이탈리아는 현재 오스트리아 및 슬로베니아로 연결되는 새로운 송전선을 활용한 국경을 넘는 전력 수출 계약을 검토하고 있습니다.

허가 지연과 NIMBY 현상

환경 허가를 받는 데는 보통 3-5년이 소요되며, 이는 EU가 권장하는 24개월이라는 상한선의 2배에 해당합니다. 지역 문화재 보호 당국은 종종 경관 영향 조사를 요구하고 있으며, 시민 단체들은 관광 코스 인근의 풍력 발전기를 상대로 소송을 제기하고 있습니다. 2025년 정령에 따라 10MW 미만의 태양광 발전 프로젝트에 대해서는 환경영향 평가 요건이 면제되었으나, 지역별 대응에 차이가 있어 불확실성이 장기화되고 있습니다. 법원은 최근 종합적인 토지 이용 금지 조치를 무효화하며 상황이 점차 개선되고 있음을 시사하고 있지만, 개발업체들의 파이프라인에는 여전히 최종 승인을 기다리고 있는 약 80GW 규모의 프로젝트가 쌓여 있습니다.

부문별 분석

2025년 기준으로 태양광 발전 설비는 총 발전 용량의 48.10%를 차지하며, 이탈리아의 재생에너지 시장에서 가장 큰 점유율을 차지했습니다. 이 부문은 토지 이용을 확대하지 않고도 발전량을 늘릴 수 있는 양면 수광형 모듈에 힘입어, 2031년까지 연평균 성장률(CAGR) 13.45%로 성장할 것으로 전망됩니다. 태양광 발전소가 주도적인 위치를 차지하는 반면, 집광형 태양열 발전은 직사 일사량이 적기 때문에 여전히 무시할 수 있는 수준에 머물러 있습니다. 육상 풍력은 발전 용량의 18.05%를 차지하고 있지만, 풀리아 주와 시칠리아 섬의 입지 여건이 거의 포화 상태에 이르렀기 때문에 개발 업체들은 고출력 리파워링으로 중점을 옮기고 있습니다. 해상 부유식 풍력 발전은 심해 지역 개발을 가능하게 하며, 2030년까지 2.1 GW가 추가될 전망입니다. 알프스 산맥의 양수식 발전소를 포함한 수력 발전은 총 발전 용량의 21.25%를 차지하며, 간헐적인 전력원이 증가하는 가운데 계속해서 주파수 안정화에 기여하고 있습니다. 고온 지열 시스템, 소규모 수력 발전, 바이오에너지가 전력 공급 구조를 보완하고 있습니다. 이탈리아의 수력 발전 시장 규모는 대체로 보합세를 보일 것으로 예상되지만, 새로운 양수 발전 설비 도입으로 인해 발전 계획의 유연성이 높아질 전망입니다. 바이오에너지 사업자들은 EU의 더욱 엄격해진 지속가능성 기준을 충족하기 위해 원료를 농업 폐기물로 전환하고 있습니다. 토스카나 지역의 지열 발전은 저온 저류층을 활용하는 바이너리 사이클의 개선으로 혜택을 보고 있는 반면, 해양 에너지는 여전히 실증 단계에 머물러 있습니다. 텐션 레그 방식이나 반잠수식 방식을 채택한 부유식 풍력 발전 플랫폼은 기술적 선택의 폭을 넓혀, 이탈리아가 태양광 발전에 대한 과도한 의존에서 벗어나 에너지 원의 다각화를 도모하는 데 일조하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, italy renewable energy market size in 2026 is estimated at 90.82 gigawatt, growing from 2025 value of 83.51 gigawatt with 2031 projections showing 138.09 gigawatt, growing at 8.76% CAGR over 2026-2031.

This report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Italy Renewable Energy Market Trends and Insights

NRRP Funding Boost

The NRRP allocates EUR 25.36 billion directly to energy transition projects, disbursing funds through competitive auctions and concessional grants that reduce the weighted-average cost of capital for new projects. The December 2023 REPowerEU addendum adds another EUR 2.9 billion, earmarked for grid digitalization and utility-scale renewables. To date, EUR 43 billion, or 22% of the total NRRP resources, has been allocated to project sponsors, with spending expected to accelerate until the 2026 deadline as permitting reforms clear backlogs. Southern provinces and islands are prioritized because historical under-investment created transmission gaps that now coincide with Italy's highest solar irradiation. Project developers thus gain preferential scoring in auctions when siting assets in regions with constrained economic development.

EU Fit-for-55 Mandate

The Fit-for-55 package requires Italy to achieve a 40.5% renewable share in final energy consumption by 2030, equivalent to approximately 131 GW of capacity, including 80 GW of PV, reinforcing the growth trajectory of solar energy. Binding milestones extend investment horizons beyond typical project finance tenures and penalize non-compliance, ensuring aggressive build-out schedules. Because renewable electricity fuels decarbonization in heating, cooling, and transport, generators can monetize guarantees of origin and carbon prices across multiple sectors. With renewable electricity already accounting for 41% of national demand in 2024, Italy is now exploring cross-border power export contracts that leverage upcoming interconnectors to Austria and Slovenia.

Permitting Delays & NIMBYism

Environmental approvals typically take 3 to 5 years, which is double the EU-recommended 24-month ceiling. Local heritage offices often require visual-impact studies, while citizen groups litigate against turbines near tourism corridors. A 2025 decree waived the environmental impact assessment requirement for PV projects below 10 MW; however, regional compliance varies, prolonging uncertainty. Courts have recently annulled blanket land-use bans, signaling a gradual improvement, but developer pipelines still carry roughly 80 GW of projects awaiting final signatures.

Other drivers and restraints analyzed in the detailed report include:

- Prosumer Energy Communities

- Offshore Floating Wind Zones

- Grid Congestion & Curtailment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar installations held 48.10% of capacity in 2025, giving them the largest slice of the Italy renewable energy market share. The segment is projected to rise at a 13.45% CAGR through 2031, supported by bifacial modules that lift output without inflating land use. Photovoltaic plants lead, while concentrated solar power remains negligible due to lower direct normal irradiance. Onshore wind provided 18.05% of the capacity, but sites in Apulia and Sicily are almost saturated, so developers are pivoting to higher-output repowering. Offshore floating wind unlocks deep-water zones and is set to add 2.1 GW by 2030. Hydropower at 21.25% of capacity, including pumped-storage hydro in the Alps, continues to stabilize frequency as intermittent assets climb.Enhanced geothermal systems, small hydro, and bioenergy round out the mix. The Italy renewable energy market size for hydropower is expected to stay largely flat, but new pumped-storage capacity will lengthen the dispatch stack. Bioenergy operators are shifting their feedstock toward agricultural waste to meet stricter EU sustainability criteria. Geothermal in Tuscany benefits from binary-cycle upgrades that tap lower-temperature reservoirs, and ocean energy remains in the pilot stage. Floating wind platforms, utilizing tension-leg and semi-submersible designs, expand the technological palette and help Italy diversify away from heavy reliance on solar energy.

Complete Report Scope:

- By Technology

- Solar Energy (PV and CSP)

- Wind Energy (Onshore and Offshore)

- Hydropower (Small, Large, PSH)

- Bioenergy

- Geothermal

- Ocean Energy (Tidal and Wave)

- By End-User

- Utilities

- Commercial and Industrial

- Residential

List of Companies Covered in this Report:

- Enel Green Power SpA

- ERG SpA

- EF Solare Italia SpA

- Vestas Wind Systems AS

- Siemens Gamesa Renewable Energy SA

- Edison SpA

- Gruppo STG Srl

- Peimar Srl

- Falck Renewables (Renantis) SpA

- A2A Rinnovabili SpA

- ACEA Energia SpA

- Sorgenia SpA

- Statkraft Italia Srl

- RWE Renewables Italia

- Engie Italia SpA

- Italgen SpA

- FERA (Fri-El Green Power) SpA

- RTR Rete Rinnovabile

- Terna Plus Srl

- Plenitude (Eni Renewables)

- Enfinity Global Italy

- BayWa r.e. Italia Srl

- Lightsource bp Italy Srl

- GreenGo Srl

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 NRRP funding boost

- 4.2.2 EU Fit-for-55 mandate

- 4.2.3 Prosumer energy communities

- 4.2.4 Offshore floating wind zones

- 4.2.5 Storage co-location incentives

- 4.2.6 Falling PV LCOE

- 4.3 Market Restraints

- 4.3.1 Permitting delays & NIMBYism

- 4.3.2 Grid congestion & curtailment

- 4.3.3 Land-use conflict (agrivoltaic)

- 4.3.4 Imported module dependency

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of New Entrants

- 4.7.5 Threat of Substitutes

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Energy (PV and CSP)

- 5.1.2 Wind Energy (Onshore and Offshore)

- 5.1.3 Hydropower (Small, Large, PSH)

- 5.1.4 Bioenergy

- 5.1.5 Geothermal

- 5.1.6 Ocean Energy (Tidal and Wave)

- 5.2 By End-User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Enel Green Power SpA

- 6.4.2 ERG SpA

- 6.4.3 EF Solare Italia SpA

- 6.4.4 Vestas Wind Systems AS

- 6.4.5 Siemens Gamesa Renewable Energy SA

- 6.4.6 Edison SpA

- 6.4.7 Gruppo STG Srl

- 6.4.8 Peimar Srl

- 6.4.9 Falck Renewables (Renantis) SpA

- 6.4.10 A2A Rinnovabili SpA

- 6.4.11 ACEA Energia SpA

- 6.4.12 Sorgenia SpA

- 6.4.13 Statkraft Italia Srl

- 6.4.14 RWE Renewables Italia

- 6.4.15 Engie Italia SpA

- 6.4.16 Italgen SpA

- 6.4.17 FERA (Fri-El Green Power) SpA

- 6.4.18 RTR Rete Rinnovabile

- 6.4.19 Terna Plus Srl

- 6.4.20 Plenitude (Eni Renewables)

- 6.4.21 Enfinity Global Italy

- 6.4.22 BayWa r.e. Italia Srl

- 6.4.23 Lightsource bp Italy Srl

- 6.4.24 GreenGo Srl

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment