|

시장보고서

상품코드

2073421

스페인의 재생에너지 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Spain Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

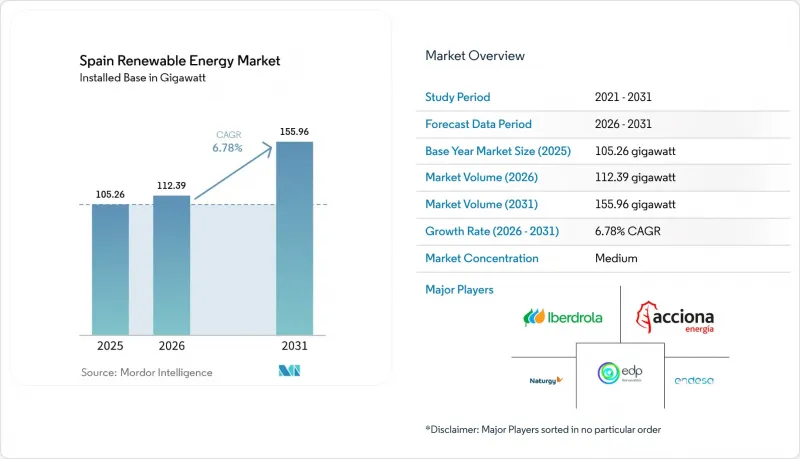

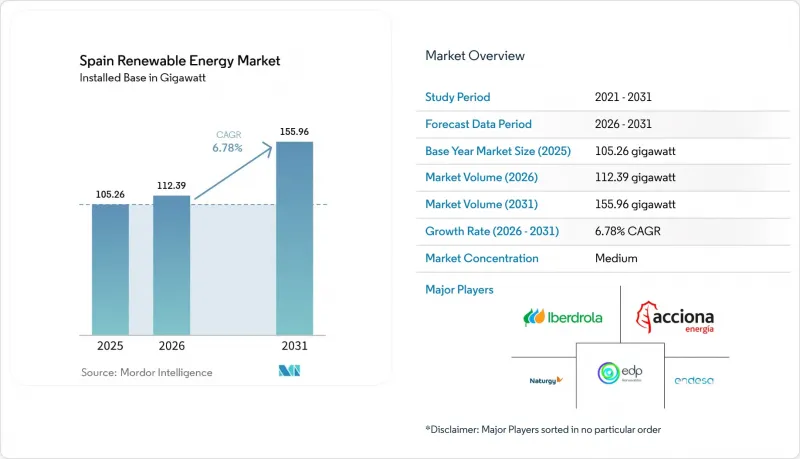

Mordor Intelligence에 의하면, 2026년 스페인의 재생에너지 시장 규모는 112.39기가와트에 달할 것으로 예상됩니다. 2025년 105.26기가와트에서 확대해, 2031년 155.96기가와트에 달하며, 2026년부터 2031년에 걸쳐 CAGR 6.78%로 성장할 전망입니다.

본 보고서는 기술별(태양광 발전, 풍력 발전, 수력 발전, 바이오에너지, 지열 발전, 해양 에너지) 및 최종 사용자별(유틸리티, 상업 및 산업, 주택)로 분류되어 있습니다. 시장 규모 및 전망은 설치 용량(GW) 단위로 표시되어 있습니다.

스페인의 재생에너지 시장 동향 및 인사이트

태양광 발전의 균등화 발전 원가(LCOE) 하락

2024년, 유틸리티 규모의 태양광 발전의 평균 LCOE는 1MWh당 29유로로, 모든 주요 지역에서 복합 사이클 가스 발전 비용을 밑돌았습니다. 이러한 비용 경쟁력은 발전량을 최대 20%까지 향상시키는 양면 모듈과 단축 추적 시스템의 보급은 물론, 중국에서 새로 진입한 기업들의 적극적인 EPC 가격 책정 덕분입니다. 공동 자가 소비 규제로 인해, 이와 유사한 경제성이 도시 지역의 옥상 설치로도 확산되어 2024년에는 설치량이 30% 증가했습니다. 태양광 발전 도입이 가속화됨에 따라 예상되는 도매 가격 하락은 화력 발전의 이익률을 위협하고, 석탄 화력 발전소의 폐쇄를 앞당길 우려가 있습니다. 그러나 아시아산 모듈 수입에 대한 반덤핑 조사가 비용 절감 추세에 차질을 빚을 가능성이 있습니다. 그럼에도 불구하고, 머천트 프로젝트나 PPA(전력구매계약)에 기반을 둔 프로젝트로의 투자 전환은 정부 입찰에 대한 의존도를 낮추고, 태양광 발전의 장기적인 경쟁력에 대한 신뢰가 높아지고 있음을 보여줍니다.

육상 풍력 발전 용량의 급속한 확대

2000년대 초에 설치된 풍력 터빈을 15MW급 플랫폼을 이용해 리파워링한 결과, 설비 가동률이 약 40% 향상되었으며, 동시에 포화 상태에 이른 지역의 토지 이용을 둘러싼 갈등도 완화되었습니다. 개발사는 데이터센터 및 철강 제조업체와의 장기 PPA를 통해 4% 미만의 차입 금리를 확보하고, 공급량에 따른 리스크를 하류로 전가하고 있습니다. 그렇긴 하지만, 그린필드 부지 부족과 조류 보호 구역의 존재로 인해 활동은 갈리시아와 카나리아 제도 연안에서의 부유식 해상 풍력 발전 시범 사업으로 전환되고 있으며, 해당 지역에서는 향후 10년 후반에 3GW 규모의 가동이 시작될 예정입니다. 스페인이 연간 평균 5GW의 풍력 발전 순 증가를 달성하고, 2030년까지 62GW라는 목표를 달성하기 위해서는 환경 심사의 효율화가 여전히 필수적입니다.

송전망의 혼잡 및 출력 억제 위험

2023년의 출력 억제 건수는 전년 대비 3배로 증가했으며, 2024년 주간 피크 시간대에는 1.2 GW 규모의 태양광 및 풍력 발전 설비가 가동을 중단할 수밖에 없어 1억 8,000만 유로의 수익 손실이 발생했습니다. REE의 확장 계획에는 2,500킬로미터의 신규 송전선로와 15곳의 변전소가 포함되어 있지만, 부지 확보가 발전 용량 증가를 따라가지 못하고 있어 2027년까지 제약이 발생할 것으로 보입니다. 병설형 축전지 프로젝트는 발전량 손실을 일부 상쇄하고 있지만, 왕복 효율 및 비용 문제로 인해 그 도입은 제한적입니다. 현재 하이브리드 발전 설비를 우선시하는 시범 운영 체제가 도입되어 있으며, 이는 단독 태양광 발전의 경우 향후 수익성이 더욱 어려워질 것임을 시사합니다.

부문별 분석

스페인의 태양광 발전은 2025년 설치 용량의 42.62%를 차지하며, 스페인의 재생에너지 시장에서 주도적인 입지를 확고히 다졌습니다. 일사량이 2,000 kWh/m²를 초과하는 안달루시아주 및 에스트레마두라주에서 진행 중인 유틸리티 규모 프로젝트들이, 2031년까지 해당 부문의 연평균 성장률(CAGR)이 10.09%를 나타낼 것이라는 전망을 뒷받침하고 있습니다. 스페인의 재생에너지 시장에서 태양광 발전의 규모는 향후 10년 말까지 약 35GW 증가할 것으로 예상되며, 이는 경쟁 에너지 원 중에서 가장 낮은 LCOE를 반영한 것입니다. 풍력 발전은 두 번째 축으로서 이에 이어집니다. 카스티야-라만차 주와 아라곤 주의 육상 풍력 발전소는 28-32%의 설비 가동률을 달성하고 있는 반면, 갈리시아 주 연안 및 카나리아 제도 연안의 3GW 규모 부유식 풍력 발전 프로젝트는 최종 허가를 취득하는 것을 목표로 하고 있습니다. 수력 발전은 20 GW를 공급하고 있으며, 그중 5.3 GW에 달하는 양수 발전이 유연성의 기반 역할을 하고 있지만, 가뭄으로 인한 유입량 변동의 영향을 받기 쉽다는 약점이 있습니다.

높은 비용 경쟁력 덕분에 투자자들의 관심이 태양광과 풍력에 쏠리고 있지만, 기술의 다양화는 여전히 필수적입니다. CSP(집광형 태양열 발전) 발전소는 열 저장 기능을 갖추고 있어, 저녁 피크 시간대에 전력을 공급함으로써 가격 상승 효과를 완화하고 있습니다. 바이오에너지, 지열, 해양 에너지는 주로 원료 확보 가능성이나 자원 품질의 한계, 기술 성숙도가 초기 단계에 머물러 있다는 점 등으로 인해, 총 공급량이 2 GW 미만에 그치고 있습니다. 그렇긴 하지만, 양수 발전의 확대와 축전지와의 하이브리드화는 간헐성을 상쇄하고 시스템의 신뢰성을 높이는 통합적인 자원 포트폴리오의 동향을 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, spain renewable energy market size in 2026 is estimated at 112.39 gigawatt, growing from 2025 value of 105.26 gigawatt with 2031 projections showing 155.96 gigawatt, growing at 6.78% CAGR over 2026-2031.

This report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Spain Renewable Energy Market Trends and Insights

Declining Levelized Cost of Solar PV

Utility-scale solar delivered an average LCOE of EUR 29 per MWh in 2024, undercutting combined-cycle gas generation in every major node. The cost advantage reflects widespread adoption of bifacial modules and single-axis tracking that lifts yields by up to 20%, as well as aggressive EPC pricing from new Chinese entrants. Collective self-consumption rules have translated the same economics into urban rooftops, where installations expanded by 30% during 2024. Lower wholesale prices, expected from accelerated solar additions, threaten thermal margins and hasten coal retirements; however, anti-dumping probes on Asian module imports could disrupt the downward cost curve. Even so, the investment shift toward merchant or PPA-backed projects reduces dependence on government auctions and signals rising confidence in the long-term competitiveness of solar energy.

Rapid Build-Out of Onshore Wind Capacity

The repowering of early-2000s turbines using 15 MW platforms has increased capacity factors by approximately 40%, while alleviating land-use tensions in saturated regions. Developers secure sub-4% debt through long-tenor PPAs with data-center and steel offtakers, transferring volumetric risk downstream. Nonetheless, limited greenfield sites and avian-protection zones push activity toward floating offshore pilots off Galicia and the Canary Islands, where 3 GW is slated for commissioning late in the decade. Streamlined environmental reviews remain essential if Spain is to achieve an average of 5 GW of net wind additions each year and stay aligned with its 2030 target of 62 GW.

Grid Congestion and Curtailment Risk

Curtailment events tripled year-over-year in 2023 and forced 1.2 GW of solar and wind capacity offline during midday peaks in 2024, erasing EUR 180 million in revenue. REE's expansion plan encompasses 2,500 kilometers of new lines and 15 substations; however, land acquisition lags behind capacity additions, resulting in constraints through 2027. Co-located battery projects partly offset lost output; however, round-trip efficiency and cost hurdles limit their uptake. A pilot dispatch regime now prioritizes hybrid assets, signaling tougher economics ahead for standalone solar.

Other drivers and restraints analyzed in the detailed report include:

- EU Fit-for-55 and PNIEC 2023 Targets

- Corporate PPAs from Energy-Intensive Industries

- Lengthy Environmental and Permitting Lead-Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spain Solar energy accounted for 42.62% of installed capacity in 2025, confirming its leadership within the Spanish renewable energy market. Utility-scale projects in Andalusia and Extremadura, where irradiance exceeds 2,000 kWh / m2, underpin the segment's 10.09% CAGR outlook through 2031. The Spain renewable energy market size for solar is forecast to add roughly 35 GW by the decade's close, reflecting the lowest LCOE across competing resources. Wind follows as the second-largest pillar; onshore parks in Castilla-La Mancha and Aragon deliver capacity factors of 28-32%, while a 3 GW floating portfolio off Galicia and the Canary Islands seeks final permits. Hydropower supplies 20 GW, with 5.3 GW of pumped storage acting as a flexibility backbone, yet it is vulnerable to drought-driven inflow variability.

Cost competitiveness drives investor preference toward solar and wind, but technological diversification remains essential. CSP plants provide thermal storage and extend dispatch into evening peaks, mitigating price cannibalization. Bioenergy, geothermal, and ocean energy collectively contribute less than 2 GW, primarily due to limited feedstock availability, resource quality, and the nascent stage of technology readiness. Nevertheless, pumped storage expansions and battery hybrids signal a trend toward integrated resource portfolios that balance intermittency and bolster system reliability.

Complete Report Scope:

- By Technology

- Solar Energy (PV and CSP)

- Wind Energy (Onshore and Offshore)

- Hydropower (Small, Large, PSH)

- Bioenergy

- Geothermal

- Ocean Energy (Tidal and Wave)

- By End-User

- Utilities

- Commercial and Industrial

- Residential

List of Companies Covered in this Report:

- Iberdrola SA

- Acciona Energia SA

- Siemens Gamesa Renewable Energy SA

- Endesa SA

- Naturgy Energy Group SA

- EDP Renovaveis (EDPR)

- Cobra Group (ACS)

- Red Electrica Corporacion SA (REE)

- Solaria Energia y Medio Ambiente SA

- JinkoSolar Holding Co. Ltd (Spain)

- Vestas Wind Systems Spain

- Enel Green Power Espana

- Grenergy Renovables

- Forestalia Renovables

- Capital Energy

- Repsol Renovables

- Solarpack Corporacion

- X-Elio

- Abengoa Solar

- IM2 Systems SLU

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining levelized cost of solar PV

- 4.2.2 Rapid build-out of on-shore wind capacity

- 4.2.3 EU Fit-for-55 & Spain's PNIEC 2023 targets

- 4.2.4 Corporate PPAs from energy-intensive industries

- 4.2.5 Green-hydrogen export hub initiatives

- 4.2.6 Cross-border interconnectors with France & Portugal

- 4.3 Market Restraints

- 4.3.1 Grid congestion & curtailment risk

- 4.3.2 Lengthy environmental/permitting lead-times

- 4.3.3 Balancing-market revenue volatility post 2025

- 4.3.4 Battery-grade lithium supply uncertainty

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Energy (PV and CSP)

- 5.1.2 Wind Energy (Onshore and Offshore)

- 5.1.3 Hydropower (Small, Large, PSH)

- 5.1.4 Bioenergy

- 5.1.5 Geothermal

- 5.1.6 Ocean Energy (Tidal and Wave)

- 5.2 By End-User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Iberdrola SA

- 6.4.2 Acciona Energia SA

- 6.4.3 Siemens Gamesa Renewable Energy SA

- 6.4.4 Endesa SA

- 6.4.5 Naturgy Energy Group SA

- 6.4.6 EDP Renovaveis (EDPR)

- 6.4.7 Cobra Group (ACS)

- 6.4.8 Red Electrica Corporacion SA (REE)

- 6.4.9 Solaria Energia y Medio Ambiente SA

- 6.4.10 JinkoSolar Holding Co. Ltd (Spain)

- 6.4.11 Vestas Wind Systems Spain

- 6.4.12 Enel Green Power Espana

- 6.4.13 Grenergy Renovables

- 6.4.14 Forestalia Renovables

- 6.4.15 Capital Energy

- 6.4.16 Repsol Renovables

- 6.4.17 Solarpack Corporacion

- 6.4.18 X-Elio

- 6.4.19 Abengoa Solar

- 6.4.20 IM2 Systems SLU

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment