|

시장보고서

상품코드

2072483

인도의 방위 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

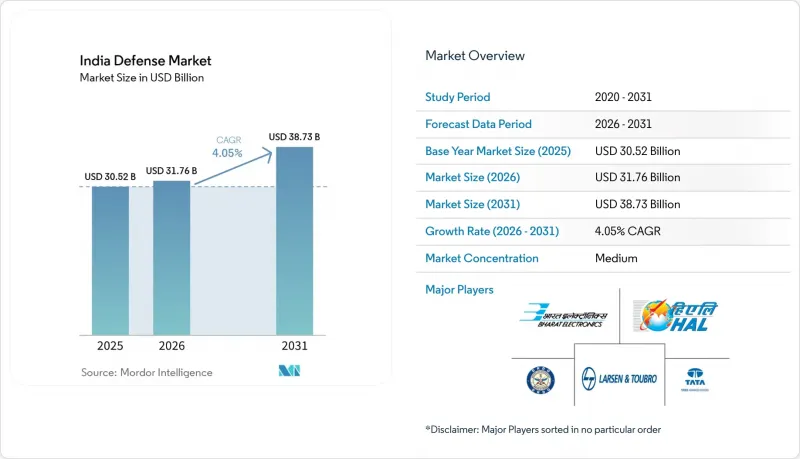

Mordor Intelligence에 의하면, 인도의 방위 시장 규모는 2025년에 305억 2,000만 달러로 평가되었습니다. 2026년 317억 6,000만 달러에서 2031년까지 387억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 4.05%를 나타낼 전망입니다.

본 보고서는 군종(공군, 육군, 해군), 유형(인력 훈련·방호, C4ISR 및 전자전, 차량, 무기·탄약, 무인 시스템, 우주·사이버 시스템), 분야(육상, 항공, 해상, 기타) 및 조달 형태(국산, 해외 조달)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 방위 시장 동향 및 인사이트

국방 예산 확대와 현지화 추진

2025-26 회계연도 연방 예산에는 국방비로 6조 8,100억 루피(787억 달러)가 편성되었으며, 이는 인도 국방 시장에서 전년 대비 9.5% 증가한 수치입니다. 현대화 비용의 4분의 3은 국내 조달에 할당되고 있으며, 이로 인해 전 세계 OEM 기업들은 현지 기업과의 제휴를 맺거나 시장 진입권을 포기해야 하는 상황에 몰리고 있습니다. DRDO의 2만 6,816.82 카롤 루피(31억 3,000만 달러) 규모의 연구 예산은 100건의 우선 순위 프로젝트를 지원하고 있으며, 한편 509개 품목의 수입 금지 조치가 인도 공급업체에 대한 안정적인 수요를 뒷받침하고 있습니다. 설비 투자액은 1조 8,000억 루피(210억 달러)에 달했으나, 국방 분야가 GDP에서 차지하는 비중은 여전히 1.9%에 그치고 있어, 이에 따라 만료되지 않는 현대화 기금 설립안 등 혁신적인 자금 조달 방안이 검토되고 있습니다. 이러한 조치들이 복합적으로 작용하여 인도 국내 기업을 위한 방위 시장 규모가 확대되고, 해외 기업에게는 보다 심도 있는 기술 이전이 촉진됨으로써 인도의 방위 시장의 성장에 기여하고 있습니다.

AI를 활용한 전투 기술 및 자율형 스웜 기술에 대한 투자 가속화

국방 인공지능 프로젝트청(Defence Artificial Intelligence Project Agency)은 인지 레이더 및 자율형 스웜 프로토타입 개발을 위해 연간 1,200만 달러의 예산을 배정받았습니다. “'닥신 샤크티(Dakshin Shakti)' 등의 연습에서는 인도의 교리가 중시하는 운영자에 의한 감독과 부합하는 ‘ "휴먼 인 더 루프(HITL)" 방식의 스웜이 선보였습니다. iDEX 프로그램을 통한 스타트업 기업과의 협력을 통해 194개사가 참여함으로써, 혁신 주기가 단축될 뿐만 아니라 인도의 방위 시장 진입 장벽이 완화되고 있습니다. 그러나 미국의 수출 규제로 인해 고급 반도체에 대한 접근이 제한되면서 기술 격차가 발생하고 있으며, 인도의 100억 달러 규모의 ‘ '반도체 미션' 는 이러한 격차 해소를 목표로 하고 있습니다. 칩의 국산화 역량이야말로 AI 역량이 실증 단계에서 실전 부대로 전환될지 여부를 최종적으로 결정지을 것이며, 이는 인도의 방위 시장의 장기적인 방향과 인도의 방위 부문의 전망을 좌우할 것입니다.

주요 합금 및 반도체 공급망의 취약점

인도는 리튬의 82%, 실리콘의 76%를 중국에서 수입하고 있어, 정밀 무기 및 항공 전자 장비 생산 지연의 위험에 직면해 있습니다. 반도체 부족으로 인해 테자스 Mk-1A의 납품이 8개월 연기되어, 하류 프로그램에 연쇄적인 영향이 미칠 것으로 밝혀졌습니다. “'국가 중요 광물 미션' 한편, 50곳의 해외 광산 확보를 위해 1만 6,000카롤 루피(18억 7,000만 달러)를 배정했으나, 지정학적 마찰로 인해 접근이 제한될 가능성이 있습니다. 2026년에 가동을 시작할 것으로 예상되는 타타 일렉트로닉스의 반도체 공장은 단기적인 공급 부족을 다소 완화시킬 수는 있겠지만, 이를 완전히 해소하기에는 부족할 것입니다. 듀얼 소싱이나 인도와 미국 간의 ‘“TRUST”이 이니셔티브가 완화책이 되겠지만, ITAR(국제무기거래규정)에 따른 제약이 기술 발전을 저해하여 인도의 방위 시장 전체의 성장을 둔화시키고 있습니다.

부문별 분석

2025년, 인도 육군은 인도의 방위 시장의 46.12%를 차지했습니다. 이는 6,811km에 달하는 분쟁 중인 국경 전역에 걸친 광범위한 현대화 수요를 통해 확보한 지위입니다. 그러나 인도 해군의 예상 연평균 성장률(CAGR)이 5.07%라는 점은 인도가 인도-태평양 지역에서 영향력을 확대함에 따라 해양 분야에 대한 투자가 강화되고 있음을 보여줍니다. 2025년에는 국산화율 75%인 ‘"INS Vikrant",“"INS Surat",“"INS Vaghsheer"이 취역함으로써 국내 조선 기술의 성숙도를 입증하고 있습니다. 프로젝트 75I에 따른 4만 3,000 카롤 루피(50억 2,000만 달러) 규모의 AIP(공기 독립 추진) 탑재 잠수함 계획은 해군의 기술적 복잡성을 한층 더 높이고 있습니다.

공군은 승인된 42개 비행대 중 31개 비행대만 보유하고 있다는 제약에 직면해 있으며, 긴급한 수요가 있음에도 불구하고 예산 확보가 지연되고 있습니다. HAL의 AMCA 프로그램(4개 민간 기업과의 합작 사업)은 공동 하이테크 개발로의 전환을 상징하고 있습니다. 동시에, 해군의 “"스프린트(Sprint)"이 이니셔티브는 매년 75건의 새로운 국산 기술을 실전 배치하는 것을 목표로 하고 있으며, 연구 개발의 집중도 면에서 다른 군을 능가하고 있습니다. 앞으로 설립될 통합전역사령부에 따라 자원 흐름이 재편될 가능성은 있지만, 육군의 지상 중심 우선 과제는 앞으로도 인도의 방위 시장의 기반이 될 것입니다.

2025년 매출액 중 차량이 28.25%를 차지했으며, 이는 인도의 방위 시장 규모가 주력 전차, 포병 수송차, 수송기 등의 플랫폼에 유리하게 작용했음을 보여줍니다. 고지대에서의 운용 수요에 부응하여, 라다크 지역의 지형에 맞추어 설계된 ‘"졸라와르"경전차 프로그램이 추진되었습니다. 그러나 무인 시스템은 연평균 성장률(CAGR) 7.02%를 기록하며, 다른 모든 부문을 능가하는 성장이 예상됩니다. 최근 군사 작전에서 AI를 탑재한 스웜 드론이 비용 대비 효과가 높은 전력 증강 수단임이 입증됨에 따라, 국내 드론 시장은 2030년까지 110억 달러에 달할 가능성이 있습니다.

“'아그니파스'근무 기간 모델에 따라 기술 육성의 가속화가 요구되는 가운데, 훈련 및 방호 시스템도 확대되고 있습니다. 다중 도메인 작전에서는 통합적인 상황 인식이 요구되기 때문에 C4ISR 및 전자전(EW) 시스템의 중요성이 커지고 있습니다. 수입이 감소하는 가운데, 스마트 탄약과 국산 탄약이 공급 안정화에 기여하고 있습니다. 전용 작전 교리에 기반을 둔 우주·사이버 분야의 새로운 조달 수요로 인해, 기존 계약업체들은 포트폴리오 다각화를 추진해야만 하며, 그렇지 않을 경우 끊임없이 진화하는 인도의 방위 시장에서 뒤처질 위험에 직면하게 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the india defense market size was valued at USD 30.52 billion in 2025 and estimated to grow from USD 31.76 billion in 2026 to reach USD 38.73 billion by 2031, at a CAGR of 4.05% during the forecast period (2026-2031).

This report is Segmented by Armed Forces (Air Force, Army, and Navy), Type (Personnel Training and Protection, C4ISR and Electronic Warfare, Vehicles, Weapons and Ammunition, Unmanned Systems, and Space and Cyber Systems), Domain (Land, Air, Naval, and More), and Procurement Nature (Indigenous Production and Foreign Procurement). The Market Forecasts are Provided in Terms of Value (USD).

India Defense Market Trends and Insights

Expanding Defense Budget and Localization Drive

The FY 2025-26 Union Budget allocates INR 6.81 trillion (USD 78.7 billion) to defense, a 9.5% rise over the previous year in the India defence market. Three-quarters of the modernization outlay is ring-fenced for domestic sourcing, pressing global OEMs to partner locally or cede market access. DRDO's INR 26,816.82 crore (USD 3.13 billion) research budget backs 100 priority projects, while 509 import-prohibited items anchor captive demand for Indian suppliers. Although capital spending hit INR 1.8 trillion (USD 21 billion), defense still absorbs only 1.9% of GDP, prompting innovative financing such as a proposed non-lapsable modernization fund. Together, these measures widen the addressable Indian defense market for homegrown firms and nudge foreign players toward deeper technology transfer, contributing to the growth of the Indian defense market size.

Accelerated Investment in AI-Enabled Combat and Autonomous Swarm Technologies

The Defence Artificial Intelligence Project Agency receives USD 12 million annually to prototype cognitive radar and autonomous swarms. Exercises such as Dakshin Shakti showcased human-in-the-loop swarms that align with India's doctrinal emphasis on operator oversight. Startup engagement via the iDEX program has onboarded 194 firms, shortening innovation cycles and easing entry barriers in the India defense market. However, limited access to high-end semiconductors-constrained by US export controls-creates a technology gap that India's USD 10 billion Semiconductor Mission seeks to close. The ability to indigenize chips will ultimately determine whether AI capabilities migrate from demonstrations to line units, shaping the long-run trajectory of the Indian defense market and the India defense sector outlook.

Vulnerabilities in Critical Alloy and Semiconductor Supply Chains

India imports 82% of lithium and 76% of silicon from China, risking production delays for precision weapons and avionics. Semiconductor shortages postponed Tejas Mk-1A deliveries by eight months, exposing cascading effects on downstream programs. The National Critical Mineral Mission earmarks INR 16,000 crore (USD 1.87 billion) to secure 50 overseas mines, yet geopolitical frictions could restrict access. Tata Electronics' fab, expected online in 2026, will narrow but not eliminate short-term supply gaps. Dual-sourcing and the India-US TRUST initiative offer mitigation, but ITAR curbs limit technology depth, tempering growth across the Indian defense market.

Other drivers and restraints analyzed in the detailed report include:

- Escalating Geopolitical Tensions Along the Borders

- Emergence of Dual-Use Space Assets Driving C4ISR Capability Demand

- Inefficient and Bureaucratic Defense Procurement Framework

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Army commanded 46.12% of the Indian defense market in 2025, a position earned through extensive modernization needs across 6,811 km of disputed borders. Yet the Navy's 5.07% forecast CAGR signals growing maritime focus as India asserts Indo-Pacific influence. INS Vikrant, INS Surat, and INS Vaghsheer entered service in 2025 with 75% indigenous content, underlining local shipbuilding maturity. Project 75I's INR 43,000 crore (USD 5.02 billion) AIP-enabled submarine program further elevates naval technological complexity.

The Air Force, hampered by a 31-squadron fleet versus an authorized 42, sees slower budget traction despite urgent requirements. HAL's AMCA program-a joint venture with four private firms-marks a pivot toward collaborative high-technology development. Concurrently, the Navy's Sprint initiative aims to field 75 new Indigenous technologies each year, outpacing peer services in R&D intensity. Upcoming Integrated Theatre Commands could realign resource flows, but the Army's land-centric imperatives will remain the anchor of the Indian defense market.

Vehicles held 28.25% of 2025 revenue as the Indian defense market size favored platforms such as main battle tanks, artillery carriers, and transport aircraft. High-altitude demands prompted the Zorawar light tank program tailored for Ladakh terrains. However, unmanned systems are set to outpace all other categories at a 7.02% CAGR. Recent military operations show that AI-enabled swarm drones proved cost-effective force multiplication, and the domestic drone market could reach USD 11 billion by 2030.

Training and protection systems are scaling alongside the Agnipath tour-of-duty model, which demands accelerated skill pipelines. C4ISR and electronic warfare (EW) suites gain prominence as multi-domain operations require unified situational awareness. Smart munitions and domestically produced ammunition address supply security as imports taper. Backed by dedicated doctrine, emerging space and cyber procurements compel legacy contractors to diversify portfolios or risk obsolescence in the evolving Indian defense market.

Complete Report Scope:

- By Armed Forces

- Air Force

- Army

- Navy

- By Type

- Personnel Training and Protection

- C4ISR and Electronic Warfare

- Vehicles

- Weapons and Ammunition

- Unmanned Systems

- Space and Cyber Systems

- By Domain

- Land

- Air

- Naval

- Space

- Cyber and Electromagnetic Spectrum

- By Procurement Nature

- Indigenous Production

- Foreign Procurement

List of Companies Covered in this Report:

- Hindustan Aeronautics Limited (HAL)

- Defence Research & Development Organisation (DRDO)

- Bharat Electronics Ltd.

- Bharat Dynamics Limited (BDL)

- Larsen & Toubro Ltd.

- Tata Advanced Systems Limited (Tata Group)

- Kalyani Strategic Systems Ltd. (Bharat Forge Limited)

- Mahindra & Mahindra Limited

- Adani Group

- Alpha Design Technologies Pvt Ltd.

- Goa Shipyard Limited

- Garden Reach Shipbuilders & Engineers Ltd (GRSE)

- Cochin Shipyard limited

- Swan Defence and Heavy Industries Limited

- Data Patterns (India) Ltd.

- Paras Defence and Space Technologies Limited

- Rafael Advanced Defense Systems Ltd.

- Israel Aerospace Industries Ltd.

- Airbus SE

- The Boeing Company

- Reliance Infrastructure Ltd.

- Mazagon Dock Shipbuilders Limited (MDL)

- Directorate of Ordnance (Coordination & Services)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding defense budget and localization drive

- 4.2.2 Accelerated investment in AI-enabled combat and autonomous swarm technologies

- 4.2.3 Escalating geopolitical tensions along the borders

- 4.2.4 Emergence of dual-use space assets driving C4ISR capability demand

- 4.2.5 Increased private sector participation enabled by liberalized FDI policies

- 4.2.6 Structural modernization of the Army, Navy, and Air Force

- 4.3 Market Restraints

- 4.3.1 Vulnerabilities in critical alloy and semiconductor supply chains

- 4.3.2 Inefficient and bureaucratic defense procurement framework

- 4.3.3 Cybersecurity breaches and IP theft are hindering indigenous R&D progress

- 4.3.4 High pension and salary expenditures limiting capital investment

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Armed Forces

- 5.1.1 Air Force

- 5.1.2 Army

- 5.1.3 Navy

- 5.2 By Type

- 5.2.1 Personnel Training and Protection

- 5.2.2 C4ISR and Electronic Warfare

- 5.2.3 Vehicles

- 5.2.4 Weapons and Ammunition

- 5.2.5 Unmanned Systems

- 5.2.6 Space and Cyber Systems

- 5.3 By Domain

- 5.3.1 Land

- 5.3.2 Air

- 5.3.3 Naval

- 5.3.4 Space

- 5.3.5 Cyber and Electromagnetic Spectrum

- 5.4 By Procurement Nature

- 5.4.1 Indigenous Production

- 5.4.2 Foreign Procurement

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Hindustan Aeronautics Limited (HAL)

- 6.4.2 Defence Research & Development Organisation (DRDO)

- 6.4.3 Bharat Electronics Ltd.

- 6.4.4 Bharat Dynamics Limited (BDL)

- 6.4.5 Larsen & Toubro Ltd.

- 6.4.6 Tata Advanced Systems Limited (Tata Group)

- 6.4.7 Kalyani Strategic Systems Ltd. (Bharat Forge Limited)

- 6.4.8 Mahindra & Mahindra Limited

- 6.4.9 Adani Group

- 6.4.10 Alpha Design Technologies Pvt Ltd.

- 6.4.11 Goa Shipyard Limited

- 6.4.12 Garden Reach Shipbuilders & Engineers Ltd (GRSE)

- 6.4.13 Cochin Shipyard limited

- 6.4.14 Swan Defence and Heavy Industries Limited

- 6.4.15 Data Patterns (India) Ltd.

- 6.4.16 Paras Defence and Space Technologies Limited

- 6.4.17 Rafael Advanced Defense Systems Ltd.

- 6.4.18 Israel Aerospace Industries Ltd.

- 6.4.19 Airbus SE

- 6.4.20 The Boeing Company

- 6.4.21 Reliance Infrastructure Ltd.

- 6.4.22 Mazagon Dock Shipbuilders Limited (MDL)

- 6.4.23 Directorate of Ordnance (Coordination & Services)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment