|

시장보고서

상품코드

2072547

종양학 분야 인공지능(AI) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Oncology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

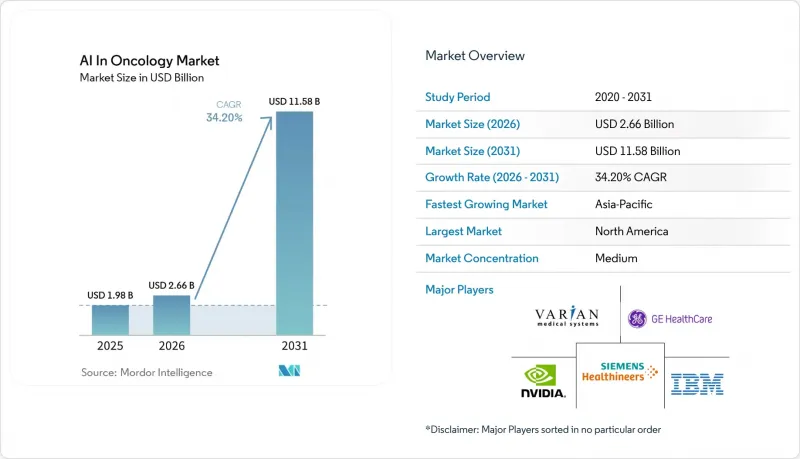

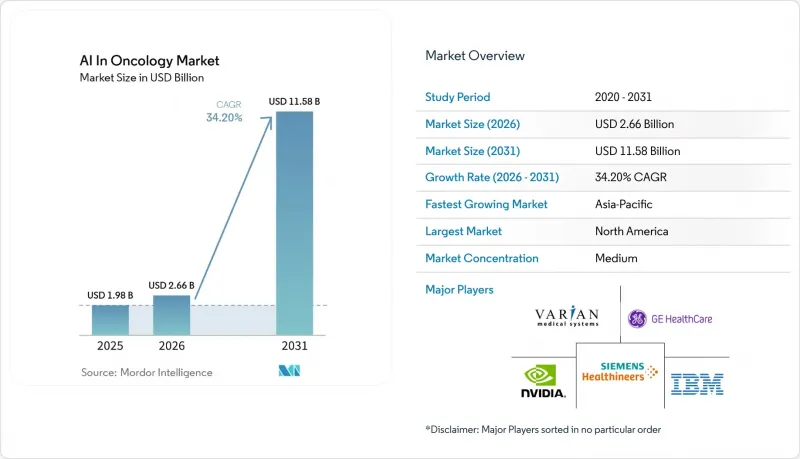

Mordor Intelligence에 의하면, 2026년 종양학 분야 인공지능(AI) 시장 규모는 26억 6,000만 달러로 추정되고 2025년 19억 8,000만 달러에서 확대해, 2031년에는 115억 8,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 34.20%가 될 것으로 전망됩니다.

본 보고서는 구성 요소(소프트웨어 솔루션, 하드웨어, 서비스), 암 유형(유방암, 폐암, 기타), 치료법(방사선 치료, 화학 요법, 면역 요법, 기타 치료법), 용도(암 검진, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 종양학 분야 인공지능(AI) 시장 동향 및 인사이트

전 세계적으로 증가하는 암의 부담

2050년까지 신규 암 진단 건수는 연간 1,200만 건 이상 증가할 것으로 예상되며, 이러한 추세는 전문의 수가 부족한 저소득 국가에서 특히 두드러집니다. 발병률이 증가함에 따라, 일반 노트북에서 구동되는 경량 AI 도구에 대한 수요가 높아지고 있습니다. 이를 통해 방사선과 의사는 영상을 신속하게 선별하여, 기존에는 바쁜 판독실에서 놓치기 쉬웠던 종양을 발견할 수 있게 됩니다. 전 세계 암 치료 및 지지 요법에 대한 지출은 2023년에 2,230억 달러에 달했으며, 2028년까지 4,090억 달러를 넘어설 것으로 예상에 따라, 보험사들은 조기 진단을 통해 비용을 절감할 수 있는 기술에 보상을 제공합니다. 대만 대학 병원의 “"PANCREASaver" 이와 같은 초기 단계의 AI 시스템은 2cm 이하의 췌장 병변을 86.4%의 정확도로 감지하고 있으며, 이는 알고리즘의 혁신이 의료의 방향을 예방으로 어떻게 전환할 수 있는지를 보여주고 있습니다.

정밀의료 프로그램의 확대

AI는 전체 유전체 염기서열 분석, RNA 발현 분석, 디지털 병리 이미지를 면밀히 검토하여 맞춤형 치료 계획을 수립하는 정밀 종양학의 분석 엔진 역할을 하고 있습니다. 무작위 검사 및 레벨 1B 근거에 기반한 ArteraAI 전립선 검사가 미국 종합암네트워크(NCCN)의 승인을 받음에 따라, 알고리즘을 통한 예후 예측이 주류 지침에서 정당화되었습니다. 유럽에서는 2,800만 유로 규모의 ‘"Thera4Care" 이 컨소시엄은 29개 기관에 걸쳐 영상 진단, 유전체학, 치료 계획을 연계하는 EU 전역의 프로토콜을 수립함으로써, 협력적인 자금 지원이 어떻게 중개 의학의 도입을 가속화할 수 있는지 입증하고 있습니다. 이러한 프로그램들은 AI의 출력 결과를 종양 위원회 워크플로우에 직접 통합함으로써, 유전자 염기서열 분석 결과부터 치료 시작까지의 반복 주기를 단축하는 상호 운용 가능한 소프트웨어 프레임워크에 대한 수요를 높이고 있습니다.

높은 도입 비용과 ROI의 불확실성

엔터프라이즈급 종양학 분야에 AI를 도입할 경우, 전용 GPU, 데이터 통합 브리지, 직원 교육 비용을 합산하면 중규모 암 센터에서는 100만 달러를 초과하는 경우가 흔합니다. 경영진은 이러한 지출과 진행기 치료를 피함으로써 발생하는 눈에 보이지 않는 비용 절감 사이에서 균형을 맞추는 데 어려움을 겪고 있습니다. 특히, 2013년부터 2023년 사이에 종양학 분야에서 AI와 관련된 실제 임상 결과 데이터를 제공한 전향적 연구는 고작 15건에 불과하기 때문입니다. 하드웨어와 관련된 위험이 문제를 더욱 복잡하게 만들고 있습니다. 알고리즘의 효율이 급속히 향상되면, 전용 추론 칩이 2회의 기기 교체 주기 이내에 구식이 되어 버릴 가능성이 있기 때문입니다. 그 결과, 소규모 의료기관들은 종량제 클라우드 모델을 선호하여 도입하고 있지만, 통합 기간 중에는 일시적으로 워크플로우 지연에 직면하고 있으며, 투자 회수 기간이 길어지고 있습니다.

부문별 분석

2025년, 소프트웨어 솔루션은 종양학 분야 인공지능(AI) 시장 점유율 63.78%를 차지했으며, 병원들이 기존의 PACS 뷰어나 방사선 치료 계획 콘솔에 설치할 수 있는 구독형 알고리즘을 선호하는 경향이 두드러졌습니다. “"서비스"이 부문은 2031년까지 연평균 성장률(CAGR) 36.10%를 나타낼 것으로 예측되며, 많은 의료 기관이 사내에 머신러닝 엔지니어를 채용하기보다는 데이터 큐레이션, 알고리즘 튜닝, 도입 후 모니터링을 전문 업체에 위탁하고 있는 것으로 나타났습니다. ConcertAI의 “"Patient360(TM)"이 프로젝트는 이러한 변화를 여실히 보여주고 있습니다. 1,000건 이상의 프로젝트를 완료했으며, 매출의 72%는 지속적인 관리형 서비스에서 발생하고 있습니다. 반면, 하드웨어는 초고해상도 디지털 병리 스캐너나 On-Premise GPU 클러스터와 관련된 틈새 시장 구매에 그치고 있습니다. 차세대 신경망은 점점 더 저렴한 칩에서 구동되기 때문에 자산의 노후화가 우려되어 구매자들이 주저하고 있습니다.

중기적으로는 데이터 관리 미들웨어, 알고리즘 시장, 규제 대응 문서 템플릿을 묶어 제공하는 ‘"플랫폼"가치가 공급업체로 이전될 것으로 보입니다. 이러한 생태계는 통합의 장벽을 낮추고 검증 기간을 단축해 주기 때문에 전문 IT 부서가 없는 지역 병원에게 매력적인 선택지가 됩니다. 2031년까지 소프트웨어 구독료와 관리형 서비스 정액 요금의 합계가 하드웨어 매출을 4대 1 이상의 비율로 상회할 것으로 예측되며, 종양학 분야 인공지능(AI) 시장에서 소프트웨어의 구조적 우위가 확고해질 것으로 보입니다.

유방암은 전국적인 유방촬영술 프로그램과 CLAIRITY BREAST와 같은 위험도 계층화 AI가 규제 당국의 승인을 받은 데 힘입어, 2025년 매출의 28.05%를 차지하며 최대 점유율을 유지했습니다. 그러나 뇌종양 치료 솔루션은 FastGlioma와 같이 10초 이내에 잔존 종양 조직을 식별하는 실시간 수술 안내 알고리즘에 힘입어, 해당 부문에서 가장 빠른 연평균 성장률(CAGR) 36.85%로 성장을 지속하고, 있습니다. 소아 신경교종 재발 예측 모델은 시공간 학습을 통해 현재 89%의 예측 정확도를 달성하고 있으며, 차세대 알고리즘의 임상적 깊이를 보여주고 있습니다. 폐암과 전립선암에 대한 응용 연구도 진전되고 있습니다. ““ArteraAI 전립선 검사”이 내용이 진료 지침에 채택된 것은 엄격한 근거가 보험 급여를 가능하게 한다는 점을 보여주고 있으며, 간이형 폐결절 분류기를 통해 이동 진료소에서 CT 선별검사를 실시할 수 있게 되었습니다.

전반적으로, 뇌종양, 전립선암, 폐암에 대한 새로운 적용 사례가 더해지면서, 치료가 충분히 이루어지지 않은 종양군을 대상으로 하는 종양학 분야 인공지능(AI) 시장 규모는 2026년 4억 2,000만 달러 미만에서 2031년에는 24억 5,000만 달러 이상으로 확대될 것이며, 각 벤더 기업들에게 대상 질환의 범위를 확대할 동기가 될 것으로 보입니다. CURATE.AI의 단일 환자용 용량 최적화 엔진 등, 소규모 데이터 기술을 습득한 벤더는 기존 빅데이터 기법이 한계에 부딪힌 희귀 악성 종양 분야에서 선구자로서의 우위를 확보할 가능성이 있습니다.

지역별 분석

북미는 2025년 매출의 44.12%를 차지했습니다. 이는 세계에서 가장 성숙한 승인 환경, 디지털 병리학에 대한 광범위한 보험 적용, AI를 최우선으로 하는 종양학 분야 스타트업들의 긴밀한 네트워크에 힘입은 결과입니다. FDA의 지속적인 지침 업데이트는 미국 내 공급업체들에게 실시간 학습 시스템에 관한 명확한 지침을 제공하며, 시판 후 성능 향상에 기여하는 지속적인 알고리즘 업데이트를 촉진하고 있습니다. GE 헬스케어가 새터 헬스와 체결한, 300개 시설에 AI 지원 영상 시스템을 전면 도입하는 7년 계약과 같은 대규모 거래는 임상 데이터 생성 및 제품 개선이라는 선순환을 강화하고 있습니다.

아시아태평양은 성장 속도의 선두주자로, 2026년부터 2031년까지의 지역별 연평균 성장률(CAGR)은 35.10%로 예측됩니다. 한국의 국가 AI 헬스 전략, 중국의 ‘'건강 중국 2030'이러한 계획과 싱가포르의 보안 데이터 샌드박스 규제가 맞물려 임상 시범 사업의 추진이 가속화되고 있습니다. 현재 호주, 중국, 일본, 싱가포르에서는 600개에 가까운 의료 AI 스타트업이 활동하고 있으며, 해당 지역의 유전적 특성과 의료 프로토콜에 맞춘 질환별 모델에 현지 데이터 세트를 적용하고 있습니다. 국립 대만 대학 병원의 “"PANCREASaver"이는 자국에서 탄생한 혁신 기술이 국내 도입과 미국 규제 당국의 승인을 모두 얻을 수 있음을 보여줍니다.

유럽에서는 국경을 초월한 연구 네트워크와 윤리적인 AI가 계속해서 우선순위로 꼽히고 있습니다. 29곳에서 진행되고 있는 2,800만 유로 규모의 ‘"Thera4Care" 이 프로젝트는 알고리즘 검토와 설명 가능성 및 데이터 관리에 관한 기준 수립을 결합한 유럽 협력 모델의 대표적인 사례입니다. GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정)으로 인해 규정 준수 부담이 증가하고 있지만, 통합 의료기기 규정(MDR)에 따라 CE 마크 승인을 획득하면 여러 국가에서 제품을 시장에 출시하기까지의 절차가 단축됩니다. 신흥 지역인 중동 및 아프리카와 남미는 아직 발전 단계에 있지만, 클라우드 연결이 확대됨에 따라 이에 대한 관심이 높아지고 있습니다. 세계보건기구(WHO)와 진행한 시범 프로그램에서는 초소형 폐암 검출 장치를 이동식 X선 진단 차량에 탑재했는데, 이는 인프라가 제한된 환경에서도 현대적인 AI 스택이 적용 가능함을 보여줍니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, AI in oncology market size in 2026 is estimated at USD 2.66 billion, growing from 2025 value of USD 1.98 billion with 2031 projections showing USD 11.58 billion, growing at 34.20% CAGR over 2026-2031.

This report is Segmented by Component (Software Solutions, Hardware, and Services), Cancer Type (Breast Cancer, Lung Cancer, and More), Treatment Type (Radiotherapy, Chemotherapy, Immunotherapy, Other Treatment Types), Application (Cancer Detection, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Oncology Market Trends and Insights

Growing Cancer Burden Worldwide

New cancer diagnoses are projected to swell by more than 12 million cases annually by 2050, a trend most acute in lower-income countries that lack specialist capacity. Rising incidence magnifies the appeal of lightweight AI tools that operate on commodity laptops, enabling radiologists to triage images rapidly and spot tumours that conventionally slip through busy reading rooms. Global spend on oncology therapeutics and supportive care hit USD 223 billion in 2023 and is on course to top USD 409 billion by 2028, prompting payers to reward technologies that can shave costs through earlier detection. Early-stage AI systems such as National Taiwan University Hospital's PANCREASaver, which detects sub-2 cm pancreatic lesions with 86.4% accuracy, illustrate how algorithmic innovation can redirect care pathways toward prevention.

Expanding Precision Medicine Programs

AI has become the analytical engine of precision oncology, sifting through whole-genome sequencing, RNA expression, and digital pathology images to craft tailored regimens. The National Comprehensive Cancer Network's endorsement of the ArteraAI Prostate Test, backed by randomised trials and level 1B evidence, has legitimised algorithmic prognostics in mainstream guidelines. In Europe, the €28 million Thera4Care consortium is establishing pan-EU protocols that link imaging, genomics, and treatment planning across 29 institutions, demonstrating how concerted funding can speed translational adoption. These programmes heighten demand for interoperable software frameworks that insert AI outputs directly into tumour-board workflows, trimming iteration cycles between sequencing results and treatment initiation.

High Implementation Costs and ROI Uncertainty

Deploying enterprise-grade oncology AI often costs mid-sized cancer centres more than USD 1 million once specialised GPUs, data-integration bridges and staff training are tallied. Management teams struggle to balance these outlays against invisible savings from avoided late-stage treatments, especially because only 15 prospective studies between 2013-2023 have provided real-world outcome data for oncology AI. Hardware risk compounds the challenge: rapid algorithmic efficiency gains can make dedicated inference chips obsolete within two equipment cycles. Consequently, smaller providers favour pay-per-use cloud models but still face temporary workflow slowdowns during integration, lengthening their payback horizon.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI With Medical Imaging Modalities

- Accelerated Approvals of AI-Based Oncology Devices

- Stringent Data Privacy and Security Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software Solutions accounted for a 63.78% AI in oncology market share in 2025, underscoring hospitals' preference for subscription-based algorithms that install on existing PACS viewers and radiation-planning consoles. The Services segment, projected to post a 36.10% CAGR to 2031, shows that many institutions are outsourcing data curation, algorithm tuning and post-deployment monitoring to specialised vendors rather than hiring in-house machine-learning engineers. ConcertAI's Patient360(TM) projects illustrate the shift: more than 1,000 projects completed and 72% of revenue sourced from recurring managed services. Hardware, meanwhile, remains a niche purchase linked to ultra-high-resolution digital-pathology scanners or on-premise GPU clusters; buyers hesitate because successive neural-network generations run on ever-cheaper chips, threatening asset obsolescence.

In the medium term, value will migrate toward "platform" vendors that bundle data-management middleware, algorithm marketplaces and regulatory documentation templates. Such ecosystems lower integration friction and compress validation timelines, making them attractive to community hospitals that lack specialised IT departments. By 2031, software subscription fees and managed-service retainers together are forecast to out-earn hardware sales by more than 4:1, cementing software's structural primacy in the AI in oncology market.

Breast Cancer retained the largest slice of 2025 revenue at 28.05%, buoyed by nationwide mammography programmes and regulatory acceptance of risk-stratification AI such as CLAIRITY BREAST. Yet Brain Tumor solutions are clocking the sector's fastest CAGR at 36.85%, propelled by real-time surgical guidance algorithms like FastGlioma that identify residual tumour tissue within 10 seconds. Paediatric glioma recurrence models now reach 89% predictive accuracy through spatio-temporal learning, exemplifying the clinical depth of next-gen algorithms. Lung and Prostate Cancer applications are advancing too: the ArteraAI Prostate Test's guideline inclusion demonstrates how rigorous evidence unlocks reimbursement, and lightweight lung-nodule classifiers make CT screening feasible in mobile clinics.

Collectively, emerging brain, prostate and lung applications will push the AI in oncology market size for under-served tumour groups from less than USD 420 million in 2026 to more than USD 2.45 billion in 2031, giving vendors an incentive to widen disease coverage. Vendors that master small-data techniques, such as CURATE.AI's single-patient dose-optimisation engine, could secure first-mover advantage in rare malignancies where traditional big-data methods stall.

Complete Report Scope:

- By Component

- Software Solutions

- Hardware

- Services

- By Cancer Type

- Breast Cancer

- Lung Cancer

- Prostate Cancer

- Colorectal Cancer

- Brain Tumor

- Other Cancer Types

- By Treatment Type

- Radiotherapy

- Chemotherapy

- Immunotherapy

- Other Treatment Types

- By Application

- Cancer Detection

- Drug Discovery

- Drug Development

- Other Applications

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 44.12% of 2025 revenue, underpinned by the world's most mature approval environment, broad reimbursement of digital pathology and a dense network of AI-first oncology start-ups. The FDA's rolling guidance updates give US vendors clarity on real-time learning systems, encouraging continuous-update algorithms that improve post-market. Mega-deals such as GE HealthCare's seven-year pact with Sutter Health to blanket 300 facilities with AI-enabled imaging reinforce a virtuous cycle of clinical data generation and product refinement.

Asia-Pacific is the velocity leader with a 35.10% regional CAGR expected between 2026-2031. South Korea's national AI-health strategy, China's Healthy China 2030 plan and Singapore's secure-data-sandbox regulations collectively speed clinical pilots. Nearly 600 health-AI start-ups now operate across Australia, China, Japan and Singapore, funnelling local datasets into disease-specific models attuned to regional genetics and care protocols. National Taiwan University Hospital's PANCREASaver underscores how indigenous innovation can secure both domestic deployment and US regulatory recognition.

Europe continues to prioritise cross-border research networks and ethical AI. The €28 million Thera4Care project, running across 29 sites, typifies the continent's collaborative template that pairs algorithm trials with standard-setting for explainability and data stewardship. While GDPR adds compliance overhead, the unified Medical Device Regulation shortens multinational launch sequencing once CE approval is obtained. Emerging regions-Middle East & Africa and South America-are still nascent but show accelerating interest as cloud connectivity widens. Pilot programmes with the World Health Organization that port ultra-compact lung-cancer detectors onto mobile X-ray vans illustrate the adaptability of contemporary AI stacks to infrastructure-light settings.

- Siemens Healthineers

- GE Healthcare

- IBM Corp.

- NVIDIA Corp.

- Varian Medical Systems

- Elekta

- Koninklijke Philips

- Tempus Labs

- Flatiron Health

- PathAI

- Azra AI

- ConcertAI

- Digital Diagnostics

- Median Technologies

- Radformation / Limbus AI

- DeepMind Health

- Intel Corp.

- Medtronic

- Canon

- Oncora Medical

- Paige AI

- Imagia Cybernetics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Cancer Burden Worldwide

- 4.2.2 Expanding Precision Medicine Programs

- 4.2.3 Integration of AI With Medical Imaging Modalities

- 4.2.4 Accelerated Approvals of AI-Based Oncology Devices

- 4.2.5 Rising Investments from Big Tech and Pharma

- 4.2.6 Proliferation of Cloud-Based Healthcare Data

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs and ROI Uncertainty

- 4.3.2 Stringent Data Privacy and Security Regulations

- 4.3.3 Limited Interoperability across Oncology IT Systems

- 4.3.4 Shortage of AI-Literate Oncology Workforce

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software Solutions

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Cancer Type

- 5.2.1 Breast Cancer

- 5.2.2 Lung Cancer

- 5.2.3 Prostate Cancer

- 5.2.4 Colorectal Cancer

- 5.2.5 Brain Tumor

- 5.2.6 Other Cancer Types

- 5.3 By Treatment Type

- 5.3.1 Radiotherapy

- 5.3.2 Chemotherapy

- 5.3.3 Immunotherapy

- 5.3.4 Other Treatment Types

- 5.4 By Application

- 5.4.1 Cancer Detection

- 5.4.2 Drug Discovery

- 5.4.3 Drug Development

- 5.4.4 Other Applications

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Siemens Healthineers AG

- 6.3.2 GE Healthcare

- 6.3.3 IBM Corp.

- 6.3.4 NVIDIA Corp.

- 6.3.5 Varian Medical Systems

- 6.3.6 Elekta AB

- 6.3.7 Philips Healthcare

- 6.3.8 Tempus Labs

- 6.3.9 Flatiron Health

- 6.3.10 PathAI

- 6.3.11 Azra AI

- 6.3.12 ConcertAI

- 6.3.13 Digital Diagnostics

- 6.3.14 Median Technologies

- 6.3.15 Radformation / Limbus AI

- 6.3.16 DeepMind Health

- 6.3.17 Intel Corp.

- 6.3.18 Medtronic

- 6.3.19 Canon Medical Systems

- 6.3.20 Oncora Medical

- 6.3.21 Paige AI

- 6.3.22 Imagia Cybernetics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment