|

시장보고서

상품코드

2072571

블랙 매스 재활용 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Black Mass Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

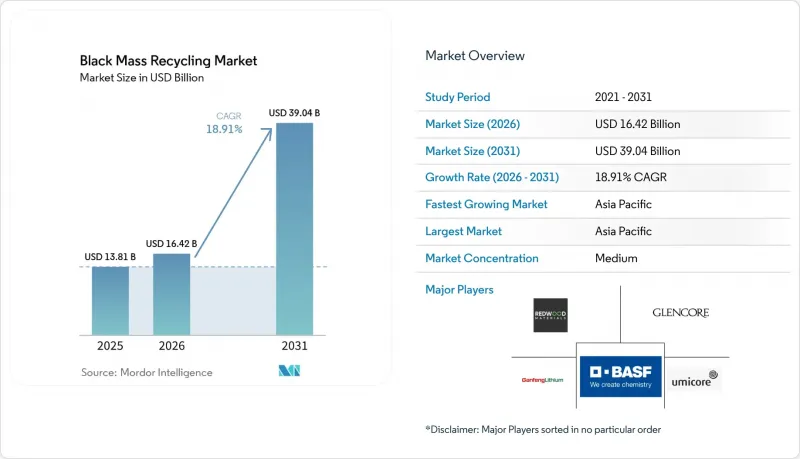

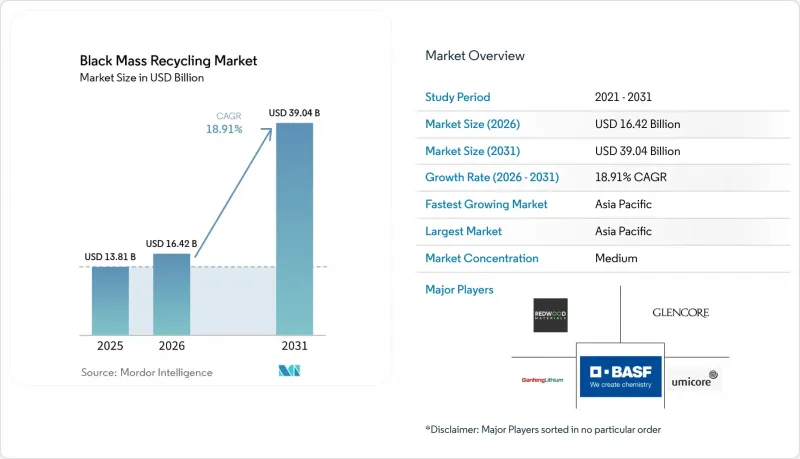

Mordor Intelligence에 의하면, 블랙 매스 재활용 시장 규모는 2026년에 164억 2,000만 달러에 달하고, 2031년까지 390억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR 18.91%로 성장할 전망입니다.

본 보고서는 배터리 유형(리튬이온, 납산, 전고체, 기타), 소재 유형(리튬, 코발트, 기타), 공급처(전기차용 배터리, 가전제품, 기타), 기술(열제련법, 습식 제련법, 기타 기술), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 블랙 매스 재활용 시장 동향 및 인사이트

리튬이온 기가팩토리의 급속한 확장

2025년, 전 세계 배터리 셀 생산 능력은 2,200GWh를 넘어섰으며, 2028년까지 800GWh가 추가로 증설될 예정입니다. 네바다주에 위치한 레드우드 머티리얼즈는 파나소닉 및 테슬라와 전략적으로 인접한 입지를 바탕으로, 재활용 시설을 동일한 부지 내에 설치함으로써 물류 시간을 48시간 이내로 단축할 수 있음을 입증하고 있습니다. 마찬가지로, 후난성에서는 CATL과 Brunp가 생산 과정에서 발생한 스크랩을 자사의 양극 전구체 공급망에 직접 재투입하고 있습니다. 자본 집약성은 큰 장벽이 되고 있습니다. Ascend Elements사는 켄튀르키예주에 연간 생산 능력 3만 톤 규모의 시설을 설립하기 위해 3억 1,000만 달러라는 거액을 투자하고 있으며, 이는 공장 자금 조달에 있어 오프테이크 계약이 필수적임을 여실히 보여주고 있습니다. 그 결과, 블랙매스 재활용 시장에서는 장기적인 원료 공급을 확보할 수 있는 수직 통합형 제조업체나 재활용 업체에게 점점 더 유리한 상황이 되고 있습니다.

EU와 중국의 전기차 제조업체에 대한 리콜 의무

2027년까지 EU의 배터리 규정은 휴대용 배터리의 회수율을 63%로 의무화하며, 2026년 12월부터는 블랙매스의 수출을 금지합니다(1). 2031년까지 자동차 제조업체는 신규 배터리에 재활용 코발트를 16%, 재활용 리튬을 6% 혼합해야 할 의무가 있으며, 이로 인해 국내 처리 업체와의 조기 협력이 촉진되고 있습니다. 중국의 추적성 코드 제도에서는 20kWh를 초과하는 배터리 팩에 대해 95%의 회수율을 요구하고 있어, 현지 자동차 제조업체들에게 회수 체계의 확보가 필수적입니다. 2025년, 폭스바겐이 잘츠기터에서 실시한 시범 사업에서는 ID 시리즈 배터리 팩 3,600톤을 처리했으나, 블랙매스 재활용 시장의 리튬 가격 하락으로 인해 여전히 적자 경영이 이어지고 있습니다.

미량 금속으로 인한 오염이 제품의 순도를 떨어뜨립니다.

블랙 매스 재활용 시장에서 파쇄 및 분쇄 과정에서 혼입되는 철, 알루미늄, 구리 부스러기로 인해 불순물 함유율이 0.5%를 초과하는 경우가 있습니다. 이로 인해 재활용된 소금은 고품질 양극재로 사용될 자격을 상실하게 됩니다. 이에 대해 재활용 업체들은 20미크론 크기의 불순물까지 감지할 수 있는 와전류 분리기나 고주파 유도 센서를 도입하여 대응하고 있습니다. 결정화 공정을 추가하면 운영 비용이 12% 증가하고, 리튬의 전체 수율이 떨어집니다. 순도 기준을 충족하지 못할 경우, 가공업체는 윤활유나 세라믹 등 이익률이 낮은 용도로 할인된 가격에 판매할 수밖에 없게 되어 수익성이 저하됩니다. 분석 장비 제조업체와의 공동 연구 개발 프로젝트에서는 현재 인라인 레이저 유도 파열 분광법(LIBS) 도입을 목표로 하고 있으나, 혼합 화학 물질의 교정이 과제로 남아 있어 실용화는 아직 초기 단계에 머물러 있습니다.

부문별 분석

2025년에는 전기차용 배터리가 블랙 매스 재활용 시장을 독점하며 58.23%의 점유율을 차지했습니다. 예측에 따르면, 해당 시장은 연평균 성장률(CAGR) 20.45%라는 견조한 성장을 보일 것으로 예상되며, 이를 통해 주도적 입지를 확고히할 것으로 보입니다. 자동차 배터리 팩 1개당 60-75Kg의 농축물을 얻을 수 있어, 플랜트의 가동 효율이 향상됩니다. 전력망용 배터리의 수명이 10-12년에 접어들면서, 에너지 저장 시스템은 수익성이 높은 백엔드 사업 기회로 부상하고 있습니다. 중국에서는 규제 대상의 회수율이 87%에 육박하는 반면, 북미는 50% 이하에 그치고 있어 원료의 안정적인 공급 측면에서 지역 간 격차가 두드러지게 나타나고 있습니다.

세컨드 라이프 에너지 저장 시스템을 활용함으로써, 전기차용 배터리 팩의 재활용 시기를 15년이라는 시점을 넘어 연장할 수 있을 가능성이 있습니다. 이러한 연장으로 인해 향후 공급량이 감소할 가능성이 있지만, 도시 지역의 가전제품이 그 공백을 메우는 역할을 할 것으로 보입니다. 산업용 전동 공구, 의료기기, 항공우주용 배터리는 총 톤수의 불과 6%에 불과하지만, 그 다양한 화학 성분으로 인해 공정 제어에 복잡성을 초래하고 있습니다. 중국에서는 OEM 추적 코드와 유럽의 의무적 회수 제도가 맞물려 구동용 배터리의 회수 효율이 향상될 전망입니다. EU의 정책을 따르는 캘리포니아주의 새로운 주법은 북미 시장 통합을 위한 길을 열어주고 있습니다.

NMC, NCA, LFP 등 다양한 화학 조성을 아우르는 리튬 이온 배터리는 리튬과 코발트를 최대 95%까지 회수할 수 있는 확립된 침출 공정이 존재하기 때문에 2025년에는 블랙매스 재활용 시장 규모의 49.35%를 차지했습니다. 높은 처리 능력, 익숙한 설비, 예측 가능한 자재 흐름을 통해 처리 비용은 경쟁사 수준을 유지하고 있습니다. 이 부문은 공정의 집약화, 특히 체류 시간을 40% 단축하는 마이크로파 지원 침출법의 혜택을 받고 있습니다. 그러나 고급 자동차 제조업체들이 요구하는 안전성과 에너지 밀도의 우위를 바탕으로, 고체 전지는 2030년에 연평균 성장률(CAGR) 20.23%라는 급속한 성장 궤도에 올라 있습니다. 다만, 해당 세라믹 전해질에는 알루미나와 황화물 매트릭스가 포함되어 있어, 현재 시범 검사 단계에 있는 맞춤형 화학적 또는 기계적 분리 방법이 요구되고 있습니다. 액체 및 고체 상태의 폐기물을 전환할 수 있는 다기능 플로우 시트를 정교하게 개발하는 재활용 기업은 제품 구성이 변화하는 가운데 선구자로서의 우위를 확보할 가능성이 높다고 볼 수 있습니다.

이러한 부문의 변화에 따라, 재리튬화를 위해 양극의 형태를 유지하는 직접 재활용 방식에 대한 연구가 촉진되어, 그 결과 전환 비용이 대폭 절감될 것입니다. 니켈수소 전지는 하이브리드 자동차 분야에서 여전히 중요한 위치를 차지하고 있지만, 블랙매스 처리량은 감소 추세를 보이고 있으며, 전문 처리 업체들은 처리량을 확보하기 위해 차량 플릿 운영 사업자와의 전략적 제휴를 모색하고 있습니다. 납축전지는 화학적 성질이 다르기 때문에 현대의 블랙매스 처리 라인에서는 사실상 제외되어 있으며, 그 확고히 자리 잡은 폐쇄형 네트워크는 여전히 독립적인 형태를 유지하고 있습니다. 수요가 증가함에 따라 산화환원 전위를 조절할 수 있는 유연한 습식 처리 라인이 표준이 되며, 처리 업체는 당시 프리미엄 가격을 기대할 수 있는 배터리 화학 계열에 맞추어 제품의 순도를 유연하게 조절할 수 있게 됩니다.

지역별 분석

아시아태평양은 2025년에 세계 블랙매스 재활용 시장 규모의 48.89%를 차지했으며, 중국, 일본, 한국을 중심으로 한 수직 통합형 배터리 밸류체인을 활용함으로써 2030년까지 연평균 성장률(CAGR) 22.25%를 나타낼 것으로 전망됩니다. 2024년 12월부터 시행된 중국의 흑연 수출 규제는 재활용 양극재에 대한 국내 수요를 확대시키고, 원료 확보를 목표로 하는 유럽의 음극 제조업체들이 합작 사업을 추진하도록 유도하고 있습니다. 자본 비용의 최대 30%를 지원하는 정부 보조금과 우대 전기 요금이 해당 지역의 선도적 지위를 더욱 공고히 하고 있습니다. 일본의 JX 메탈즈는 재생에너지를 활용하여 하이드로메트 공장을 최적화하고 있으며, 한국의 SK 테스는 화학 성분의 변동에 대비하기 위해 전자 폐기물 흐름과 자동차 배터리 팩을 결합하고 있습니다.

북미에서는 신규 시설의 내부수익률을 높이는 연방 세액 공제를 바탕으로, 블랙매스 재활용 시장의 생산 능력 확대가 가속화되고 있습니다. 레드우드 머티리얼즈는 네바다주와 사우스캐롤라이나주에서 다단계 복합 시설을 확장하고 있는 반면, BASF는 지역 전력 회사와 제휴하여 저탄소 전력 확보에 나서고 있습니다. 캐나다의 각 주는 주별 재활용 목표를 자동차 OEM의 생산 전망과 연계하고, 미국·멕시코·캐나다 협정(USMCA)에 따라 물류 효율화를 도모하는 국경을 넘는 자재 흐름을 촉진하고 있습니다. 멕시코의 조립 제조업체는 부피가 큰 배터리 팩을 북부 시설로 운송하는 비용을 절감하기 위해 사내에서 파쇄 처리를 검토하고 있습니다.

유럽의 엄격한 규제를 배경으로, 독일, 스웨덴, 폴란드에 위치한 블랙매스 재활용 시장의 고순도 습식 제련 허브에 대한 투자가 활발해지고 있으며, 이들 시설은 각각 현지 기가팩토리 클러스터와 연계되어 있습니다. 2027년에 운영을 시작할 예정인 ‘‘EU 배터리 여권'은 상세한 수명 주기 데이터의 제공을 의무화함으로써, 추적 가능하고 저탄소 배출을 실현하는 재활용 솔루션으로의 자본 유입을 촉진하고 있습니다. 아프리카 광산 업체와의 제휴를 통해 전처리된 정광이 유럽의 제련소로 공급되어, 공급 리스크를 분산시키고 있습니다. 중동 및 아프리카의 소규모 시장은 전처리나 방화 대책이 마련된 보관 시설과 같은 틈새 역할을 담당하고 있으며, 주요 해운 노선과 인접해 있다는 이점을 활용하고 있지만, 하류 수요가 제한적이라는 점으로 인해 여전히 제약을 받고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

제8장 CEO가 생각해야 할 중요 전략적 과제

KTH 26.07.03According to Mordor Intelligence, the black mass recycling market size is projected to be USD 16.42 billion in 2026 and reach USD 39.04 billion by 2031, growing at an 18.91% CAGR over 2026-2031.

This report is Segmented by Battery Type (Lithium-Ion, Lead-Acid, Solid-State, Others), Material Type (Lithium, Cobalt, Others), Source (EV Batteries, Consumer Electronics, Others), Technology (Pyrometallurgical, Hydrometallurgical, and Other Technology), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Black Mass Recycling Market Trends and Insights

Rapid Scale-up of Li-ion Gigafactories

In 2025, global cell production capacity exceeded 2,200 GWh, with an additional 800 GWh slated for completion before 2028. Redwood Materials, strategically positioned alongside Panasonic and Tesla in Nevada, demonstrates how co-located recycling can streamline logistics to under 48 hours. Similarly, in Hunan Province, CATL and Brunp are channeling production scrap directly back into their cathode precursor supply chains. Capital intensity is a significant hurdle: Ascend Elements invested a hefty USD 310 million to establish a 30,000-ton annual capacity in Kentucky, underscoring the necessity of offtake agreements for plant financing. As a result, the black mass recycling market increasingly favors vertically integrated manufacturers and recyclers that can secure long-term feedstock.

EV-OEM Take-back Mandates in EU & China

By 2027, the EU Battery Regulation mandates a 63% collection rate for portable cells and prohibits black mass exports starting December 2026[1]. By 2031, automakers are required to incorporate 16% recycled cobalt and 6% recycled lithium into new batteries, which is driving them to engage with domestic processors sooner. China's traceability-code system demands a 95% recovery rate for packs exceeding 20 kWh, making it essential for local OEMs to ensure collection. In 2025, Volkswagen's pilot in Salzgitter processed 3,600 tons of ID series packs, yet it continues to operate at a loss due to falling lithium prices in the black mass recycling market.

Trace-metal Contamination Reducing Output Purity

Iron, aluminium, and copper shavings introduced during shredding and milling in the black mass recycling market can push impurity levels beyond 0.5%, disqualifying recycled salts from premium cathode use. Recyclers respond by installing eddy-current separators and high-frequency inductive sensors that spot inclusions down to 20 microns. Additional crystallisation passes lift operating costs by 12% and shrink overall lithium yield. Failure to meet purity benchmarks forces processors to sell at discounts into lower-margin applications such as lubricants or ceramics, eroding profitability. Collaborative R&D projects with analytical-instrument suppliers now target in-line laser-induced breakdown spectroscopy, yet commercial deployment remains nascent given calibration challenges for mixed chemistries.

Other drivers and restraints analyzed in the detailed report include:

- Inflation Reduction Act Clean-material Tax Credits (US)

- Down-stream Demand from LFP-to-NMC Chemistry Switch

- High Capex for Fire-safe Black-mass Logistics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, EV batteries dominated the black mass recycling market, holding a 58.23% share. Forecasts predict a robust 20.45% CAGR growth for them, solidifying their leading position. Each automotive pack produces a concentrate yield of 60-75 kilograms, streamlining plant operations. As grid batteries reach the end of their 10-12 year lifespan, energy-storage systems are emerging as a lucrative back-end opportunity. While China boasts regulatory capture rates nearing 87%, North America lags with figures under 50%, highlighting regional disparities in feedstock security.

Utilizing second-life energy-storage could extend the recycling timeline for EV packs past the 15-year threshold. This extension might lead to a future supply dip, but urban consumer electronics could bridge the gap. Though industrial power tools, medical devices, and aerospace cells account for only 6% of the tonnage, their diverse chemistry introduces complexities in process control. In China, OEM traceability codes, combined with Europe's mandatory take-back schemes, are set to boost collection efficiency for traction batteries. California's new statewide law, echoing EU policies, paves the way for a unified North American market.

Lithium-ion packs, spanning NMC, NCA and LFP chemistries, generated 49.35% of Black Mass Recycling market size in 2025 owing to well-established leaching routes that recover up to 95% of lithium and cobalt. High throughput, familiar equipment, and predictable material flows keep processing costs competitive. The segment benefits from process intensification, notably microwave-assisted leaching that cuts residence times by 40%. However, solid-state cells are on a steep 20.23% CAGR trajectory toward 2030, fuelled by their safety and energy-density edge sought by premium automakers. Their ceramic electrolytes, though, introduce alumina and sulfide matrices that demand bespoke chemical or mechanical liberation methods now in pilot trials. Recycling firms that refine polyvalent flowsheets capable of toggling between liquid and solid-state waste are likely to gain early-mover advantage as product mix shifts.

The segmental shift boosts research into direct-recycling approaches that preserve cathode morphology for relithiation, thereby slashing conversion costs. Nickel-metal hydride batteries retain relevance in hybrid cars but contribute diminishing black-mass tonnage, pushing specialised processors toward strategic alliances with fleet operators to secure volume. Lead-acid units are largely excluded from modern black-mass lines due to divergent chemistry; their entrenched closed-loop networks remain distinct. As demand climbs, flexible hydromet lines with adjustable oxidation-reduction potentials will become standard, allowing processors to pivot output purity toward whichever battery chemistry commands premium pricing at any given time.

Complete Report Scope:

- By Battery Type

- Lithium-ion (NMC, NCA, LFP)

- Nickel-metal Hydride (NiMH)

- Lead-acid

- Solid-state (Emerging)

- Others

- By Material Type

- Lithium

- Cobalt

- Nickel

- Manganese

- Graphite

- Others

- By Source

- EV Batteries

- Consumer Electronics

- Energy-storage Systems

- Industrial Power Tools

- Others

- By Technology

- Pyrometallurgical Process

- Hydrometallurgical Process

- Combined (Hybrid) Processes

- Direct Recycling / Physical Separation

- Bio-leaching

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- South Africa

- United Arab Emirates

- Rest of Middle-East and Africa

- Asia-Pacific

Geography Analysis

Asia-Pacific produced 48.89% of the global Black Mass Recycling market size in 2025 and is forecast to post a 22.25% CAGR through 2030 as it leverages vertically integrated battery value chains centered in China, Japan, and South Korea. Chinese export controls on graphite, effective from December 2024, amplify domestic demand for recycled anode material and attract joint ventures from European cathode makers looking to safeguard feedstock. Government subsidies covering up to 30% of capital costs and preferential electricity tariffs further cement regional leadership. Japan's JX Metals optimises hydromet plants with renewable power, while Korea's SK tes combines e-waste streams with automotive packs to hedge chemistry fluctuations.

North America accelerates capacity in the black mass recycling market on the back of federal tax credits that enhance internal rates of return for new facilities. Redwood Materials expands multi-phase complexes in Nevada and South Carolina, while BASF partners with local utilities to secure low-carbon electricity. Canadian provinces align provincial recycling targets with automotive OEM production forecasts, fostering cross-border material flows that streamline logistics under the United States-Mexico-Canada Agreement (USMCA) trade pact. Mexican assemblers explore in-house shredding to reduce the cost of transporting bulky packs to northern facilities.

Europe's regulatory stringency fuels investment in high-purity hydrometallurgical hubs in the black mass recycling market located in Germany, Sweden and Poland, each tied to local gigafactory clusters. The EU Battery Passport, operational in 2027, mandates granular life-cycle data, steering capital towards traceable, low-emission recycling solutions. Collaborations with African miners supply pre-processed concentrates to European smelters, balancing supply risk. Smaller markets in the Middle East and Africa target niche roles in preprocessing and fire-safe storage, benefiting from proximity to shipping arteries but still constrained by limited downstream demand.

- American Battery Technology Company

- Ascend Elements, Inc.

- BASF

- Duesenfeld GmbH

- Fortum

- Ganfeng Lithium Group Co., Ltd

- Glencore

- Graphite One Inc.

- Li-Cycle Corp.

- Lithion Technologies

- Livium

- Metso

- Neometals Ltd

- Primobius GmbH

- RecycLiCo Battery Materials Inc.

- Redwood Materials Inc.

- SK Tes

- SungEel HITech

- Umicore

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid scale-up of Li-ion gigafactories

- 4.2.2 EV-OEM take-back mandates in European Union and China

- 4.2.3 Inflation Reduction Act clean-material tax credits

- 4.2.4 Down-stream demand from LFP-to-NMC chemistry switch

- 4.2.5 Municipal e-waste partnerships unlocking urban feedstock

- 4.3 Market Restraints

- 4.3.1 Trace-metal contamination reducing output purity

- 4.3.2 High capex for fire-safe black-mass logistics

- 4.3.3 Slow permitting cycles for new recycling plants

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Battery Type

- 5.1.1 Lithium-ion (NMC, NCA, LFP)

- 5.1.2 Nickel-metal Hydride (NiMH)

- 5.1.3 Lead-acid

- 5.1.4 Solid-state (Emerging)

- 5.1.5 Others

- 5.2 By Material Type

- 5.2.1 Lithium

- 5.2.2 Cobalt

- 5.2.3 Nickel

- 5.2.4 Manganese

- 5.2.5 Graphite

- 5.2.6 Others

- 5.3 By Source

- 5.3.1 EV Batteries

- 5.3.2 Consumer Electronics

- 5.3.3 Energy-storage Systems

- 5.3.4 Industrial Power Tools

- 5.3.5 Others

- 5.4 By Technology

- 5.4.1 Pyrometallurgical Process

- 5.4.2 Hydrometallurgical Process

- 5.4.3 Combined (Hybrid) Processes

- 5.4.4 Direct Recycling / Physical Separation

- 5.4.5 Bio-leaching

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 American Battery Technology Company

- 6.4.2 Ascend Elements, Inc.

- 6.4.3 BASF

- 6.4.4 Duesenfeld GmbH

- 6.4.5 Fortum

- 6.4.6 Ganfeng Lithium Group Co., Ltd

- 6.4.7 Glencore

- 6.4.8 Graphite One Inc.

- 6.4.9 Li-Cycle Corp.

- 6.4.10 Lithion Technologies

- 6.4.11 Livium

- 6.4.12 Metso

- 6.4.13 Neometals Ltd

- 6.4.14 Primobius GmbH

- 6.4.15 RecycLiCo Battery Materials Inc.

- 6.4.16 Redwood Materials Inc.

- 6.4.17 SK Tes

- 6.4.18 SungEel HiTech

- 6.4.19 Umicore

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment