|

시장보고서

상품코드

2072611

서버 스토리지 에어리어 네트워크(SAN) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2030년)Server Storage Area Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

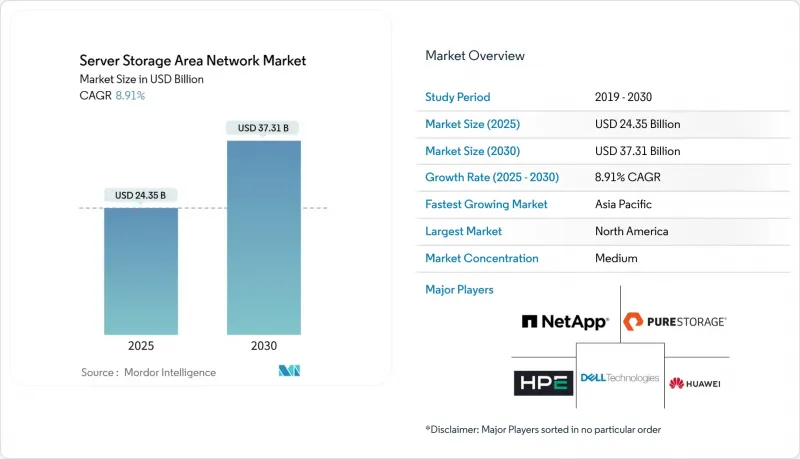

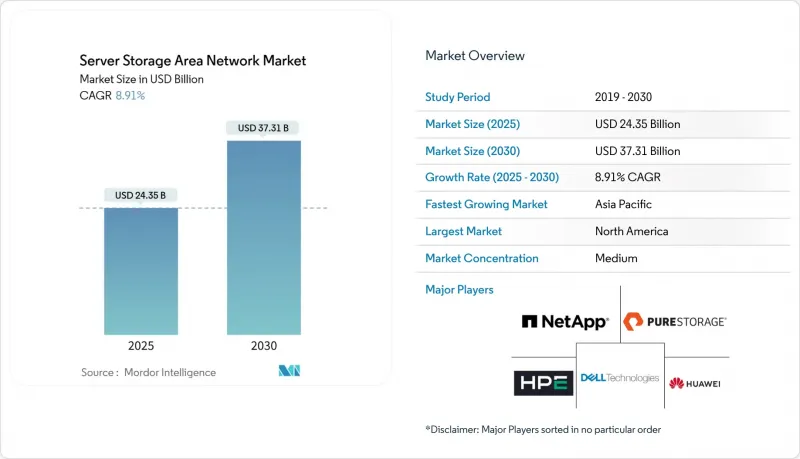

Mordor Intelligence에 의하면, 서버 스토리지 에어리어 네트워크(SAN) 시장 규모는 2025년에 243억 5,000만 달러로 평가되었고, 2030년까지 373억 1,000만 달러에 이를 것으로 예측되며, 동기 사이에 CAGR 8.91%로 성장할 전망입니다.

본 보고서는 제품 유형별(하드웨어, 소프트웨어, 서비스), 기술 유형별(파이버 채널 SAN, iSCSI SAN 등), 조직 규모별(대기업, 중소기업), 최종 사용자 산업별(IT 및 통신, 의료 및 생명과학, 미디어 및 엔터테인먼트 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 서버 스토리지 에어리어 네트워크(SAN) 시장 동향 및 인사이트

하이퍼스케일 데이터센터의 급속한 확장

각 클라우드 제공업체들은 2025년 초까지 신규 캠퍼스에 6,760억 달러 이상을 투자하며, 1.4 엑사플롭스에 육박하는 GPU 연산 능력을 갖춘 랙에 데이터를 공급할 수 있는 페타바이트 규모의 어레이에 대한 수요를 가속화하고 있습니다. 아마존은 펜실베이니아주와 노스캐롤라이나주의 거점에 300억 달러를 배정했으며, 구글은 PJM 송전망 업그레이드와 관련해 250억 달러를 지원하겠다고 약속했고, 마이크로소프트는 회계연도 내 건설에 800억 달러를 예산으로 편성했습니다. 이러한 프로젝트에는 랙 단위로 10마이크로초 미만의 지연 시간으로 AI 데이터 세트를 불러오고, 체크포인트를 생성하며, 스트리밍할 수 있는 스토리지 패브릭이 필요합니다. 각 벤더사는 계층화를 균등화하고, CXL 연결 메모리를 풀링하며, 동서 방향의 혼잡을 해소하는 긴밀하게 통합된 컴퓨팅·스토리지 노드를 통해 이에 대응하고 있습니다. 또한, 이러한 지출의 급증으로 인해 가격 결정권이 구매자 쪽으로 옮겨가고 있으며, 공급업체들은 수년에 걸친 리프레시 계약의 락인(lock-in)을 확보하기 위해 라이프사이클 관리 서비스나 에너지 효율이 높은 컨트롤러를 번들로 제공해야 하는 압박을 받고 있습니다. 전반적으로 볼 때, 이러한 투자 열풍은 서버 스토리지 에어리어 네트워크 시장의 연평균 성장률(CAGR)을 2.8% 끌어올리는 요인이 되고 있습니다.

소프트웨어 정의형 및 하이퍼컨버지드 스토리지로의 전환

거시경제의 불확실성과 기술 인력 부족에 직면한 기업들은 어플라이언스 기반의 하이퍼컨버지드 인프라로 전환하여, 사우지-저먼 헬스(Saudi German Health)의 Nutanix 도입 사례와 같이 하드웨어 비용을 최대 40% 절감하고, 백업 시간을 4시간에서 1시간 미만으로 단축하는 데 성공했습니다. 현재 신규 도입 사례의 75%에서는 컴퓨팅, 스토리지, 네트워크를 통합한 벤더 통합형 노드가 채택되고 있으며, 소규모 IT 팀도 단일 GUI를 통해 대규모 클러스터를 관리할 수 있게 되었습니다. 또한, 이러한 시스템은 RESTful API를 공개하고 있으며, 정책 기반 자동화를 구현함으로써 AI 추론 트래픽이 급증할 때 처리량을 동적으로 확장할 수 있습니다. 수익 모델은 영구 라이선스에서 구독 모델로 전환되면서 현금 흐름이 안정화되는 한편, 벤더 종속 현상이 더욱 심화되고 있습니다. 그 결과, ‘소프트웨어 퍼스트’ 전략 덕분에 서버 스토리지 에어리어 네트워크(SAN) 시장의 연평균 성장률(CAGR)이 2.1포인트 상승했습니다.

올플래시 어레이의 높은 초기 설비 투자(CAPEX)

NAND 제조업체들은 2024년에 웨이퍼 생산 시작 물량을 최대 25% 줄였으나, AI 수요의 급증으로 공급 과잉이 해소되면서 2025년 3월에는 엔터프라이즈용 SSD 가격이 10% 이상 상승했습니다. 중복 구성이 적용된 400 GbE 광 모듈을 탑재한 새로운 NVMe-oF 패브릭은 동급의 16Gb FC를 업그레이드하는 것에 비해 4-6배의 비용이 들 수 있으므로, CFO는 도입을 단계적으로 진행하거나, 스토리지-어즈-어-서비스(Storage-as-a-Service)를 채택할 수밖에 없는 상황에 처해 있습니다. 미국의 철강 제조업체가 Celona를 활용해 현대화를 이룬 사례에서 볼 수 있듯이, 운영 비용 절감분을 반영하면 투자 회수 기간이 3개월 미만으로 단축될 가능성이 있지만, 자금 사정에 어려움을 겪고 있는 중소기업에게는 여전히 자금 조달의 어려움이 심각한 과제로 남아 있습니다. 그 결과, 설비 투자(CAPEX) 증가로 인해 단기적으로는 서버 스토리지 에어리어 네트워크(SAN) 시장의 연평균 성장률(CAGR)이 1.4포인트 하락할 것으로 전망됩니다.

부문별 분석

2024년에도 하드웨어가 여전히 최대 수익원으로 자리매김했으며, 기업들이 GPU 팜을 가동하기 위해 고밀도 NVMe 셸프를 지속적으로 도입함에 따라 서버 스토리지 에어리어 네트워크(SAN) 시장 점유율의 46.71%를 차지했습니다. 한편, 서비스 부문은 구매자들이 CAPEX를 OPEX로 전환하고 지속적인 업그레이드를 보장하는 종량제 계약으로 몰리고 있어, 연평균 성장률(CAGR) 11.23%로 확대될 것으로 전망됩니다. NetApp의 'Keystone'는 2025 회계연도 동안 계약 총액을 2배 이상 늘려 약 1억 5,000만 달러에 달했습니다. 한편, Pure Storage의 'Evergreen//One'은 City National Bank가 시스템을 전면적으로 개편하지 않고도 새로운 환경을 구축하는 데 도움이 되었습니다. 각 벤더사는 랜섬웨어 대응 보장, 전력 사용 현황 대시보드, 예방적 부품 교체를 패키지로 묶어 도입 위험을 줄이고, 해당 서비스를 서버 스토리지 에어리어 네트워크(SAN) 시장의 전략적 성장 동력으로 자리매김하고 있습니다.

이러한 변화는 예측 가능성, 업무 부담 경감, 그리고 지속가능성 보고를 중시하는 보다 광범위한 IT 조달 동향을 반영하고 있습니다. 기업 측은 인력, 공과금 및 사무실 공간 절감분을 고려할 때, 자체 관리형 어레이에 비해 총 소유 비용(TCO)이 20% 감소한다고 지적하고 있습니다. 중소기업에게 있어 이 모델은 전문 관리자가 없어도 Tier 1 수준의 기능을 활용할 수 있는 '균등화 요인'로 간주되고 있습니다. 이와 동시에, 계층화 및 이상 감지를 자동화하는 AI 기반 분석을 바탕으로 소프트웨어 매출이 꾸준히 증가하고 있습니다. 전반적으로, 이러한 서비스의 동향이 서버 스토리지 에어리어 네트워크(SAN) 시장의 장기적인 회복력을 뒷받침하고 있습니다.

파이버 채널은 확고히 자리 잡은 미션 크리티컬 워크로드 덕분에 2024년 매출의 39.87%를 차지했으나, 고성능이 요구되는 AI 및 분석 분야가 NVMe-oF 패브릭을 선택함에 따라 그 성장세는 둔화되고 있으며, NVMe-oF 패브릭은 연평균 성장률(CAGR) 10.67%로 성장을 지속하고 있습니다. RDMA-over-Converged-Ethernet은 저속한 직렬 SCSI 변환을 배제하고 NVMe 네임스페이스에 직접 액세스함으로써 지연 시간을 10마이크로초 미만으로 줄입니다. 하이퍼스케일러는 CXL 스위치를 통해 연결된 컨트롤러가 없는 풀링된 스토리지 블레이드를 도입함으로써 경로 길이를 더욱 단축하고 있습니다. 하이퍼컨버지드/vSAN 노드는 피크 속도보다 편의성이 중시되는 엣지 및 부서 수준의 거점에서 증가하고 있는 반면, iSCSI는 비용 효율성이 중요한 아카이브 환경에서만 여전히 사용되고 있습니다.

이러한 기술 전환으로 인해 무전기 및 ASIC 공급업체들은 공급 측면에서 압박을 받고 있으며, 800 GbE 광 모듈의 리드타임은 최대 18개월에 달하고 있습니다. 각 벤더사는 문제 해결로 인한 지연을 방지하기 위해 여러 광모듈 제조업체를 인증하고, 자동 협상용 펌웨어에 대한 사전 인증을 실시함으로써 위험을 분산하고 있습니다. 상호 운용성이 안정됨에 따라 기업들은 2027년까지 NVMe-oF 가격이 15-20% 하락할 것으로 예상하고 있으며, 이에 따라 파이버 채널의 도입 기반은 더욱 축소될 전망입니다. 그 결과, NVMe-oF는 서버 스토리지 에어리어 네트워크(SAN) 시장의 사실상 중추로 부상할 전망입니다.

지역별 분석

북미 매출 점유율 36.82%는 하이퍼스케일 분야로의 집중, AI 네이티브 환경의 적극적인 구축, 그리고 NVMe-oF, 컴퓨테이셔널 스토리지, CXL 메모리 풀링의 조기 도입을 반영하고 있습니다. 2025년 초에는 미국 기업들만 해도 6,760억 달러 이상이 투자되었으며, 아마존은 펜실베이니아주와 노스캐롤라이나주에 걸쳐 있는 고전력 밀도 캠퍼스에 1,000억 달러를 투자했습니다. 캐나다에서는 탄소 중립형 코로케이션에 대한 주 정부의 우대 조치가 성장을 뒷받침하고 있으며, 멕시코에서는 니어쇼어링과 자동차 산업의 디지털화가 호재로 작용하고 있습니다. 방위 및 공공 안전 분야의 엣지 디바이스에 대한 정부 자금 지원 또한 시장 기회를 더욱 확대되고 있습니다.

아시아태평양의 연평균 성장률(CAGR) 9.53%는 성숙한 클라우드 생태계, 활기를 띠고 있는 핀테크 허브, 그리고 엄격한 데이터 거주 요건 체계에 기인합니다. 중국의 '사이버 보안법' 및 베트남의 데이터 현지화 관련 법규에 따라 다국적 기업들은 국내에 스토리지 팜을 운영해야 할 의무가 있으며, 이에 따라 주권 클라우드 내의 하이퍼컨버지드 vSAN 클러스터에 대한 수요가 증가하고 있습니다. 일본의 대형 은행들은 트랜잭션 시간 SLA를 충족하기 위해 파이버 채널을 NVMe-oF로 업그레이드하고 있습니다. 한편, 인도의 공적 부문 은행들은 인도 중앙은행의 실시간 결제 지침을 준수하기 위해 워크로드를 플래시 어레이로 이전하고 있습니다. 동남아시아의 통신 사업자들은 비디오 스트리밍 및 모바일 게임의 백홀 지연을 줄이기 위해 호텔에 위치한 베이스밴드 사이트에 마이크로 SAN을 도입하고 있습니다.

유럽의 꾸준한 성장세는 규정 준수를 중심으로 한 혁신과 국경을 초월한 엣지 페더레이션 덕분입니다. EU 데이터법은 상호 운용성을 의무화하고 있으며, 서비스 제공업체에 대해 개방형 API 및 양방향 마이그레이션 툴킷의 설계를 요구하고 있습니다. 독일과 북유럽 국가들에서는 재생에너지망을 전원으로 하는 에너지 효율이 높은 어레이를 우선적으로 도입하고 있습니다. 프랑스에서는 환자 데이터 보관 의무를 이행하기 위해 의료 영상 저장소에 올플래시 스토리지 도입을 확대되고 있습니다. 영국에서는 자동차 및 생명과학 컨소시엄과 연계된 AI 연구 클러스터를 지원하기 위해 하이퍼컨버지드 노드에 대한 투자가 진행되고 있습니다. 전반적으로, 지역별 복잡성과 주권 관련 우려가 서버 스토리지 에어리어 네트워크(SAN) 시장에 대한 지속적인 수요를 창출하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the server storage area network market size stood at USD 24.35 billion in 2025 and is forecast to reach USD 37.31 billion by 2030, advancing at an 8.91% CAGR over the period.

This report is Segmented by Product Type (Hardware, Software, and Services), Technology Type (Fibre Channel SAN, ISCSI SAN, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (IT and Telecom, Healthcare and Life-Sciences, Media and Entertainment, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Server Storage Area Network Market Trends and Insights

Rapid Hyperscale Data-Center Build-Outs

Cloud providers committed more than USD 676 billion to new campuses during early 2025, accelerating demand for petabyte-scale arrays capable of feeding racks that approach 1.4 exaFLOPS of GPU compute. Amazon earmarked USD 30 billion for sites in Pennsylvania and North Carolina, Google pledged USD 25 billion tied to PJM grid upgrades, and Microsoft budgeted USD 80 billion for fiscal-year builds. These projects require storage fabrics that ingest, checkpoint and stream AI data sets with sub-ten-microsecond latency at rack scale. Vendors are responding with tightly integrated compute-storage nodes that flatten tiering, pool CXL-attached memory and eliminate east-west congestion. The spending surge also shifts pricing power to buyers, pushing suppliers to bundle lifecycle management services and energy-efficient controllers to win multiyear refresh lock-ins. Collectively, the capital wave contributes a 2.8-percentage-point uplift to the Server Storage Area Network market CAGR.

Shift to Software-Defined and Hyper-Converged Storage

Enterprises facing macroeconomic uncertainty and skill shortages pivoted toward appliance-based hyper-converged infrastructure, achieving up to 40% hardware savings and shrinking backup windows from four hours to under one hour in deployments such as Saudi German Health's Nutanix rollout. Seventy-five percent of new rollouts now use vendor-integrated nodes that merge compute, storage and networking, allowing small IT teams to administer vast clusters through a single GUI. These systems also expose RESTful APIs, enabling policy-based automation that dynamically extends volumes for AI inference spikes. Financial models have shifted from perpetual licenses to subscription, smoothing cash flow and deepening vendor lock-in. As a result, software-first strategies are adding 2.1 percentage points to the Server Storage Area Network market CAGR.

High Upfront CAPEX of All-Flash Arrays

NAND vendors cut wafer starts by up to 25% during 2024, but surging AI demand reversed the glut and pushed enterprise SSD prices more than 10% higher in March 2025. A new NVMe-oF fabric with redundant 400 GbE optics can cost four to six times more than a like-for-like 16 Gb FC refresh, forcing CFOs to stage deployments or adopt storage-as-a-service. Although payback periods can drop below three months when operational savings are tallied-as in a U.S. steel manufacturer's Celona-enabled modernization-liquidity constraints remain acute for cash-strapped SMEs. Consequently, elevated CAPEX shaves 1.4 percentage points from the Server Storage Area Network market CAGR in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of NVMe-over-Fabrics for Ultra-Low Latency

- Emergence of Computational Storage Off-Loads

- Multi-Vendor Interoperability and Legacy Lock-In

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware remained the largest revenue contributor in 2024, capturing 46.71% of Server Storage Area Network market share as enterprises continued rolling out high-density NVMe shelves to feed GPU farms. The services line, however, is forecast to expand at an 11.23% CAGR as buyers flock to consumption contracts that convert capex to opex and guarantee evergreen upgrades. NetApp's Keystone more than doubled total contract value to nearly USD 150 million during fiscal 2025, while Pure Storage's Evergreen//One helped City National Bank spin up new environments without forklift refreshes. Vendors bundle ransomware warranties, power-use dashboards and proactive component replacement to de-risk adoption, positioning services as the strategic growth lever for the Server Storage Area Network market.

The pivot reflects broader IT procurement trends favoring predictability, labor off-load and sustainability reporting. Enterprises cite 20% lower total cost of ownership versus self-managed arrays once staffing, utility and floor-space savings are counted. Smaller firms view the model as an equalizer that grants access to Tier-1 features without specialized administrators. In parallel, software revenues rise steadily on the back of AI-driven analytics that automate tiering and anomaly detection. All told, the services trajectory anchors long-run resilience of the Server Storage Area Network market.

Fibre Channel still delivered 39.87% of 2024 revenue thanks to entrenched mission-critical workloads, yet its growth is flattening as performance-hungry AI and analytics choose NVMe-oF fabrics posting a 10.67% CAGR. RDMA-over-Converged-Ethernet eliminates slow Serialized SCSI translation, directly accessing NVMe namespaces and slashing latency below ten microseconds. Hyperscalers further shrink path length by deploying controller-free, pooled storage blades attached via CXL switches. Hyper-converged/vSAN nodes grow in edge and departmental sites where simplicity trumps peak speed, while iSCSI lingers only in cost-sensitive archives.

The technology shift places transceiver and ASIC vendors under supply stress, lengthening lead times to up to 18 months for 800 GbE optics. Vendors hedge by qualifying multiple optic manufacturers and pre-certifying auto-negotiation firmware to avoid troubleshooting delays. As interoperability stabilizes, enterprises expect NVMe-oF pricing to drop 15-20% by 2027, further eroding Fibre Channel's installed base. Consequently, NVMe-oF is set to emerge as the de-facto backbone of the Server Storage Area Network market.

Complete Report Scope:

- By Product Type

- Hardware

- Software

- Services

- By Technology Type

- Fibre Channel SAN

- iSCSI SAN

- Hyper-converged / vSAN

- NVMe-oF SAN

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Industry

- Banking, Financial Services and Insurance (BFSI)

- IT and Telecom

- Healthcare and Life-Sciences

- Media and Entertainment

- Cloud Service Providers

- Government and Public Sector

- Manufacturing

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America's 36.82% revenue share mirrors hyperscale concentration, aggressive AI-native build-outs and early adoption of NVMe-oF, computational storage and CXL memory pooling. U.S. players alone invested more than USD 676 billion during early 2025, with Amazon dedicating USD 100 billion to power-dense campuses across Pennsylvania and North Carolina. Canada adds growth through provincial incentives for carbon-neutral colocation, while Mexico gains from near-shoring and automotive digitization. Government funding for edge devices in defense and public safety further widens market opportunity.

Asia-Pacific's 9.53% CAGR stems from maturing cloud ecosystems, thriving fintech hubs and strict data-residency frameworks. China's Cybersecurity Law and Vietnam's data-localization statutes oblige multinationals to operate in-country storage farms, boosting demand for hyper-converged vSAN clusters within sovereign clouds. Japan's megabanks refresh Fibre Channel with NVMe-oF to meet transaction-time SLAs, whereas India's public-sector banks migrate workloads to flash arrays to align with the Reserve Bank's real-time settlement directives. South-east Asian telcos deploy micro-SANs at base-band hotel sites to reduce backhaul latency for video streaming and mobile gaming.

Europe's steady trajectory owes to compliance-driven refreshes and cross-border edge federations. The EU Data Act enforces interoperability, pushing providers to design open APIs and bidirectional migration toolkits. Germany and the Nordics prioritize energy-efficient arrays powered by renewable grids. France expands all-flash adoption within medical imaging repositories to meet patient data retention mandates. The United Kingdom invests in hyper-converged nodes to support AI research clusters tied to automotive and life-sciences consortia. Cumulatively, regional complexity and sovereignty concerns generate sustainable demand for the Server Storage Area Network market.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- NetApp Inc.

- Pure Storage Inc.

- Huawei Technologies Co., Ltd.

- International Business Machines Corporation

- Hitachi Vantara LLC (Hitachi Ltd.)

- Fujitsu Limited

- Inspur Electronic Information Industry Co., Ltd.

- Super Micro Computer, Inc.

- Lenovo Group Limited

- Western Digital Corporation

- Seagate Technology Holdings plc

- NEC Corporation

- Cisco Systems, Inc.

- VMware, Inc.

- Nutanix, Inc.

- StorCentric, Inc.

- QSAN Technology, Inc.

- Infinidat Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid hyperscale data-center build-outs

- 4.2.2 Shift to software-defined and hyper-converged storage

- 4.2.3 Adoption of NVMe-over-Fabrics for ultra-low latency

- 4.2.4 Emergence of computational storage off-loads

- 4.2.5 Edge-localized micro-SANs for sovereign data control

- 4.2.6 CXL-based memory pooling enabling disaggregated SAN

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX of all-flash arrays and fabrics

- 4.3.2 Multi-vendor interoperability and legacy lock-in

- 4.3.3 Skills gap in RDMA / NVMe-oF configuration

- 4.3.4 ASIC and optical-transceiver supply-chain risks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Technology Type

- 5.2.1 Fibre Channel SAN

- 5.2.2 iSCSI SAN

- 5.2.3 Hyper-converged / vSAN

- 5.2.4 NVMe-oF SAN

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 IT and Telecom

- 5.4.3 Healthcare and Life-Sciences

- 5.4.4 Media and Entertainment

- 5.4.5 Cloud Service Providers

- 5.4.6 Government and Public Sector

- 5.4.7 Manufacturing

- 5.4.8 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Dell Technologies Inc.

- 6.4.2 Hewlett Packard Enterprise Company

- 6.4.3 NetApp Inc.

- 6.4.4 Pure Storage Inc.

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 International Business Machines Corporation

- 6.4.7 Hitachi Vantara LLC (Hitachi Ltd.)

- 6.4.8 Fujitsu Limited

- 6.4.9 Inspur Electronic Information Industry Co., Ltd.

- 6.4.10 Super Micro Computer, Inc.

- 6.4.11 Lenovo Group Limited

- 6.4.12 Western Digital Corporation

- 6.4.13 Seagate Technology Holdings plc

- 6.4.14 NEC Corporation

- 6.4.15 Cisco Systems, Inc.

- 6.4.16 VMware, Inc.

- 6.4.17 Nutanix, Inc.

- 6.4.18 StorCentric, Inc.

- 6.4.19 QSAN Technology, Inc.

- 6.4.20 Infinidat Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment