|

시장보고서

상품코드

2072619

TV 방송 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Television Broadcasting Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

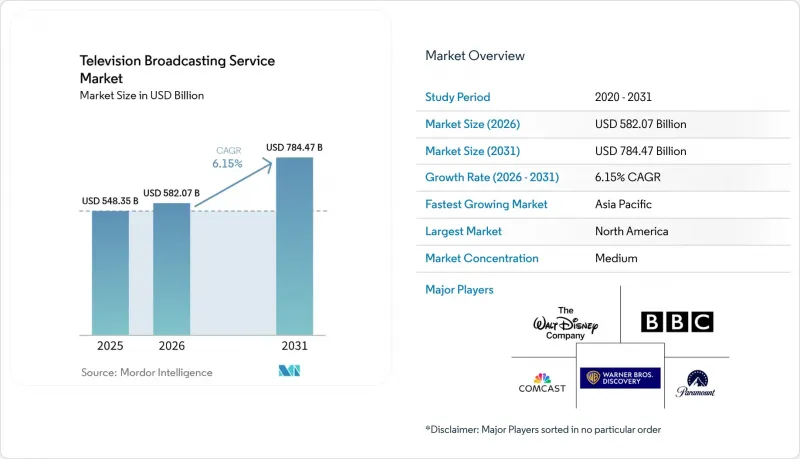

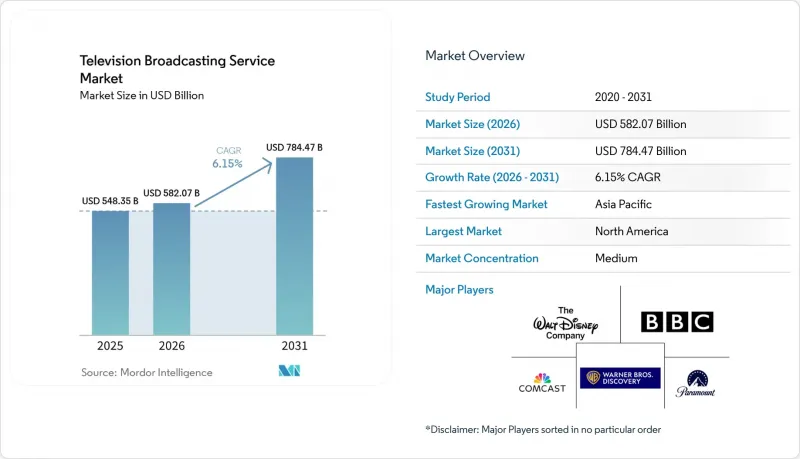

Mordor Intelligence에 의하면, TV 방송 서비스 시장 규모는 2025년에 5,483억 5,000만 달러로 평가되었고, 2026년 5,820억 7,000만 달러로 추정되고, 2031년까지 7,844억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.15%를 나타낼 전망입니다.

본 보고서는 전송 플랫폼별(지상파 TV, 케이블 TV, IPTV, OTT 및 인터넷 TV, 기타), 서비스 유형별(구독형, 광고 지원형, 기타), 방송국 유형별(공영 방송, 민영 방송, 기타), 컨텐츠 장르별(엔터테인먼트 및 드라마, 스포츠, 뉴스 및 시사 문제, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 TV 방송 서비스 시장 동향 및 인사이트

'코드 커팅'이 OTT와 스트리밍 TV의 보급을 뒷받침하고 있습니다.

2026년 1월, TV 이용 총량에서 스트리밍이 차지하는 비중은 47%에 달했으며, 12개월 동안 5.4포인트 상승했습니다. 각 가구는 고속 광대역 서비스를 유지하면서, 다중 채널 번들 계약을 해지하고, 주문형 컨텐츠 라이브러리와 실시간 선형 채널을 결합한 알라카르트형 앱으로 지출을 전환하고 있습니다. 컴캐스트는 2025년 4분기, 국내 선형 유료 TV 가입자 수가 전년 동기 대비 10% 감소했으나, 한편으로는 '피콕'는 같은 기간 동안 유료 가입자를 12% 늘렸습니다. 광고 수익으로 운영되는 무료 서비스는 가입비가 전혀 들지 않기 때문에 서비스 전환의 장벽이 크게 낮아져, 케이블 TV 해지를 가속화하고 있습니다. 2026년 1월까지 Tubi와 The Roku Channel은 각각 시청 점유율에서 한 자릿수 중반대 증가세를 기록했습니다. 따라서 방송사들은 스트리밍 계약 협상보다 원활한 앱 사용 경험과 풍부한 컨텐츠 라이브러리를 우선시하며, 자본을 D2C(소비자 직접 판매) 기술로 전환하고 있습니다.

라이브 스포츠 광고 슬롯에 대한 광고주 수요 증가

2014-2024년 스포츠 중계권 가치는 113% 상승했으며, 브랜드들이 실시간 도달 범위와 높은 참여도를 중시함에 따라 광고 시장의 전반적인 성장률을 훨씬 웃돌았습니다. 넷플릭스가 일본에서 선보이는 '월드 베이스볼 클래식'의 생중계는 3,140만 명의 시청자를 모았으며, 이는 구독 기반 플랫폼조차도 독점적인 라이브 이벤트에는 높은 요금을 지불할 의향이 있음을 보여줍니다. FAST 서비스에서 스포츠 채널의 광고 수익은 105% 증가했으며, 광고 기억률도 숏폼 동영상보다 71% 더 높았습니다. 재정력이 탄탄한 스트리밍 서비스와 전국 방송사들이 주목도가 높은 컨텐츠를 독점하고 있기 때문에 지역 방송사들은 틈새 스포츠나 보조적인 프로그램 편성 쪽으로 방향을 전환할 수밖에 없게 되었습니다.

SVOD 플랫폼이 선형 방송 시청자를 빼앗고 있습니다.

워너 브라더스 디스커버리의 2025년 4분기 선형 네트워크 매출은 스트리밍 가입자가 1억 3,160만 명으로 증가했음에도 불구하고, 전년 동기 대비 12% 감소했습니다. 시청자의 이동에 따라 리니어 광고 슬롯은 축소되고 있으며, SVOD의 시청자 1인당 수익은 정규 방송보다 낮아지고 있습니다. 컴캐스트는 2025년 4분기에 국내 유료 TV 가입 가구의 10%를 잃게 되며, 10년에 걸친 '코드 커팅'의 움직임이 더욱 거세졌습니다. 따라서 방송사는 기존 네트워크를 유지하면서 소비자용 직접 스트리밍 앱을 운영하기 위한 중복된 인프라에 자금을 투입해야 하므로, 전환 기간 동안 수익성이 압박받고 있습니다.

부문별 분석

OTT와 인터넷 TV는 2025년 TV 방송 서비스 시장 매출의 36.45%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 6.57%로 성장할 전망입니다. 이러한 급증은 스트리밍 앱을 전면에 내세운 스마트 TV의 OS와, 동영상 트래픽에 대해 제로레이팅을 적용하는 모바일 네트워크의 보급을 반영하고 있습니다. 케이블 및 위성 방송은 여전히 지방 및 연안 지역의 방송 송출 기반이 되고 있지만, 저지구궤도 광대역 서비스가 3년 이내에 현실적인 대안으로 자리 잡을 전망인 만큼 가입자 수는 계속 감소하고 있습니다. 지상파 TV는 ATSC 3.0의 양방향성 혜택을 누리고 있지만, 주파수 재편으로 인해 그 확대가 제한되고 있습니다. IPTV 시장 점유율은 광섬유 인프라가 구축된 지역의 통신 사업자들이 제공하는 번들 서비스에 국한된 상태입니다.

방송 사업자들은 현재 통합된 기술 스택을 도입하여, 하나의 컨텐츠가 리니어 채널, 온디맨드 에피소드, 동적 광고 삽입 기능을 갖춘 FAST 피드로 제공되도록 하고 있습니다. 파라마운트는 2025년 4분기에 Paramount+와 Pluto TV의 워크플로를 통합하여 스트림당 비용을 15% 절감했습니다. 이 모델은 시청자의 취향 변화에 대응하면서도 규모의 경제를 확보하고, 기존 형태를 완전히 잠식하지 않으면서 OTT 플랫폼용 TV 방송 서비스 시장 규모가 확대될 것을 보장합니다.

광고 지원형 서비스는 2025년 매출의 55.78%를 차지한 것으로 평가되었으며, 가계 예산 부담에 대한 우려가 커지는 가운데 구독 서비스의 성장률을 상회하는 연평균 성장률(CAGR) 6.88%로 확대될 것으로 전망됩니다. 넷플릭스의 광고 포함 요금제는 2026년 1분기에 월간 활성 사용자 수 1억 9,000만 명을 달성하며, 분기 매출을 122억 5,000만 달러로 대폭 끌어올렸습니다. Roku의 2025년 4분기 플랫폼 매출액 12억 2,000만 달러는 FAST 모델의 경제성을 입증하는 것으로, 시청 완료율 향상과 정교한 타겟팅을 통해 CPM이 상승하고 있습니다.

구독 서비스는 여전히 대히트 오리지널 작품의 기반이 되고 있지만, 컨텐츠 카탈로그의 업데이트가 정체되면 해지율이 급증하는 상황에 직면하게 됩니다. 현재는 하이브리드 모델이 주류를 이루고 있으며, 광고가 포함된 무료 요금제라는 '입구'를 통해 사용자를 프리미엄 요금제로 유도하고, 소득 분포 전반에 걸친 '지불 의향액'를 포함하고 있습니다. 그 결과, TV 방송 서비스 시장 점유율 구조는 광고 주도형으로 회귀하고 있지만, 프로그래매틱 시스템을 통한 광고 슬롯 판매의 자동화로 인해 이익률은 향상되고 있습니다.

지역별 분석

아시아태평양은 인도의 OTT 시장이 비약적으로 성장하고, 중국에서 정부 자금을 투입해 5G 방송 인프라를 구축한 데 힘입어 2025년 매출의 32.87%를 차지했습니다. Zee5가 5억 6,400만 루피(680만 달러)로 EBITDA 흑자를 달성한 것은 지역 언어 플랫폼의 단위 경제성 실현 가능성을 입증하고 있습니다. 한국에서는 TVING과 Wavve의 통합으로 광고 수익이 74.7% 증가했으며, 후지 TV가 F1 독점 중계권을 확보한 것은 프리미엄 스포츠에 대한 충성도를 강화하기 위한 도박이 되었습니다.

북미와 유럽의 기존 TV 플랫폼은 관리된 감소 추세를 보이고 있지만, 이는 스트리밍 서비스의 성장으로 상쇄되고 있습니다. 2026년 1분기까지 Peacock의 유료 가입자 수는 12% 증가해 4,600만 명에 달한 반면, Comcast의 기존 TV 가입자 수는 10% 감소했습니다. FCC가 제안한 ATSC 1.0의 폐지는 IP 중심의 전송 모델로의 전환을 가속화하고 있습니다. 한편, 유럽의 방송 할당 쿼터 및 소유주 상한 규제는 해당 지역의 산업 재편 움직임에 복잡성을 더하고 있습니다.

중동은 현지 스튜디오에 대한 정부계 펀드의 지원과 4K HDR 리니어 채널을 가능하게 하는 FTTH(광 FTTH) 인프라 구축에 힘입어 7.98%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 남미에서는 브라질의 'Globoplay'가 중심적인 역할을 하고 있으며, 다운로드 수는 1억 건을 넘어섰고, 포르투갈어권 축구 중계권을 활용해 전 세계 신생 기업들의 공세를 막아내고 있습니다. 아프리카는 광대역 요금이 비싸 보급이 제한적이며 여전히 발전 단계에 머물러 있지만, 모바일 우선 비즈니스 모델을 통해 예측 기간 후반에는 뒤처진 부분을 만회할 만한 성장이 예상됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the television broadcasting service market size was valued at USD 548.35 billion in 2025 and estimated to grow from USD 582.07 billion in 2026 to reach USD 784.47 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031).

This report is Segmented by Delivery Platform (Terrestrial Broadcast TV, Cable TV, IPTV, OTT/Internet TV, and More), Service Type (Subscription-Based, Advertising-Supported, and More), Broadcaster Type (Public Service, Commercial, and More), Content Genre (Entertainment and Drama, Sports, News and Current Affairs, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Television Broadcasting Service Market Trends and Insights

Cord-Cutting Pushes Adoption of OTT and Streaming TV

Streaming's share of total television usage reached 47% in January 2026, a 5.4-point jump in 12 months. Households keep high-speed broadband but cancel multichannel bundles, funneling spending toward a-la-carte apps that bundle on-demand libraries with live linear channels. Comcast lost 10% of domestic linear pay-TV subscribers year-over-year in Q4 2025, yet Peacock added 12% more paid subscribers over the same period. Free ad-supported services accelerate churn from cable because zero subscription cost slashes switching friction; Tubi and The Roku Channel each posted mid-single-digit viewing-share gains by January 2026. Broadcasters therefore prioritize seamless app experiences and robust libraries over carriage negotiations, shifting capital toward direct-to-consumer technology.

Growing Advertiser Demand for Live-Sports Inventory

Sports rights appreciated 113% in value between 2014 and 2024, dwarfing overall advertising growth because brands prize real-time reach and high engagement. Netflix's World Baseball Classic stream in Japan drew 31.4 million viewers, illustrating that even subscription-first platforms will pay premiums for exclusive live events. On FAST services, sports channels enjoyed 105% advertising-revenue growth and 71% higher ad recall than short-form video. Deep-pocketed streamers and national broadcasters thus lock up marquee properties, forcing regional networks to pivot toward niche sports or shoulder programming.

SVOD Platforms Cannibalizing Linear Viewership

Warner Bros Discovery's linear-networks revenue fell 12% year-over-year in Q4 2025 even as streaming subscribers rose to 131.6 million. Linear advertising inventory shrinks alongside audience migration, and per-viewer revenue on SVOD is lower than on scheduled broadcasts. Comcast lost 10% of domestic pay-TV households in Q4 2025, reinforcing a decade-long cord-cutting trend. Broadcasters must therefore fund duplicative infrastructure to run direct-to-consumer apps while still maintaining legacy networks, compressing margins during transition.

Other drivers and restraints analyzed in the detailed report include:

- Broadband and Smart-TV Penetration in Emerging Markets

- Roll-Out of ATSC 3.0 Enabling Interactive Broadcasts

- Escalating Premium-Rights Acquisition Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

OTT and internet TV captured 36.45% of 2025 revenue in the television broadcasting service market and will rise at a 6.57% CAGR to 2031. The surge reflects smart-TV operating systems that foreground streaming apps and mobile networks that zero-rate video traffic. Cable and satellite still anchor rural and maritime distribution, yet subscriber erosion continues as low-earth-orbit broadband promises viable alternatives within three years. Terrestrial broadcast TV benefits from ATSC 3.0 interactivity, but spectrum refarming limits expansion. IPTV's share remains confined to carrier bundles in fiber-rich geographies.

Broadcasters now deploy converged technology stacks so that one asset manifests as a linear channel, an on-demand episode, and a FAST feed with dynamic ad insertion. Paramount unified its Paramount+ and Pluto TV workflows in Q4 2025, cutting per-stream cost by 15%. This model safeguards scale economics while surfing audience preference shifts, ensuring that the television broadcasting service market size for OTT platforms grows without wholly cannibalizing legacy formats.

Advertising-supported offerings controlled 55.78% of 2025 revenue and are projected to expand at a 6.88% CAGR, exceeding subscription growth as households manage budget fatigue. Netflix's ad tier achieved 190 million monthly active users in Q1 2026, materially boosting quarterly revenue of USD 12.25 billion. Roku's USD 1.22 billion Q4 2025 platform revenue validates FAST economics, where higher completion rates and granular targeting lift CPMs.

Subscription services still underpin blockbuster originals but face churn spikes when catalogs stagnate. Hybrid models now dominate: a free, ad-supported on-ramp funnels users toward premium tiers, capturing willingness-to-pay across the income curve. The television broadcasting service market share mix therefore tilts back toward advertising, yet margins improve because programmatic systems automate inventory sales.

Complete Report Scope:

- By Delivery Platform

- Terrestrial Broadcast TV

- Satellite Broadcast TV

- Cable TV

- IPTV

- OTT / Internet TV

- By Service Type

- Subscription-Based Services

- Advertising-Supported Services

- Pay-Per-View / Transactional

- By Broadcaster Type

- Public Service Broadcasters

- Commercial Broadcasters

- Community / Educational Broadcasters

- By Content Genre

- Entertainment and Drama

- Sports

- News and Current Affairs

- Kids and Family

- Other Content Genre

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

Asia-Pacific generated 32.87% of 2025 revenue, buoyed by India's OTT leapfrog and China's state-funded 5G broadcast infrastructure. Zee5's EBITDA-positive milestone at INR 564 million (USD 6.8 million) confirms unit-economics viability for regional-language platforms. South Korea's TVING integration with Wavve boosted advertising 74.7%, and Fuji Television's exclusive Formula 1 rights bet on premium sports loyalty.

Linear platforms in North America and Europe are witnessing a managed decline, which is being offset by the growth of streaming services. By Q1 2026, Peacock achieved a 12% increase in paid subscribers, reaching 46 million, while Comcast's linear base saw a 10% contraction. The FCC's proposed ATSC 1.0 sunset is expediting the transition to IP-centric distribution models. Meanwhile, European quotas and ownership caps are adding complexity to consolidation efforts in the region.

The Middle East is forecast to post the highest 7.98% CAGR, underwritten by sovereign wealth-fund backing of local studios and fiber-to-the-home builds that enable 4K HDR linear channels. South America pivots around Brazil's Globoplay, exceeding 100 million downloads, leveraging Portuguese-language football rights to fend off global entrants. Africa remains nascent because broadband affordability limits mass adoption, but mobile-first models promise catch-up growth in the outer forecast years.

- British Broadcasting Corporation (BBC)

- Comcast Corporation

- Paramount Global

- The Walt Disney Company

- Warner Bros. Discovery, Inc.

- RTL Group S.A.

- Nippon Television Holdings, Inc.

- Fuji Media Holdings, Inc.

- Sky Group Limited

- Mediaset S.p.A.

- Eutelsat Communications S.A.

- Sinclair Broadcast Group, Inc.

- Nexstar Media Group, Inc.

- Seven West Media Limited

- ITV plc

- ProSiebenSat.1 Media SE

- Grupo Globo Comunicacao e Participacoes S.A.

- China Central Television (CCTV)

- Zee Entertainment Enterprises Limited

- CJ ENM Co., Ltd.

- Television Broadcasts Limited (TVB)

- Roku, Inc.

- Amazon.com, Inc. (Freevee)

- Pluto TV LLC

- DAZN Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cord-Cutting Pushes Adoption of OTT and Streaming TV

- 4.2.2 Growing Advertiser Demand for Live-Sports Inventory

- 4.2.3 Broadband and Smart-TV Penetration in Emerging Markets

- 4.2.4 Roll-Out of ATSC 3.0 Enabling Interactive Broadcasts

- 4.2.5 OEM-Backed FAST Channel Ecosystems Gain Traction

- 4.2.6 Cloud-Based Playout Lowers Entry Barriers for Niche Nets

- 4.3 Market Restraints

- 4.3.1 SVOD Platforms Cannibalizing Linear Viewership

- 4.3.2 Local Content and Foreign-Ownership Regulation Caps

- 4.3.3 Escalating Premium-Rights Acquisition Costs

- 4.3.4 Spectrum Refarming for 5G Reduces Terrestrial Capacity

- 4.3.5 Impact of Macroeconomic Factors on the Market

- 4.3.6 Industry Value / Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.7 Threat of New Entrants

- 4.8 Bargaining Power of Suppliers

- 4.9 Bargaining Power of Buyers

- 4.10 Threat of Substitutes

- 4.11 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Delivery Platform

- 5.1.1 Terrestrial Broadcast TV

- 5.1.2 Satellite Broadcast TV

- 5.1.3 Cable TV

- 5.1.4 IPTV

- 5.1.5 OTT / Internet TV

- 5.2 By Service Type

- 5.2.1 Subscription-Based Services

- 5.2.2 Advertising-Supported Services

- 5.2.3 Pay-Per-View / Transactional

- 5.3 By Broadcaster Type

- 5.3.1 Public Service Broadcasters

- 5.3.2 Commercial Broadcasters

- 5.3.3 Community / Educational Broadcasters

- 5.4 By Content Genre

- 5.4.1 Entertainment and Drama

- 5.4.2 Sports

- 5.4.3 News and Current Affairs

- 5.4.4 Kids and Family

- 5.4.5 Other Content Genre

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 British Broadcasting Corporation (BBC)

- 6.4.2 Comcast Corporation

- 6.4.3 Paramount Global

- 6.4.4 The Walt Disney Company

- 6.4.5 Warner Bros. Discovery, Inc.

- 6.4.6 RTL Group S.A.

- 6.4.7 Nippon Television Holdings, Inc.

- 6.4.8 Fuji Media Holdings, Inc.

- 6.4.9 Sky Group Limited

- 6.4.10 Mediaset S.p.A.

- 6.4.11 Eutelsat Communications S.A.

- 6.4.12 Sinclair Broadcast Group, Inc.

- 6.4.13 Nexstar Media Group, Inc.

- 6.4.14 Seven West Media Limited

- 6.4.15 ITV plc

- 6.4.16 ProSiebenSat.1 Media SE

- 6.4.17 Grupo Globo Comunicacao e Participacoes S.A.

- 6.4.18 China Central Television (CCTV)

- 6.4.19 Zee Entertainment Enterprises Limited

- 6.4.20 CJ ENM Co., Ltd.

- 6.4.21 Television Broadcasts Limited (TVB)

- 6.4.22 Roku, Inc.

- 6.4.23 Amazon.com, Inc. (Freevee)

- 6.4.24 Pluto TV LLC

- 6.4.25 DAZN Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment