|

시장보고서

상품코드

2072642

SPC 바닥재 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Stone Plastic Composite Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

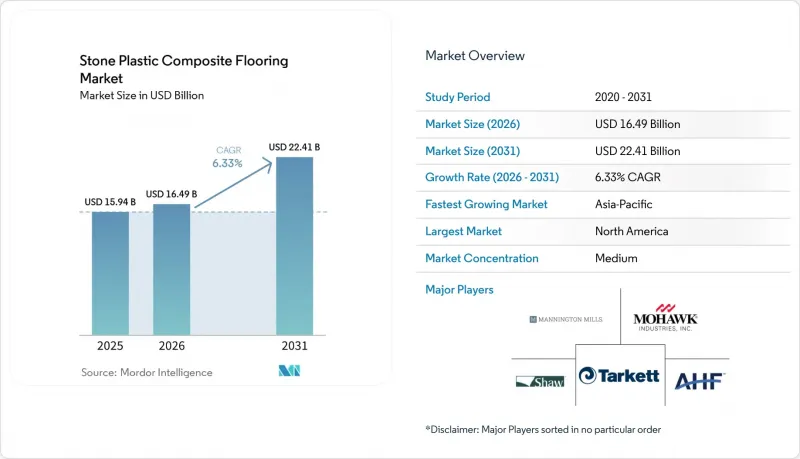

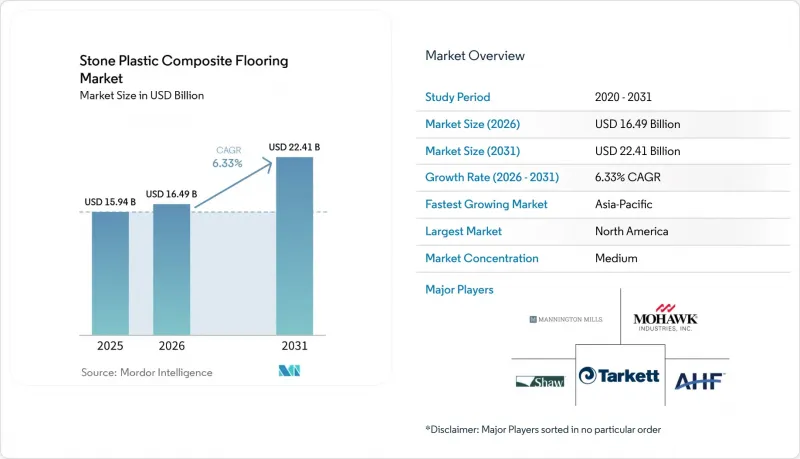

Mordor Intelligence에 의하면, SPC 바닥재 시장 규모는 2025년 159억 4,000만 달러로 평가되었고, 2026년에는 164억 9,000만 달러로 추정되고, 2031년까지 연평균 복합 성장률(CAGR) 6.33%로 성장이 전망되며, 224억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형별(SPC 타일, SPC 플랭크), 제품 두께별(4.0-5.0 mm, 5.1-6.0 mm, 6.1-6.5 mm, 6.5 mm 이상), 시공 방법별(자체 접착식 등), 최종 사용자별(주택, 상업시설), 유통 채널별(B2C 및 소매, B2B 및 시공업체), 지역별(북미, 남미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액 기준으로 제시되어 있습니다.

세계의 SPC 바닥재 시장 동향 및 분석

주택 및 소규모 상업시설에서 라미네이트 및 플렉서블 LVT를 대체하는 방수성 리지드 코어

SPC 바닥재 시장은 주방, 욕실, 지하실 및 소규모 상업시설에서 점유율을 지속적으로 확대되고 있습니다. 이러한 장소에서는 100% 방수 기능을 갖춘 리지드 코어와 내구성이 뛰어난 마모층 덕분에, 다른 소재에서 흔히 발생하는 팽창이나 습기 침투로 인한 결함의 위험이 줄어듭니다. 예를 들어, 기존의 라미네이트 마루는 장기간 물에 노출될 경우 두께가 6-12% 팽창할 가능성이 있지만, SPC 제품은 표준화된 침수 및 안정성 시험(미국재료시험협회(ASTM)의 방법 등)을 통해 유사한 조건에서도 치수 변화가 극히 미미한 것으로 확인되었습니다. 클릭 잠금 구조 덕분에 접착제 경화가 필요 없는 신속한 플로팅 시공이 가능해져, 단계적인 입주나 영업 시간 손실을 최소화해야 하는 소매점의 야간 리모델링에도 대응할 수 있습니다. 클릭 시스템의 시공 생산성은 일반적으로 시공자 1인당 하루 20-40 m² 정도인 반면, 접착제 도포 및 경화가 필요한 접착식 마루 시스템의 경우 하루 10-20 m²에 그칩니다. 이 '신속한 이용 시작'라는 장점 덕분에 SPC 바닥재는 의료시설이나 호텔 및 리조트 등의 복도에서 특히 매력적입니다. 이러한 장소에서는 빡빡한 일정 속에서 공사를 진행하여, 즉시 또는 당일 중으로 보행자 통행이 가능하도록 해야 합니다. 반면, 접착제를 사용하는 탄성 바닥재의 경우, 완전히 사용할 수 있게 되기까지 24-48시간이 소요될 수 있습니다. 상업시설의 인테리어에서 리지드 코어 사양의 SPC 바닥재는 목재나 타일을 사용할 경우 공사 기간이 길어지거나 유지보수 부담이 늘어나는 상황에서 탄성 바닥재의 대안으로 활용되고 있습니다. 예를 들어, 세라믹 타일 시공의 경우, 타일 부설 및 이음매 경화에 2-3일이 소요되는 경우가 많으며, 원목 시공의 경우 현장 상황에 따라 3-7일간의 적응 기간이 필요합니다. 이에 반해, SPC 마루는 치수 안정성이 뛰어나기 때문에 대부분의 경우 적응 기간 없이 시공이 가능합니다.

DIY에 가장 적합한 클릭 잠금 방식과 리모델링 수요의 급증

클릭 잠금 방식 덕분에 필요한 공구가 줄어들고 접착제도 필요 없기 때문에 숙련된 DIY 리모델링 애호가라도 시공이 가능해져 주택 소유주들은 SPC 마루 시장에 매력을 느끼고 있습니다. 또한, 기존의 경질 바닥재 위에서 철거 작업 없이 시공할 수 있으므로 공사 기간이 단축되고, 공사로 인한 생활의 불편도 줄어듭니다. 따라서 리노베이션 과정에서 주말에 한 번만으로도 공간을 새롭게 단장하거나, 즉시 사용할 수 있는 상태로 만들어야 하는 주방이나 욕실의 신속한 개보수 작업에 리지드 코어 제품이 선호되고 있습니다. 이러한 추세는 비전문가도 확실한 시공 결과를 얻을 수 있도록 간소화된 시공 방법, 바탕면의 허용 오차 및 환경 적응에 관한 지침을 강조하는 공급업체의 정보에 힘입어 더욱 가속화되고 있습니다. 상업 분야에서도 이와 같은 부담 경감의 혜택을 누리고 있으며, 소규모 사무실, 진료소, 부티크 소매점 등의 인테리어 공사 기간을 단축하는 동시에, 공사 완료 후 더 빨리 영업을 재개할 수 있게 되었습니다.

폴리염화비닐(PVC)의 지속가능성에 대한 면밀한 검토와 순환 경제 및 재활용의 장애물

지속가능성에 대한 엄격한 시선은 SPC 바닥재 시장에 여전히 뿌리 깊은 역풍으로 작용하고 있습니다. 특히 유럽에서는 순환형 경제 목표와 공공 조달 기준이 자재 선정에 영향을 미치고 있습니다. Plastics Recyclers Europe(PRE)는 수십 년에 걸친 노력에도 불구하고, 유럽 내 인증된 사용 후 PVC의 재활용량이 여전히 총 폐기물 발생량보다 훨씬 낮은 수준에 머물고 있다고 결론지었으며, 이는 순환 경제에 대한 의지와 실제 성과 사이에 격차가 있음을 여실히 보여주고 있습니다. 『VinylPlus 진행 보고서(2024-2025년)』에서 지적된 바와 같이, PVC 재활용량은 해마다 변동하고 있습니다. 구체적으로 말하면, 총 재활용량은 2023년의 73만 7,000톤을 상회하던 수준에서 2024년에는 약 72만 4,000톤으로 감소했으며, 이는 시장과 그 구조가 직면한 과제를 여실히 드러내고 있습니다. 이러한 현실을 감안하여, 각 제조업체는 EPD를 통해 수명 주기에 미치는 영향을 문서화하고, 특정 탄성 바닥재 제품 라인에 대해 재활용 이니셔티브를 제공합니다. 이러한 노력은 투명성을 높이고, 검증 가능한 데이터를 중시하는 그린빌딩 프로그램 참여를 용이하게 합니다. 이러한 조치는 점차 확대되고 있지만, 재생 소재나 바이오 유래 소재의 현재 사용량은 신재의 총 처리량에 비해 여전히 적기 때문에 지속가능성을 가장 중시하는 프로젝트라 하더라도 사양을 결정할 때는 PVC 함유량을 신중하게 검토할 필요가 있습니다. 유럽의 업계 진행 보고서 및 새로운 EPD는 환경 성과를 보다 정확하게 평가하고, 인프라가 잘 갖춰진 지역에서 사용 후 제품 처리를 계획하고자 하는 프로젝트 팀에게 신뢰할 수 있는 기준을 제공합니다. 경질 코어 바닥재에 대한 카테고리별 EPD의 공표는 사양 결정자가 제품 수준의 환경 영향 및 문서화 요건을 비교 검토하는 데 더욱 도움이 됩니다. 대상 프로젝트에 대해 탄성 바닥재 회수 프로그램을 제공하는 기업의 노력은 이미 설치된 제품의 매립 처분을 줄이기 위한 실질적인 방안 중 하나를 제시하고 있습니다.

부문별 분석

SPC 플랑크는 2025년 시장 규모의 84.00%를 차지했으며, 나뭇결 무늬의 주택용 바닥재로 여전히 표준적인 형태를 유지하고 있습니다. 또한, SPC 바닥재 시장에서 석재, 테라조, 콘크리트 느낌의 디자인이 상업 공간에 널리 보급됨에 따라, 이 부문은 2031년까지 연평균 성장률(CAGR) 8.03%로 확대될 것으로 전망됩니다. SPC 바닥재 시장에서 플랭크 형태의 점유율은 천연 목재의 미관과 방수 성능을 겸비한 제품, 그리고 시공으로 인한 생활에 미치는 영향을 줄여주는 플로팅 시공 방식에 대한 주택 소유자들의 지속적인 선호도를 반영하고 있습니다. 타일은 세라믹이나 포셀린과 같은 무게, 경화 시간, 이음매 관리가 필요 없으면서도 대형 석재와 같은 외관을 추구하는 디자이너들 사이에서 인기가 높아지고 있습니다. 상업시설에서는 리지드 코어 타일이 사실적인 외관을 구현하고 신속한 영업 재개를 가능하게 하여, 로비나 복도의 야간 보수 공사를 지원하고 있습니다.

상업 프로젝트에 국한되지 않고, 외관과 표면 마감 품질은 지속적으로 향상되고 있으며, 천연 소재와의 미적 측면에서의 절충이 줄어들고 있습니다. 폭이 넓고 길이가 긴 플랭크 제품군은 짧은 길이의 제품으로는 지금까지 구현하기 어려웠던, 방 전체에 걸쳐 실감 나는 질감을 선사합니다. 타일의 경우, 다양한 패턴 옵션을 통해 호텔,리조트 업계 및 의료시설에서 존재감 있는 바닥 마감 효과를 구현하면서도, 탄성 바닥재 특유의 관리 용이성을 유지하고 있습니다. SPC 바닥재 시장은 단계별 시공을 가능하게 하고, 접착제 사용량을 줄이며, 더 깨끗한 현장 환경을 실현하는 안정적인 시공 방식의 이점을 누리고 있습니다. 제조업체가 발행하는 업계 간행물에서는 가동 시간이 일정의 제약 요인이 되는 상황에서 리지드 코어 제품이 노동 집약적인 바닥재를 대체할 수 있다는 점이 강조되고 있습니다.

2025년에는 4.0-5.0 mm 두께 대가 SPC 바닥재 시장의 43.67%를 차지했으나, 고급 주택이나 공동 주택에서 프로젝트 팀이 더 높은 방음 성능과 발밑의 쿠션감을 추구하는 경향에 따라, 5.1-6.0 mm 제품은 2031년까지 연평균 성장률(CAGR) 9.23%를 나타낼 것으로 예측됩니다. 기층재가 일체화된 두꺼운 구조는 여러 층을 조립할 필요 없이 IIC 및 STC와 관련된 건축 기준의 최소 요건을 충족하는 데 도움이 되며, 불확실성을 줄이고 서류 작성 절차를 간소화합니다. 더 강력한 충격음 제어를 추구하는 개발자에게 있어, 두께가 있는 단일 SKU 조립 제품은 현장 상황과 실험실에서 테스트된 패키지의 불일치 위험을 줄여줍니다. 이러한 선택지들은 바탕면의 미세한 요철로 인한 '텔레그래핑' 또한 이를 완화하여, 단단한 바탕에서 발생하는 공극이나 단차로 인한 재시공 요청을 줄입니다. EPD(환경 제품 선언)에서는 현재 지구 온난화 계수(kg CO2-eq/m2), 에너지 소비량(MJ/m²), 그리고 다양한 SPC 구조물의 폐기 시나리오와 같은 정량화된 수명 주기 지표가 제공되고 있어, 사양 수립자는 두께나 바탕재의 변경이 프로젝트의 전체 선택지 내에서 환경 성능에 어떤 영향을 미치는지 비교할 수 있게 되었습니다.

두께에는 실용적인 상한선이 있으며, 이를 초과하면 자재비가 높아지고 인접한 방과의 경계 처리도 어려워집니다. 그러나 일반적인 범위 내에서는 음향 성능, 쾌적성, 시공 용이성 간의 균형을 고려하여, 프리미엄 사양이 공동주택이나 고급 주택의 사양으로 계속해서 채택되고 있습니다. 프리미엄급 SPC 바닥재 시장 규모는 건축 기준 준수를 간소화하고 거주자의 쾌적성을 확보하는 것을 주요 구매 요인으로 삼는 프로젝트들에 힘입어 성장하고 있습니다. 또한, 공급업체들이 음향에 관한 정의와 현장 지침을 표준화함에 따라, 기초 자재에 대한 지식도 향상되고 있습니다. 미국에서는 방음을 위한 세대 간 최소 분리 요건이 공동주택의 맥락에서 이러한 선택지 중 상당 부분을 결정짓고 있습니다. 기층재 공급업체가 진행하는 교육 활동은 목표 성능인 IIC, STC 및 Delta IIC를 달성하기 위한 구성 선정 과정에서 팀을 지속적으로 지원하고 있습니다.

지역별 분석

2025년, 북미는 전 세계 SPC 시장 가치의 35.88%를 차지했습니다. 북미의 프로젝트에서는 신속한 리모델링 주기와 건축기준법에 따른 방음 기준을 이유로, 신속한 플로팅 시공과 하부재에 의한 음향 제어를 결합한 리지드 코어 구조를 지정하는 사례가 증가하고 있습니다. 국내 탄성 바닥재 생산 능력의 확대로 인해 제품의 입수성이 향상되고, 긴 납기나 변동하는 추가 요금의 영향이 완화될 것으로 예측됩니다. 사양을 중시하는 상업 프로젝트의 경우, 미국 건축 기준법이 세대 간 칸막이의 IIC 및 STC에 대한 바닥·천장 성능의 최저 기준을 규정하고 있습니다. 이 기준은 적절한 바탕재와 결합된 두꺼운 SPC 구조 덕분에 종종 초과되고 있습니다. 이러한 고려 사항들로 인해 SPC 바닥재 시장은 임대 주택의 리모델링은 물론, 각 세대 간 일관된 주거 경험을 추구하는 신규 다세대 주택 개발 분야에서 계속해서 중요한 역할을 수행하고 있습니다. 탄성 바닥재 생산 확대와 관련하여 각사가 발표한 바에 따르면, 국내 신규 생산 라인이 풀가동에 접어들면서 리드타임과 제품 라인업의 폭이 개선될 것이라고 강조되고 있습니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 9.77%를 기록하며 가장 빠른 성장세를 보일 것으로 전망됩니다. 이는 SPC 바닥재 시장에서 생산 업체의 규모 확대와, 리모델링 주기에서 방수성과 탄력성을 갖춘 바닥재를 채택하는 도시 지역의 주택 재고 증가를 모두 반영한 것입니다. 유럽에서는 성숙한 시장에서 음향적 쾌적성, 환경 정보 공개 및 상세한 문서화를 우선시하는 공공 조달 기준이 중시되고 있어, 성장이 꾸준한 속도로 이어지고 있습니다. 2025년 유럽의 무역 조치는 하류 가공업체의 수지 경제성을 재편했으며, 이를 통해 원자재의 다양화와 최종 수요에 가까운 공정 및 생산 라인에 대한 투자가 촉진되었습니다. 이러한 상황으로 인해 유럽 내 SPC 바닥재 시장의 신뢰할 수 있는 공급처의 폭이 넓어졌으며, 검증된 데이터와 규격에 부합하는 시공에 주력하는 프로젝트 팀이 힘을 얻게 되었습니다.

영국 및 EU에서는 2025년에 시행된 반덤핑 조치로 인해 일부 수지 가격 구조가 변화하면서, 가공업체의 조달 계획에 영향을 미쳤습니다. 이러한 변화는 탄성 바닥재에 관한 투명한 환경 제품 데이터와 실내 공기질에 관한 문서화에 대한 지속적인 중시와 함께 이루어졌습니다. SPC에 맞추어 조정된 업계 단체가 발행한 EPD(환경 제품 선언)는 제품 유형 간 수명 주기 보고서를 비교하는 팀에게 직접적인 참고 자료가 되며, 일관된 선정 체계를 뒷받침합니다. 민간 및 공공 부문의 친환경 건축 기준이 보급됨에 따라, 조달 과정에서 문서화 및 재활용, 회수 옵션의 중요성이 커지고 있으며, 검증된 데이터와 회수 프로그램을 제공할 수 있는 기업이 유리한 입장에 있습니다. 이러한 요인들은 유럽의 SPC 바닥재 시장을 뒷받침하는 동시에, 정책 및 문서화 동향에 부합하는 형태와 공급업체로 시장을 이끌고 있습니다. 이러한 복합적인 효과로 인해, 성능과 정보 공개라는 두 가지 기준을 모두 충족하는 제품에 대한 수요가 꾸준히 증가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the stone plastic composite flooring market size stood at USD 16.49 billion in 2026, up from USD 15.94 billion in 2025, and is projected to reach USD 22.41 billion by 2031 at a 6.33% CAGR.

This report is Segmented by Product Type (SPC Tiles, SPC Planks), Product Thickness (4. 0-5. 0 Mm, 5. 1-6. 0 Mm, 6. 1-6. 5 Mm, Above 6. 5 Mm), Installation Method (Self-Adhesive, and More), End User (Residential, Commercial), Distribution Channel (B2C/Retail, B2B/Contractors), and Geography (North America, South America, Europe, and More). Market Forecasts are Provided in Terms of Value.

Global Stone Plastic Composite Flooring Market Trends and Insights

Waterproof Rigid-Core Replacing Laminate and Flexible LVT in Home and Light Commercial

The SPC flooring market continues to gain share in kitchens, bathrooms, basements, and light-commercial areas where 100% waterproof rigid cores and durable wear layers reduce failure risk associated with swelling or moisture ingress in other materials. Traditional laminate flooring, for example, can swell by 6-12% in thickness after prolonged water exposure, whereas SPC products typically show negligible dimensional change under similar conditions, as determined by standardized water-immersion and stability tests (e.g., American Society for Testing and Materials methods). Click-lock construction enables fast floating installations that require no adhesive cure, supporting phased occupancies and overnight retail refits that minimize lost trading hours. Installation productivity for click systems typically ranges from 20-40 m2 per installer per day, compared with 10-20 m2 for glued flooring systems due to adhesive application and curing requirements. This speed-to-service benefit makes SPC flooring compelling in healthcare and hospitality corridors where installations must proceed under tight schedules and enable immediate or same-day walk-on use, unlike adhesive-based resilient flooring, which may require 24-48 hours before full service. In commercial interiors, rigid-core options serve as resilient alternatives where wood or tile would extend timelines or increase maintenance demand. Ceramic tile installations, for instance, often require 2-3 days for setting and grout curing, while hardwood installations involve acclimation periods of 3-7 days depending on site conditions. By contrast, SPC flooring can be installed without acclimation in many cases due to its dimensional stability.

DIY-Friendly Click-Lock and Renovation-Led Demand Spike

Homeowners are drawn to the SPC flooring market because click-lock systems reduce tool requirements and eliminate the need for adhesives, bringing installation within reach for proficient DIY renovators. The ability to install over many existing hard surfaces without demolition also shortens project duration and reduces overall project disruption. Renovation cycles have therefore favored rigid-core products for single-weekend room refreshes and fast kitchen or bath upgrades that must be ready for immediate use. This pattern is reinforced by supplier content that emphasizes simplified installs, subfloor tolerances, and acclimation guidance that help non-professionals achieve reliable outcomes. The commercial side benefits from the same friction reduction, which compresses fit-out schedules for small offices, clinics, and boutique retail while keeping spaces open for business sooner after install.

Polyvinyl Chloride (PVC) Sustainability Scrutiny and Circularity/Recycling Barriers

Sustainability scrutiny remains a persistent headwind for the SPC flooring market, especially in Europe, where circular-economy targets and public procurement standards shape material selection. Plastics Recyclers Europe (PRE) has concluded that, despite decades of initiatives, certified post-consumer PVC recycling volumes in Europe remain well below overall waste generation, which underscores the gap between circular ambition and realized outcomes. As highlighted in the VinylPlus Progress Report (2024-2025), PVC recycling volumes have fluctuated year on year. Specifically, the total recycled volumes dipped from exceeding 737,000 tons in 2023 to approximately 724,000 tons in 2024, underscoring the challenges faced in the market and its structure. These realities have pushed manufacturers to document lifecycle impacts through EPDs and to offer reclamation initiatives for certain resilient lines. These steps improve transparency and ease participation in green building programs that value verifiable data. While such measures are expanding, current volumes of reclaimed or bio-attributed materials are small compared to total virgin throughput, which means specification decisions in the most sustainability-sensitive projects still weigh PVC content carefully. European industry progress reports and new EPDs provide credible baselines for project teams that want to evaluate environmental performance more precisely and to plan end-of-life handling where infrastructure exists. Published category EPDs for rigid-core floors further help specifiers benchmark product-level impacts and documentation requirements. Company programs that offer resilient reclamation for qualifying projects demonstrate one practical route to reduce landfill disposal of installed products.

Other drivers and restraints analyzed in the detailed report include:

- Price-to-Performance vs Wood/Tile Expands Addressable Market

- Growth of Multi-Family and Rental Refresh Cycles

- Feedstock Price Volatility (PVC Resin, Additives)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SPC planks held 84.00% of the 2025 market size and remain the default format for wood-look residential installations, and the segment is projected to expand at an 8.03% CAGR through 2031 as stone, terrazzo, and concrete visuals gain reach in commercial spaces within the SPC flooring market. The SPC flooring market share of plank formats reflects sustained homeowner preference for natural wood aesthetics paired with waterproof performance, and for floating installations that reduce disruption. Tiles are gaining popularity among designers who want large-format stone looks without the weight, cure time, or grout maintenance of ceramic or porcelain. In commercial settings, rigid-core tiles support overnight lobby and corridor upgrades with realistic visuals and immediate return to service.

Across residential and commercial projects, visuals and surface finishes continue to improve, reducing aesthetic trade-offs with natural materials. Wider and longer plank assortments deliver room-scale realism that was previously difficult to achieve with shorter lengths. For tiles, patterning options allow statement floors in hospitality and healthcare while maintaining the maintenance profile that resilient platforms are known for. The SPC flooring market benefits from a stable installation method that supports phased work, reduces adhesive use, and results in cleaner job sites. Commercial publications from manufacturers reinforce how rigid-core products can replace more labor-intensive surfaces where uptime is a scheduling constraint.

The 4.0-5.0 mm tier accounted for 43.67% of the SPC flooring market in 2025, yet 5.1-6.0 mm products are forecast to grow at a 9.23% CAGR through 2031, as project teams pursue higher acoustic ratings and a more cushioned feel underfoot in premium residential and multi-family settings. Thicker constructions with integrated underlayment help projects meet minimum code thresholds for IIC and STC without assembling multiple layers, reducing variables and simplifying documentation. For developers seeking stronger impact sound control, thicker single-SKU assemblies reduce the risk of mismatches between field conditions and lab-tested packages. These choices also reduce telegraphing from minor subfloor unevenness, which limits callbacks for hollow spots or lippage on harder substrates. EPDs now provide quantified lifecycle metrics, such as global warming potential (kg CO2-eq/m2), energy use (MJ/m2), and end-of-life scenarios for different SPC constructions, enabling specifiers to compare how changes in thickness and underlayment affect environmental performance across project options.

There is a practical upper bound on thickness beyond which material cost and transitions to adjacent rooms become less forgiving. Within common ranges, however, the balance of acoustics, comfort, and ease of install continues to push premium formats into multi-family and higher-end residential specifications. The SPC flooring market size for premium assemblies is supported by projects where simplified code compliance and occupant comfort are procurement drivers. Underlayment knowledge has also improved as suppliers standardize acoustic definitions and field guidance. In the United States, minimum dwelling separation requirements for sound control anchor many of these choices in multi-family contexts. Education from underlayment providers continues to help teams select assemblies to reach target IIC, STC, and Delta IIC outcomes.

Complete Report Scope:

- By Product Type

- SPC Tiles

- SPC Planks

- By Product Thickness

- 4.0-5.0 mm

- 5.1-6.0 mm

- 6.1-6.5 mm

- Above 6.5 mm

- By Installation Method

- Self-Adhesive

- Glue-Down

- Interlocking/Click-lock

- Others

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Flooring Stores

- Online

- Other Distribution Channels

- B2B/Contractors

- B2C/Retail

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Geography Analysis

North America accounted for 35.88% of the global SPC market value in 2025. North American projects increasingly cite rapid renovation cycles and code-bound soundproofing thresholds as reasons to specify rigid-core assemblies that combine fast floating installation with underlayment-based acoustic control. Expanded domestic resilient capacity is expected to improve availability and reduce exposure to long shipping windows and variable surcharges. For spec-driven commercial projects, U.S. codes set floor-ceiling performance minimums for IIC and STC in dwelling separations. This baseline is often exceeded by thicker SPC assemblies with matched underlays. Those considerations keep the SPC flooring market relevant in rental refreshes and in new multi-family developments aiming for consistent resident experiences across stacked units. Company disclosures on resilient manufacturing expansion underline that lead times and product breadth will improve as new domestic lines reach full production.

Asia-Pacific is projected to record the fastest growth at a 9.77% CAGR from 2026 to 2031, reflecting both producer scale and urban housing stock adopting waterproof, resilient surfaces during renovation cycles in the SPC flooring market. European growth continues at a measured pace as mature markets weigh acoustic comfort, environmental disclosures, and public procurement criteria that prioritize detailed documentation. Trade actions in Europe have reshaped resin economics for downstream converters in 2025, which encouraged material diversification and investment in processes and lines closer to end demand. These conditions have expanded the SPC flooring market's range of reliable sources in Europe and supported project teams focused on validated data and compliant assemblies.

In the United Kingdom and the EU, anti-dumping measures implemented in 2025 altered some resin price relationships and affected converters' sourcing plans. These changes arrived alongside continued emphasis on transparent environmental product data and indoor-air quality documentation for resilient floors. Association-issued EPDs tailored to SPC provide a direct reference for teams comparing lifecycle reporting across product types, which supports consistent selection frameworks. As public and private green-building criteria spread, documentation and reclamation options become more relevant to procurement, and companies that can offer validated data and take-back programs are well-positioned. These factors sustain the SPC flooring market in Europe while steering it toward formats and suppliers that align with policy and documentation trends. The combined effect is steady demand with a tilt toward offerings that meet both performance and disclosure thresholds.

- Mohawk Industries

- Shaw Industries (incl. COREtec)

- Tarkett

- Mannington Mills

- CFL Flooring

- Novalis Innovative Flooring

- Beaulieu International Group (BerryAlloc)

- LX Hausys

- Huali Industrial Group

- DECNO Group

- NOX Corporation

- Forbo Flooring Systems

- Gerflor

- AHF Product

- HMTX Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Waterproof rigid-core replacing laminate and flexible LVT in home and light commercial

- 4.2.2 DIY-friendly click-lock and renovation-led demand spike

- 4.2.3 Price-to-performance vs wood/tile expands addressable market

- 4.2.4 Growth of multi-family and rental refresh cycles

- 4.2.5 Tariff-driven supply shifts (China->Vietnam/Korea/Turkey) expand localized availability/spec acceptance

- 4.2.6 Fast-turn commercial fit-outs valuing minimal downtime installation

- 4.3 Market Restraints

- 4.3.1 PVC sustainability scrutiny and circularity/recycling barriers

- 4.3.2 Feedstock price volatility (PVC resin, additives)

- 4.3.3 Acoustics and scratch resistance trade-offs vs WPC/laminate

- 4.3.4 Tariff/trade actions and non-tariff barriers raise landed costs and complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 SPC Tiles

- 5.1.2 SPC Planks

- 5.2 By Product Thickness

- 5.2.1 4.0-5.0 mm

- 5.2.2 5.1-6.0 mm

- 5.2.3 6.1-6.5 mm

- 5.2.4 Above 6.5 mm

- 5.3 By Installation Method

- 5.3.1 Self-Adhesive

- 5.3.2 Glue-Down

- 5.3.3 Interlocking/Click-lock

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C/Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B/Contractors

- 5.5.1 B2C/Retail

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South-East Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mohawk Industries

- 6.4.2 Shaw Industries (incl. COREtec)

- 6.4.3 Tarkett

- 6.4.4 Mannington Mills

- 6.4.5 CFL Flooring

- 6.4.6 Novalis Innovative Flooring

- 6.4.7 Beaulieu International Group (BerryAlloc)

- 6.4.8 LX Hausys

- 6.4.9 Huali Industrial Group

- 6.4.10 DECNO Group

- 6.4.11 NOX Corporation

- 6.4.12 Forbo Flooring Systems

- 6.4.13 Gerflor

- 6.4.14 AHF Product

- 6.4.15 HMTX Industries

7 Market Opportunities & Future Outlook

- 7.1 Healthcare & clinic retrofits: hygienic, quick-install SPC with enhanced stain/chemical resistance

- 7.2 Acoustic code-compliant SPC with pre-attached underlayment for multi-family/high-rise specifications