|

시장보고서

상품코드

2072643

북미의 SPC 바닥재 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Stone Plastic Composite Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

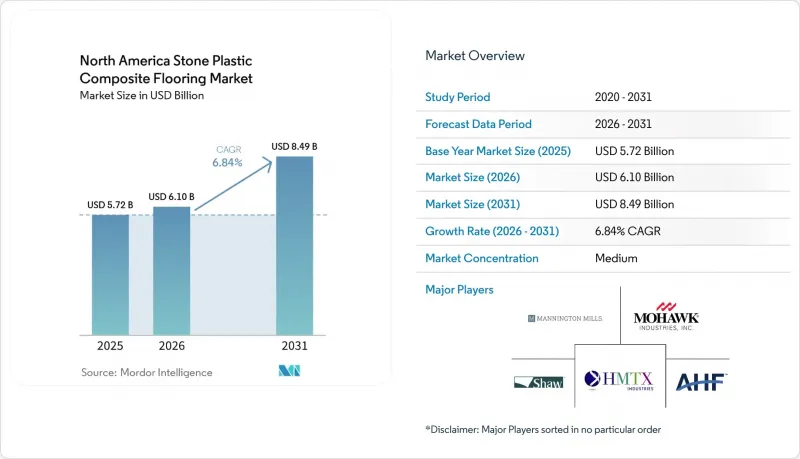

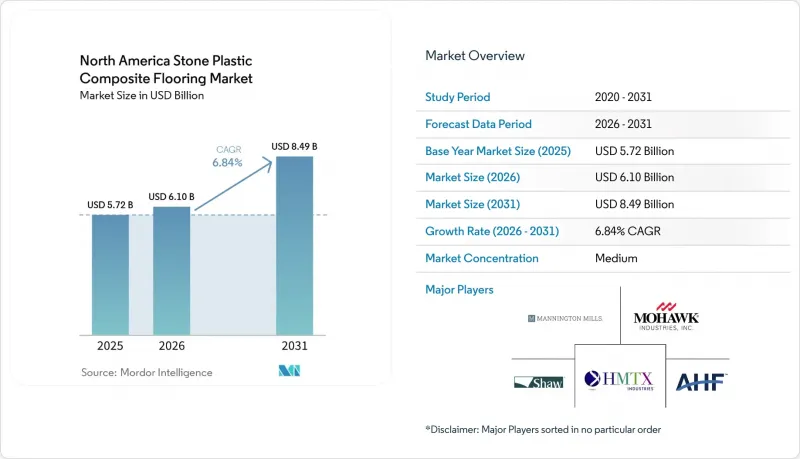

Mordor Intelligence에 의하면, 북미의 SPC 바닥재 시장 규모는 2025년 57억 2,000만 달러로 평가되었고, 2026년에는 61억 달러로 추정되고, 2031년까지 연평균 복합 성장률(CAGR) 6.84%로 전망되며, 84억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형별(SPC 타일, SPC 플랭크), 제품 두께별(4.0-5.0 mm, 5.1-6.0 mm, 6.1-6.5 mm 이상), 시공 방법별(자체 접착식, 기타), 최종 사용자별(주거용, 상업용), 유통 채널별(B2C/소매, B2B/시공업체/건설업체), 지역별(미국, 캐나다, 멕시코)로 분류되어 있습니다. 예측치는 금액(달러)으로 표시되어 있습니다.

북미의 SPC 바닥재 시장 동향 및 인사이트

방수성 리지드 코어에 대한 리모델링 및 DIY 수요

SPC는 습기나 온도 변화가 있는 실내 공간에서 발생하는 실질적인 문제를 해결합니다. 그 이유는 돌이나 플라스틱으로 만들어진 코어가 목재 제품처럼 습기에 노출되어도 팽창하지 않기 때문입니다. 주택 소유자들은 접착제를 사용하지 않고 시공 기간을 단축하며, 접착 시공에 비해 인건비를 절감할 수 있는 클릭락 방식의 플로팅 시공을 높이 평가하고 있으며, 이에 따라 북미 SPC 바닥재 시장은 리모델링 예산에서 더 큰 점유율을 차지하고 있습니다. SPC의 채택은 리모델링 행태와 자재 성능에 대한 수요의 뚜렷한 변화에 힘입어 이루어지고 있습니다. 전미부동산협회(NAR)에 따르면, 기존 주택은 연간 주택 거래의 약 85-90%를 차지하며, 대규모 리모델링 수요의 기반을 뒷받침하고 있습니다. 홈 임프루브먼트 리서치 인스티튜트(Home Improvement Research Institute)의 조사에 따르면, 주택 소유자의 60% 이상이 1년에 적어도 한 번은 DIY 프로젝트를 진행하고 있으며, 바닥재 교체는 가장 일반적인 리모델링 항목 중 하나입니다. 또한, SPC는 약 -20°C에서 60°C의 온도 범위에서 구조적 안정성을 유지하므로, 햇볕이 잘 드는 곳이나 냉난방 시설이 미흡한 공간에서 발생하는 팽창으로 인한 틈을 최소화합니다. 이러한 성능 특성 덕분에 유지보수 빈도가 줄어들고 수명 주기 비용이 절감되므로, 임대 주택 소유주나 자가 거주자들의 재구매가 촉진되고 있습니다.

성능과 가격 측면에서 유연성이 뛰어난 LVT/WPC에서 SPC로의 전환

SPC는 코어 밀도가 높고 압축 내구성이 뛰어나기 때문에 더 부드러운 WPC나 플렉서블 LVT에 비해 구름 하중이나 가구 다리에 의한 충격에 대한 내성이 향상되어, 합리적인 가격대로 유동 인구가 많은 지역에서 폭넓게 사용할 수 있습니다. 사람들이 많이 오가는 복도나 거실 공간에서 카펫이나 플렉서블 LVT를 SPC로 교체한 부동산 소유주들은 팽창 및 수축 문제가 줄어들었습니다고 보고하고 있으며, 이로 인해 교체나 수리를 위한 재방문 횟수가 감소하고 있습니다. 북미의 SPC 바닥재 시장에서는 일상적인 사용 시 내구성, 내스크래치성, 내수성 측면에서 리지드 코어 방식이 가성비가 더 뛰어나다는 인식이 긍정적인 요인으로 작용하고 있습니다. SPC로의 전환은 플렉서블 LVT나 WPC와 비교했을 때 기계적 성능이 정량적으로 향상된 점이 주된 원동력이 되고 있습니다. ASTM International에 따르면, SPC의 리지드 코어 밀도는 일반적으로 1,900-2,100 kg/m³를 초과하는 반면, WPC의 경우 800-1,200 kg/m³에 불과하여, 그 결과 SPC는 압흔 및 구름 하중에 대한 내성이 훨씬 더 높습니다.

관세, UFLPA에 따른 심사, 그리고 PVC 원료 가격 변동

수입업체들은 집행 과정에서 신뢰성이 더 높은 증거와 종단 간 추적 가능성이 요구됨에 따라, 투명한 공급망을 입증하기 위해 조달처 및 서류를 정비하고 있습니다. 미국 세관·국경보호청(CBP)에 따르면, '위구르인 강제노동방지법(UFLPA)'에 따른 집행으로 인해, 시행 첫 해에만 3,500건 이상의 화물이 압류되었으며, 그 가치는 9억 달러 이상에 달했습니다. 이로 인해 규정 준수 비용과 통관 시간이 증가하고 있습니다. 구매 담당자는 관세 리스크를 포함한 총 입고 비용 시나리오를 검토하고 있습니다. 중국산 비닐 바닥재 제품에 대한 제301조 관세는 여전히 최대 25%로 설정되어 있으며, 수입이 중단될 경우 항구에서의 체류 기간이 2-4주 연장되고, 컨테이너 1개당 하루 100-300달러의 보관료 및 선박 체류료가 추가로 부과될 가능성이 있습니다. PVC 수지는 여전히 SPC 원가의 상당 부분을 차지하고 있으며, 소매 가격이 엄격하게 관리되는 상황에서 수지 가격의 변동은 이익률에 부담을 주는 요인이 됩니다. 일부 브랜드는 관세 체계의 균형을 맞추고 감사를 효율화하기 위해 생산 거점을 동남아시아와 북미에 분산시키고 있으며, 이로 인해 미국 및 캐나다로의 출하량 배분이 변화하고 있습니다. 이러한 상반된 요인들로 인해 계획 수립이 더욱 복잡해지고 있으며, 북미 SPC 바닥재 시장의 단기적인 성장이 억제되고 있습니다.

부문별 분석

2025년에는 SPC 플랑크가 72.10%의 시장 점유율을 차지한 것으로 평가되었으며, 북미의 SPC 바닥재 시장에서 디자인을 중시하는 프로젝트가 확대됨에 따라 SPC 타일은 2031년까지 연평균 성장률(CAGR) 7.10%를 나타낼 것으로 전망됩니다. 플랑크는 사실적인 나뭇결 무늬의 외관, 엠보싱 처리된 질감, 그리고 주택 사용자의 취향과 DIY 시공 흐름에 부합하는 친숙한 방 배치와 같은 장점을 가지고 있습니다. 타일 형식은 기하학적 레이아웃이나 대형 모듈을 통해 피팅를 줄여 유지보수 작업을 신속하게 진행할 수 있기 때문에 호텔·리조트 업계나 복합 용도 공간에서의 적용 사례가 확대되고 있습니다. 시공 업체 측에서는 대형 타일에 대해 '클릭 잠금 장치의 안정적인 성능'이라고 '평탄성'이 필수적이라는 지적이 나오고 있으며, 이로 인해 유동 인구가 많은 장소에서 인증된 시스템의 도입이 촉진되고 있습니다. 이러한 미관과 실용성의 균형 덕분에, 두 형태 모두 북미 SPC 바닥재 시장의 꾸준한 성장에 기여하고 있습니다.

SPC 타일은 플랭크 제품만으로는 쉽게 구현할 수 없는 시각적인 스토리성을 가능하게 함으로써, 라미네이트나 플렉서블 비닐과의 차별화를 꾀할 수 있습니다. 제품 개발팀은 공공 장소용 타일 SKU에 미끄럼 방지 처리와 두꺼운 마모층을 추가하여, 이를 통해 매일 청소하거나 바퀴가 지나다녀도 외관을 유지하기 쉬워졌습니다. 홈센터와 전문점이 플래노그램을 조정하고 더 다양한 액센트 타일 옵션을 도입함에 따라, 타일은 북미 SPC 바닥재 시장에서 주력 제품인 플랭크의 판매량을 압박하지 않으면서 점차 시장 점유율을 확대해 나갈 것으로 기대됩니다. 또한, 시각화 도구는 일반 구매자가 집에서 타일의 외관을 평가하는 데 도움이 되며, 다양한 패턴이 있는 공간에서 구매 결정을 내리는 데 따르는 부담을 줄여줍니다.

2025년에는 5.1-6.0 mm급 제품이 북미 SPC 바닥재 시장 점유율의 34.80%를 차지한 것으로 평가된 반면, 두께 6.5 mm를 초과하는 플랭크는 2031년까지 연평균 성장률(CAGR) 7.45%를 나타낼 것으로 전망됩니다. 중간 두께 유형의 구조는 리지드 코어의 안정성과 경쟁력 있는 비용 간의 균형을 잘 맞추고 있어, 대부분의 주거용 공간과 많은 경량 상업용 공간에 적합합니다. 두께가 두꺼운 제품에는 충격음을 줄이는 데 도움이 되는 패드가 일체형으로 장착되어 있어, 적절한 바탕재와 함께 사용하면 다양한 시공 방식에서 건축 기준의 목표를 충족하는 데 도움이 됩니다. 시공 업체는 모든 두께에서 장기적인 성능을 유지하기 위한 핵심 요소로 모서리의 강도와 프로파일의 정밀도를 강조하고 있으며, 이러한 주장은 ASSURE 규격에서 채택된 파단 저항 시험을 통해 입증되었습니다. 이러한 특성들은 북미 SPC 바닥재 시장의 모든 프로젝트에서 목적에 맞는 제품을 선정하는 데 지침이 되고 있습니다.

얇은 엔트리 레벨 제품은 간편하게 외관을 리프레시하는 데 적합하지만, 바탕면의 평탄도나 무거운 점하중의 영향을 받기 쉬우므로, 유동 인구가 많은 공간에서는 위험이 커집니다. 두께가 6.5 mm를 초과하는 프리미엄 제품은 호텔 및 리조트 등의 복도나 지상층 아파트에 적합합니다. 이러한 용도에서는 방음성과 찌그러짐 저항성이 더욱 중요하게 여겨지기 때문입니다. 특정 두께 범위를 표준화하는 시공업체는 교육의 복잡성을 줄이고, 출입구에서프로파일 전환과 관련된 문제를 최소화할 수 있으며, 이를 통해 북미 SPC 바닥재 업계의 시공 성과가 향상됩니다. 구매자들은 총 시공 비용과 건축 기준 준수 여부를 고려하기 때문에 중가대 SKU가 북미 SPC 바닥재 시장에서 계속해서 중심적인 위치를 차지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the north america stone plastic composite flooring market size stood at USD 6.10 billion in 2026, up from USD 5.72 billion in 2025, and is projected to reach USD 8.49 billion by 2031 at a 6.84% CAGR.

This report is Segmented by Product Type (SPC Tiles, SPC Planks), Product Thickness (4. 0-5. 0 Mm, 5. 1-6. 0 Mm, 6. 1-6. 5 Mm, and More), Installation Method (Self-Adhesive, and More), End User (Residential, Commercial), Distribution Channel (B2C/Retail, and B2B/Contractors/Builders), and Geography (United States, Canada, Mexico). Forecasts are Provided in Terms of Value (USD).

North America Stone Plastic Composite Flooring Market Trends and Insights

Renovation and DIY Preference for Waterproof Rigid Core

SPC addresses a practical problem in wet or variable-temperature interior spaces because its stone-plastic core does not swell like wood-based products under moisture exposure. Homeowners value click-lock floating installation that avoids adhesives, shortens project duration, and lowers labor costs compared with glue-down jobs, helping the North American SPC flooring market capture a larger share of renovation budgets. SPC adoption is supported by measurable shifts in renovation behavior and material performance needs. According to the National Association of Realtors, existing homes account for roughly 85-90% of annual housing transactions, sustaining a large renovation base. The Home Improvement Research Institute notes that over 60% of homeowners undertake at least one DIY project annually, with flooring among the most common upgrades. SPC also maintains structural stability over a temperature range of approximately -20°C to 60°C, minimizing expansion gaps in sunlit or semi-conditioned spaces. These performance characteristics translate into lower maintenance frequency and reduced lifecycle costs, reinforcing repeat purchases among landlords and owner-occupiers.

Shift from Flexible LVT/WPC to SPC on Performance to Price

SPC's higher core density and compression tolerance improve resistance to rolling loads and furniture legs compared to softer WPC or flexible LVT, supporting wider use in high-traffic zones at accessible price points. Property owners who switch from carpet or flexible LVT to SPC in busy corridors and living areas report fewer expansion and contraction issues, which cuts callbacks for replacements and repairs. The North American SPC flooring market also benefits from the perception that rigid core formats deliver greater value per dollar due to their durability, scratch resistance, and water tolerance in daily use. The transition toward SPC is driven by quantifiable improvements in mechanical performance relative to flexible LVT and WPC. According to ASTM International, SPC's rigid core density typically exceeds 1,900-2,100 kg/m3, compared with 800-1,200 kg/m3 for WPC, resulting in significantly higher resistance to indentation and rolling loads.

Tariffs, UFLPA Scrutiny, and PVC Input Price Volatility

Importers adjust sourcing and documentation to show clean supply chains because enforcement tools now require higher confidence evidence and end-to-end traceability. According to U.S. Customs and Border Protection, enforcement under the Uyghur Forced Labor Prevention Act led to over 3,500 shipment detentions valued at over USD 900 million in its first year, increasing compliance costs and clearance times. Buyers weigh landed cost scenarios that include tariff exposure, Section 301 tariffs on Chinese vinyl flooring products remain at up to 25%, and potential detentions, which can extend port dwell times by 2-4 weeks and add storage and demurrage costs of USD 100-USD 300 per container per day. PVC resin remains a significant share of SPC cost, and swings in resin pricing create margin pressure when retail price points are tightly managed. Some brands diversify production footprints to Southeast Asia or North America to balance tariff grids and streamline audits, which shifts how volumes are allocated to the United States and Canada . These cross-currents make planning more complex and temper near-term growth for the North American SPC flooring market.

Other drivers and restraints analyzed in the detailed report include:

- Retail Push: Home Centers and Specialty Expanding SPC Access

- Commercial Uptake in Hospitality and Multifamily Retrofits

- Quality Issues from Ultra Thin SPC Eroding Category Trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SPC planks held 72.10% in 2025, and SPC tiles are projected to post a 7.10% CAGR through 2031 as design-driven projects gain scale in the North America SPC flooring market. Planks benefit from realistic wood visuals, embossed textures, and familiar room layouts that align with residential preferences and DIY installation flows. Tile formats expand use cases in hospitality and mixed-use spaces where geometric layouts or larger modules reduce grout lines and speed maintenance routines. Installers cite consistent click lock performance and flatness as critical for large format tiles, which supports the selection of certified systems in higher traffic locations. This balance of aesthetics and practicality positions both formats to contribute to steady growth in the North America SPC flooring market.

SPC tiles improve differentiation against laminate and flexible vinyl because tiles enable visual narratives not easily created with plank-only assortments. Product teams add slip-resistant finishes and thicker wear layers to tile SKUs aimed at public spaces, which helps preserve appearance under daily cleaning and rolling traffic. As home centers and specialty stores adjust planograms to include more statement tile options, tiles can capture incremental share without displacing core plank volume in the North America SPC flooring market. Visualizer tools also help household buyers evaluate tile looks at home, which lowers decision friction for pattern rich spaces.

The 5.1-6.0 mm class accounted for 34.80% of the North America SPC flooring market share in 2025, while planks thicker than 6.5 mm are projected to post a 7.45% CAGR through 2031. Mid-range constructions balance rigid core stability with competitive cost, making them a good fit for most residential rooms and many light commercial spaces. Thicker builds integrate attached pads that support impact sound reduction, helping satisfy building code targets in many assemblies when paired with appropriate subfloors. Contractors highlight edge strength and profile precision as keys to long-term performance across all thicknesses, a claim reinforced by the fracture resistance test adopted in the ASSURE standard. These attributes inform fit-for-purpose selections across projects in the North America SPC flooring market.

Thin, entry-level products can work for quick cosmetic refreshes, yet they are more sensitive to subfloor flatness and heavy point loads, which increases the risk in high-traffic spaces. Premium >6.5 mm products suit hospitality corridors and multifamily units above grade because acoustics and indentation resistance carry more weight in those applications. Installers who standardize on a thickness band reduce training complexity and minimize profile transition issues at doorways, which improves job outcomes in the North America SPC flooring industry . Buyers weigh total installed cost and code alignment, which keeps mid range SKUs central to the North America SPC flooring market.

Complete Report Scope:

- By Product Type

- SPC Tiles

- SPC Planks

- By Product Thickness

- 4.0-5.0 mm

- 5.1-6.0 mm

- 6.1-6.5 mm

- Above 6.5 mm

- By Installation Method

- Self-Adhesive

- Glue-Down

- Interlocking/Click-lock

- Others

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C / Retail

- Home Centers

- Specialty Flooring Stores

- Online

- Local Hardware Shops (unorganized market)

- Other Distribution Channels

- B2B / Contractors

- B2C / Retail

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Shaw Industries

- Mohawk Industries

- Mannington Mills

- AHF Products

- Tarkett North America

- CFL Flooring

- Novalis Innovative Flooring (NovaFloor)

- Wellmade Performance Floors

- Nox Corporation

- Huali Floors

- Gerflor

- Beaulieu International Group (Beauflor)

- LX Hausys (formerly LG Hausys)

- United Surface Solutions

- Republic Floor (manufacturing)

- Zhejiang Kingdom Flooring Plastic Co., Ltd.

- Zhejiang Walrus New Material Co., Ltd.

- Zhangjiagang Yihua Plastics Co., Ltd.

- Jiangsu Lejia Plastic Co., Ltd.

- Changzhou Runchang Wood Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renovation and DIY preference for waterproof rigid core

- 4.2.2 Shift from flexible LVT/WPC to SPC on performance-to-price

- 4.2.3 Retail push: home centers and specialty expanding SPC access

- 4.2.4 Commercial uptake in hospitality and multifamily retrofits

- 4.2.5 Locking-system advances (5G/Unilin) cut install time/recalls

- 4.2.6 Nearshoring/domestic SPC capacity reduces lead-times/compliance risk

- 4.3 Market Restraints

- 4.3.1 Tariffs/UFLPA detentions and PVC input volatility

- 4.3.2 Quality issues from ultra-thin SPC eroding category trust

- 4.3.3 IP enforcement (USITC GEO on interlocking LVT/SPC) raises costs

- 4.3.4 Tightening standards (ASSURE v2.0 fracture test) add retooling burden

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Industry

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD Billion)

- 5.1 By Product Type

- 5.1.1 SPC Tiles

- 5.1.2 SPC Planks

- 5.2 By Product Thickness

- 5.2.1 4.0-5.0 mm

- 5.2.2 5.1-6.0 mm

- 5.2.3 6.1-6.5 mm

- 5.2.4 Above 6.5 mm

- 5.3 By Installation Method

- 5.3.1 Self-Adhesive

- 5.3.2 Glue-Down

- 5.3.3 Interlocking/Click-lock

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C / Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Local Hardware Shops (unorganized market)

- 5.5.1.5 Other Distribution Channels

- 5.5.2 B2B / Contractors

- 5.5.1 B2C / Retail

- 5.6 By Geography

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Shaw Industries

- 6.4.2 Mohawk Industries

- 6.4.3 Mannington Mills

- 6.4.4 AHF Products

- 6.4.5 Tarkett North America

- 6.4.6 CFL Flooring

- 6.4.7 Novalis Innovative Flooring (NovaFloor)

- 6.4.8 Wellmade Performance Floors

- 6.4.9 Nox Corporation

- 6.4.10 Huali Floors

- 6.4.11 Gerflor

- 6.4.12 Beaulieu International Group (Beauflor)

- 6.4.13 LX Hausys (formerly LG Hausys)

- 6.4.14 United Surface Solutions

- 6.4.15 Republic Floor (manufacturing)

- 6.4.16 Zhejiang Kingdom Flooring Plastic Co., Ltd.

- 6.4.17 Zhejiang Walrus New Material Co., Ltd.

- 6.4.18 Zhangjiagang Yihua Plastics Co., Ltd.

- 6.4.19 Jiangsu Lejia Plastic Co., Ltd.

- 6.4.20 Changzhou Runchang Wood Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 Performance-led premiumization: thicker SPC (> 6.5 mm) for IIC/STC code compliance in multifamily/hospitality

- 7.2 Domestic/nearshore SPC programs for tariff/UFLPA-sensitive RFPs with faster lead-times