|

시장보고서

상품코드

2072646

미국의 소독제 및 살균제 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Antiseptic And Disinfectant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

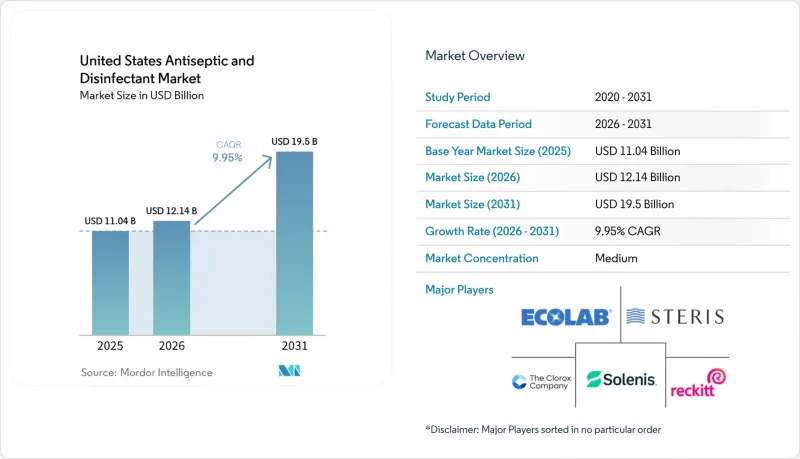

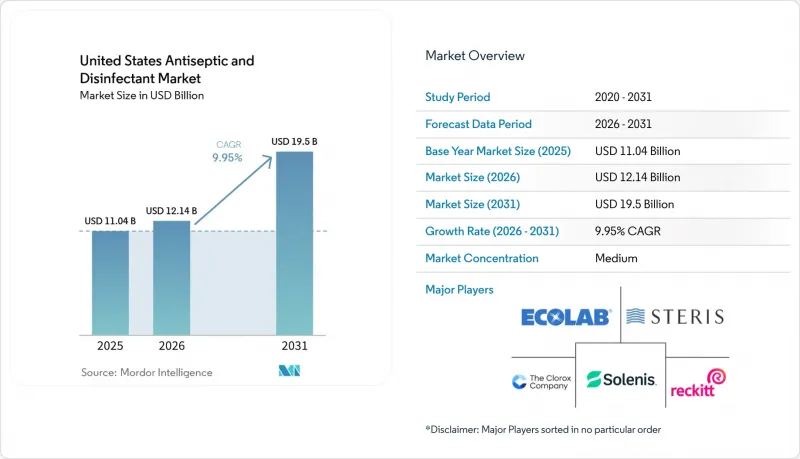

Mordor Intelligence에 의하면, 미국의 소독제 및 살균제 시장 규모는 2025년에 110억 4,000만 달러로 평가되었고, 2026년 121억 4,000만 달러로 추정되고, 2031년까지 195억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 9.95%를 나타낼 전망입니다.

본 보고서는 제품 유형별(QAC, 염소 화합물, 알코올 및 알데히드, 비구아나이드 및 요오드, H₂O₂ 및 과초산, 효소계 세정제, 기타), 제형별(액체, 물티슈, 스프레이 및 에어로졸, 젤 및 폼), 용도별(표면, 의료기기의 고수준 소독(HLD), 기구 및 효소계, 피부 전처리, 기타), 최종 사용자별(병원, 외래수술센터(ASC), 장기 요양 시설별(LTC) 및 특별 양로원별(SNF), 검사실, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 소독제 및 살균제 시장 동향과 인사이트

끊임없이 지속되는 병원 내 감염(HAI), 칸디다 아울리스, 그리고 다제내성균(MDRO)의 위협

의료 관련 감염(HAI)은 미국의 소독제 및 살균제 시장 전체에서 지속적인 수요를 뒷받침하고 있습니다. 2024년 CDC 보고서에 따르면, 미국 병원에서는 2023년과 비교해 대부분의 병원 내 감염(HAI) 범주에서 2%에서 11%의 감소가 나타났으나, 복부 자궁적출술 후 수술 부위 감염은 여전히 8% 증가했으며, 시술 유형에 따라 감염 관리 성과에 차이가 있는 것으로 나타났습니다. 칸디다 아우리스(Candida auris)는 CDC가 2024년에 6,304건의 임상 사례를 확인함에 따라(2023년의 4,523건에서 증가), 조달을 촉진하는 요인으로서 그 중요성이 더욱 커지고 있습니다. 칸디다 아울리스는 여러 유형의 항진균제에 내성을 보이기 때문에 의료 기관에서는 치료에만 의존하기보다는 환경 소독과 더 강력한 포자 살균 절차에 중점을 두고 있습니다. 이러한 압박은 더 이상 급성기 병원 내부에만 국한되지 않습니다. 장기 급성기 치료 병원과 인공호흡기를 갖춘 전문 요양 시설도, 확산과 감염 사례를 계기로 조달 기준을 강화하고 있기 때문입니다. 이러한 변화로 인해, 미국 소독제 및 살균제 시장의 고객 기반은 기존에는 그다지 고가의 제품을 구매하지 않았던 급성기 이후 의료 현장으로 확대되고 있습니다.

의료 및 공공기관의 영구적인 위생 기준

팬데믹 이후의 위생 기준은 많은 바이어들이 당초 예상했던 것보다 더 오랫동안 유지되고 있으며, 이것이 미국의 소독제 및 살균제 시장을 계속해서 지탱하고 있습니다. CDC의 지침과 병원의 감염 예방 대책에 따라, 표면 청소 빈도와 소독 절차가 비상 시 프로토콜이 아닌 일상 업무로 정착되었습니다. 즉, 시설에서 병상 수를 줄이거나 서비스 구성을 변경하더라도 소독제 사용량이 그만큼 줄어들지는 않습니다. 현재, 수요를 주도하는 더 중요한 요인은 사용 중인 방, 시술 구역 및 공용 장비별 소독제 사용량입니다. 이로 인해 병원 통합이나 성숙한 의료 시장에서 인구 증가세가 둔화되는 상황에서도 판매량은 더욱 탄탄해지고 있습니다. 또한, 워크플로우상의 실수를 줄이고, 살균 시간을 단축하며, 표면과의 적합성을 향상시키는 프리미엄 제품에 대한 수요도 생기고 있습니다. 이러한 기능들은 시설이 프로토콜을 더 엄격하게 준수하는 데 도움이 되기 때문입니다.

첨단 의료기기 및 표면과의 재료 적합성 위험

적합성 관련 위험은 미국 내 소독제 및 살균제 시장에 있어 여전히 실질적인 제약 요인으로 작용하고 있습니다. 특히, 복잡한 재사용 가능한 의료기기나 폴리머를 많이 사용한 기기를 사용하는 환경에서는 그 현상이 두드러집니다. 화학적 부적합은 환경 응력 균열, 광학적 손상, 씰의 열화를 초래할 수 있으며, 그 결과 장비의 수명을 단축시키고 수리 비용을 증가시킬 가능성이 있습니다. PDI 적합성에 관한 문서에 따르면, 유효 항균 성분뿐만 아니라 용매, 계면활성제, pH 조절제 등의 비활성 성분도 표면 열화의 주요 원인이 될 수 있다고 합니다. 이로 인해 감염 관리팀이 표준화를 추진하기가 어려워집니다. 왜냐하면 다양한 장비 구성에서 승인된 모든 표면에 적합한 단일 제품은 거의 없기 때문입니다. 자본 예산이 부족해지면서 로봇 수술 시스템이나 첨단 내시경 기기의 가동 기간이 길어짐에 따라, 이 문제는 더욱 심각해지고 있습니다. 그렇긴 하지만, 이러한 제약은 재료에 가해지는 부담을 늘리지 않으면서도 효능을 유지하기 위해 표면 특성을 고려한 화학 플랫폼 개발을 공급업체가 추진하도록 유도하는 요인이 되고 있습니다.

부문별 분석

2025년, 제품 유형별로 살펴본 미국의 소독제 및 살균제 시장에서 QAC(4급 암모늄 화합물)는 32.31%의 점유율을 차지했으며, 경질 및 연질 등 다양한 표면의 이용 사례에 대응할 수 있다는 점 덕분에 계속해서 1위 자리를 지켰습니다. 이러한 폭넓은 범용성, 낮은 사용 비용, 그리고 다양한 의료용 플라스틱과의 호환성 덕분에, 병원 및 의료 기관에서 QAC는 여전히 처방 목록에서 큰 비중을 차지하고 있습니다. QAC가 차지하는 미국 소독제 및 살균제 시장 점유율은 일상적인 환경 청소 프로그램에서 QAC가 오랫동안 수행해 온 역할도 반영하고 있습니다. 그렇긴 하지만, 일부 감염 예방 팀이 치사 농도 미만의 QAC에 노출된 미생물의 내성 양상에 대한 보고에 더욱 주목하고 있기 때문에 그 지위가 완전히 확고한 것은 아닙니다. 특히 C. difficile 및 C. auris의 오염 제거와 관련된 프로토콜에서 편의성보다 포자 살균 성능이 더 중요하게 여겨지는 경우, 염소계 화합물은 여전히 중요한 역할을 하고 있습니다.

효소계 세정제는 2026-2031년 연평균 성장률(CAGR) 11.38%를 나타낼 것으로 예측되며, 이 부문에서 가장 빠르게 성장하는 제품 유형이 될 전망입니다. 수요를 견인하고 있는 요인은 저침습 수술 증가, 재사용 가능한 기구의 복잡화, 그리고 무균 조제 세척 절차의 철저화입니다. 다중 효소가 함유된 제품은 소독 전 단일 세척 공정만으로 단백질, 지질, 탄수화물, 생물막을 분해할 수 있다는 점에서 가치가 있습니다. 헬스케어 서피스 인스티튜트(Healthcare Surfaces Institute)의 연구 발표에 따르면, 일반적인 세제가 함유된 물티슈조차 0.5%의 변형률에서 일부 플라스틱에 환경 응력 균열을 유발할 가능성이 있다고 지적되고 있으며, 이것이 시설 측이 세정 성능뿐만 아니라 소재에 대한 친화성에도 더욱 주목하고 있는 이유를 설명해 줍니다. 과산화수소 및 과초산 제품 역시 포자 살균 효과와 뛰어난 생분해성을 겸비하고 있어, 내시경 재처리 분야에서 시장 점유율을 확대되고 있습니다. 알코올, 알데히드, 비구아나이드, 요오드 유도체 및 일부 특수한 화학 물질은 특정 환경에서 여전히 사용되고 있지만, 증거에 기반한 약제 목록의 재검토로 인해 우선순위가 낮은 제품 시장 점유율은 점차 줄어들고 있습니다.

2025년 기준, 미국의 소독제 및 살균제 시장에서 액상 제형은 제형별 점유율 52.24%를 차지했으며, 의료기관에서의 사용에 있어 여전히 가장 큰 비중을 차지하고 있습니다. 시설에서 1회 사용당 비용이 저렴하고 대량 공급이 가능하며, 광범위한 환경 위생 프로그램을 위해 유연한 희석이 필요한 경우, 액상 제제는 여전히 가장 일반적인 선택지입니다. 미국의 소독제 및 살균제 시장 중 액상 제품이 차지하는 규모는 청소와 소독을 단일 작업 흐름으로 결합할 수 있는 EPA 등록 원스텝 소독 세정제에 의해서도 뒷받침되고 있습니다. 스프레이나 에어로졸은 소규모 외래 진료 현장이나 손이 닿기 어려운 표면에서 여전히 중요하며, 한편 젤이나 폼은 손의 항균 및 상처 관리 분야에서 계속해서 실용적인 역할을 수행하고 있습니다.

와이프 시장은 2026-2031년 연평균 성장률(CAGR) 10.52%를 나타낼 것으로 예측되며, 가장 두드러진 성장세를 보이는 제형입니다. 그 가치는 더 이상 편의성에만 그치지 않습니다. 일회용 제품이기 때문에 희석 실수를 줄이고, 사용 현장에서 유효 성분 농도를 적절하게 관리할 수 있기 때문입니다. 또한, 시설 측에서는 와이프가 직원들의 규정 준수 의식 향상에 도움이 된다고 보고 있습니다. 그 이유는 이러한 형태라면 교육이 용이하고, 분주한 간호 구역 전체에서 표준화하기 쉽기 때문입니다. 2024년 7월 에코랩이 출시한 '소독용 물티슈 1장'은 공급업체가 신속한 소독 효과를 내세우면서도 생분해성이나 플라스틱 미사용이라는 장점을 결합함으로써, 물티슈를 단순한 범용 제품의 범주를 넘어선 제품으로 포지셔닝하려 하고 있음을 보여줍니다. 2025년 9월 CloroxPro가 출시한 'Screen+소독 물티슈'는 터치스크린, 노트북, 공유 전자기기를 대상으로 하며, 와이프의 혁신이 기기 관련 관리 업무의 워크플로우로 확대되고 있음을 다시 한번 보여주었습니다(단, 이 제품에 관한 시장 조사 인용 자료는 여기에서는 사용하지 않았습니다). 앞으로 호환성에 관한 보다 확실한 데이터와 환경적 배려가 제시됨에 따라, 프리미엄 와이프 형식에 대한 기존의 비용 측면에서의 우려는 점차 사라질 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the united states antiseptic and disinfectant market size was valued at USD 11.04 billion in 2025 and is estimated to grow from USD 12.14 billion in 2026 to reach USD 19.5 billion by 2031, at a CAGR of 9.95% during the forecast period (2026-2031).

This report is Segmented by Product Type (QACs, Chlorine Compounds, Alcohols & Aldehydes, Biguanides & Iodine, H2O2 & Peracetic Acid, Enzymatic Cleaners, Other), Formulation (Liquids, Wipes, Sprays & Aerosols, Gels & Foams), Application (Surface, Medical Device HLD, Instrument & Enzymatic, Skin Prep, Other), and End User (Hospitals, Ascs, LTC & SNFs, Labs, Other). Value (USD).

United States Antiseptic And Disinfectant Market Trends and Insights

Persistent HAI, Candida Auris, and MDRO Pressure

Healthcare-associated infections continue to support recurring demand across the US antiseptic and disinfectant market. CDC reporting for 2024 showed that U.S. hospitals reduced most HAI categories by 2% to 11% from 2023, but abdominal hysterectomy surgical site infections still increased by 8%, which shows that infection control performance remains uneven by procedure type. Candida auris has become a stronger procurement trigger because the CDC confirmed 6,304 clinical cases in 2024, up from 4,523 in 2023. Because C. auris is resistant across multiple antifungal classes, facilities rely more heavily on environmental disinfection and stronger sporicidal protocols than on treatment alone. This pressure no longer sits only inside acute hospitals, because long-term acute care hospitals and ventilator-capable skilled nursing facilities are also tightening purchasing standards after colonization and transmission events. That shift is widening the customer base for the US antiseptic and disinfectant market into post-acute settings that historically purchased less sophisticated products.

Permanent Hygiene Baselines Across Healthcare and Public Institutions

The post-pandemic hygiene floor has remained in place longer than many buyers first expected, which continues to support the US antiseptic and disinfectant market. CDC guidance and hospital infection prevention practices have kept more frequent surface turnover and disinfection routines embedded in day-to-day operations rather than emergency protocols. That means facilities can lower bed capacity or change service mix without producing a similar drop in disinfectant use. The more important demand driver is now disinfectant use intensity per occupied room, procedure area, and shared device. This makes volumes more resilient against hospital consolidation and slower demographic growth in mature care markets. It also creates room for premium products that reduce workflow errors, shorten kill times, or improve surface compatibility because those features help facilities hold tighter protocol compliance.

Material Compatibility Risk With Advanced Devices and Surfaces

Compatibility risk remains a practical restraint for the US antiseptic and disinfectant market, especially in settings that use complex reusable devices and polymer-heavy equipment. Incompatible chemistries can contribute to environmental stress cracking, optical damage, and seal degradation, which can shorten device life and increase repair cost. PDI's compatibility documentation states that inactive ingredients such as solvents, surfactants, and pH modifiers can be major contributors to surface degradation, not only the active antimicrobial ingredient. This makes standardization harder for infection control teams because one product rarely fits every approved surface across a mixed equipment base. The challenge becomes more severe as robotic surgery systems and advanced endoscopy assets remain in service longer under tighter capital budgets. Even so, this restraint is also pushing suppliers toward surface-aware chemistry platforms that try to protect efficacy without increasing material stress.

Other drivers and restraints analyzed in the detailed report include:

- Outpatient Surgery Migration Increasing Fast-Turn Reprocessing Demand

- EPA List N and EVP-Ready Procurement Standards

- EPA/FDA Registration, Labeling, and Claim-Substantiation Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

QACs held 32.31% of the US antiseptic and disinfectant market by product type in 2025, which kept them in the leading position because they work across many hard and soft surface use cases. Their broad utility, cost-in-use profile, and compatibility with many healthcare plastics continue to support large formulary positions across hospitals and institutional settings. The US antiseptic and disinfectant market share held by QACs also reflects their long-standing role in routine environmental cleaning programs. Even so, that position is not fully secure because some infection prevention teams are paying closer attention to documented tolerance patterns in organisms exposed to sub-lethal QAC concentrations. Chlorine compounds remain important where sporicidal performance matters more than convenience, especially in protocols tied to C. difficile and C. auris decontamination.

Enzymatic cleaners are forecast to expand at an 11.38% CAGR from 2026 to 2031, making them the fastest-growing product type in this segment. Demand is being pulled by minimally invasive surgery growth, higher reusable instrument complexity, and more intensive sterile compounding cleaning routines. Multi-enzyme formulations have value because they break down proteins, lipids, carbohydrates, and biofilm in a single cleaning step before disinfection. A Healthcare Surfaces Institute study presentation noted that even standard detergent wipes can induce environmental stress cracking in several plastics at 0.5% strain, which explains why facilities are paying more attention to material gentleness as well as cleaning performance. Hydrogen peroxide and peracetic acid products are also gaining space in endoscopy reprocessing because they combine sporicidal action with better biodegradability profiles. Alcohols, aldehydes, biguanides, iodine derivatives, and smaller niche chemistries continue to serve specific settings, but evidence-based formulary reviews are gradually compressing the tail of low-priority products.

Liquid formulations commanded 52.24% of the US antiseptic and disinfectant market by formulation in 2025, keeping them as the largest format across institutional use. Liquids remain the default choice where facilities need low cost per use, bulk dispensing, and flexible dilution for broad environmental services programs. The US antiseptic and disinfectant market size attached to liquids is also supported by one-step EPA-registered disinfectant cleaners that help sites combine cleaning and disinfection in a single workflow. Sprays and aerosols still matter in smaller outpatient settings and on hard-to-reach surfaces, while gels and foams keep a practical role in hand antisepsis and wound-related applications.

Wipes are projected to grow at a 10.52% CAGR from 2026 to 2031, which makes them the fastest-growing formulation. Their value is no longer limited to convenience because the unit-dose format also reduces dilution error and helps deliver a controlled active concentration at the point of use. Facilities also view wipes as helpful in staff compliance because the format is simpler to train and easier to standardize across fast-paced care areas. Ecolab's Disinfectant 1 Wipe launch in July 2024 showed how suppliers are pairing rapid disinfection claims with biodegradability and plastic-free positioning to move wipes beyond commodity status. CloroxPro's September 2025 Screen+ Sanitizing Wipes launch, which targeted touchscreens, laptops, and shared electronics, further showed that wipe innovation is extending into device-adjacent care workflows, although the supporting market-research citation behind that product reference is not used here. Over time, stronger compatibility data and environmental credentials are likely to narrow the historic cost objection to premium wipe formats.

Complete Report Scope:

- By Product Type

- Quaternary Ammonium Compounds

- Chlorine Compounds

- Alcohols & Aldehyde Products

- Biguanides & Iodine Derivatives

- Hydrogen Peroxide & Peracetic Acid

- Enzymatic Cleaners

- Other Product Types

- By Formulation

- Liquids

- Wipes

- Sprays & Aerosols

- Gels & Foams

- By Application

- Surface Disinfectants

- Medical Device High-Level Disinfectants

- Instrument & Enzymatic Cleaners

- Skin Preparation Antiseptics

- Other Applications

- By End User

- Hospitals & Clinics

- Ambulatory Surgery Centers

- Long-Term Care & Skilled Nursing Facilities

- Laboratories & Diagnostic Centers

- Other End Users

List of Companies Covered in this Report:

- Advanced Sterilization Products (ASP)

- Atlantis Consumer Healthcare Inc.

- Beckton Dickinson

- Best Sanitizers, Inc.

- Cardinal Health

- Diversey, a Solenis Company

- Ecolab

- Kimberly-Clark Worldwide

- Lonza LLC

- Medline Industries

- Metrex Research, LLC

- PDI Healthcare

- Procter & Gamble

- Reckitt Benckiser Group

- SC Johnson Professional USA, Inc.

- Solventum Corporation

- STERIS

- The Clorox Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Persistent HAI, Candida auris, and MDRO pressure

- 4.2.2 Permanent hygiene baselines across healthcare and public institutions

- 4.2.3 Outpatient surgery migration increasing fast-turn reprocessing demand

- 4.2.4 EPA List N and EVP-ready procurement standards

- 4.2.5 Revised USP sterile-compounding hygiene intensity

- 4.3 Market Restraints

- 4.3.1 Material compatibility risk with advanced devices and surfaces

- 4.3.2 EPA/FDA registration, labeling, and claim-substantiation burden

- 4.3.3 Product contamination recalls raising QA and switching costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Quaternary Ammonium Compounds

- 5.1.2 Chlorine Compounds

- 5.1.3 Alcohols & Aldehyde Products

- 5.1.4 Biguanides & Iodine Derivatives

- 5.1.5 Hydrogen Peroxide & Peracetic Acid

- 5.1.6 Enzymatic Cleaners

- 5.1.7 Other Product Types

- 5.2 By Formulation

- 5.2.1 Liquids

- 5.2.2 Wipes

- 5.2.3 Sprays & Aerosols

- 5.2.4 Gels & Foams

- 5.3 By Application

- 5.3.1 Surface Disinfectants

- 5.3.2 Medical Device High-Level Disinfectants

- 5.3.3 Instrument & Enzymatic Cleaners

- 5.3.4 Skin Preparation Antiseptics

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Ambulatory Surgery Centers

- 5.4.3 Long-Term Care & Skilled Nursing Facilities

- 5.4.4 Laboratories & Diagnostic Centers

- 5.4.5 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)}

- 6.3.1 Advanced Sterilization Products (ASP)

- 6.3.2 Atlantis Consumer Healthcare Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Best Sanitizers, Inc.

- 6.3.5 Cardinal Health Inc.

- 6.3.6 Diversey, a Solenis Company

- 6.3.7 Ecolab Inc.

- 6.3.8 Kimberly-Clark Corporation

- 6.3.9 Lonza LLC

- 6.3.10 Medline Industries, LP

- 6.3.11 Metrex Research, LLC

- 6.3.12 PDI Healthcare

- 6.3.13 Procter & Gamble Co.

- 6.3.14 Reckitt Benckiser Group plc

- 6.3.15 SC Johnson Professional USA, Inc.

- 6.3.16 Solventum Corporation

- 6.3.17 STERIS plc

- 6.3.18 The Clorox Company

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment