|

시장보고서

상품코드

2072697

미국의 여성 건강 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Women´s Health - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

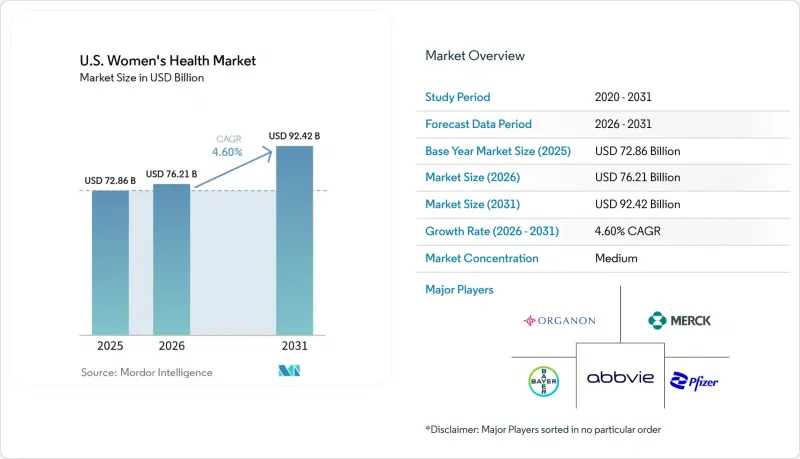

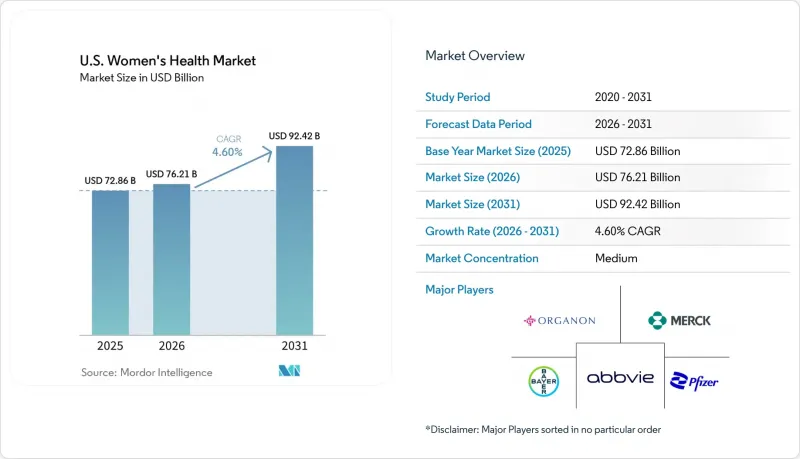

Mordor Intelligence에 의하면, 미국의 여성 건강 시장 규모는 2025년 728억 6,000만 달러로 평가되었고, 2026년에는 762억 1,000만 달러로 추정되고, 2031년까지 924억 2,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 4.60%로 성장할 전망입니다.

본 보고서는 제공 분야별(의약품, 의료기기, 진단약, 디지털 헬스, 영양보조식품), 용도별(피임, 불임 치료, 갱년기 등), 의료 제공 현장별(병원, 산부인과, 불임 치료 시설, 검사 기관, 원격 의료), 연령대별(사춘기, 생식 연령, 폐경 전후, 폐경 후), 유통 채널별(소매, 온라인, 전문 약국, 병원, DTC)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 여성 건강 시장 동향 및 인사이트

비침습적 및 진료소 내 여성 건강 시술에 대한 수요 증가

미국의 여성 건강 시장에서는 응급성이 낮은 의료 환경에서의 시술이 점점 더 보편화되고 있습니다. 2026년 4월, Femasys사는 'FemaSeed Complete'를 출시했습니다. 이를 통해 산부인과 의사는 1차 선택지인 인공수정을 시행하거나 진료소 내에서 정자 처리가 가능해지며, 외부 검사 기관에 대한 의존도가 낮아집니다. 이 혁신적인 기술은 불임 치료에 대한 접근성을 높이고, 환자의 비용 부담을 줄여줍니다. 또한, 2026년 초 FemaSeed를 이용한 난관 내 인공수정에 대한 새로운 카테고리 III CPT 코드가 승인됨에 따라 보험 급여 체계가 강화되어, 치료의 보급과 환자 참여가 가속화되고 있습니다.

치료 가능한 질환으로서 갱년기에 대한 임상적 인식의 확대

갱년기 관리는 미국 여성 건강 시장에서 주요 관심사로 부상하고 있으며, 수요 증가를 주도하고 있습니다. FDA는 2025년 10월 엘리나제탄을 승인함으로써, 갱년기 열감에 대한 비호르몬 치료 옵션을 확대했습니다. 2026년 2월, FDA는 6가지 호르몬 치료제의 포장 경고문을 삭제함으로써, 오랫동안 제기되어 온 처방 관련 우려를 해소했습니다. 이러한 진전은 근거에 기반한 치료를 촉진하고, 더 많은 여성이 중년기에 진단과 치료를 받도록 장려하고 있습니다.

진단 지연과 치료 시작 지연이 여전히 계속되고 있습니다.

진단 부족으로 인해 미국 여성 건강 시장에서는 임상적 수요가 치료 건수로 이어지지 못하고 있습니다. 다낭성 난소 증후군은 가임기 여성의 6%에서 12%에 영향을 미치고 있지만, 많은 여성이 오랫동안 진단받지 못한 채 지내고 있습니다. 미국에서 자궁내막증의 경우 평균 4.4년의 진단 지연이 발생하고 있으며, 증상이 악화된 후에야 치료가 시작되는 경우가 많아 경제적 부담으로 이어지고 있습니다. 자궁근종과 자궁내막증은 모든 의료 현장에서 여전히 진단이 미흡하여, 유병률과 기록된 치료 건수 사이에 차이가 발생하고 있습니다. 진단이 늦어지면 초기 단계에서 의약품 사용이 줄어들게 되어, 환자들이 복잡하고 확장성이 낮은 치료법으로 내몰리게 됩니다.

부문별 분석

2025년, 피임, 갱년기, 자궁내막증, 다낭성 난소 증후군(PCOS) 관리에서의 역할을 배경으로, 의약품은 미국 여성 건강 시장의 45.12%를 차지했습니다. 처방약에 의한 치료는 환자 수가 많은 질환에 대한 주요 치료법으로 자리 잡고 있습니다. 2025년 10월 FDA가 엘리나제탄(elinzanetant)을 승인함에 따라, 비호르몬성 갱년기 치료의 선택지가 확대되었습니다. 오르가논은 2026년 1분기 여성 건강 관련 매출이 16% 감소했다고 보고하며, 사업 규모 확대와 병행하여 제품 포트폴리오를 개편할 필요가 있음을 강조했습니다.

디지털 헬스 솔루션 시장은 2031년까지 연평균 성장률(CAGR) 7.25%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 부문이 될 전망입니다. 메이븐은 2026년 5월, GLP-1 치료, 호르몬 요법 및 30개 이상의 여성 건강 전문 분야를 통합하여 가상 클리닉을 확충했습니다. Onclarity HPV 자가 채취 키트나 BD Onclarity HPV 분석법 등 진단 및 의료기기 중심의 서비스는 침습성이 낮은 치료 경로에 대한 접근성을 높이고 있습니다.

피임 및 가족 계획은 2025년 미국 여성 건강 시장에서 36.76%를 차지했으며, 이는 소매, 의료 기관, 공적 보험 등 각 채널에 걸쳐 광범위한 역할을 반영하고 있습니다. 이 부문은 상담 및 처방전 갱신을 지원하는 디지털 플랫폼에 힘입어, 정기 처방, 지속형 제품, 예방 의료의 혜택을 누리고 있습니다.

갱년기 관리 시장은 새로운 비호르몬 치료법과 호르몬 요법의 적응증 확대에 힘입어 2031년까지 연평균 성장률(CAGR) 6.56%를 기록하며 성장할 것으로 전망됩니다. 자궁내막증 및 다낭성 난소 증후군(PCOS)은 높은 질병 부담과 미충족 의료 수요로 인해 계속해서 주요 성장 분야로 남아 있으며, 진단 기술의 발전에 따라 약물 사용 및 전문의 의뢰가 증가할 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the u.S. women's health market size is expected to increase from USD 72.86 billion in 2025 to USD 76.21 billion in 2026 and reach USD 92.42 billion by 2031, growing at a CAGR of 4.60% over 2026-2031.

This report is Segmented by Offering (Pharmaceuticals, Devices, Diagnostics, Digital Health, Nutraceuticals), Application (Contraception, Fertility, Menopause, and More), Care Setting (Hospitals, OB-GYN, Fertility, Labs, Telehealth), Age Group (Adolescents, Reproductive, Peri-, Postmenopausal), Distribution (Retail, Online, Specialty, Hospital, DTC). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Women's Health Market Trends and Insights

Rising Demand for Noninvasive and In-Office Women's Health Procedures

The United States women's health market is increasingly adopting procedures in lower-acuity settings. In April 2026, Femasys introduced FemaSeed Complete, enabling OB-GYNs to perform first-line inseminations and in-office sperm preparations, reducing reliance on external labs. This innovation simplifies fertility care access and lowers patient costs. Additionally, the approval of a new Category III CPT code for FemaSeed intratubal insemination in early 2026 strengthens reimbursement pathways, accelerating treatment adoption and patient participation.

Expanding Clinical Recognition of Menopause as a Treatable Condition

Menopause care is becoming a mainstream focus in the United States women's health market, driving increased demand. The FDA approved elinzanetant in October 2025, expanding non-hormonal treatment options for menopause-related hot flashes. In February 2026, the FDA removed boxed warnings from six hormone therapy products, addressing long-standing prescribing concerns. These developments are fostering evidence-based care and encouraging more women to seek diagnosis and treatment during midlife.

Persistent Underdiagnosis and Late Treatment Initiation

Underdiagnosis limits the United States women's health market from converting clinical needs into treatment volumes. Polycystic ovary syndrome affects 6% to 12% of women of reproductive age, yet many remain undiagnosed for extended periods. Endometriosis in the United States faces an average diagnostic delay of 4.4 years, leading to economic burdens as care often begins after symptoms worsen. Uterine fibroids and endometriosis remain underdiagnosed across care settings, creating a gap between prevalence and documented treatment. Late diagnoses reduce early-stage pharmaceutical use and shift patients toward complex, less scalable interventions.

Other drivers and restraints analyzed in the detailed report include:

- Higher Utilization of Fertility Diagnostics and Assisted Reproductive Technologies

- Payor and Employer Interest in Women's Health Benefits

- Coverage Friction for Long-Acting Contraception and Fertility Treatments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, pharmaceuticals accounted for 45.12% of the United States women's health market, driven by their role in managing contraception, menopause, endometriosis, and PCOS. Prescription therapies remain the primary treatment for high-volume conditions. The FDA's approval of elinzanetant in October 2025 expanded non-hormonal menopause treatment options. Organon reported a 16% decline in women's health revenue in Q1 2026, emphasizing the need for portfolio renewal alongside scale.

Digital health solutions are projected to grow at a 7.25% CAGR through 2031, making them the fastest-growing segment. Maven expanded its virtual clinic in May 2026, integrating GLP-1 care, hormone therapy, and over 30 women's health specialties. Diagnostics and device-led offerings, such as the Onclarity HPV Self-Collection Kit and BD Onclarity HPV Assay, are enhancing access to less invasive care pathways.

Contraception and family planning represented 36.76% of the United States women's health market in 2025, reflecting their broad role across retail, provider, and public coverage channels. This segment benefits from recurring prescriptions, long-acting products, and preventive care, supported by digital platforms for consultations and renewals.

Menopause management is projected to grow at a 6.56% CAGR through 2031, driven by new non-hormonal treatments and updated hormone therapy labels. Endometriosis and PCOS remain key growth areas due to high disease burden and unmet needs, with diagnosis improvements expected to boost medication use and specialist referrals.

Complete Report Scope:

- By Offering

- Pharmaceuticals

- Medical Devices

- Diagnostics

- Digital Health Solutions

- Nutraceuticals and Wellness Products

- By Application

- Contraception and Family Planning

- Fertility and Reproductive Endocrinology

- Menopause Management

- Osteoporosis Prevention and Treatment in Women

- Endometriosis and Uterine Fibroids

- PCOS Management

- Breast Health and Screening-Linked Care

- By Care Setting

- Hospitals

- OB-GYN Clinics

- Fertility Centers

- Diagnostic Laboratories

- Retail and Mail-Order Pharmacies

- Telehealth and Virtual Women's Health Platforms

- By Age Group

- Adolescents and Young Adults

- Reproductive Age Women

- Perimenopausal Women

- Postmenopausal Women

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Pharmacies

- Direct-to-Consumer and Employer Channels

List of Companies Covered in this Report:

- Abbvie

- Amgen

- Ascend Wellness Holdings, Inc.

- Bayer

- Dare Bioscience, Inc.

- Exact Sciences

- Femasys Inc.

- Hologic

- Insulet

- Johnson & Johnson

- Labcorp Holdings Inc.

- Merck

- Myovant Sciences Ltd.

- Organon

- Pfizer

- Progyny, Inc.

- Quest Diagnostics

- Teva Pharmaceutical Industries

- The Cooper Companies

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Noninvasive and In-Office Women's Health Care

- 4.2.2 Expanding Clinical Recognition of Menopause as a Treatable Care Category

- 4.2.3 Higher Utilization of Fertility Diagnostics and Assisted Reproductive Services

- 4.2.4 Payor and Employer Interest in Women's Health Benefit Design

- 4.2.5 Wider Adoption of Specialty Women's Health Diagnostics and Digital Navigation

- 4.2.6 State-Level Policy Support for Family Planning and Preventive Care Access

- 4.3 Market Restraints

- 4.3.1 Persistent Underdiagnosis and Late Treatment Initiation in Midlife Women

- 4.3.2 Coverage Friction for Long-Acting Contraception and Fertility Services

- 4.3.3 Clinical Hesitancy and Safety-Label Sensitivity Around Hormonal Therapies

- 4.3.4 Fragmented Care Pathways Across Primary Care, OB-GYN, and Specialty Care

- 4.4 Value and Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Pharmaceuticals

- 5.1.2 Medical Devices

- 5.1.3 Diagnostics

- 5.1.4 Digital Health Solutions

- 5.1.5 Nutraceuticals and Wellness Products

- 5.2 By Application

- 5.2.1 Contraception and Family Planning

- 5.2.2 Fertility and Reproductive Endocrinology

- 5.2.3 Menopause Management

- 5.2.4 Osteoporosis Prevention and Treatment in Women

- 5.2.5 Endometriosis and Uterine Fibroids

- 5.2.6 PCOS Management

- 5.2.7 Breast Health and Screening-Linked Care

- 5.3 By Care Setting

- 5.3.1 Hospitals

- 5.3.2 OB-GYN Clinics

- 5.3.3 Fertility Centers

- 5.3.4 Diagnostic Laboratories

- 5.3.5 Retail and Mail-Order Pharmacies

- 5.3.6 Telehealth and Virtual Women's Health Platforms

- 5.4 By Age Group

- 5.4.1 Adolescents and Young Adults

- 5.4.2 Reproductive Age Women

- 5.4.3 Perimenopausal Women

- 5.4.4 Postmenopausal Women

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online Pharmacies

- 5.5.4 Specialty Pharmacies

- 5.5.5 Direct-to-Consumer and Employer Channels

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 Ascend Wellness Holdings, Inc.

- 6.3.4 Bayer AG

- 6.3.5 Dare Bioscience, Inc.

- 6.3.6 Exact Sciences Corporation

- 6.3.7 Femasys Inc.

- 6.3.8 Hologic, Inc.

- 6.3.9 Insulet Corporation

- 6.3.10 Johnson and Johnson

- 6.3.11 Labcorp Holdings Inc.

- 6.3.12 Merck & Co., Inc.

- 6.3.13 Myovant Sciences Ltd.

- 6.3.14 Organon & Co.

- 6.3.15 Pfizer Inc.

- 6.3.16 Progyny, Inc.

- 6.3.17 Quest Diagnostics Incorporated

- 6.3.18 Teva Pharmaceutical Industries Ltd.

- 6.3.19 The Cooper Companies, Inc.

- 6.3.20 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment