|

시장보고서

상품코드

2072706

미국의 치과용 소프트웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Dental Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

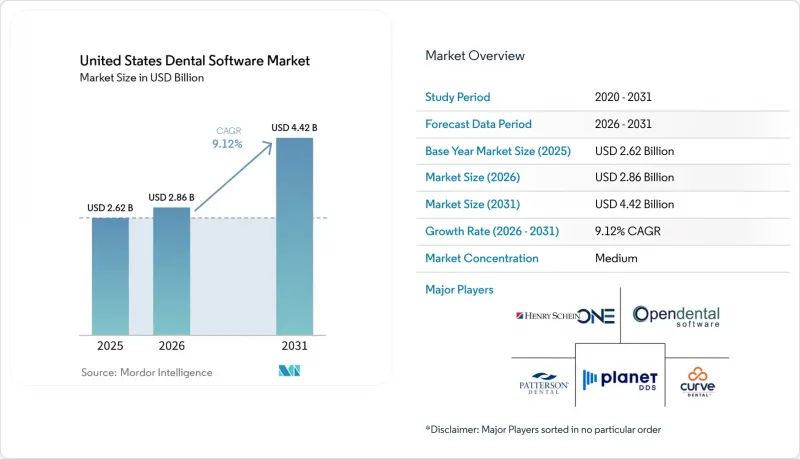

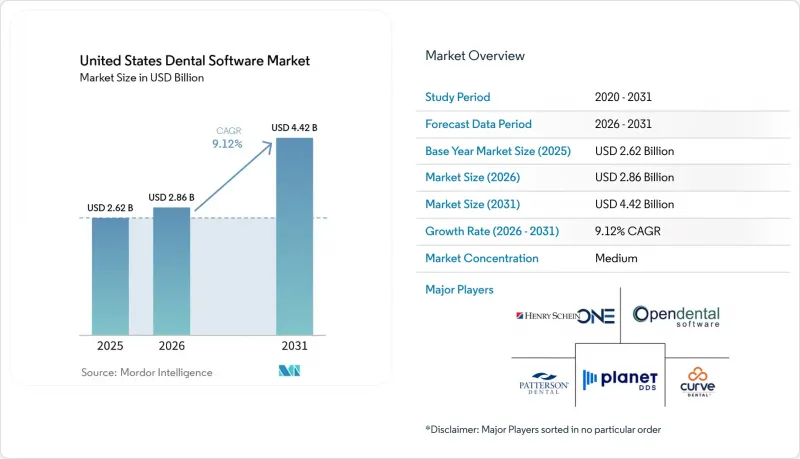

Mordor Intelligence에 의하면, 미국의 치과용 소프트웨어 시장 규모는 2025년에 26억 2,000만 달러로 평가되었고, 2026년에 28억 6,000만 달러로 추정되고, 2031년까지 44억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 9.12%로 성장할 전망입니다.

본 보고서는 도입 형태별(클라우드 기반, 웹형, 온프레미스형), 용도별(환자와의 소통 및 참여 유도, 예약 및 일정 관리 등), 최종 사용자별(치과, 병원 및 전문 의료 센터 등), 진료 규모별(개인 개원, 소규모 그룹 진료 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 치과용 소프트웨어 시장 동향 및 인사이트

워크플로우 자동화를 통해 진료 규모와 관계없이 관리상의 부담이 줄어듭니다.

미국의 치과 소프트웨어 시장은 진료소가 인력 부족과 이익률에 대한 압박이 커지는 가운데 더 많은 업무를 처리하려는 추세에 힘입어 자동화 수요가 증가하는 혜택을 누리고 있습니다. VideaHealth사는 2026년 1월에 출시한 'AutoVerify'에 따라 진료소를 350개 이상의 보험사와 연계하여 주당 최대 40시간의 업무 시간을 절감하고, 보험금 지급 처리를 40% 가속화하며, 청구 거절률을 50% 줄였습니다고 밝혔습니다. 이는 워크플로우 도구가 일상적인 경영 상황을 변화시킬 수 있다는 명확한 증거를 구매자에게 보여주고 있습니다. 이 점이 중요한 이유는 많은 치과 병원이 더 이상 자동화를 단순한 편의성 향상으로만 여기지 않고, 접수 업무에 소요되는 시간을 빼앗는 반복적인 작업을 줄이기 위해 활용하고 있기 때문입니다. 이와 같은 사고방식은 청구서 심사, 피보험자 자격 확인, 알림 발송 분야로도 확대되고 있으며, 이러한 분야에서는 오류나 지연이 단순한 추가 업무에 그치지 않고 수익 손실로 이어집니다. 그 결과, 미국의 치과 소프트웨어 시장에서는 직원의 근무 시간, 결제 속도, 진료 기록 확보 측면에서 직접적인 비용 절감 효과를 입증할 수 있는 제품에 대한 수요가 증가하고 있습니다.

클라우드 전환에 따라 진료소의 경영 모델은 더욱 유연한 운영 형태로 변화하고 있습니다.

미국의 치과 소프트웨어 시장은 여러 지점에서의 보고서 작성, 자동 업데이트, 원격 접속이 선택적 기능이 아닌 기본적인 운영 요구 사항으로 자리 잡아가고 있는 만큼, 꾸준히 클라우드 인프라로 전환되고 있습니다. 헨리 샤인 왕은 2026년 3월, 신규 개원하는 치과, 성장 중인 그룹 및 엔터프라이즈 규모의 DSO(치과 서비스 조직)에 단일 클라우드 플랫폼 구조를 통해 서비스를 제공하기 위해 단계적인 'Dentrix Ascend' 패키지를 도입했습니다. 이는 공급업체가 제품 설계를 치과 병원의 규모에 맞추어 조정하고 있음을 보여줍니다. 2026년 4월, 헨리 샤인 왕은 'Dentrix Ascend MCP' 레이어를 AI 에이전트 및 사용자 지정 워크플로 빌더에서도 사용할 수 있도록 했습니다. 이는 클라우드 플랫폼이 별도의 데이터 커넥터 없이도 새로운 도구를 지원할 수 있는 운영 환경으로 발전하고 있음을 보여줍니다. 이러한 변화는 DSO에게 특히 중요합니다. 표준화된 클라우드 시스템을 통해 지점 간 편차가 줄어들고, 새로 인수한 지점을 단일 워크플로우로 통합하기가 쉬워지기 때문입니다. 따라서 미국의 치과 소프트웨어 시장에서는 현장의 IT 부담을 줄여주면서도 통합된 가시성과 명확한 업그레이드 경로를 모두 갖춘 공급업체가 높이 평가받고 있습니다.

HIPAA, HITECH 및 주 정부의 개인정보 보호 규정 준수는 소규모 치과에 과도한 부담을 주고 있습니다.

미국의 치과 소프트웨어 시장은 여전히, 소규모 치과 병원이 대규모 관리 인프라에 부담을 분산시킬 수 없는 규정 준수 및 보안 요건으로 인한 저항에 직면해 있습니다. 개인 개업이나 소규모 그룹 형태의 치과 병원은 대규모 조직과 동일한 문서 관리, 접근 제어, 감사 요건을 부과받는 경우가 많지만, 이에 상응하는 내부 IT 지원이나 구매력을 갖추고 있지는 않습니다. 이러한 비용 압박으로 인해, 보안, 사용자 권한, 감사 로그 및 청구 관련 관리 기능을 핵심 구독의 일부로 제공할 수 있는 공급업체를 선택하는 구매자가 늘고 있습니다. 주별 개인정보 보호 규제는 또 다른 과제를 안겨주고 있습니다. 여러 주에 걸쳐 활동하는 그룹은 각 거점에서 개별적으로 수작업할 필요 없이, 서로 다른 법적 환경에서도 운영할 수 있는 도구가 필요하기 때문입니다. 이 때문에 미국 치과용 소프트웨어 시장에서는 레거시 시스템보다 최신 플랫폼을 도입해야 한다는 근거가 점점 더 설득력을 얻고 있음에도 불구하고, 일부 구매 결정이 지연되고 있는 상황입니다.

부문별 분석

2025년 기준으로 클라우드 기반 도입은 미국 치과 소프트웨어 시장 규모의 58.31%를 차지했으며, 2026-2031년 연평균 성장률(CAGR) 11.38%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 도입 형태이기도 합니다. 이러한 우위는 확대되는 진료 네트워크 전반에 걸쳐 일원화된 관리, 원격 접속, 그리고 업데이트의 용이화를 향한 미국 치과 소프트웨어 시장의 더 깊은 변화를 반영하고 있습니다. 클라우드 시스템은 로컬 서버에 대한 의존도를 해소하고, 여러 거점에 걸친 보고서 작성을 용이하게 하므로, 독립 치과와 DSO(치과 진료소 운영 조직) 모두의 요구 사항에 적합합니다. 또한, 벤더 입장에서는 로컬 하드웨어의 변경을 기다릴 필요 없이 새로운 청구, 워크플로우, AI 기능을 신속하게 출시할 수 있는 방안도 제공합니다.

헨리 샤인 왕이 2026년 3월에 'Dentrix Ascend'의 'Essentials', 'Pro', 'Accelerate' 각 패키지를 출시한 것은 클라우드 벤더가 계층형 설계를 활용하여 개원 초기 단계부터 대규모 DSO에 이르기까지 모든 진료소의 단계를 아우르고 있음을 보여줍니다. 2026년 4월, 이 회사는 'Dentrix Ascend MCP' 레이어를 AI 에이전트 및 맞춤형 워크플로우 개발에 개방함으로써, 이 제품은 단순한 소프트웨어 접근 수단에서 더 광범위한 플랫폼으로서의 역할로 진화했습니다. 웹 기반 제품은 서버 기반 도구에 비해 접근성을 높이기 때문에 미국 치과 소프트웨어 업계에서 여전히 중간 위치를 차지하고 있지만, 클라우드 네이티브 제품과 동등한 다중 지점 관리 기능이나 네이티브 AI 지원 기능을 항상 제공하는 것은 아닙니다. 온프레미스형 플랫폼은 영상 진단 및 청구 처리와의 연동 기능이 내장된 유서 깊은 그룹에서는 여전히 사용되고 있지만, 구매자들이 일원화된 관리와 손쉬운 통합을 더욱 중요시하게 되면서 그 입지는 점차 약화되고 있습니다.

2025년에는 예약 관리와 일정 관리가 26.24%로 가장 큰 용도 점유율을 차지한 것으로 평가되었으며, 환자 흐름, 진료 의자 가동률, 접수 처리 능력 모두가 여기서 시작되기 때문에 미국 치과 소프트웨어 시장에서 계속해서 중심적인 위치를 차지하고 있습니다. 예약 관리는 알림, 취소 후 조치, 생산 계획 지원을 수행하게 되면서 단순한 일정 관리 이상의 역할을 하게 되었습니다. Planet DDS는 『2026년 치과 업계 전망』 보고서에서 8,500개 이상의 치과에서 수집한 데이터를 바탕으로, 예약 취소율이 전년 대비 17% 감소했으며, 노쇼율도 마찬가지로 감소했다고 보고했습니다. 이는 이러한 도구들이 일상 업무 성과에 있어 얼마나 중요한지를 입증하는 것입니다. 미국의 치과 소프트웨어 시장에서 이로 인해 예약 관리는 소프트웨어가 명확한 수익 창출로 직결되는 가장 두드러진 기능 중 하나가 되었습니다.

환자와의 소통 및 참여는 2031년까지 연평균 성장률(CAGR) 12.52%를 나타낼 것으로 예측되며, 이는 용도 부문 중 가장 높은 성장률입니다. 이는 환자들이 다른 서비스 분야와 동등한 수준의 디지털 편의성을 기대하게 되었기 때문입니다. Planet DDS는 2026년 1월, Denticon에 원활하게 통합된 환자 경험 레이어로 'MyTooth'를 출시했습니다. 이 도구는 예약 및 초진 등록 데이터를 실시간으로 진료 관리 시스템에 반영합니다. 청구, 결제 처리, 치료 계획은 여전히 필수적이지만, 성장의 초점은 진료 전후의 불편함을 줄여주는 도구로 옮겨가고 있습니다. 환자의 재방문율과 의사소통의 질이 진료소의 효율성과 치료 수용률 모두에 영향을 미치게 되면서, 이러한 추세는 미국 치과 소프트웨어 업계에서 더욱 두드러지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the united states dental software market size is projected to be USD 2.62 billion in 2025, USD 2.86 billion in 2026, and reach USD 4.42 billion by 2031, growing at a CAGR of 9.12% from 2026 to 2031.

This report is Segmented by Deployment Mode (Cloud-Based, Web-Based, On-Premise), Application (Patient Communication & Engagement, Appointment Scheduling & Calendar, and More), End User (Dental Clinics, Hospitals & Specialty Centers, and More), and Practice Size (Solo Practices, Small Group Practices, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Dental Software Market Trends and Insights

Workflow Automation Reduces Administrative Overhead Across Practice Sizes

The United States dental software market is benefiting from a stronger automation case as practices try to do more with tighter staffing and more pressure on margins. VideaHealth stated that its AutoVerify launch in January 2026 connected practices to 350+ payers, saved up to 40 hours per week, accelerated reimbursements by 40%, and reduced claim denials by 50%, which gives buyers clear proof that workflow tools can change daily economics. This matters because many practices are no longer looking at automation as a convenience layer, and are instead using it to reduce repetitive tasks that absorb front-desk time. The same logic is spreading into claim review, eligibility checks, and reminders, where errors and delays create lost revenue rather than only extra work. As a result, the United States dental software market is seeing stronger demand for products that can document direct savings in staff time, payment speed, and production capture.

Cloud Migration Shifts Practice Economics Toward More Flexible Operating Models

The United States dental software market is moving steadily toward cloud infrastructure because multi-site reporting, automatic updates, and remote access are becoming basic operating needs rather than optional features. Henry Schein One introduced tiered Dentrix Ascend packaging in March 2026 to serve de novo practices, growing groups, and enterprise DSOs through a single cloud platform structure, which shows how vendors are aligning product design with practice scale. In April 2026, Henry Schein One also opened the Dentrix Ascend MCP layer to AI agents and custom workflow builders, which shows that cloud platforms are developing into operating environments that can support new tools without separate data connectors. This shift is especially important for DSOs because standardized cloud systems reduce variation across locations and make newly acquired sites easier to bring onto one workflow. The United States dental software market is therefore rewarding vendors that can combine lower local IT burden with centralized visibility and a clear upgrade path.

HIPAA, HITECH, and State Privacy Compliance Disproportionately Burden Smaller Practices

The United States dental software market still faces resistance from compliance and security demands that smaller practices cannot spread across a large administrative base. Solo and small-group offices often carry the same documentation, access control, and audit expectations as larger organizations, but they do not have the same internal IT support or purchasing leverage. That cost pressure is pushing more buyers toward vendors that can present security, user permissions, audit logs, and claims-related controls as part of the core subscription. State-specific privacy rules add another layer because multi-state groups need tools that can operate across different legal settings without separate manual work at every location. This slows some buying decisions in the United States dental software market, even though it also strengthens the case for modern platforms over legacy systems.

Other drivers and restraints analyzed in the detailed report include:

- AI-Assisted Scheduling, Billing, and Analytics Create Clear Performance Separation

- DSO Consolidation Reshapes Technology Procurement Across the Value Chain

- Legacy Migration Friction Delays Adoption but Does Not Stop It

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment held 58.31% of the United States dental software market size in 2025, and it is also the fastest-growing deployment mode with an 11.38% CAGR from 2026 to 2031. The lead reflects a deeper shift in the United States dental software market toward centralized administration, remote access, and easier updates across growing practice networks. Cloud systems fit the needs of both independent practices and DSOs because they remove local server dependence and make reporting easier across more than 1 site. They also give vendors a faster path to release new billing, workflow, and AI features without waiting for local hardware changes.

Henry Schein One's March 2026 Dentrix Ascend rollout with Essentials, Pro, and Accelerate packaging showed how cloud vendors are using tiered design to cover every practice stage from startup to large DSO. In April 2026, the company opened the Dentrix Ascend MCP layer to AI agents and custom workflow development, which moved the product beyond software access and into a broader platform role. Web-based products still occupy a middle position in the United States dental software industry because they improve access compared with server-based tools, but they do not always offer the same depth of multi-site control or native AI readiness as cloud-native products. On-premise platforms remain present in established groups with embedded imaging and billing links, yet their position is weakening as buyers place more value on centralized management and easier integration.

Appointment scheduling and calendar management held the largest application share at 26.24% in 2025, which keeps it at the center of the United States dental software market because patient flow, chair utilization, and front-desk throughput all start there. Scheduling has become more than calendar administration because it now supports reminders, cancellation recovery, and production planning. Planet DDS said in its 2026 Dental Industry Outlook that cancellations fell 17% and no-show rates also declined year over year across data drawn from 8,500+ practices, which reinforces how central these tools are to day-to-day performance. In the United States dental software market, that makes scheduling one of the clearest functions where software can be linked to visible revenue capture.

Patient communication and engagement is projected to grow at a 12.52% CAGR through 2031, the fastest rate among application segments, because patients now expect digital convenience that matches other service categories. Planet DDS launched MyTooth in January 2026 as a native Denticon patient experience layer that writes booking and intake data back into the live practice management environment in real time. Billing, payment processing, and treatment planning remain essential, but growth is shifting toward tools that reduce friction before and after the clinical visit. That pattern is strengthening in the United States dental software industry because patient retention and communication quality now affect both practice efficiency and treatment acceptance.

Complete Report Scope:

- By Deployment Mode

- Cloud-Based

- Web-Based

- On-Premise

- By Application

- Patient Communication & Engagement

- Appointment Scheduling & Calendar

- Billing & Invoicing

- Payment Processing

- Treatment Planning & Charting

- Imaging & Diagnostics Integration

- Other Applications

- By End User

- Dental Clinics

- Hospitals & Specialty Centers

- Dental Service Organizations

- Other End Users

- By Practice Size

- Solo Practices

- Small Group Practices

- Mid-Market Multi-site Practices

- Large DSOs / Enterprise Chains

List of Companies Covered in this Report:

- CareStack

- Carestream Dental

- Curve Dental

- Dental Intelligence

- DentiMax

- Henry Schein One

- iDentalSoft

- MacPractice

- NexHealth

- NextGen Healthcare

- Open Dental Software

- Patterson Dental

- Planet DDS

- Practice-Web

- Solutionreach

- tab32

- VideaHealth

- YAPI

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Workflow Automation Demand in Busy Practices

- 4.2.2 Cloud Migration to Reduce Server Overhead

- 4.2.3 AI-Assisted Scheduling, Billing, and Analytics

- 4.2.4 DSO Consolidation and Standardization

- 4.2.5 Interoperability Pressure Across Imaging, Claims, and EHRs

- 4.2.6 Teledentistry and Digital Patient Engagement Expectations

- 4.3 Market Restraints

- 4.3.1 HIPAA, HITECH, and State Privacy Compliance Cost

- 4.3.2 Legacy Migration and Vendor Lock-in Friction

- 4.3.3 Upfront Software, Implementation, and Training Costs

- 4.3.4 Sparse Dental IT Support in Smaller Practices

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 Web-Based

- 5.1.3 On-Premise

- 5.2 By Application

- 5.2.1 Patient Communication & Engagement

- 5.2.2 Appointment Scheduling & Calendar

- 5.2.3 Billing & Invoicing

- 5.2.4 Payment Processing

- 5.2.5 Treatment Planning & Charting

- 5.2.6 Imaging & Diagnostics Integration

- 5.2.7 Other Applications

- 5.3 By End User

- 5.3.1 Dental Clinics

- 5.3.2 Hospitals & Specialty Centers

- 5.3.3 Dental Service Organizations

- 5.3.4 Other End Users

- 5.4 By Practice Size

- 5.4.1 Solo Practices

- 5.4.2 Small Group Practices

- 5.4.3 Mid-Market Multi-site Practices

- 5.4.4 Large DSOs / Enterprise Chains

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 CareStack

- 6.3.2 Carestream Dental

- 6.3.3 Curve Dental

- 6.3.4 Dental Intelligence

- 6.3.5 DentiMax

- 6.3.6 Henry Schein One

- 6.3.7 iDentalSoft

- 6.3.8 MacPractice

- 6.3.9 NexHealth

- 6.3.10 NextGen Healthcare

- 6.3.11 Open Dental Software

- 6.3.12 Patterson Dental

- 6.3.13 Planet DDS

- 6.3.14 Practice-Web

- 6.3.15 Solutionreach

- 6.3.16 tab32

- 6.3.17 VideaHealth

- 6.3.18 YAPI

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment