|

시장보고서

상품코드

2072723

미국의 카프노그래피 장비 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Capnography Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

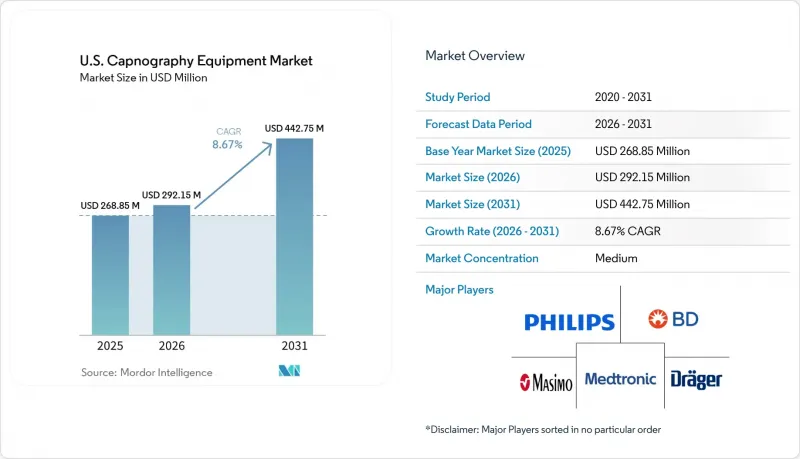

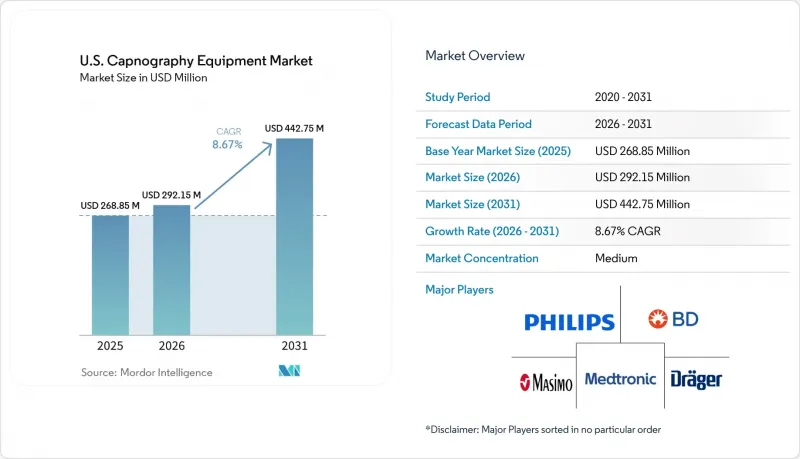

Mordor Intelligence에 의하면, 미국의 카프노그래피 장비 시장 규모는 2025년 2억 6,885만 달러로 평가되었고, 2026년에는 2억 9,215만 달러로 추정되고, 2031년까지 4억 4,275만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 8.67%로 성장할 전망입니다.

본 보고서는 제품 유형별(다중 매개변수, 독립형, 휴대용), 구성 요소별(기기, 부속품, 소모품, 소프트웨어), 기술별(메인스트림, 사이드스트림, 마이크로스트림), 용도별(마취, 중환자 치료, 응급 의료, 진정, 호흡기), 최종 사용자별(병원, 외래수술센터(ASC), 재택치료)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 카프노그래피 장비 시장 동향 및 인사이트

COPD 및 기타 만성 호흡기 질환으로 인한 부담 증가

미국의 카프노그래피 장비 시장은 만성 폐쇄성 폐질환(COPD) 및 관련 호흡기 질환의 임상적 부담이 증가함에 따라 호조를 보이고 있습니다. 2024년, 미국의 연령 조정 COPD 유병률은 3.8%였으며, 75세 이상 성인의 경우 10.5%, 65-74세의 경우 8.9%로 더 높은 유병률을 보였습니다. 약 1,170만 명의 보험 가입자가 COPD 진단을 받았으며, 이에 따라 180만 건의 COPD 관련 급성기 입원이 발생했습니다. 지역 간 격차 측면에서 보면, 서부(3.1%)에 비해 남부 및 중서부(4.2%)의 유병률이 높아, 지역 병원 및 지방 의료 시스템과 견고한 네트워크를 구축한 공급업체들에게 비즈니스 기회가 되고 있습니다. 또한, 외래 진료 및 재택치료로의 전환이 진행되고 있는 점도 카프노그래피 장비에 대한 지속적인 수요를 더욱 뒷받침하고 있습니다.

마취 및 시술 현장에서의 카프노그래피 활용 확대

마취 모니터링은 미국 내 카프노그래피 장비 시장의 주요 성장 동력으로 자리매김하고 있으며, 2025년에는 용도별 매출의 34.77%를 차지한 것으로 평가되었습니다. 수술실이 주요 수요처인 한편, 회복실의 업무 흐름이나 중등도의 진정 상태가 필요한 시술실 등으로 수요가 확대되고 있습니다. 전신 마취 및 기도 확보에 관한 기준에 따라, 호기 말 이산화탄소 모니터링의 중요성이 더욱 강조되고 있습니다. 또한, 소화기내과 전문의, 호흡기내과 전문의, 방사선과 전문의, 응급의학과 전문의들이 카프노그래피를 도입하는 추세가 확산되면서 수요가 증가하고 있으며, 이는 다양한 전문 분야에 걸친 판매 역량을 갖춘 공급업체에 유리하게 작용하고 있습니다.

초기 투자 비용과 소모품에 대한 지속적인 부담

미국의 카프노그래피 장비 시장은 초기 하드웨어 투자와 지속적인 소모품 구매에 의존하는 비즈니스 모델이기 때문에 상업적인 과제에 직면해 있습니다. Microstream™ 필터 라인이나 NomoLine 샘플링 세트와 같은 공급업체별 전용 액세서리는 초기 장비 구입 비용에 더해 총 소유 비용을 증가시킵니다. 이로 인해 대규모 의료기관에 비해 장비 교체나 지속적인 소모품 비용 관리에 어려움을 겪고 있는 지방 병원이나 소규모 시설에서는 여러 가지 문제가 발생하고 있습니다. 수술실 밖에서는 직접 청구 경로가 제한되어 있고, 사례별로 승인이 필요한 미등재 코드 94799에 의존해야 한다는 점이 도입을 더욱 복잡하게 만들고 있습니다. 게다가, 교육 및 알람 관리가 운영상의 부담이 되어, 비용에 민감한 환경에서의 도입을 지연시키고 있습니다.

부문별 분석

2025년에는 독립형 카프노미터가 매출의 52.35%를 차지했으며, 미국 카프노그래피 장비 시장에서 주도적인 위치를 유지했습니다. 이러한 우위는 파형의 가시성, 안정적인 성능, 모니터와의 호환성이 극히 중요한 수술실, 중환자실, 응급실 등에서 폭넓게 활용되고 있다는 점에 기인합니다. 병원 측은 기존 모니터링 시스템과의 원활한 통합이 가능하고 상호 운용성에 대한 우려가 최소화되기 때문에 이러한 장비를 선호하여 도입하고 있습니다.

휴대용 카프노그래피 장비는 2031년까지 연평균 성장률(CAGR) 9.65%를 기록하며 성장할 것으로 예상되며, 미국 카프노그래피 장비 시장에서 가장 빠르게 성장하는 부문이 될 전망입니다. 이러한 성장은 응급의료서비스(EMS)를 통한 조달, 외래 수술에서의 활용, 그리고 재택 간호에서의 지속적인 호흡 모니터링 도입과 관련이 있습니다. 휴대성이 향상되고 일회용 설계가 더욱 사용자 친화적으로 변함에 따라, 관리 프로토콜이 이러한 발전에 얼마나 신속하게 적응할 수 있을지가 주목받고 있습니다.

2025년에는 기기가 구성 요소별 매출의 45.65%를 차지했으며, 미국 카프노그래피 장비 시장에서 기기 본체 구매가 얼마나 중요한지 여실히 드러났습니다. 독립형 및 다중 매개변수형 기기가 주류를 이루며, 병원 및 시술 현장에서 모니터링의 핵심을 이루고 있습니다. 소프트웨어와 연결 모듈은 보다 광범위한 환자 모니터링 시스템과의 통합에서 중요한 역할을 수행하고 있기 때문에 구매 결정에 점점 더 큰 영향을 미치고 있습니다.

소모품 시장은 2031년까지 연평균 성장률(CAGR) 9.55%를 기록하며 성장할 것으로 예상되며, 구성 요소 중 가장 빠르게 성장하는 부문이 될 전망입니다. 이러한 성장은 병원, 응급실, 외래 진료 시설에서의 도입 대수 증가를 반영하고 있으며, 비강 캐뉼라, 샘플링 라인, 기도 어댑터에 대한 수요를 견인하고 있습니다. 지속적인 액세서리 수요는 이익률과 고객 유지에 큰 영향을 미치며, 시장에서 하드웨어의 역할을 보완하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the u.S. capnography equipment market size is expected to increase from USD 268.85 million in 2025 to USD 292.15 million in 2026 and reach USD 442.75 million by 2031, growing at a CAGR of 8.67% over 2026-2031.

This report is Segmented by Product Type (Multiparameter, Standalone, Handheld), Component (Equipment, Accessories, Consumables, and Software), Technology (Mainstream, Sidestream, Microstream), Application (Anesthesia, Critical Care, Emergency Medicine, Sedation, and Respiratory), and End User (Hospitals, Ascs, and Home Healthcare). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Capnography Equipment Market Trends and Insights

Rising Burden of COPD and Other Chronic Respiratory Conditions

The United States capnography equipment market benefits from the growing clinical burden of COPD and related respiratory disorders. In 2024, the age-adjusted COPD prevalence rate in the United States was 3.8%, with higher rates of 10.5% among adults aged 75 and older and 8.9% among those aged 65-74. Approximately 11.7 million insured individuals had a COPD diagnosis, leading to 1.8 million COPD-related acute inpatient hospitalizations. Regional disparities show higher prevalence in the South and Midwest (4.2%) compared to the West (3.1%), creating opportunities for suppliers with strong community hospital and rural system networks. The shift toward ambulatory and home settings further supports sustained demand for capnography equipment.

Higher Use of Capnography in Anesthesia and Procedural Settings

Anesthesia monitoring remains a key driver in the United States capnography equipment market, contributing 34.77% of application revenue in 2025. While operating rooms are the primary demand center, growth is expanding into recovery workflows and procedural areas requiring moderate sedation. Standards for general anesthesia and airway confirmation reinforce the importance of end-tidal carbon dioxide monitoring. Additionally, the adoption of capnography by gastroenterologists, pulmonologists, radiologists, and emergency physicians broadens its demand, favoring vendors with multispecialty sales capabilities.

Capital Cost and Recurring Consumables Burden

The United States capnography equipment market faces a commercial challenge as its model relies on upfront hardware investments and recurring disposable purchases. Vendor-specific accessories like Microstream(TM) filter lines and NomoLine sampling sets increase the total cost of ownership beyond the initial device purchase. This creates difficulties for rural hospitals and smaller facilities, which struggle to manage fleet upgrades and ongoing consumable costs compared to larger systems. Outside the operating room, limited direct billing pathways and reliance on the unlisted 94799 code, which requires case-by-case approval, further complicate adoption. Additionally, training and alarm management add operational burdens, slowing deployment in cost-sensitive settings.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Emergency and Critical Care Monitoring

- Migration Toward Portable and Workflow-Integrated Monitors

- Reimbursement and Billing Friction in Non-Acute Care Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standalone capnometers accounted for 52.35% of revenue in 2025, maintaining their leadership in the United States capnography equipment market. Their dominance is driven by extensive use in operating rooms, intensive care units, and emergency departments, where waveform visibility, stable performance, and monitor compatibility are critical. Hospitals prefer these devices for their seamless integration into existing monitoring systems and minimal interoperability concerns.

Handheld capnography devices are projected to grow at a 9.65% CAGR through 2031, making them the fastest-growing segment in the United States capnography equipment market. Their growth is linked to EMS procurement, ambulatory surgery use, and the adoption of continuous respiratory monitoring in home care. As portability improves and disposable designs become more user-friendly, the focus is shifting to how quickly care protocols will adapt to these advancements.

Equipment contributed 45.65% of component revenue in 2025, highlighting the importance of capital device purchases in the United States capnography equipment market. Standalone and multiparameter devices dominate, forming the core monitoring footprint in hospitals and procedural settings. Software and connectivity modules are increasingly influencing purchasing decisions due to their role in integrating with broader patient monitoring systems.

Consumables are expected to grow at a 9.55% CAGR through 2031, making them the fastest-growing component category. This growth reflects the rising installed base in hospitals, emergency departments, and ambulatory sites, driving demand for nasal cannulas, sampling lines, and airway adapters. Recurring accessory demand significantly impacts margins and customer retention, complementing the role of hardware in the market.

Complete Report Scope:

- By Product Type

- Multiparameter Capnometers

- Standalone Capnometers

- Handheld Capnography Devices

- By Component

- Equipment

- Capnometers

- Monitors

- Accessories and Consumables

- Nasal Cannulas

- Sampling Lines

- Airway Adapters and Related Consumables

- Software and Connectivity

- By Technology

- Mainstream Capnography

- Sidestream Capnography

- Microstream Capnography

- By Application

- Anesthesia Monitoring

- Critical Care Monitoring

- Emergency Medicine

- Procedural Sedation

- Pain Management

- Respiratory Monitoring

- Other Applications

- By End User

- Hospitals and Clinics

- Ambulatory Surgery Centers

- Home Healthcare Settings

- Other End Users

List of Companies Covered in this Report:

- Avante Health Solutions, LLC

- Baxter

- Beckton Dickinson

- Criticare Technologies, Inc.

- Dragerwerk AG and Co. KGaA

- EDAN Instruments, Inc.

- GE HealthCare Technologies Inc.

- Hamilton Medical

- ICU Medical

- Infinium Medical

- Koninklijke Philips

- Masimo

- Medtronic

- Mindray

- Nihon Kohden

- Nonin Medical

- Smiths Group

- Spacelabs Healthcare, LLC

- Vyaire Medical

- Zoll Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of COPD and Other Chronic Respiratory Conditions

- 4.2.2 Higher Use of Capnography in Anesthesia and Procedural Sedation

- 4.2.3 Expansion of Emergency and Critical Care Monitoring Protocols

- 4.2.4 Migration Toward Portable and Workflow-Integrated Monitoring Systems

- 4.2.5 Greater Focus on Early Detection of Hypoventilation and Patient Safety

- 4.2.6 Increasing Adoption of Capnography in Non-Operating Room Settings

- 4.3 Market Restraints

- 4.3.1 Capital Cost and Recurring Consumables Burden

- 4.3.2 Reimbursement and Billing Friction in Non-Acute Settings

- 4.3.3 Staff Training and Alarm-Management Requirements

- 4.3.4 Device Integration Challenges Across Mixed-Vendor Hospital Estates

- 4.4 Value Chain Analysis

- 4.5 Supply Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Product Type

- 5.1.1 Multiparameter Capnometers

- 5.1.2 Standalone Capnometers

- 5.1.3 Handheld Capnography Devices

- 5.2 By Component

- 5.2.1 Equipment

- 5.2.2 Capnometers

- 5.2.3 Monitors

- 5.2.4 Accessories and Consumables

- 5.2.5 Nasal Cannulas

- 5.2.6 Sampling Lines

- 5.2.7 Airway Adapters and Related Consumables

- 5.2.8 Software and Connectivity

- 5.3 By Technology

- 5.3.1 Mainstream Capnography

- 5.3.2 Sidestream Capnography

- 5.3.3 Microstream Capnography

- 5.4 By Application

- 5.4.1 Anesthesia Monitoring

- 5.4.2 Critical Care Monitoring

- 5.4.3 Emergency Medicine

- 5.4.4 Procedural Sedation

- 5.4.5 Pain Management

- 5.4.6 Respiratory Monitoring

- 5.4.7 Other Applications

- 5.5 By End User

- 5.5.1 Hospitals and Clinics

- 5.5.2 Ambulatory Surgery Centers

- 5.5.3 Home Healthcare Settings

- 5.5.4 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Avante Health Solutions, LLC

- 6.3.2 Baxter International Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Criticare Technologies, Inc.

- 6.3.5 Dragerwerk AG and Co. KGaA

- 6.3.6 EDAN Instruments, Inc.

- 6.3.7 GE HealthCare Technologies Inc.

- 6.3.8 Hamilton Medical AG

- 6.3.9 ICU Medical, Inc.

- 6.3.10 Infinium Medical, Inc.

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Masimo Corporation

- 6.3.13 Medtronic plc

- 6.3.14 Mindray Medical International Limited

- 6.3.15 Nihon Kohden Corporation

- 6.3.16 Nonin Medical, Inc.

- 6.3.17 Smiths Group plc

- 6.3.18 Spacelabs Healthcare, LLC

- 6.3.19 Vyaire Medical, Inc.

- 6.3.20 ZOLL Medical Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment