|

시장보고서

상품코드

2072734

미국의 수의 진단 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Veterinary Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

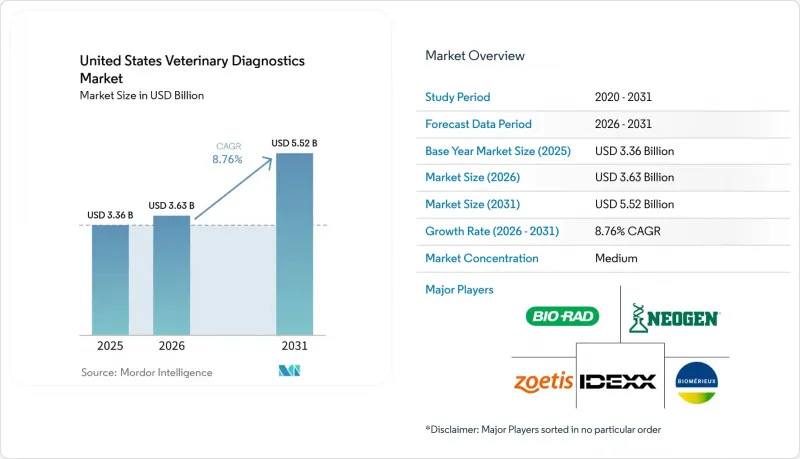

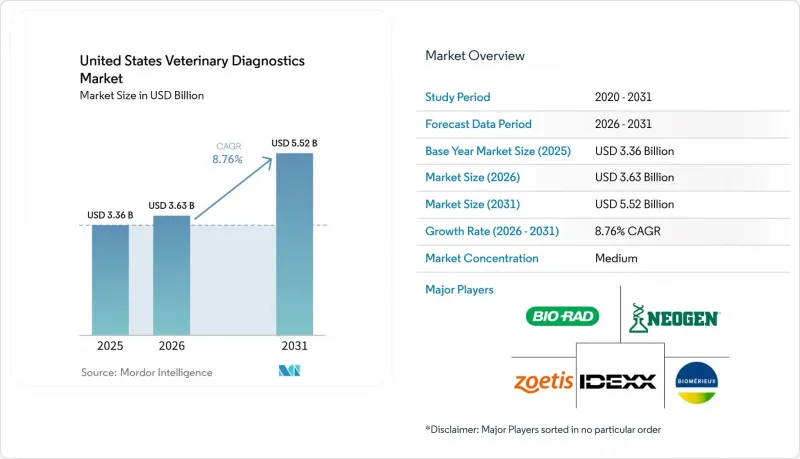

Mordor Intelligence에 의하면, 미국의 수의 진단 시장 규모는 2025년에 33억 6,000만 달러로 평가되었고, 2026년에 36억 3,000만 달러로 추정되고, 2031년까지 55억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 8.76%로 성장할 전망입니다.

본 보고서는 제품별(소모품 및 시약, 기기), 기술별(면역진단, 생화학, 분자진단, 혈액학, 소변검사, 기타), 동물 유형별(반려동물, 가축), 용도별(감염병, 내분비학, 순환기학, 종양학, 기타), 최종 사용자별(참조 실험실, 병원 및 클리닉, POC 및 병원 내 검사, 연구 기관)로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

미국의 수의 진단 시장 동향 및 인사이트

증가하는 반려동물의 의료비

2024년, 미국의 반려동물 보험 가입률은 반려동물 총 수의 3.9%에 달했으며, 640만 마리의 개와 고양이가 보험 적용 대상이 되었습니다. 한편, 총 보험료 수입은 47억 4,000만 달러를 넘어 전년 대비 21.4% 증가했습니다. 그럼에도 불구하고, 대부분의 반려동물은 여전히 정식 보험 적용 대상에서 제외되어 있으며, 이는 미국의 수의 진단 시장에서 프리미엄 패널의 도입이 본인 부담금 상한선이라는 큰 장벽에 계속해서 직면하고 있음을 의미합니다. 반면, 보험에 가입한 가구는 사고나 질병에 대한 보상 플랜이 임상 평가와 관련된 검사 비용을 일반적으로 보장하고 있기 때문에 보다 상세한 진단 검사를 받기 쉬워졌습니다. '반려동물 보험 모델법'을 통한 주 차원의 기준 설정은 보험 계약의 일관성을 보다 광범위하게 확보하고, 예측 기간 동안 보험의 보급 확대를 촉진할 것으로 기대됩니다. 그 결과, 미국의 수의 진단 시장 전체에서 보험 적용을 받는 진료의 경우 진단 검사가 더욱 중요시되는 반면, 보험에 가입하지 않은 환자의 진료에서는 여전히 가격에 대한 민감도가 높은 것으로 나타났습니다.

병원 내 검사 및 현장 검사 확대

미국의 수의 진단 시장에서는 소형 분석 장비가 일반 병원은 물론 소규모 이동 진료 모델에도 적합해짐에 따라, 병원 내 검사의 성장이 가속화되고 있습니다. Zomedica사의 TRUFORMA 플랫폼은 이러한 변화를 명확히 보여주고 있으며, 이 시스템은 공간이 제한된 진료소나 이동 진료 현장에서도 사용할 수 있는 컴팩트한 형태로 내분비 검사를 제공할 수 있도록 설계되었습니다. 포인트 오브 케어(POC) 시스템을 도입하는 진료소가 늘어남에 따라, 수익 구조는 일회성 하드웨어 판매에서 지속적인 소모품 수요로 전환되고 있습니다. 이 점은 중요합니다. 이는 현장 진단 및 병원 내 검사가 미국 수의 진단 시장에서 가장 빠르게 성장하고 있는 최종 사용자 채널이며, 2031년까지 10.2%의 성장이 예상되기 때문입니다. 더 광범위한 영향으로, 특히 당일 진료 시 임상적 판단이 가장 중요한 상황에서 병원 내 검사의 신속한 결과 보고가 일상적인 진료의 일부로 자리 잡아가고 있습니다.

수의사 및 검사 기사의 만성적인 부족

미국의 수의 진단 시장은 지난 10년 동안 반려동물을 담당하는 수의사의 수는 증가한 반면, 혼합동물 및 농업 분야 수의사의 수는 감소함에 따라, 식용 동물 관리 서비스의 격차가 확대되어 계속해서 공급 제약에 직면하고 있습니다. 또한, 2025년에는 미국 농무부 동식물검역국(USDA APHIS)이 1,300명 이상의 직원을 감원했으며, 주요 동물 질병 검사 연구소 직원의 20%에서 30%가 감축된 것으로 보고되어 연방 정부의 대응 능력도 약화되었습니다. 따라서 미국의 수의 진단 시장에서는 검체 채취, 분석 및 후속 조치가 여전히 수의사에 의존하고 있음에도 불구하고, 감염병 발생 시에는 민간 검사 기관이 대응 부담을 더 많이 떠안게 됩니다. 또한, 세포진단, 조직병리학 및 전문적인 검사 워크플로는 아직 상업적 규모에서 완전한 자동화가 실현되지 않았기 때문에 검사 기술자 부족이 또 다른 병목 현상으로 대두되고 있습니다. 이러한 압박은 검사 수요는 있음에도 불구하고, 지역 진료 체계가 너무 취약하여 그 수요 전부를 안정적인 수익으로 연결할 수 없는 지방의 축산 지역에서 가장 크게 느껴지고 있습니다.

부문별 분석

2025년, 소모품, 키트, 시약은 미국 수의 진단 시장 점유율의 46.27%를 차지했으며, 매출 기준 최대 제품 카테고리가 되었습니다. 이러한 위상은 미국 수의 진단 업계에서 분석 장비가 성공적으로 도입될 때마다 분석 카트리지, 슬라이드, 시약, 검사 키트와 같은 소모품에 대한 지속적인 수요가 발생한다는 특성을 반영하고 있습니다. 동물병원이 IDEXX Catalyst나 Zoetis Vetscan과 같은 플랫폼을 도입하면, 재주문은 임의의 구매 주기가 아닌 운영비의 안정적인 일부가 됩니다. 또한, 미국의 수의 진단 시장에서는 1회 내원당 검사 빈도가 높아지고 있는 점도 긍정적인 요인으로 작용하고 있습니다. 이는 내원 환자 수 증가세가 완만하더라도 검사의 정밀도가 높아지면 시약 사용량이 증가하기 때문입니다.

기기 시장은 2031년까지 연평균 성장률(CAGR) 9.08%를 나타낼 것으로 예측되며, 이에 따라 미국 수의 진단 시장에서 가장 빠르게 성장하는 제품 부문으로 자리매김하고 있습니다. 현재의 투자 사이클은 하드웨어 교체, AI 기반 영상 진단 시스템의 업그레이드, 그리고 설치 공간이 적은 소형 시스템에 대한 수요에 힘입어 유지되고 있습니다. IDEXX가 2026년 1월에 출시한 'ImageVue DR50 Plus'는 AI 기반 영상 진단 옵션을 추가하여 경쟁 수의학 시스템에 비해 방사선 피폭량을 최대 60%까지 줄였으며, 이는 공급업체가 차별화된 하드웨어를 활용하여 신규 도입의 타당성을 입증한 실제 사례를 보여줍니다. 기업 그룹은 여러 거점에서 일괄 구매를 진행하기 때문에 이러한 설비 투자를 보다 수월하게 감당할 수 있지만, 독립 동물병원은 가격 협상력이 낮은데도 불구하고 유사한 경쟁 압박에 직면해 있습니다. 시간이 지남에 따라 신규 도입이 이루어질 때마다 하류 소모품에 대한 수요가 확대되고 있으며, 이에 따라 미국 수의 진단 업계의 제품 성장은 장비 교체와 정기적인 검사 이용 모두에 의해 뒷받침되고 있습니다.

2025년에는 감염증 패널, 매개성 질환 검사, 심장사상충 선별 검사, 알레르기 진단 분야의 빈번한 이용에 힘입어 면역 진단이 매출의 35.79%를 차지하며 1위를 차지했습니다. 이러한 검사 방법은 오랫동안 표준적인 건강 관리 및 질병 관리 프로토콜의 일부로 자리 잡아 왔으며, 진료소와 검사 기관 모두에서 폭넓게 도입된 실적을 바탕으로 하고 있습니다. 임상생화학 및 혈액학은 다수의 환자를 대상으로 간, 신장, 내분비 및 전혈구 계수 평가를 뒷받침하고 있기 때문에 일상적인 내과 진료에서 여전히 핵심적인 위치를 차지하고 있습니다. 이러한 안정적인 검사 체계 덕분에, 미국 수의진단 시장에 새로운 기법이 점차 도입되고 있음에도 불구하고, 성숙한 기술이 여전히 중요한 역할을 하고 있습니다.

분자진단 시장은 2031년까지 연평균 성장률(CAGR) 8.38%를 나타낼 것으로 예측되며, 가장 빠르게 성장하고 있는 기술 분야입니다. 미국 농무부(USDA)의 '전국 우유 검사 전략'에 따라 2024년 12월 연방 명령 이후, 젖소 군집 감시에서 PCR 인프라가 영구적인 역할을 맡게 되었습니다. 반려동물 분야에서는 동료 심사를 거친 검증 결과를 통해, 암 조기 발견에 있어 체액 생검 및 관련 분자진단 도구의 유효성이 입증되었습니다. 여기에는 2024년에 개를 대상으로 실시된 선별 연구에서 나타난 98.7%의 특이도도 포함됩니다. 이러한 병행 이용 사례는 단일 질환 분야나 동물 집단에 대한 의존도를 낮추는 측면에서 중요합니다. 따라서, 이러한 기술의 결합은 기존의 방식을 완전히 대체하는 것이 아니라, 미국 수의 진단 시장의 실질적인 적용 범위를 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the united states veterinary diagnostics market size is projected to be USD 3.36 billion in 2025, USD 3.63 billion in 2026, and reach USD 5.52 billion by 2031, growing at a CAGR of 8.76% from 2026 to 2031.

This report is Segmented by Product (Consumables/Reagents, Instruments), Technology (Immunodiagnostics, Biochemistry, Molecular, Hematology, Urinalysis, Others), Animal Type (Companion Animals, Livestock), Application (Infectious Diseases, Endocrinology, Cardiology, Oncology, Others), and End User (Reference Labs, Hospitals/Clinics, POC/In-House, Research Institutes). Forecasts in Value (USD).

United States Veterinary Diagnostics Market Trends and Insights

Rising Companion Animal Health Spend

Pet insurance penetration in the United States reached 3.9% of the total pet population in 2024, covering 6.4 million dogs and cats, while gross written premiums exceeded USD 4.74 billion and rose 21.4% year over year. That still leaves most pets outside formal reimbursement, which means the United States veterinary diagnostics market continues to face a meaningful out-of-pocket limit on premium panel adoption. At the same time, insured households are more able to accept deeper diagnostic workups because accident and illness plans commonly cover testing costs tied to clinical evaluation. State-level standard setting through the Pet Insurance Model Act supports broader policy consistency and should make insurance easier to scale through the forecast period. The result is a market where premium visits are becoming more diagnostics-intensive, while uninsured visits remain more price sensitive across the United States veterinary diagnostics market.

Expansion of In-Clinic and Point-of-Care Testing

The United States veterinary diagnostics market is seeing faster growth in in-clinic testing because compact analyzers now fit both standard hospitals and smaller ambulatory models. Zomedica's TRUFORMA platform shows this shift clearly, as the system is built to deliver endocrine assays in a compact format that can work in practices with limited space and in mobile settings. As more practices place point-of-care systems, the revenue profile moves beyond one-time hardware sales and toward recurring consumable pull. This is important because point-of-care and in-house testing is the fastest-growing end-user channel, with forecast growth of 10.2% through 2031 in the United States veterinary diagnostics market. The broader effect is that faster in-house turnaround is becoming part of routine care expectations, especially where same-visit clinical decisions matter most.

Persistent Veterinarian and Laboratory Technician Shortages

The United States veterinary diagnostics market continues to face a supply constraint because companion-animal veterinarian numbers rose over the past decade, while mixed-animal and agricultural veterinarian numbers moved lower, widening the service gap in food-animal care. Federal capacity also weakened in 2025 when USDA APHIS lost more than 1,300 staff members, including a reported 20% to 30% of personnel at a key animal disease testing laboratory. That leaves commercial laboratories carrying more of the response burden during outbreaks, even though the United States veterinary diagnostics market still depends on veterinarians to collect, interpret, and follow up on samples. Technician shortages add another bottleneck because cytology, histopathology, and specialized lab workflows cannot yet be fully automated at a commercial scale. The pressure is strongest in rural livestock territories, where test demand exists but local clinical capacity remains too thin to convert all of that demand into steady revenue.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Interpretation of Images and Bloodwork

- Wider Use of Molecular and Rapid Assays in Routine Practice

- High Cost of Advanced Diagnostics for Price-Sensitive Owners

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumables, kits, and reagents held 46.27% of the United States veterinary diagnostics market share in 2025, making them the largest product category by revenue. This position reflects the recurring nature of assay cartridges, slides, reagents, and test kits that follow every successful analyzer placement in the United States veterinary diagnostics industry. Once a clinic commits to a platform such as IDEXX Catalyst or Zoetis Vetscan, repeat ordering becomes a stable part of operating spend rather than a discretionary purchase cycle. The United States veterinary diagnostics market also benefits here from stronger diagnostic intensity per visit, because higher test depth lifts reagent use even when visit growth is modest.

Instruments are forecast to grow at 9.08% CAGR through 2031, which makes them the fastest-growing product segment in the United States veterinary diagnostics market. The current investment cycle is being supported by hardware replacement, AI-enabled imaging upgrades, and demand for compact systems that fit smaller footprints. IDEXX's January 2026 launch of the ImageVue DR50 Plus added an imaging option with AI support and up to 60% lower radiation exposure than competing veterinary systems, which shows how vendors are using differentiated hardware to justify new placements. Corporate groups can absorb this capital spending more easily because they buy across many sites, while independents face the same competitive pressure with less pricing leverage. Over time, each new placement expands the downstream consumables tail, which keeps product growth in the United States veterinary diagnostics industry tied to both equipment refresh and recurring test use.

Immunodiagnostics led with 35.79% of revenue in 2025, supported by high-frequency use in infectious disease panels, vector-borne disease testing, heartworm screening, and allergy diagnostics. These assays have long been part of standard wellness and disease management protocols, which gives them broad installed-base support in both clinics and reference laboratories. Clinical biochemistry and hematology remain central to routine internal medicine because they support liver, kidney, endocrine, and complete blood count evaluation across large patient volumes. That steady test mix keeps mature technologies relevant even as the United States veterinary diagnostics market adds newer methods at the margin.

Molecular diagnostics are projected to grow at 8.38% CAGR through 2031, which makes them the fastest-expanding technology segment. USDA's National Milk Testing Strategy created a lasting role for PCR infrastructure in dairy herd surveillance after the December 2024 Federal Order. In companion animals, peer-reviewed validation has strengthened the case for liquid biopsy and related molecular tools in earlier cancer detection, including 98.7% specificity in a 2024 canine screening study. These parallel use cases matter because they reduce dependence on a single disease area or animal population. The technology mix is therefore widening the practical scope of the United States veterinary diagnostics market rather than replacing legacy formats outright.

Complete Report Scope:

- By Product

- Consumables, Kits and Reagents

- Instruments

- By Technology

- Immunodiagnostics

- Clinical Biochemistry

- Molecular Diagnostics

- Hematology

- Urinalysis

- Other Technologies

- By Animal Type

- Companion Animals

- Dogs

- Cats

- Other Companion Animals

- Livestock

- Cattle

- Swine

- Poultry

- Other Livestock Animals

- Companion Animals

- By Application

- Infectious Diseases

- Endocrinology

- Cardiology

- Oncology

- Other Applications

- By End User

- Veterinary Reference Laboratories

- Veterinary Hospitals and Clinics

- Point-of-Care and In-House Testing

- Veterinary Research Institutes and Universities

List of Companies Covered in this Report:

- Agfa-Gevaert

- Antech Diagnostics

- Bionote

- Bio-Rad Laboratories

- bioMerieux

- Covetrus

- FUJIFILM

- Heska

- Henry Schein

- IDEXX

- INDICAL BIOSCIENCE GmbH

- Neogen

- QIAGEN

- Randox Laboratories

- Scil Animal Care Company

- Shenzhen Mindray Animal Medical Technology Co., Ltd.

- Siemens Healthineers

- Thermo Fisher Scientific

- Virbac

- Zoetis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Companion Animal Health Spend

- 4.2.2 Expansion of In-Clinic and Point-of-Care Testing

- 4.2.3 AI-Enabled Interpretation of Images and Bloodwork

- 4.2.4 Wider Use of Molecular and Rapid Assays in Routine Practice

- 4.2.5 Corporate Chain Standardization and Bulk Reagent Buying

- 4.2.6 Under-Served Mobile and Ambulatory Veterinary Models

- 4.3 Market Restraints

- 4.3.1 Persistent Veterinarian and Laboratory Technician Shortages

- 4.3.2 High Cost of Advanced Diagnostics for Price-Sensitive Owners

- 4.3.3 Fragmented Workflow Integration Across Practice Software and Devices

- 4.3.4 Limited Reimbursement Visibility for Premium Diagnostics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Consumables, Kits and Reagents

- 5.1.2 Instruments

- 5.2 By Technology

- 5.2.1 Immunodiagnostics

- 5.2.2 Clinical Biochemistry

- 5.2.3 Molecular Diagnostics

- 5.2.4 Hematology

- 5.2.5 Urinalysis

- 5.2.6 Other Technologies

- 5.3 By Animal Type

- 5.3.1 Companion Animals

- 5.3.1.1 Dogs

- 5.3.1.2 Cats

- 5.3.1.3 Other Companion Animals

- 5.3.2 Livestock

- 5.3.2.1 Cattle

- 5.3.2.2 Swine

- 5.3.2.3 Poultry

- 5.3.2.4 Other Livestock Animals

- 5.3.1 Companion Animals

- 5.4 By Application

- 5.4.1 Infectious Diseases

- 5.4.2 Endocrinology

- 5.4.3 Cardiology

- 5.4.4 Oncology

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Veterinary Reference Laboratories

- 5.5.2 Veterinary Hospitals and Clinics

- 5.5.3 Point-of-Care and In-House Testing

- 5.5.4 Veterinary Research Institutes and Universities

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Agfa-Gevaert N.V.

- 6.3.2 Antech Diagnostics, Inc.

- 6.3.3 BioNote, Inc.

- 6.3.4 Bio-Rad Laboratories, Inc.

- 6.3.5 bioMerieux SA

- 6.3.6 Covetrus, Inc.

- 6.3.7 FUJIFILM Holdings Corporation

- 6.3.8 Heska Corporation

- 6.3.9 Henry Schein, Inc.

- 6.3.10 IDEXX Laboratories, Inc.

- 6.3.11 INDICAL BIOSCIENCE GmbH

- 6.3.12 Neogen Corporation

- 6.3.13 QIAGEN N.V.

- 6.3.14 Randox Laboratories Ltd.

- 6.3.15 Scil Animal Care Company GmbH

- 6.3.16 Shenzhen Mindray Animal Medical Technology Co., Ltd.

- 6.3.17 Siemens Healthineers AG

- 6.3.18 Thermo Fisher Scientific Inc.

- 6.3.19 Virbac

- 6.3.20 Zoetis Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment