|

시장보고서

상품코드

2063614

말 진단 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Equine Diagnostic Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

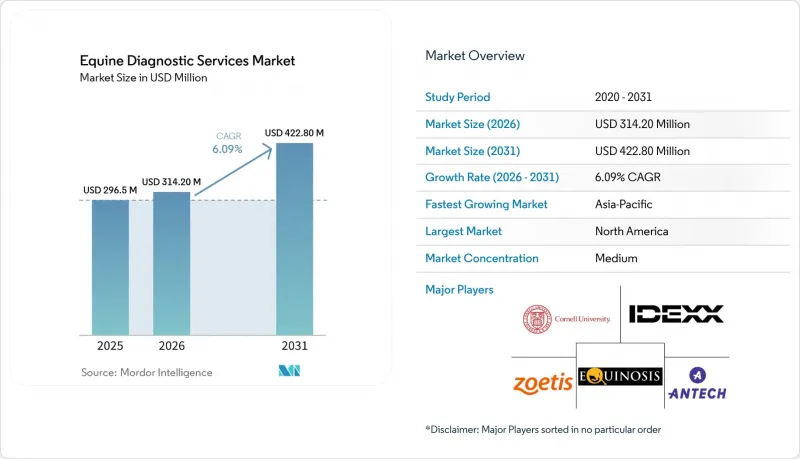

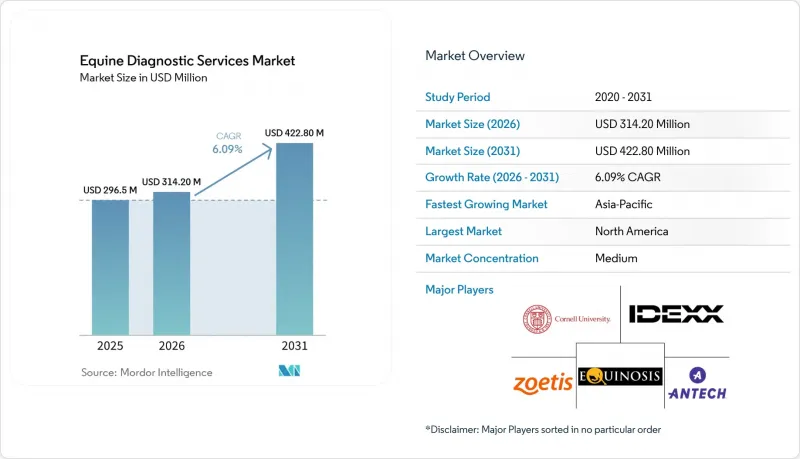

Mordor Intelligence에 의하면, 말 진단 서비스 시장 규모는 2025년에 2억 9,650만 달러로 평가되었고 2026년 3억 1,420만 달러에서 2031년까지 4억 2,280만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.09%를 나타낼 전망입니다.

본 보고서는 서비스 유형(임상 검사, 영상 진단 서비스 등), 최종 사용자/제공 기관(민간 수의학 검사 기관, 말 전문 소개·전문 병원 등) 및 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 규모 및 예측치는 금액(달러)으로 표시되어 있습니다.

전 세계 말 진단 서비스 시장 동향 및 인사이트

첨단 영상 진단 기술(기립 MRI/CT)이 파행의 확정 진단을 가속화합니다.

입위 MRI 및 하중 CT의 도입으로 인해, 검사 과정이 마취가 수반되는 당일 수술에서 단시간의 진정 시술로 단축되었습니다. 이를 통해 위험이 줄어들었으며, 경주마의 경우 당일 중 치료 계획을 수립할 수 있게 되었습니다. Hallmarq사의 보고에 따르면, 입위 MRI는 변화가 미세한 경우 기존 엑스레이 검사에서는 간과되기 쉬운, 고가치 경주마와 관련된 뼈 및 연조직의 초기 변화를 더 잘 시각화해 줍니다. 이를 통해 조기 부하 경감 프로토콜이 지원되어, 더 나은 치료 결과를 기대할 수 있습니다. Asto CT 등 업체들이 제공하는 하중 CT는 생리적 부하 상태에서의 3D 평가를 가능하게 하며, 앙와위 자세에서의 영상 진단으로는 확인할 수 없는 병변을 밝혀냅니다. 이는 경주마나 장애물 경주마의 사지 말단부 평가에 있어 매우 중요합니다. 대구경 시스템을 통해 주요 시설에서는 입식 촬영의 적용 범위가 근위부 및 경흉추 접합부까지 확대되었으며, 진정만 시행하는 프로토콜을 적용할 수 있는 증례의 폭이 넓어지고 있습니다. 진료 현장에서는 한 번의 내원 기간 내에 소견을 대조하기 위해 여러 가지 영상 기법을 조합하고 있으며, 원격 조작을 통한 스캔은 전담 전문의가 없는 시설에서도 고난도 증례를 효율적으로 처리하는 데 도움이 되고 있습니다. 이러한 변화로 인해 소개 거점 전체의 진단 기준이 향상되었으며, 말 진단 서비스 시장의 처리 능력이 향상되고 있습니다.

집단 발생 관리에서 분자 PCR/qPCR의 급속한 보급

주목을 받은 EHV-1 관련 사건으로 인해, PCR 검사는 확정 진단에서 행사장 도착 시나 검역 기간 중의 1차 선별 검사로 그 역할이 변화했으며, 분자진단 워크플로가 말의 이동 및 대회 운영의 일상 업무에 정착되었습니다. 코넬 대학교 AHDC와 콜로라도 주립대학교 등의 참고 센터는 집단 발생 시 처리 능력을 급격히 확대했습니다. 한편, 원인을 알 수 없는 발열에 대한 검사 패널은 패혈증이나 장 질환으로 인한 발열 진단 시의 사각지대를 메우기 위해 확충되었습니다. 인두낭 세척액은 비인두 면봉보다 훨씬 민감도가 높고, qPCR은 배양법보다 우수한 성능을 발휘하기 때문에 증거에 기반한 검체 채취는 말 전염성 후두염의 통제에 있어 매우 중요합니다. 이를 통해 무증상 보균자가 새로운 감염 사례를 유발할 위험이 줄어듭니다. 마구간 옆에서 LAMP 장비와 차세대 멀티플렉스 PCR 패널을 활용함으로써 판정 시간이 며칠에서 몇 시간으로 단축되었고, 이는 검역 정확도 향상과 시설 가동 중단 시간 단축으로 이어지고 있어, 결과가 나오기까지 걸리는 시간이 중요한 차별화 요인으로 부상하고 있습니다. bioMerieux사의 VETFIRE와 같은 새로운 통합형 호흡기 검사 키트는 다중 병원체 PCR을 단일 독립형 카트리지에 담아, 이를 통해 콜드체인의 장벽을 제거함으로써 택배 네트워크가 제한된 지역에서의 도입을 촉진합니다. 이러한 운영상의 발전으로 말 진단 서비스 시장에 안정적인 수요가 창출되고, 쇼나 경매에서 발생할 수 있는 상황에 대비하는 기준이 높아질 것입니다.

높은 검사 비용과 보험 적용 범위의 불균형

고도의 영상 진단 비용과 다중 모달리티 검사의 연쇄적인 진행은 많은 말 소유주에게 연간 보험 적용 한도를 초과할 가능성이 있어, 엘리트 말이 아닌 말에 대한 선택적 이용을 억제하고 있습니다. 기본적인 영상 진단 패키지조차도 진정제, 판독비, 시설 이용료가 포함되어 있어, 최종 청구액은 표면상의 검사 비용을 초과합니다. 따라서 투명한 견적과 단계별 요금 체계는 신뢰를 쌓는 데 중요한 요소가 됩니다. 마구간 내 진단은 택배 비용과 운송으로 인한 시간 손실을 줄여주지만, 카트리지 및 소모품 비용이 추가되므로 진료소 측은 응급 상황이나 시간 외 서비스 시 이러한 비용을 요금에 반영해야 합니다. 보험 제도에서는 면책 금액이나 본인 부담금이 부과되는 경우가 많으며, 증례에 추적 검사나 중재적 처치가 필요해지면 이러한 부담이 겹치게 되어, 임상적 긴급성이 남아 있는 경우에도 마주가 검사 선택을 주저하게 되는 원인이 될 수 있습니다. 이에 대해 진료소 측은 검사 범위를 단일 부위로 한정하고, 당일 퇴원이 가능한 패키지 형태의 옵션을 제공함으로써 대응하고 있습니다. 이를 통해 가격에 민감한 고객은 완전한 입원이나 여러 부위의 영상 진단을 약속하지 않고도 검사를 진행할 수 있습니다. 보험 적용 범위가 확대되거나 종합적 케어 모델이 보급되기 전까지는 비용 측면의 마찰로 인해 말 진단 서비스 시장에서 특정 말 소유주 계층의 검사 건수 증가가 억제될 것으로 보입니다.

부문별 분석

임상 검사 진단은 2025년 말 진단 서비스 시장 규모의 36.98%를 차지하고 있으며, 이는 혈액학, 면역 분석 및 복잡한 배양 워크플로우 분야에서 여전히 많은 현장용 키트보다 광범위성과 민감도 면에서 우수하기 때문에 참조 센터의 이용이 정착되어 있음을 반영합니다. 현장 진단(POC) 시장은 2031년까지 연평균 성장률(CAGR) 8.93%로 확대될 것으로 전망됩니다. 이는 카트리지 플랫폼, 휴대용 혈액가스 분석기, 그리고 이동식 초음파 장치가 마구간 내의 진료 처리 능력을 향상시키고, 야간 택배 서비스에 대한 의존도를 줄이며, 임상적 상황에 맞추어 의사결정을 내릴 수 있게 하기 위함입니다. X선 촬영, 초음파 검사, MRI, CT, 내시경 검사를 포함한 영상 진단 서비스는 수익이 집중될 것으로 예측됩니다. 이는 첨단 검사법이 기본 스캔보다 검사 건수는 적지만, 건당 요금이 비싸기 때문입니다. 또한, 입식 MRI와 하중 CT는 현재 많은 의뢰 네트워크에서 핵심 서비스로 자리 잡고 있습니다. 유전자 검사는 여전히 틈새 시장이지만, 대학이나 민간 검사 기관을 통해 실시되는 표적 패널을 이용한 착상 전 위험도 검사가 생식 프로그램의 표준 절차로 자리 잡으면서, 고부가가치 번식 판단에 있어 그 중요성이 커지고 있습니다. 내시경 검사나 인두 세척과 같은 전문적인 처치는 말 전염성 후두염(스트랭글스) 보균자를 특정하는 데 필수적이며, 학술 연구소에서 제시한 검체 채취 지침에 따라 민감도가 향상되고 재감염 위험이 감소하고 있습니다. 이를 통해 면봉 검사만으로 음성 판정을 받았을 때 생기는 잘못된 안심감이 줄어들고 있습니다.

이러한 상황에서 기기에 내장된 AI와 소프트웨어의 통합을 통해 일상적인 검사 결과 확인 작업이 환자 곁에서 이루어지게 되었으며, 검사실과 수의사 간의 의사소통 주기가 단축되고 있습니다. 이로 인해 외래 진료를 담당하는 임상의는 환자가 한 번 내원했을 때 보다 종합적인 검사를 실시하는 것의 타당성을 설명하기가 더 쉬워졌습니다. FEI(국제승마연맹)의 규정 변경 및 경기 의학의 발전에 따라, 투약 및 건강 상태 확인과 관련된 당일 기록 작성에 대한 수요가 증가하고 있으며, 의료적 필요성을 입증하고 연맹 규정에 따른 출전 자격을 뒷받침하기 위해 경기장 내 생화학 검사 및 혈액 검사 패널에 대한 수요가 늘어나고 있습니다. 성숙한 시장에서는 첨단 영상진단 허브를 중심으로 구축되는 반면, 급성장 지역에서는 대규모 시설 투자 없이 접근성을 개선하는 휴대용 플랫폼이 중시되기 때문에 지역별 도입 경로는 서로 다르게 나타나고 있습니다. 이러한 추세가 강화됨에 따라, 1차 진료 사례에서 당일 내에 검사를 완료하는 비율이 증가하여 말 진단 서비스 업계의 지속적인 수요를 확대시키는 동시에, 외부 위탁에서 마구간 내 판단으로 업무 구성을 전환하고 있습니다.

지역별 분석

북미는 2025년 시장 점유율의 41.66%를 차지하고 있으며, 이는 이동 및 대회에서 진단 활용을 제도화하는 주 및 연방 차원의 질병 감시 및 수입 생물 보안 관련 요건에 힘입은 결과입니다. 주 경계를 넘는 이동은 일반적으로 최근의 코긴스 검사 결과와 수의사가 발급한 증명서에 따라 결정되며, 수입되는 번식용 말은 전염성 말 자궁내막염(CEM)에 대한 연속 배양 검사 등 다단계 검역 선별 검사를 통과해야 합니다. 이를 통해 진단 수요가 일상적인 업무 흐름에 통합되었습니다. 행사 주최 측과 규제 당국은 체온 기록을 관리하고, 기준치를 초과할 경우 PCR 검사를 실시하기 때문에 분자 검사가 쇼 서킷과 훈련 센터 전반으로 확대되고 있습니다. EHV-1 관련 행사가 개최될 때, 대학 및 주립 연구소가 검사 역량 강화와 정보 공유를 조율함으로써 대응 시간이 표준화되고, 대규모 마구간이나 행사장에서의 감염 확산 위험이 줄어듭니다. 고도의 영상 진단 서비스는 대학 캠퍼스나 승마가 활발한 지역 및 그 주변에 집중되어 있지만, 원격 운영을 통해 영상 검사와 현장의 전문의 상주 여부를 분리함으로써 인접 주까지 서비스 제공 범위가 확대되고 있습니다. 이러한 요인들이 미국 및 캐나다 전역의 말 진단 서비스 시장의 꾸준한 성장을 뒷받침하고 있습니다.

유럽에서는 주요 학술 센터와 경마 거점이 다양한 보험 환경과 연계되어 있어, 이에 따라 소개 의료기관이 밀집된 지역에서는 도입이 진전되고 있는 반면, 특정 국가의 경마와 무관한 고객층 사이에서는 보다 신중한 도입 양상이 나타나고 있습니다. 로열 수의과대학은 광범위한 해부학적 영역에서 진정만으로도 스캔이 가능한 대형 입식 CT 시스템을 도입했습니다. 이로 인해 영국의 의료기관 연계 생태계에서 검사 대상 사례의 범위가 확대되고 처리 능력이 향상되고 있습니다. 유럽의 제조업체 및 검사 기관들은 다중 병원체 대응 호흡기 PCR 키트와 기타 통합형 솔루션을 지속적으로 출시하고 있으며, 이를 통해 진료소 간 워크플로우 연계가 촉진되고 신규 사용자의 교육 부담이 줄어들고 있습니다. 유럽연합(EU)의 규제 조화와 세계동물보건기구(WOAH)의 말 질병 검사 전문 지식 역량 강화는 국경을 넘는 이동의 원활화와 감시 관행의 표준화를 뒷받침하고 있으며, 이는 유럽 전역의 경기 일정에 있어 중요한 요소입니다. 소개 병원이 고객에게 입위 영상 진단의 가치를 알리고, 검사 기관들이 결과 서식을 통일함에 따라 국경을 초월한 예측 가능한 사례 흐름이 형성되어, 유럽의 말 진단 서비스 시장에서 수요가 유지될 것입니다.

아시아태평양은 일본의 경마 중심 영상 진단 시장의 성장과 호주의 협력 병원 집중화에 힘입어, 비율 기준으로 가장 빠른 성장세를 보이고 있습니다. 한편, 주요 시장에서는 대도시권의 거점에 고도의 진단 역량이 구축되어 있습니다. 일본중앙경마회의 훈련센터에서 MRI 활용에 관한 데이터와 사지 말단의 영상 진단을 둘러싼 규제 관련 논의는 정식 경마 제도가 얼마나 고도의 검사법에 대한 기초적인 수요를 높이고 있는지를 뒷받침하고 있습니다. 호주에서는 멜버른 대학교가 단일 말 전문센터에 고자기장 영상 진단과 CT를 한데 모아둔 것이 강점으로 작용하고 있으며, 인근 주와 주변 국가에서 발생하는 복잡한 증례들을 모아들이는 지역적 거점 역할을 하고 있습니다. CT 기술 및 단층 해부학에 관한 교육 자료는 교육 플랫폼을 통해 지속적으로 보급되고 있으며, 성장하는 시장에서 임상의와 방사선사들 사이에서 해당 기술의 확산을 가속화하고 있습니다. 아시아태평양의 거점들이 알찬 PCR 프로그램에 더해 상설 CT 및 MRI 장비를 도입함에 따라, 이들 거점은 동심원 형태의 서비스권을 형성하며 말 진단 서비스 시장의 지역 전체 수요를 끌어올리고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the equine diagnostic services market size was valued at USD 296.5 million in 2025 and is estimated to grow from USD 314.20 million in 2026 to reach USD 422.80 million by 2031, at a CAGR of 6.09% during the forecast period (2026-2031).

This report is Segmented by Service Type (Laboratory Diagnostics, Imaging Services, and More), End-User / Provider Setting (Commercial Veterinary Reference Laboratories, Equine Referral & Specialty Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasted in Terms of Value (USD).

Global Equine Diagnostic Services Market Trends and Insights

Advanced Imaging Access (standing MRI/CT) Accelerating Definitive Lameness Diagnosis

Standing MRI and weight-bearing CT have compressed workups from anesthesia-based day procedures to short sedated sessions, which cuts risk and enables same-day treatment planning in performance horses. Hallmarq reports that standing MRI improves visualization of early bone and soft-tissue changes relevant to high-value athletes that traditional radiography can miss when changes are subtle, which supports earlier offloading protocols and better outcomes. Weight-bearing CT from vendors such as Asto CT adds 3D assessment under physiological load that can reveal pathology not seen with recumbent imaging, which is critical for distal-limb evaluation in racing and jumping cohorts. Large-bore systems have extended standing coverage into proximal regions and cervicothoracic junctions in major centers, which widens case eligibility for sedation-only protocols. Practices are pairing modalities to correlate findings within a single visit, and teleoperated scanning is helping sites without on-staff specialists to run advanced cases efficiently. These shifts are raising the diagnostic baseline across referral hubs and lifting throughput in the equine diagnostic services market.

Rapid Adoption of Molecular PCR/qPCR for Outbreak Management

High-profile EHV-1 events have pushed PCR from confirmatory testing to frontline screening at event arrival and during quarantine, which hardwires molecular workflows into routine movement and competition. Reference centers such as Cornell AHDC and Colorado State ramped surge capacity during outbreaks, while panels for fever-of-unknown-origin broadened to close blind spots in septic and enteric causes of pyrexia. Evidence-based sampling is central to strangles control since guttural pouch lavage is far more sensitive than nasopharyngeal swabs and qPCR outperforms culture, which reduces the risk of silent carriers seeding new cases. Time-to-result is becoming a key differentiator as stall-side LAMP units and next-generation multiplex PCR panels compress decisions from days to hours, which improves quarantine precision and reduces facility downtime. New integrated respiratory kits, such as bioMerieux VETFIRE, place multi-pathogen PCR into a single self-contained cartridge, which removes cold-chain hurdles and supports adoption in regions with limited courier networks. This operational evolution shifts steady volumes into the equine diagnostic services market and raises the baseline for outbreak readiness at shows and sales.

High Procedure and Per-Test Costs with Uneven Insurance Coverage

Advanced imaging prices and multi-modality cascades can exceed annual coverage limits for many owners, which suppresses elective utilization for non-elite horses. Even basic imaging packages include sedation, interpretation, and facility fees that raise the final bill beyond the headline scan price, which makes transparent estimates and tiered offerings an important trust driver. Stall-side diagnostics reduce courier expenses and time lost to shipping, but they add cartridge and consumable costs that practices must price into emergency and after-hours services. Insurance structures often impose deductibles and co-pays that compound when cases require follow-up scans or interventional procedures, which can cause owners to pause between modalities even when clinical urgency remains. Clinics are responding with menu-based options that align scan scope to a single region and same-day discharge, which helps price-sensitive clients move forward without committing to full hospitalization or multi-region imaging. Until insurance coverage rises or bundled care models spread, cost friction will temper volume growth in certain owner segments within the equine diagnostic services market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Stall-Side/Ambulatory Diagnostics in Equine Practice

- Growth in Organized Equestrian Sport and Stricter Biosecurity/Anti-Doping Programs

- Scarcity of Board-Certified Equine Imaging Specialists/Radiologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laboratory Diagnostics held 36.98% of the 2025 share of the equine diagnostic services market size, reflecting entrenched use of reference centers for hematology, immunoassays, and complex culture workflows that still outperform many field kits for breadth and sensitivity. Point-of-care or field diagnostics is projected to expand at an 8.93% CAGR through 2031 as cartridge platforms, portable blood gas analyzers, and mobile ultrasound improve case throughput at the stable, which reduces dependency on overnight couriers and aligns decisions to the clinical clock. Imaging Services, including radiography, ultrasound, MRI, CT, and endoscopy, concentrate revenue because advanced modalities command higher per-case fees despite lower unit volumes than basic scans, and standing MRI and weight-bearing CT are now core offerings in many referral networks. Genetic testing remains a niche but is gaining relevance in high-value breeding decisions as reproductive programs formalize pre-implantation risk checks via targeted panels run through university or commercial labs. Endoscopy and specialty procedures such as guttural pouch lavage are critical for strangles carrier identification, and sampling guidance from academic labs is improving sensitivity and lowering reinfection risk, which reduces false reassurance from negative swab-only protocols.

In this context, on-instrument AI and software integration are pulling routine review tasks closer to the patient, which compresses lab-to-vet communication loops and helps ambulatory clinicians justify more complete workups in a single visit. FEI rule changes and competition medicine are raising same-day documentation needs for medications and welfare checks, which boosts demand for in-venue chemistry and hematology panels to document medical necessity and support eligibility under federated rules. Regional adoption paths diverge since mature markets build around advanced imaging hubs while fast-growing regions emphasize portable platforms that improve access without major facilities investment. As these patterns reinforce, a larger share of first-opinion cases complete the workup within the same day, which expands recurring demand in the equine diagnostic services industry while shifting mix from send-outs to stall-side decisions.

Geography Analysis

North America held 41.66% of the 2025 share, sustained by state and federal requirements for disease surveillance and import biosecurity that institutionalize diagnostic use across movements and competitions. Interstate movement commonly hinges on recent Coggins tests and veterinary certificates, and imported breeding stock must clear multi-step quarantine screens such as serial cultures for contagious equine metritis, which embeds diagnostic demand in routine workflows. Event organizers and regulators maintain temperature logs and trigger PCR when thresholds are exceeded, which spreads molecular testing throughout show circuits and training centers. During EHV-1 events, university and state labs coordinate surge capacity and communications, which normalizes response times and reduces spread risk in large barns and event venues. Advanced imaging access is concentrated in and around university hubs and high-density equestrian regions, and teleoperations are extending coverage into adjoining states by decoupling scans from on-site specialist availability. These factors support steady growth in the equine diagnostic services market across the United States and Canada.

Europe pairs leading academic centers and racing hubs with mixed insurance environments, which produces strong adoption in referral clusters and more cautious uptake among non-racing clients in select countries. The Royal Veterinary College installed a large-bore standing CT system that enables sedation-only scans in wider anatomical regions, which broadens case eligibility and improves throughput in the UK's referral ecosystem. European manufacturers and labs continue to launch multi-pathogen respiratory PCR kits and other integrated offerings, which helps synchronize workflows across clinics and reduces training overhead for new users. Federation harmonization and WOAH capacity building on laboratory expertise for equine diseases support improved cross-border movement and standardized surveillance practices, which is important for pan-European competition calendars. As referral hospitals educate clients on the value of standing imaging and as labs align result formats, predictable case flows can develop across national boundaries, which sustains demand in the equine diagnostic services market in Europe.

Asia-Pacific is the velocity leader on a percentage basis, anchored by Japan's racing-driven imaging growth and Australia's referral concentration, while large markets build advanced capacity in metro hubs. Japan Racing Association data on training center MRI use and regulatory discussions around distal-limb imaging reinforce how formal racing systems lift baseline demand for advanced modalities. Australia benefits from the University of Melbourne's concentration of high-field imaging and CT in a single equine center, which acts as a regional magnet for complex cases in neighboring states and countries. Educational resources on CT techniques and cross-sectional anatomy continue to spread through training platforms, which accelerates skill diffusion among clinicians and radiographers in growing markets. As hubs in Asia-Pacific add standing CT and MRI alongside robust PCR programs, they seed concentric catchments that raise regional volumes in the equine diagnostic services market.

- Antech Diagnostics

- Asto CT

- Cornell University (Animal Health Diagnostic Center)

- Equine Diagnostic Solutions, LLC

- Equinosis, LLC

- Esaote S.p.A.

- Hallmarq Veterinary Imaging Ltd

- IDEXX

- IMV Imaging Ltd

- Kansas State University

- Moore Equine Veterinary Centre Ltd

- Rainbow Equine Hospital Ltd

- Royal Veterinary College, University of London

- Texas A&M University

- University of California, Davis

- University of Connecticut (CVMDL)

- Virginia Equine Imaging, PLLC

- Virginia Polytechnic Institute and State University

- Zoetis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advanced Imaging Access (standing MRI/CT) Accelerating Definitive Lameness Diagnosis

- 4.2.2 Rapid Adoption of Molecular PCR/qPCR for Outbreak Management

- 4.2.3 Expansion of Stall-Side/Ambulatory Diagnostics in Equine Practice

- 4.2.4 Growth in Organized Equestrian Sport and Stricter Biosecurity/Anti-Doping Programs

- 4.2.5 Imaging-as-a-service and pay-as-you-scan Models Lowering Capex Barriers

- 4.2.6 Objective Gait Analytics (Inertial Sensors/Computer Vision) Scaling Referral Throughput

- 4.3 Market Restraints

- 4.3.1 High Procedure and Per-Test Costs with Uneven Insurance Coverage

- 4.3.2 Scarcity of Board-Certified Equine Imaging Specialists/Radiologists

- 4.3.3 Inter-Laboratory Variability and Limited Standardization in Some Equine PCR Assays

- 4.3.4 Field Logistics Delaying Turnaround

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Anlaysis

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Laboratory Diagnostics

- 5.1.2 Imaging Services

- 5.1.3 Point-of-Care / Field Diagnostics

- 5.1.4 Genetic Testing

- 5.1.5 Endoscopy & Other Procedures

- 5.2 By End-user / Provider Setting

- 5.2.1 Commercial Veterinary Reference Laboratories

- 5.2.2 Equine Referral & Specialty Hospitals

- 5.2.3 Ambulatory / Field Veterinary Practices

- 5.2.4 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia Pacific

- 5.3.4 Middle East & Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of MEA

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Antech Diagnostics, Inc.

- 6.3.2 Asto CT, Inc.

- 6.3.3 Cornell University (Animal Health Diagnostic Center)

- 6.3.4 Equine Diagnostic Solutions, LLC

- 6.3.5 Equinosis, LLC

- 6.3.6 Esaote S.p.A.

- 6.3.7 Hallmarq Veterinary Imaging Ltd

- 6.3.8 IDEXX Laboratories, Inc.

- 6.3.9 IMV Imaging Ltd

- 6.3.10 Kansas State University

- 6.3.11 Moore Equine Veterinary Centre Ltd

- 6.3.12 Rainbow Equine Hospital Ltd

- 6.3.13 Royal Veterinary College, University of London

- 6.3.14 Texas A&M University

- 6.3.15 University of California, Davis

- 6.3.16 University of Connecticut (CVMDL)

- 6.3.17 Virginia Equine Imaging, PLLC

- 6.3.18 Virginia Polytechnic Institute and State University

- 6.3.19 Zoetis Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment