|

시장보고서

상품코드

2072737

헬스케어 제로 트러스트 보안 분야 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Healthcare Zero-Trust Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

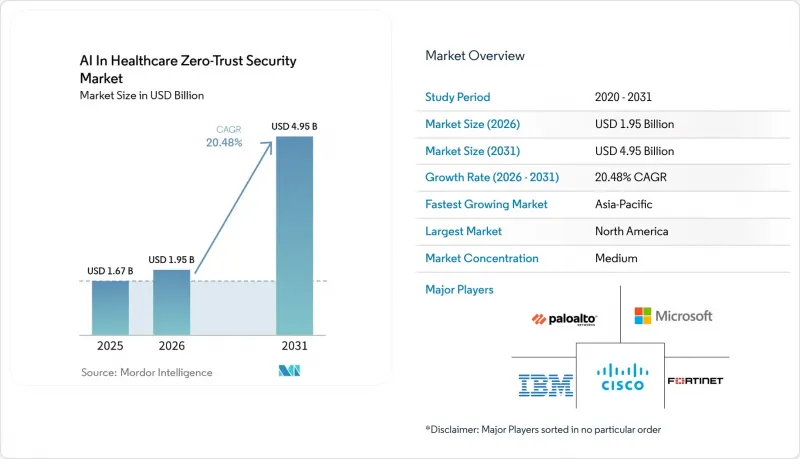

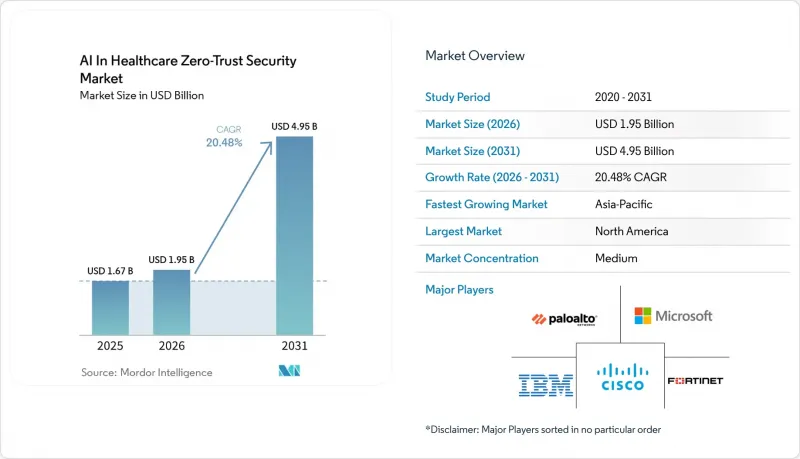

Mordor Intelligence에 의하면, 헬스케어 제로 트러스트 보안 분야 AI 시장 규모는 2025년 16억 7,000만 달러로 평가되었고, 2026년에는 19억 5,000만 달러로 추정되고, 2026-2031년 CAGR 20.48%로 성장을 지속할 전망이며, 2031년에는 49억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(솔루션 및 서비스), 도입 형태별(클라우드 및 온프레미스), 용도별(임상 데이터 보호 및 기타), 최종 사용자별(의료 제공업체, 제약 및 바이오기술 기업 및 기타), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 헬스케어 제로 트러스트 보안 분야 AI 시장 동향 및 인사이트

AI를 활용한 마이크로 세분화가 횡방향 침해의 확산을 억제

AI를 활용한 마이크로 세분화는 과거에는 대부분의 병원 IT 팀에게 너무 복잡해 처리할 수 없었던 작업을 자동화해 주기 때문에 실질적인 성장의 원동력이 되고 있습니다. 대규모 의료 시스템에서는 수천 개에 달하는 장치와 용도의 상태가 끊임없이 변화하기 때문에 머신러닝의 지원 없이는 최소 권한 원칙을 수동으로 최신 상태로 유지하는 것이 어렵습니다. MultiCare Health System은 2025-2026년 진행된 프로그램에서 13개 병원과 350개 이상의 진료소에 연결된 4만 대 이상의 기기에 ID 기반 마이크로 세분화을 도입했습니다. 이 사업은 최대 14명분의 기준에 비해, 2명분의 정규직에 해당하는 인력으로 수행되었습니다. 이러한 운영상의 효율성은 헬스케어 제로 트러스트 보안 분야 AI 시장에서 중요합니다. 왜냐하면 병원에서는 임상 업무 흐름을 방해하지 않으면서도 적용할 수 있는 세분화가 필요하기 때문입니다. 또한, 헬스케어 제로 트러스트 보안 분야 AI 시장에서는 고가치 공격 경로가 되는 영상 진단 시스템과 패치 적용이 드문 기타 자산에 대한 보호도 강화될 것입니다. 점점 더 많은 의료 서비스 제공업체들이 번거로움이 적은 도입 모델을 추구함에 따라, 자동화된 세분화은 제로 트러스트를 개념에서 일상적인 임상 보안 관행으로 전환하기 위한 가장 명확한 수단 중 하나로 자리 잡고 있습니다.

연결형 의료기기를 표적으로 삼는 랜섬웨어의 급증

의료 분야의 AI 기반 제로 트러스트 보안 시장에서는 의료 업무에 대한 랜섬웨어 위협이 급증함에 따라 수요가 크게 증가하고 있습니다. FBI의 인터넷 범죄 신고 센터(IC3)는 2025년에 의료 분야에서 278건의 랜섬웨어 피해를 확인했으며, 이로 인해 사이버 보안은 예산 편성 시 최우선 과제 중 하나로 계속해서 자리 잡고 있습니다. 버라이즌의 '2026년 데이터 침해 조사 보고서'에 따르면, 추적된 1,492건의 사고 중 48%(전년은 44%)에 해당하는 의료 분야의 데이터 침해 사건에 랜섬웨어가 연루된 것으로 밝혀졌습니다. 연결형 의료기기가 문제를 더욱 심각하게 만들고 있습니다. 2026년에는 조직의 24%가 연결형 의료기기를 대상으로 한 사이버 공격을 받았으며, 그 공격의 80%가 환자 치료에 중등도 또는 심각한 영향을 미쳤기 때문입니다. 의료기기를 표적으로 한 원격 액세스 악용 사례도 2025년 28%에서 2026년 38%로 증가했으며, 이는 공격자들이 상시 연결 상태인 임상용 엔드포인트를 새로운 표적으로 삼고 있음을 시사합니다. 이에 대응하기 위해, 의료 분야의 AI 기반 제로 트러스트 보안 시장에서는 기기의 전면적인 교체를 강요하지 않으면서도 횡방향 이동을 차단할 수 있는 지속적인 기기 인증 및 세밀한 트래픽 제어 방식으로 전환되고 있습니다.

AI 보안 및 DevSecOps 인재의 기술 격차

헬스케어 제로 트러스트 보안 분야 AI 시장의 주요 운영상의 제약은 AI를 활용한 보안 프로그램을 일상적으로 운영할 수 있는 인력이 부족하다는 점입니다. ISC2의 보고서에 따르면, 2025년에는 전 세계적으로 400만 명 이상의 사이버 보안 인력이 부족할 것으로 예상되며, 많은 의료 기관에서는 정책 엔진의 조정, 모델 동작 검증, 지속적인 검증 유지에 필요한 충분한 인력을 확보하지 못하고 있습니다. 이러한 인력 부족은 보안 팀이 제한된 인력으로 ID 관리, 기기 관리, 클라우드 워크로드 관리, 규정 준수 대응을 동시에 수행해야 하는 자원이 제한된 의료 기관에서 더욱 심각한 문제로 대두되고 있습니다. 병원이 새로운 플랫폼을 도입하더라도, 도입 진행이 지연될 수 있습니다. 왜냐하면 구매 후에야 비로소 가장 어려운 작업이 시작되며, 팀은 정책 정의, 동작 기준 설정, 임상 업무 전반에 걸친 예외 테스트를 수행해야 하기 때문입니다. 소규모 의료기관이나 지방 의료기관은 방대한 시설 전체나 전담 보안 부서에 전문 인력을 배치할 수 없기 때문에 가장 심각한 부담에 직면해 있습니다. 따라서 자동화 및 의료 업계에 특화된 템플릿을 통해 전문 인력의 필요성을 줄여주는 벤더들이, 의료 분야의 AI 기반 제로 트러스트 보안 시장에서 지지를 얻고 있습니다.

부문별 분석

이 솔루션은 2025년에 의료 AI 제로 트러스트 보안 시장 점유율의 54.32%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 21.44%로 성장할 것으로 전망됩니다. 이는 소프트웨어 플랫폼이 여전히 도입의 기반 계층을 형성하고 있음을 보여줍니다. 이 범주에는 마이크로 세분화 엔진, AI를 활용한 ID 및 액세스 관리, 행동 분석, 보안 모니터링 통합 등이 포함되며, 이를 통해 병원은 정책을 지속적으로 개선하는 데 필요한 텔레메트리 정보를 확보할 수 있습니다. 2025년에는 Zscaler의 Zero Trust Exchange에서 의료 AI가 710억 건의 AI 및 ML 트랜잭션을 생성했으며, 의료 분야는 거래량 측면에서 공공 부문 내에서 가장 큰 기여를 한 분야가 되었습니다. 이는 솔루션 플랫폼이 소규모 시범 프로젝트가 아니라, 이미 임상 규모의 활동을 처리하고 있음을 보여줍니다. 이러한 규모 덕분에 벤더는 정적인 정책 라이브러리에만 의존하지 않고, 실제 운영 행동을 바탕으로 감지 및 액세스 모델을 학습시킬 수 있습니다. 의료 분야의 제로 트러스트 보안 업계에서는 이러한 피드백 루프가 존재하기 때문에 솔루션 플랫폼이 임상 업무에 통합되면 이를 대체하기가 더욱 어려워집니다.

많은 의료 시스템에서 제로 트러스트 도입 시 관리형 감지 및 대응, 도입 지원, 규정 준수 관련 지침이 여전히 필요하기 때문에 이 서비스는 계속해서 중요한 위치를 차지하고 있습니다. 서비스 제공업체는 또한 병원이 범용 플랫폼을 의료기기 환경, 임상 용도의 흐름, 감사 및 문서화 요건에 맞게 조정할 수 있도록 지원하고 있습니다. 앞으로 의료 분야의 AI 기반 제로 트러스트 보안 시장에서는 서비스가 기본적인 도입 단계에서 복잡한 임상 환경에 적합한 모델 검증, 감사 지원, 정책 설계 단계로 점차 전환될 것으로 보입니다.

클라우드는 시장 점유율의 56.34%를 차지했으며, 가장 빠르게 성장하고 있는 도입 형태이기도 합니다. 헬스케어 제로 트러스트 보안 분야 AI 시장의 클라우드 기반 서비스 규모는 2031년까지 연평균 성장률(CAGR) 22.25%로 확대될 것으로 전망됩니다. 이러한 성장은 단일 네트워크 경계 내에 국한되지 않는 병원, 진료소, 원격지 직원 및 타사 용도를 아우르는 단일 정책 계층에 대한 요구를 반영하고 있습니다. 또한, 클라우드를 통한 서비스는 구매자에게 유연성을 제공하므로, 입원 환자 수의 급증이나 원격 진료, 혹은 데이터 집약형 AI 워크로드 증가에 따라 정책 및 검사 역량을 확장할 수 있습니다. Illumio는 2026년 2월, 하이브리드 환경을 위한 에이전트 없는 가시화 및 침해 차단 플랫폼을 발표했습니다. 이 플랫폼은 Check Point 및 Fortinet의 기존 방화벽 텔레메트리 데이터를 활용하여 혼합 환경 전반에 걸쳐 보호 범위를 확대합니다. 이 접근 방식은 의료 분야 AI용 제로 트러스트 보안 시장에 적합합니다. 왜냐하면 의료 분야의 구매자들은 기존의 온프레미스 자산을 관리 대상에서 제외하지 않으면서도 클라우드 수준의 정책 제어를 원하고 있기 때문입니다.

온프레미스 구축은 에어갭 요건이나 데이터 소재지에 대한 우려로 인해 완전한 클라우드 전환이 제한되는 대학 부속 병원, 정부 산하 의료 시스템, 연구 기관에서 여전히 명확한 역할을 수행하고 있습니다. 따라서 클라우드와 온프레미스 인프라 전반에 걸쳐, 중앙 집중식 정책과 분산형 적용이 연계되는 하이브리드 모델이 일반적입니다. 2025년 기준, 의료 기관들은 평균 11가지의 서로 다른 클라우드 서비스를 동시에 이용하고 있으며, 이것이 통합적인 접근 방식 없이는 통일된 정책을 유지하기 어려운 이유 중 하나입니다.

지역별 분석

2025년, 북미는 헬스케어 제로 트러스트 보안 분야 AI 시장 점유율의 49.36%를 차지했으며, 이 지역은 가장 큰 도입 기반을 갖추고 있을 뿐만 아니라 단기적으로 가장 강력한 구매력을 보유하고 있었습니다. 미국이 이 분야에서 선두를 달리고 있는 이유는 데이터 침해 위험이 높을 뿐만 아니라, HIPAA 개정안에 따라 마이크로 세분화이 단순한 선택지가 아닌 필수적인 통제 수단이 되기 때문입니다. 2024년, 미국에서 의료 데이터 유출로 인한 비용은 1,093만 달러에 달했으며, 이를 통해 이사회에 보다 강력한 접근 제어 및 차단 조치의 도입을 정당화할 수 있는 명확한 재무적 근거가 제시되었습니다. 캐나다와 멕시코는 도입 속도가 미국보다 느리긴 하지만, 의료의 디지털화와 병원 네트워크 확장을 통해 해당 지역의 성장에 기여하고 있습니다. 2031년까지 규정 준수 기한, 보험사의 압력, 그리고 기업의 조달 동향이 같은 방향으로 나아가고 있는 만큼, 헬스케어 제로 트러스트 보안 분야 AI 시장은 북미에서 안정적인 수요를 지속할 것으로 전망됩니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 23.27%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 지역이 될 전망입니다. 이 지역의 성장은 인도, 일본, 한국, 중국, 호주에서 시행되고 있는 디지털 헬스 프로그램으로 인해, 검증된 신뢰성 관리가 필요한 클라우드 연결 의료 기록, 의료기기, 원격 진료 워크플로우가 증가하고 있기 때문입니다. 이에 따라 헬스케어 제로 트러스트 보안 분야 AI 시장에는 큰 성장 여지가 생겨나고 있습니다. 특히, 각국 정부가 국가 차원의 의료 데이터 인프라를 구축하고, 의료 제공업체들이 보다 긴밀하게 연계된 진료 모델로 전환하고 있는 지역에서는 이러한 경향이 두드러집니다. 또한, 해당 지역의 의료 서비스 제공업체들은 성장과 데이터 상주 규정 간의 균형을 모색하고 있으며, 이는 연합 학습(federated learning)과 엣지 보안의 실용성을 높이고 있습니다. 또한, 데이터 거버넌스에 대한 기대치가 더욱 엄격해지고 있는 점도 성장 요인으로 작용하고 있으며, 이에 따라 개인정보 보호형 분석 및 엣지 기반 보안이 아시아태평양 전반에 걸쳐 도입되는 과정에서 그 중요성이 더욱 커지고 있습니다.

유럽은 시장에서 중요한 위치를 차지하고 있으며, 독일은 'TI 2.0' 제로 트러스트 프로그램을 통해 가장 강력한 공식적인 방향성을 제시하고 있습니다. 영국, 프랑스, 이탈리아, 스페인도 비슷한 길을 걷고 있으며, 주요 분야를 대상으로 한 사이버 규제와 의료 시스템 현대화 프로그램에 힘입어 보안 지출이 증가하고 있습니다. 중동 및 아프리카와 남미에서는 헬스케어 제로 트러스트 보안 분야 AI 시장이 여전히 초기 단계의 기회에 머물러 있습니다. GCC(걸프협력회의)의 디지털 헬스 프로그램이 도입을 주도하고 있는 반면, 설비 교체 주기의 지연으로 인해 더 광범위한 보급은 여전히 제한되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the AI in healthcare zero-trust security market size is expected to grow from USD 1.67 billion in 2025 to USD 1.95 billion in 2026 and is forecasted to reach USD 4.95 billion by 2031 at 20.48% CAGR over 2026-2031.

This report is Segmented by Component (Solutions and Services), Deployment Mode (Cloud and On-Premise), Application (Clinical Data Protection, and Others), End User (Healthcare Providers, Pharmaceutical and Biotech Companies, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Healthcare Zero-Trust Security Market Trends and Insights

AI-Driven Micro-Segmentation Curbs Lateral Breach Spread

AI-driven micro-segmentation has become a practical growth driver because it automates a task that was once too complex for most hospital IT teams. In large health systems, thousands of devices and applications change status constantly, so manual least-privilege rules are hard to keep current without machine learning support. MultiCare Health System used identity-based microsegmentation across more than 40,000 connected devices in 13 hospitals and more than 350 clinics during a 2025-2026 program, and it ran the effort with 2 full-time equivalents against a benchmark of up to 14. This operational leverage matters in the AI in healthcare zero-trust security market because hospitals need segmentation that can adapt without interrupting clinical workflows. It also improves protection around imaging systems and other rarely patched assets, which are high-value attack paths in the AI in healthcare zero-trust security market. As more providers look for lower-touch deployment models, automated segmentation is becoming one of the clearest ways to turn zero-trust from concept into day-to-day clinical security practice.

Surge in Ransomware Targeting Connected Medical Devices

The AI in healthcare zero-trust security market is seeing strong demand from the sharp rise in ransomware pressure on healthcare operations. The FBI's Internet Crime Complaint Center logged 278 confirmed healthcare ransomware incidents in 2025, which kept cybersecurity near the top of budget agendas. Verizon's 2026 Data Breach Investigations Report found that ransomware was involved in 48% of healthcare breaches, up from 44%, across 1,492 tracked incidents. Connected devices widen the problem because 24% of organizations experienced a cyberattack on a connected device in 2026, and 80% of those attacks caused moderate or significant impact on patient care. Remote access exploitation targeting medical devices also rose from 28% in 2025 to 38% in 2026, which shows how attackers are moving toward always-on clinical endpoints. In response, the AI in healthcare zero-trust security market is shifting toward continuous device authentication and fine-grained traffic controls that can block lateral movement without forcing a full device refresh.

Skills Gap in AI-Security DevSecOps Talent

The main operational restraint on the AI in healthcare zero-trust security market is the shortage of people who can run AI-assisted security programs day to day. ISC2 reported a global cybersecurity workforce gap of more than 4 million professionals in 2025, which leaves many healthcare organizations without enough staff to tune policy engines, review model behavior, or maintain continuous verification. This shortage matters more in lean provider settings, where security teams often have to manage identity, devices, cloud workloads, and compliance with the same limited staff. Even when hospitals buy new platforms, deployment can slow because the hardest work begins after purchase, when teams must define policies, set behavioral baselines, and test exceptions across clinical operations. Smaller and rural providers face the sharpest strain because they cannot spread specialist labor across large estates or dedicated security functions. Vendors that reduce the need for specialist labor through automation and healthcare-specific templates are therefore gaining preference in the AI in healthcare zero-trust security market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Zero-Trust in HIPAA and HITECH Updates

- Rapid Cloud Adoption of Electronic Health Records

- High TCO of Continuous Verification Frameworks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 54.32% of the AI in healthcare zero-trust security market share in 2025, and is also projected to grow at 21.44% CAGR through 2031, which shows that software platforms still form the base layer of deployment. This category includes micro-segmentation engines, AI-driven identity and access management, behavioral analytics, and security monitoring integrations that give hospitals the telemetry needed for continuous policy refinement. Healthcare AI generated 71 billion AI and ML transactions across Zscaler's Zero Trust Exchange in 2025, and healthcare was the largest public-sector contributor by volume, which indicates that solution platforms are already handling clinical-scale activity rather than small pilots. This scale helps vendors train detection and access models on real operational behavior instead of relying only on static policy libraries. In the AI in healthcare zero-trust security industry, that feedback loop makes solution platforms harder to displace once they are embedded in clinical operations.

Services remain important because many health systems still need managed detection and response, implementation support, and compliance guidance around zero-trust rollouts. Service providers also help hospitals adapt generic platforms to medical device estates, clinical application flows, and audit documentation needs. Over time, the AI in healthcare zero-trust security market is likely to see services shift from basic deployment work toward model validation, audit support, and policy design for complex clinical environments.

Cloud held 56.34% share in the market and is also the fastest-growing deployment mode, with AI in healthcare zero-trust security market size for cloud-based delivery projected to rise at 22.25% CAGR through 2031. This growth reflects the need for one policy plane across hospitals, clinics, remote staff, and third-party applications that do not sit inside a single network boundary. Cloud delivery also gives buyers elasticity, so policy and inspection capacity can expand with admissions spikes, remote consultations, or data-intensive AI workloads. Illumio introduced an agentless visibility and breach containment platform for hybrid environments in February 2026, using existing firewall telemetry from Check Point and Fortinet to extend protection across mixed estates. That approach fits the AI in healthcare zero-trust security market because healthcare buyers want cloud-scale policy control without leaving older on-premise assets unmanaged.

On-premise deployment still holds a defined role in academic medical centers, government health systems, and research settings where air-gap requirements or data residency concerns limit full cloud migration. The hybrid model is therefore common, with centralized policy and distributed enforcement working together across cloud and local infrastructure. Healthcare organizations were using an average of 11 different cloud services at the same time in 2025, which helps explain why uniform policy is hard to maintain without a blended approach.

Complete Report Scope:

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premise

- By Application

- Clinical Data Protection

- Medical Device and IoMT Security

- EHR and EMR Security

- Healthcare Cloud Workload Security

- Others

- By End User

- Healthcare Providers

- Pharmaceutical and Biotech Companies

- Healthcare Payers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 49.36% of the AI in healthcare zero-trust security market share in 2025, giving the region the largest installed base and the strongest near-term buying power. The United States leads that position because it combines high breach exposure with proposed HIPAA changes that make microsegmentation a required control rather than a flexible option. Healthcare data breach costs in the United States reached USD 10.93 million in 2024, which gave boards a clear financial case for stronger access control and containment. Canada and Mexico add to regional growth through healthcare digitization and hospital network expansion, even though their adoption pace remains below the United States. Through 2031, the AI in healthcare zero-trust security market should keep finding stable demand in North America because compliance deadlines, insurer pressure, and enterprise procurement are moving in the same direction.

Asia-Pacific is projected to grow at 23.27% CAGR through 2031, making it the fastest-growing regional pocket. The region is expanding because digital health programs in India, Japan, South Korea, China, and Australia are increasing the number of cloud-connected records, devices, and remote care workflows that need verified trust controls. This creates a large runway for the AI in healthcare zero-trust security market, especially where governments are building national health data infrastructure and providers are moving into more connected care models. Providers in the region are also balancing growth with data residency rules, which makes federated learning and edge security a practical fit. The growth profile is also supported by stricter data governance expectations, which make privacy-preserving analytics and edge-based security more relevant across APAC deployments.

Europe holds a significant position in the market, with Germany setting the strongest formal direction through its TI 2.0 zero-trust program. The United Kingdom, France, Italy, and Spain are also advancing along the same path as critical-sector cyber rules and health system modernization programs push security spending higher. The Middle East, Africa, and South America remain earlier-stage opportunities in the AI in healthcare zero-trust security market, with adoption led by GCC digital health programs while broader uptake is still held back by slower capital refresh cycles.

- Check Point Software Technologies

- Cisco Systems

- CrowdStrike Holdings

- Cynerio

- Fortinet

- Google LLC (Google Cloud Security)

- IBM

- Illumio

- Imperva

- Juniper Networks

- Medigate (Claroty)

- Microsoft

- Okta Inc.

- Palo Alto Networks

- Proofpoint Inc.

- SentinelOne

- Sophos Group PLC

- Trellix

- Trend Micro Inc.

- Zscaler Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Driven Micro-Segmentation Reduces Lateral Threat Movement

- 4.2.2 Rapid Cloud Adoption of Electronic Health Records (EHR)

- 4.2.3 Surge In Ransomware Targeting Connected Medical Devices

- 4.2.4 Regulatory Push for "Zero-Trust" in HIPAA and HITECH Updates

- 4.2.5 Integration of Federated Learning for Privacy-Preserving Analytics

- 4.2.6 Hospital-to-Home Tele-Monitoring Expansion Requiring Edge Trust

- 4.3 Market Restraints

- 4.3.1 Skills Gap in AI-Security DevSecOps Talent

- 4.3.2 Legacy On-Prem Devices Lacking Agent Support

- 4.3.3 High TCO of Continuous Verification Frameworks

- 4.3.4 Inter-Vendor Algorithmic Bias Risk in Patient-Data Models

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By Application

- 5.3.1 Clinical Data Protection

- 5.3.2 Medical Device and IoMT Security

- 5.3.3 EHR and EMR Security

- 5.3.4 Healthcare Cloud Workload Security

- 5.3.5 Others

- 5.4 By End User

- 5.4.1 Healthcare Providers

- 5.4.2 Pharmaceutical and Biotech Companies

- 5.4.3 Healthcare Payers

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Check Point Software Technologies

- 6.3.2 Cisco Systems

- 6.3.3 CrowdStrike Holdings

- 6.3.4 Cynerio

- 6.3.5 Fortinet

- 6.3.6 Google LLC (Google Cloud Security)

- 6.3.7 IBM

- 6.3.8 Illumio

- 6.3.9 Imperva

- 6.3.10 Juniper Networks

- 6.3.11 Medigate (Claroty)

- 6.3.12 Microsoft Corporation

- 6.3.13 Okta Inc.

- 6.3.14 Palo Alto Networks

- 6.3.15 Proofpoint Inc.

- 6.3.16 SentinelOne

- 6.3.17 Sophos Group PLC

- 6.3.18 Trellix

- 6.3.19 Trend Micro Inc.

- 6.3.20 Zscaler Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment