|

시장보고서

상품코드

2072739

헬스케어 AI 컨설팅 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Healthcare AI Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

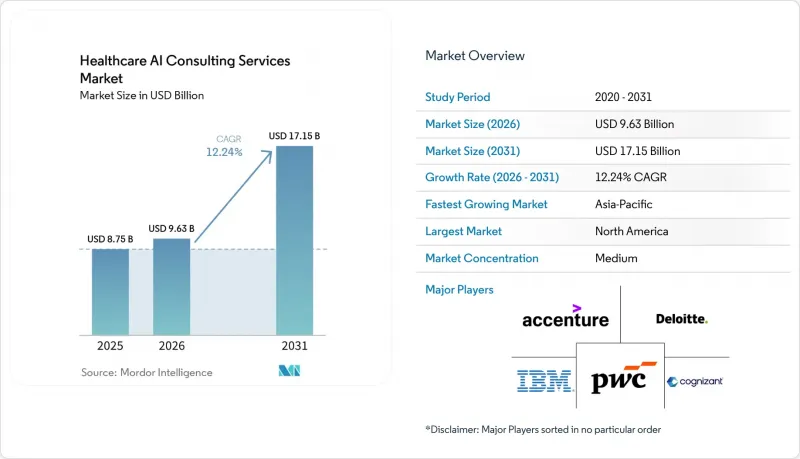

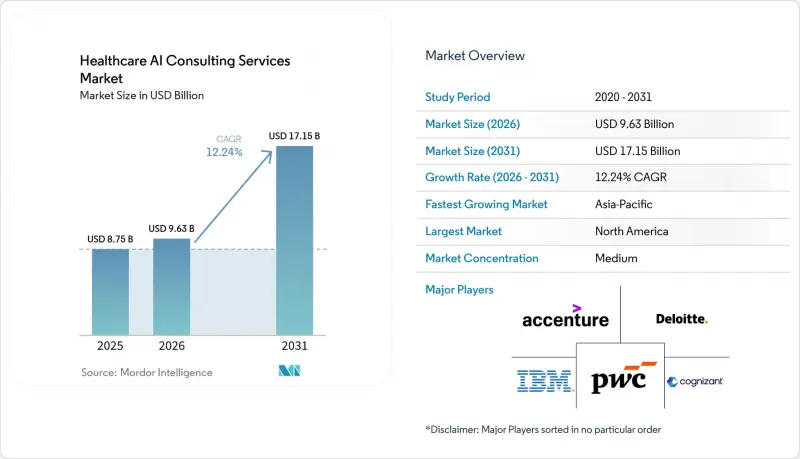

Mordor Intelligence에 의하면, 헬스케어 AI 컨설팅 서비스 시장은 2025년 87억 5,000만 달러로 평가되었고, 2026년에는 96억 3,000만 달러로 추정되고, 2031년까지 171억 5,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 12.24%로 성장할 전망입니다.

본 보고서는 서비스 유형별(전략 및 자문, 기타), 도입 모델별(온프레미스, 클라우드 기반, 하이브리드), 최종 사용자별(의료 제공업체, 기타), 용도별(임상 의사결정 지원, 기타) 및 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 헬스케어 AI 컨설팅 서비스 시장 동향 및 인사이트

AI를 활용한 임상 의사결정 지원 시스템의 도입 확대

병원과 의료 시스템은 제한적인 시범 운영에서 AI 기반 임상 의사결정 지원의 본격적인 운영으로 전환되고 있으며, 이러한 변화에 따라 헬스케어 AI 컨설팅 서비스 시장에서 설계, 검증, 통합, 최적화 업무에 대한 꾸준한 수요가 발생하고 있습니다. 2026년 1월 FDA가 재발행한 '임상 의사결정 지원 소프트웨어(CDS)'에 관한 지침에 따라, 의료기기에 해당하지 않는 CDS 기능과 규제 대상 소프트웨어 간의 경계가 명확해졌습니다. 이에 따라 미국에서는 시스템 설계 및 규정 준수 대응과 관련하여 외부 자문 및 지원의 필요성이 높아지고 있습니다. 또한, 해당 지침에서는 각 기능을 법정 기준에 비추어 신중하게 매핑함으로써 AI를 활용한 권장 사항을 보다 신속하게 도입할 여지도 남겨두고 있어, 이를 정확하게 수행할 수 있는 컨설팅 팀의 중요성이 커지고 있습니다. 조직은 모델의 출력을 임상 워크플로우, 에스컬레이션 규칙, 문서화 기준 및 감독 관리와 일치시키기 위한 지원도 필요로 하기 때문에 업무는 더 이상 모델 선정에만 국한되지 않습니다. 이에 따라 헬스케어 AI 컨설팅 서비스 시장의 범위는 단순한 도입에서 검증, 모니터링, 거버넌스 지원 등 보다 폭넓은 조합으로 확대되고 있습니다. 또한, 규제 용어를 의료 시스템이나 공급업체에 있어 실용적인 운영 규칙으로 전환할 수 있는 컨설턴트의 가치도 높아지고 있습니다.

의료비 부담 증가가 효율성을 중시하는 AI 컨설팅을 뒷받침하고 있습니다.

의료비 상승 압박으로 인해 헬스케어 AI 컨설팅 서비스 시장의 지출이 둔화되기는커녕, 오히려 AI 컨설팅 수요의 직접적인 원동력이 되고 있습니다. 의료 기관들은 현재, 장기간에 걸친 전략 중심의 프로젝트가 아니라, 측정 가능한 워크플로우 개선, 청구 처리 효율화, 직원의 업무 시간 단축으로 직접 이어지는 범위가 명확하게 정의된 프로그램을 원하고 있습니다. 이에 따라 관리 및 재무 업무 프로세스는 컨설팅 주도형 AI 도입에서 가장 신속하게 도입할 수 있는 분야 중 하나가 되었습니다. 왜냐하면, 많은 임상 이용 사례에 비해 모호한 부분이 적고, 리더가 사이클 타임, 재작업, 처리량 및 청구 거절 결과를 명확하게 추적할 수 있기 때문입니다. 2026년 5월에 출시된 Aetna의 2세대 'Claims Assist Manager'는 복잡한 보험 청구 처리 시간을 20% 이상 단축했습니다. 이는 보험사나 의료 제공 기관이 재현 가능한 이용 사례에 컨설팅 예산을 할당하고 있는 이유를 보여줍니다. 따라서 헬스케어 AI 컨설팅 서비스 시장에서는 단기간 내 도입, 워크플로우 재설계 및 효과 추적에 대한 지원에 대한 수요가 높아지고 있습니다. 수익 사이클 및 관련 백오피스 분야에서 신속한 실행력을 입증할 수 있는 기업은 보다 광범위한 기업 자산 전반에 걸친 추가 업무를 수주하는 데 있어 유리한 입장에 있습니다.

HIPAA/GDPR(EU 개인정보보호규정)에 따른 데이터 개인정보 보호 및 보안 관련 우려 사항

헬스케어 AI 컨설팅 서비스 시장에서 개인정보 보호 및 보안 문제는 수요를 완전히 중단시키지는 않지만, 주로 도입 일정을 연장함으로써 프로젝트 진행을 지연시키고 있습니다. 보호 대상인 건강 정보를 처리하는 AI 도구는 실제 운영 환경으로 이전하기 전에 위험 분석, 접근 제어 재검토, 워크플로우 문서화 및 계약상 관리 조치가 필요합니다. 이로 인해 이미 복잡한 의료 시스템 프로그램에 추가적인 순서 정리의 부담이 가중됩니다. 미국과 유럽 양쪽 관할권에서 사업을 영위하는 조직의 경우, 이러한 대응이 더욱 어렵습니다. 왜냐하면, 기반이 되는 법적 체계가 서로 다른 경우, 로그 기록, 문서화, 거버넌스 요건을 단일한 공통 프로세스로 다룰 수 없기 때문입니다. 그 결과, 각 프로젝트별 규정 준수 업무 부담은 점점 늘어나는 반면, 많은 구매자들이 광범위한 전개 예산을 승인하기 전에 요구하는 '실증 데이터'의 제시도 늦어지게 됩니다. 이로 인해 개별 컨설팅 프로젝트의 범위는 확대되겠지만, 헬스케어 AI 컨설팅 서비스 시장에는 단기적인 걸림돌이 되고 있습니다. 또한, 개인정보 보호 대책, 기술적 통제, 운영 모델 지원을 하나의 프로그램으로 통합함으로써 이러한 마찰을 줄일 수 있는 제공업체가 유리해집니다.

부문별 분석

2025년에는 구현 및 통합이 매출의 37.14%를 차지했는데, 이는 헬스케어 AI 컨설팅 서비스 시장이 초기 단계의 아이디어 창출보다는 실제 운영으로의 확대에 여전히 중점을 두고 있음을 보여줍니다. 의료 시스템에서는 컨설턴트를 활용하여 AI 모델을 현재 운영 중인 전자건강기록(EHR) 환경에 연결하고, 출력 결과를 기존의 임상 경로에 통합함으로써 IT 및 임상 거버넌스 요건을 모두 충족하는 모니터링 프로세스를 구축하고 있습니다. 이에 따라 구현 작업의 범위는 단순한 기술적 가동 개시에 그치지 않고, 워크플로우 재설계, 테스트, 운영 인계 등도 포함되므로 더욱 광범위해졌습니다. AI 모델의 개발 및 맞춤화는 가장 빠르게 성장하고 있는 서비스 유형으로, 2026-2031년 연평균 성장률(CAGR) 12.77%로 확대될 것으로 전망됩니다. 이러한 성장은 규제가 엄격한 의료 현장에서 지역별로 최적화된 모델에 대한 수요가 증가하고, 범용 모델의 동작에 의존할 수 없는 이용 사례에 대한 수요가 늘어나고 있음을 반영합니다.

헬스케어 AI 컨설팅 서비스 시장은 이 서비스 부문 내에서도 더욱 다층화되고 있습니다. '전략 및 자문', '데이터 거버넌스 컨설팅', '규제 및 컴플라이언스 컨설팅'의 각 분야는 시장 점유율은 작지만, 조직이 초기 도입 단계에서 관리, 최적화, 감사 대응 단계로 넘어감에 따라 지속적으로 의뢰 대상이 되고 있습니다. 즉, 도입 프로젝트는 모델이 가동된 시점에서 종료되는 것이 아니라, 거버넌스나 컴플라이언스 분야에서 후속 수요를 창출하는 경우가 많아지고 있습니다.

2025년에는 클라우드 기반 AI 솔루션이 매출의 55.46%를 차지했으며, 클라우드는 헬스케어 AI 컨설팅 서비스 시장의 주요 인프라 계층으로 자리매김하고 있습니다. 이러한 위상은 의료 제공업체, 보험사, 디지털 헬스 플랫폼 전반에 걸쳐 엔터프라이즈급 AI 워크로드 지원, 보다 광범위한 데이터 접근성, 그리고 더 신속한 도입 주기에 대한 수요가 증가하고 있음을 반영합니다. EHR 환경, 원격의료 시스템 및 데이터 집약형 워크로드의 조기 클라우드 전환을 통해, 기술적으로는 AI 도입 준비가 완료되었으나 실제 운영에는 여전히 외부 지원이 필요한 조직의 기반이 이미 형성되어 있습니다. 또한, 클라우드 기반 AI 솔루션은 가장 빠르게 성장하고 있는 도입 부문으로, 2031년까지 연평균 성장률(CAGR) 12.68%를 나타낼 것으로 전망됩니다. 이에 따라, 특히 오케스트레이션, 상호운용성, 모니터링, 보안을 통합적으로 다뤄야 하는 경우, 클라우드 컨설팅은 헬스케어 AI 컨설팅 서비스 시장의 다음 단계에서 핵심적인 역할을 담당하게 될 것입니다.

온프레미스형 AI 솔루션은 엄격한 데이터 보관 규정, 고도로 관리되는 네트워크 환경, 혹은 인프라를 직접 관리하고자 하는 조직 내의 요구에 직면해 있는 조직에서 여전히 중요한 역할을 수행하고 있습니다. 이는 기밀성이 높은 워크로드를 공유 호스팅 환경으로 쉽게 이전할 수 없는 상황에서 특히 해당됩니다. 많은 의료 시스템이 클라우드, 로컬 처리 및 용도별 환경에 걸친 유연성을 필요로 하기 때문에 하이브리드 솔루션이 현실적인 중간 대안으로 부상하고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 53.13%를 차지했으며, 헬스케어 AI 컨설팅 서비스 시장에서 최대 지역 블록으로서의 위상을 유지했습니다. 미국은 성숙한 디지털 인프라, 의료 시스템당 높은 컨설팅 지출, 그리고 규정 준수 업무와 명확한 구매 동기를 모두 제공하는 규제 환경을 통해 그 위상을 공고히 하고 있습니다. 2026년 5월, Aetna사가 2세대 'Claims Assist Manager'를 출시한 것과 AI를 활용한 보험사 업무의 지속적인 확대는 이 지역에서 이용 사례가 실제 컨설팅 수요로 어떻게 이어지고 있는지를 보여주고 있습니다. 캐나다와 멕시코도 공공 디지털 헬스 활동 및 상업 의료 현대화 프로그램을 통해 기여하고 있습니다. 캘리포니아주의 AB-2575 법안은 AI 기반 임상 의사결정 지원에 대한 구체적인 책임 규정을 도입하고 있으며, 이는 한 주에 국한되지 않고 규정 준수 계획에 영향을 미칠 가능성이 높기 때문에 더욱 중요한 요소로 대두되고 있습니다.

유럽은 독일, 영국, 프랑스를 필두로 헬스케어 AI 컨설팅 서비스 시장에서 여전히 2위의 규모를 자랑하고 있습니다. 독일의 환경은 디지털 헬스의 보험 급여 구조와 EU AI법의 실무적 해석에 의해 형성되어 있으며, BfArM은 2025년에 AI를 활용한 의료 제품이 관련 유럽 규범 하에서 어떻게 분류되어야 하는지에 대한 지침을 발표할 예정입니다. 프랑스 역시 국가 주도의 도입 규정과 국가 보건 데이터 전략의 우선 과제에 따라, 지역 실정에 맞는 아키텍처, 거버넌스 및 도입 지원에 대한 수요가 높아지고 있어 그 중요성이 커지고 있습니다. 영국, 이탈리아, 스페인은 여전히 활발한 도입 시장이며, 그 밖의 유럽 국가들도 보다 광범위한 디지털 헬스 프로그램을 통해 계속해서 성장세를 보이고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2026-2031년 연평균 성장률(CAGR) 13.92%로 확대될 것으로 예측되며, 헬스케어 AI 컨설팅 서비스 시장에서 가장 강력한 성장세를 보일 것으로 전망됩니다. 중국, 한국, 인도의 성장세는 균일하지 않습니다. 각 시장은 상환 정책, 디지털 헬스 인프라, 공공 프로그램의 설계와 같은 요소들이 서로 다르게 조합되어 형성되기 때문입니다. 한국에서는 2026년부터 국민건강보험을 통한 AI 암 검진이 의무화됨에 따라, 즉각적인 도입 및 규정 준수 조치가 필요합니다. 한편, 인도의 '국가 디지털 헬스 미션'은 대규모이며 다양한 의료 인프라 전반에 걸쳐 상호 운용 가능한 데이터 표준을 지속적으로 지원하고 있습니다. 중동 및 아프리카은 주로 GCC(걸프협력회의) 회원국들의 스마트 헬스 프로그램에 의해 주도되고 있으며, 남미에서는 브라질과 아르헨티나 등 국가를 필두로 한 민간 보험사들의 도입이 진행되고 있습니다. 이는 헬스케어 AI 컨설팅 서비스 시장이 지리적으로 확대되고 있음을 의미하지만, 컨설팅 수요 증가 속도는 여전히 정책 이행 상황, 공공 디지털 인프라, 그리고 현지 시스템 구축 현황에 크게 좌우되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the healthcare AI consulting services market is expected to increase from USD 8.75 billion in 2025 to USD 9.63 billion in 2026 and reach USD 17.15 billion by 2031, growing at a CAGR of 12.24% over 2026-2031.

This report is Segmented by Service Type (Strategy and Advisory, and Others), Deployment Model (On-Premise, Cloud-Based, and Hybrid), End User (Healthcare Providers, and Others), Application (Clinical Decision Support, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare AI Consulting Services Market Trends and Insights

Growing Adoption of AI-Driven Clinical Decision Support Systems

Hospitals and health systems are moving from limited pilots to live use of AI-driven clinical decision support, and that shift is creating steady demand for design, validation, integration, and optimization work in the healthcare AI consulting services market. The FDA's reissued Clinical Decision Support Software guidance in January 2026 sharpened the boundary between non-device CDS functions and regulated software, which increases the need for outside advisory support on system design and compliance mapping in the United States. That same guidance also leaves room for faster deployment of AI-assisted recommendations when each function is carefully mapped against the statutory criteria, so consulting teams that can do this precisely are gaining importance. The work is no longer limited to model selection, because organizations also need help aligning model outputs with clinical workflow, escalation rules, documentation standards, and oversight controls. This expands the scope of the healthcare AI consulting services market from implementation alone to a broader mix of validation, monitoring, and governance support. It also raises the value of consultants that can translate regulatory language into practical operating rules for health systems and software vendors.

Rising Healthcare-Cost Pressures Pushing Efficiency-Focused AI Consulting

Healthcare cost pressure is acting as a direct catalyst for AI consulting demand rather than slowing spending in the healthcare AI consulting services market. Health systems are now asking for tightly scoped programs tied to measurable workflow gains, claims efficiency, and staff time savings instead of longer strategy-heavy engagements. This has made administrative and financial workflows one of the fastest entry points for consulting-led AI deployment, because leaders can track cycle time, rework, throughput, and denial outcomes with less ambiguity than many clinical use cases. Aetna's second-generation Claims Assist Manager, launched in May 2026, reduced processing time for complex claims by more than 20%, which shows why payer and provider organizations are directing consulting budgets toward repeatable operational use cases.The healthcare AI consulting services market is therefore seeing stronger demand for short-cycle implementation, workflow redesign, and benefits tracking support. Firms that can prove rapid execution in revenue cycle and adjacent back-office areas are better positioned to win follow-on work across a broader enterprise estate.

Data-Privacy and Security Concerns Under HIPAA/GDPR

Privacy and security issues slow projects in the healthcare AI consulting services market mainly by extending deployment timelines instead of stopping demand outright. AI tools that process protected health information require risk analysis, access control review, workflow documentation, and contract controls before they move into production, which adds sequencing pressure to already complex health system programs. This is more difficult for organizations operating across both U.S. and European jurisdictions, because logging, documentation, and governance needs cannot be treated as one common process when the underlying legal frameworks differ. The result is a larger compliance workload per engagement, but it also delays the proof points that many buyers want before approving broader rollout budgets. This creates a short-term drag on the healthcare AI consulting services market even while it expands the scope of individual consulting assignments. It also favors providers that can reduce friction by combining privacy, technical controls, and operating model support in one program.

Other drivers and restraints analyzed in the detailed report include:

- Emerging Demand for Foundation-Model Fine-Tuning to Meet Data-Sovereignty Rules

- Increasing Regulatory Focus on Responsible AI Governance in Healthcare

- Shortage of AI-Skilled Healthcare Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Implementation and integration held 37.14% of revenue in 2025, which shows that the healthcare AI consulting services market is still centered on production deployment rather than early-stage ideation. Health systems are using consultants to connect AI models with live EHR environments, fit outputs into existing clinical pathways, and build monitoring processes that satisfy both IT and clinical governance needs. This makes implementation work larger in scope than simple technical activation, because it also includes workflow redesign, testing, and operational handoff. AI model development and customization is the fastest-growing service type and is projected to expand at a 12.77% CAGR from 2026 to 2031. That growth reflects rising demand for locally tuned models in regulated healthcare settings and for use cases that cannot rely on generic model behavior.

The healthcare AI consulting services market is also becoming more layered within this service split. Strategy and Advisory, Data and Governance Consulting, and Regulatory and Compliance Consulting hold smaller shares, but they are becoming recurring mandates as organizations move from first deployment to control, optimization, and audit readiness. This means implementation projects often create downstream demand for governance and compliance scopes rather than ending once a model is live.

Cloud-based AI solutions accounted for 55.46% of revenue in 2025, which makes cloud the leading infrastructure layer for the healthcare AI consulting services market. That position reflects the growing need to support enterprise-scale AI workloads, broader data access, and faster deployment cycles across providers, payers, and digital health platforms. Earlier cloud transitions in EHR environments, telehealth systems, and data-intensive workloads have already created a base of organizations that are technically ready for AI but still need outside help to operationalize it. Cloud-based AI solutions are also the fastest-growing deployment segment and are expected to be forecasted at 12.68% CAGR through 2031. This makes cloud consulting central to the next phase of the healthcare AI consulting services market, especially where orchestration, interoperability, monitoring, and security have to be handled together.

On-premise AI solutions still retain a meaningful role in organizations that face strict residency rules, highly controlled network environments, or internal preferences for direct infrastructure oversight. This is especially relevant in settings where sensitive workloads cannot be moved easily into shared hosted environments. Hybrid Solutions are therefore emerging as the practical middle path, because many health systems need flexibility across cloud, local processing, and application-specific environments.

Complete Report Scope:

- By Service Type

- Strategy and Advisory

- Implementation and Integration

- AI Model Development and Customization

- Data and Governance Consulting

- Regulatory and Compliance Consulting

- Others

- By Deployment Model

- On-Premise AI Solutions

- Cloud-Based AI Solutions

- Hybrid Solutions

- By End User

- Healthcare Providers

- Healthcare Payers

- Life Sciences and Pharma Companies

- MedTech and Device Companies

- Healthcare IT and Digital Health Companies (incl. startups)

- Government and Public Health Agencies

- By Application

- Clinical Decision Support and Diagnostics

- Medical Imaging

- Population Health and Predictive Analytics

- Drug Discovery and Development

- Administrative and Operational Optimization (incl. RCM)

- Others

- By Clinical Setting

- Inpatient

- Outpatient

- Emergency and Urgent Care

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 53.13% of global revenue in 2025, which kept it as the largest regional block in the healthcare AI consulting services market. The United States supports that position through mature digital infrastructure, high consulting spend per health system, and a regulatory environment that creates both compliance work and clearer buying triggers. The launch of Aetna's second-generation Claims Assist Manager in May 2026 and the continued scaling of AI-enabled payer operations show how operational use cases are translating into real consulting demand in the region. Canada and Mexico also contribute through public digital health activity and commercial healthcare modernization programs. California's AB-2575 adds another layer of importance because it introduces specific liability rules for AI-based clinical decision support and is likely to influence compliance planning beyond one state.

Europe remains the second-largest region in the healthcare AI consulting services market, led by Germany, the United Kingdom, and France. Germany's environment is shaped by digital health reimbursement structures and by practical interpretation of the EU AI Act, with BfArM publishing guidance in 2025 on how AI-based medical products should be classified under the relevant European frameworks. France is also becoming more important as sovereign deployment rules and national health data strategy priorities raise demand for localized architecture, governance, and implementation support. The United Kingdom, Italy, and Spain remain active adoption markets, while the rest of Europe continues to build momentum through broader digital health programs.

Asia-Pacific is the fastest-growing region and is anticipated to expand at a 13.92% CAGR from 2026 to 2031, which gives it the strongest growth profile in the healthcare AI consulting services market. Growth across China, South Korea, and India is not uniform, because each market is being shaped by different combinations of reimbursement policy, digital health infrastructure, and public program design. South Korea's 2026 mandate for AI cancer screening under national health insurance creates immediate implementation and compliance work, while India's National Digital Health Mission continues to support interoperable data standards across a large and diverse care base. Middle East and Africa is being driven mainly by GCC smart health programs, and South America is progressing through private insurer adoption led by countries such as Brazil and Argentina. This means the healthcare AI consulting services market is broadening geographically, but the pace of consulting demand still depends heavily on policy execution, public digital infrastructure, and local system readiness.

- Accenture

- Bain & Company

- Boston Consulting Group (BCG)

- Capgemini

- Cognizant

- Deloitte

- EY

- GE Healthcare Consulting

- HCLTech

- IBM

- Infosys

- IQVIA

- KPMG

- McKinsey & Company

- Optum Advisory

- Philips Healthcare Consulting

- PwC

- SAS Institute

- Siemens Healthineers Consulting

- Tata Consultancy Services (TCS)

- Wipro

- ZS Associates

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of AI-Driven Clinical Decision Support Systems

- 4.2.2 Rising Healthcare-Cost Pressures Pushing Efficiency-Focused AI Consulting

- 4.2.3 Increasing Cloud Migration of Healthcare IT Infrastructure

- 4.2.4 Shift Toward Outcome-Based Consulting Fee Models Enabling Risk-Sharing

- 4.2.5 Emerging Demand for Foundation-Model Fine-Tuning to Meet Data-Sovereignty Rules

- 4.2.6 Increasing Regulatory Focus on Responsible AI Governance in Healthcare

- 4.3 Market Restraints

- 4.3.1 Data-Privacy and Security Concerns Under HIPAA/GDPR

- 4.3.2 Shortage of AI-Skilled Healthcare Workforce

- 4.3.3 Vendor-Liability Uncertainty in AI-Caused Misdiagnosis Litigation

- 4.3.4 High Implementation and Integration Costs Across Legacy Healthcare Systems

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Strategy and Advisory

- 5.1.2 Implementation and Integration

- 5.1.3 AI Model Development and Customization

- 5.1.4 Data and Governance Consulting

- 5.1.5 Regulatory and Compliance Consulting

- 5.1.6 Others

- 5.2 By Deployment Model

- 5.2.1 On-Premise AI Solutions

- 5.2.2 Cloud-Based AI Solutions

- 5.2.3 Hybrid Solutions

- 5.3 By End User

- 5.3.1 Healthcare Providers

- 5.3.2 Healthcare Payers

- 5.3.3 Life Sciences and Pharma Companies

- 5.3.4 MedTech and Device Companies

- 5.3.5 Healthcare IT and Digital Health Companies (incl. startups)

- 5.3.6 Government and Public Health Agencies

- 5.4 By Application

- 5.4.1 Clinical Decision Support and Diagnostics

- 5.4.2 Medical Imaging

- 5.4.3 Population Health and Predictive Analytics

- 5.4.4 Drug Discovery and Development

- 5.4.5 Administrative and Operational Optimization (incl. RCM)

- 5.4.6 Others

- 5.5 By Clinical Setting

- 5.5.1 Inpatient

- 5.5.2 Outpatient

- 5.5.3 Emergency and Urgent Care

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Accenture

- 6.3.2 Bain & Company

- 6.3.3 Boston Consulting Group (BCG)

- 6.3.4 Capgemini

- 6.3.5 Cognizant

- 6.3.6 Deloitte

- 6.3.7 EY

- 6.3.8 GE Healthcare Consulting

- 6.3.9 HCLTech

- 6.3.10 IBM

- 6.3.11 Infosys

- 6.3.12 IQVIA

- 6.3.13 KPMG

- 6.3.14 McKinsey & Company

- 6.3.15 Optum Advisory

- 6.3.16 Philips Healthcare Consulting

- 6.3.17 PwC

- 6.3.18 SAS Institute

- 6.3.19 Siemens Healthineers Consulting

- 6.3.20 Tata Consultancy Services (TCS)

- 6.3.21 Wipro

- 6.3.22 ZS Associates

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment