|

시장보고서

상품코드

2072802

북미의 곤충 사료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America Insect Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

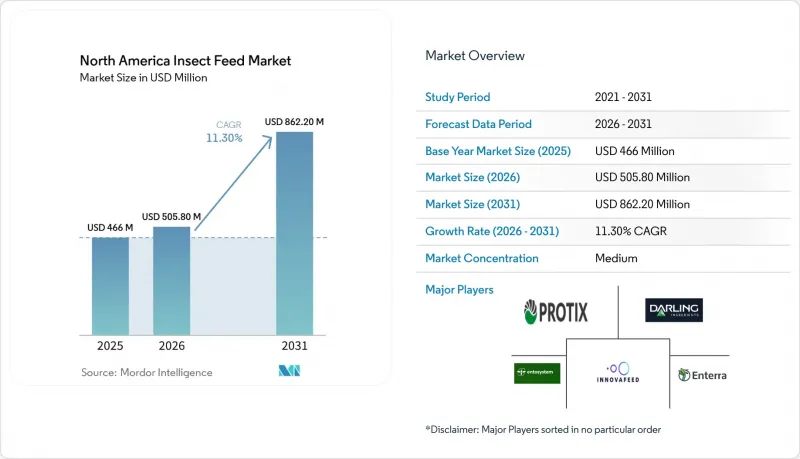

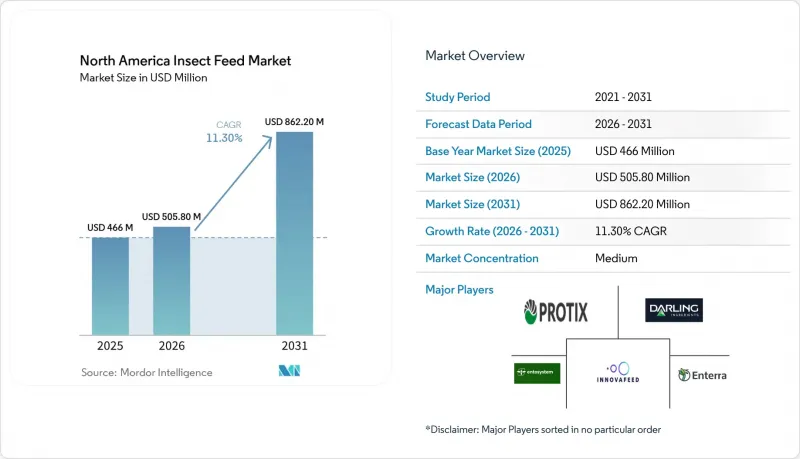

Mordor Intelligence에 의하면, 북미 곤충 사료 시장 규모는 2025년에 4억 6,600만 달러에 이르고, 2026년 5억 580만 달러에서 2031년까지 8억 6,220만 달러로 확대한다고 예측되고 있어 예측 기간(2026-2031년) CAGR은 11.3%를 나타낼 전망입니다.

본 보고서는 곤충의 유형(검은파리, 밀웜 등), 제품 형태(곤충 분말, 곤충유 등), 용도(수산물 양식, 가금류 등), 최종 사용자(상업용 사료 공장 등) 및 지역(미국, 캐나다, 멕시코 및 기타 북미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

북미 곤충 사료 시장 동향과 인사이트

AAFCO 및 CFIA의 승인을 통해 사료로서의 사용이 확대됨

규제 당국의 승인 절차 진전은 북미 곤충 사료 시장에서 여전히 운영상 가장 중요한 성장 요인으로 남아 있습니다. 미국 사료 관리관 협회(AAFCO)는 2024년 2월, 검은 군파리 유충(BSFL)에 관한 잠정 정의 T60.117을 승인하고, 연어과 어류, 가금류, 돼지 및 성체 반려동물용 사료에 이를 사용할 수 있도록 허가했습니다. 또한 2024년 1월에는 성견용 사료용 건조 밀웜 가루를 밀웜에 특화된 최초의 사료 정의로 승인했습니다. 이어 캐나다는 2024년 7월, ““2024년 사료 규정”이를 도입하여 국내 체계를 갱신하는 한편, 곤충 유래 원료 신청에 관한 등록 절차의 일부를 간소화했습니다. 각 승인은 상업용 사료 공장에서 새로운 배합 작업 단계를 만들어내기 때문에 도입은 단일 구매 결정이라기보다는 반복되는 조달 주기를 통해 이루어지는 경향이 있습니다. 이러한 추세는 북미 곤충 사료 시장의 꾸준한 수요 증가를 뒷받침하고 있습니다. 왜냐하면, 각종 제품 및 용도별 승인이 새로운 명확한 상업 경로를 개척하기 때문입니다. 2026년 4월에 제출된 캐나다의 법안 C-273은 이러한 추세에 또 다른 요소를 더하고 있습니다. 이는 이미 2개 이상의 관할 구역에서 승인된 원료에 대해 90일 이내의 잠정 등록을 허용하는 것으로, 이를 통해 상품화까지의 기간을 단축하고 캐나다의 규제적 입지를 강화할 가능성이 있기 때문입니다.

어분 및 대두박의 가격 변동이 대체 수요를 촉진

기존 사료용 단백질 원료의 가격 변동으로 인해, 북미의 곤충 사료 시장은 지난 몇 년에 비해 더욱 견고한 경제적 기반을 확보하고 있습니다. 2026년 3월 전 세계 어분 가격은 톤당 1,992달러에 달하고, 전년 대비 40.9% 상승했습니다. 한편, 대두박은 같은 시점에 톤당 312달러였습니다. 이러한 가격 차이는 중요한 의미를 지닙니다. 많은 배합 사료에서 곤충박이 대두박보다 여전히 가격이 비싸긴 하지만, 어분 가격 변동 위험에 노출된 구매자에게는 곤충박이 헤지 수단으로서 더 유용하기 때문입니다. FAO(유엔 식량농업기구) 보고서에 따르면, 페루에서는 엘니뇨 현상과 관련하여 멸치 어획 할당량이 축소되어 2023년 어획량이 28% 감소했습니다. 이는 기후 변화로 인한 스트레스 상황에서 해양 단백질공급이 얼마나 급속히 부족해질 수 있는지를 보여줍니다. 또한, 2026년 5월 미국 농무부(USDA) 시장 데이터에 따르면, 단백질 함량이 46.5-48%인 대두박은 미국 콘벨트 시장에서 1메트릭톤당 315-360달러에 거래되고 있으며, 가격 측면만 놓고 보면, 곤충박이 대두의 기준 가격을 따라잡기는 여전히 어렵습니다. 그 결과, 대규모 사료 구매업체들은 곤충 사료의 조달을 공급망 리스크 관리의 일환으로 간주하는 경향이 강해지고 있으며, 이는 어분에 대한 의존도가 높은 북미의 곤충 사료 시장에서 곤충 사료의 더 광범위한 채택을 촉진하고 있습니다.

기존 단백질 원료에 비해 곤충 분말의 가격 프리미엄

북미 곤충 사료 시장에서 가장 큰 상업적 제약 요인은 여전히 기존 단백질 원료에 비해 곤충 사료의 가격이 더 비싸다는 점입니다. 2026년 5월 미국 농무부(USDA)의 자료에 따르면, 대두박 가격은 1메트릭톤당 315-360달러로, 이는 상업적으로 생산된 곤충박의 원가보다 훨씬 낮은 수준이었습니다. 어분 가격의 급등으로 인해 수산 양식 분야에서 대체안의 타당성은 높아지고 있지만, 돼지나 가금류 사료 구매자들에게는 경제성이라는 관점만으로는 곤충 사료의 광범위한 도입을 정당화할 수 있을 정도의 가격 충격을 겪는 경우는 보통 없습니다. 곤충 생산의 비용 곡선은 규모 확대, 육종 발전, 자동화 및 배지 통합을 통해 점차 개선되고 있지만, 최근의 실패 사례에서도 알 수 있듯이 이러한 전환에는 여전히 막대한 비용이 소요되며, 그 진척 상황도 고르지 않은 것으로 나타났습니다. 달링 인그리디언츠는 2026년 2월, 주로 엔바이로플라이트 및 CTH의 천연 케이싱 사업과 관련된 5,800만 달러 규모의 사업 재편 비용 및 감손 손실을 계상했습니다. 이는 현재의 경제 상황이 어렵다는 점을 여실히 드러내는 것입니다. 더 많은 생산자들이 가격 조건이 유리한 시기에 다년 계약을 체결하기 전까지는 북미 곤충 사료 시장에서 범용 사료로의 확산은 제한적인 수준에 그칠 것으로 보입니다.

부문별 분석

2025년, 검은 군파리 유충(BSFL)은 북미 곤충 사료 시장에서 61.6%의 점유율을 차지하며, 북미 곤충 사료 시장에서 다른 모든 곤충 종을 압도적으로 앞질렀습니다. 이러한 지위는 광범위한 기질에 대한 범용성, 가장 폭넓은 규제 적용 범위, 그리고 경쟁 종 대부분보다 자동화 생산 시스템과의 호환성이 높다는 점에 의해 뒷받침되고 있습니다. AAFCO의 T60.117 승인을 통해 BSFL은 연어과 어류, 가금류, 돼지 및 성견용 반려동물사료에 사용될 수 있게 되었으며, 미국과 캐나다 양국에서 상업적 활용 범위가 확대되었습니다. 밀웜 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 17.0%를 기록하며 성장할 것으로 전망됩니다. 이는 2024년 1월 AAFCO가 성견용 사료에 대한 사용을 승인한 것이 뒷받침된 결과이며, 이를 통해 새로운 곤충 종들이 프리미엄 반려동물 시장에 진출할 수 있는 길이 열렸습니다.

BSFL은 또한 북미 곤충 사료 업계의 생산 체계가 성숙해진 데서 혜택을 보고 있으며, 이로 인해 구매자들은 공급의 지속성에 대해 더 큰 신뢰를 보이고 있습니다. 텍사스 A&M 대학교 아그리라이프는 2026년 1월에 특허를 취득한 "BSF 빌렛" 기술을 도입했습니다. 이 시스템을 통해 생산성이 20-30% 향상될 뿐만 아니라, 유충을 실온에서 수 주에서 수개월 동안 보관할 수 있게 됩니다. 밀웜에는 여전히 큰 가능성이 남아 있습니다. 그 가치 제안은 BSFL과는 달리, 대량 생산형 수산 양식보다는 프리미엄 반려동물사료 분야와의 연관성이 더 강하기 때문입니다. 귀뚜라미나 집파리는 규모는 작지만, 북미 곤충 사료 시장에서 친근감, 기호성, 혹은 종 특유의 활용 사례가 시범 사용을 촉진하는 상황에서는 여전히 중요한 위치를 차지하고 있습니다.

2025년, 북미 곤충 사료 시장 규모 중 곤충 분말이 57.6%를 차지했으며, 단백질 농축 사료는 북미 곤충 사료 시장에서 가장 큰 제품 형태로서의 위상을 유지했습니다. 이러한 우위는 규제상 입장이 명확하고, 기존의 사료 배합 시스템에 쉽게 적용할 수 있으며, 수산 양식 및 가축 사육 분야에서 확고한 근거가 있다는 점에 기인합니다. 또한, 구매자들은 메티오닌과 리신의 균형이 중요한 종별 사료 배합에서 곤충 분말의 아미노산 구성이 효과적으로 작용한다는 점 때문에 이 제품을 높이 평가했습니다. 곤충유는 2031년까지 연평균 성장률(CAGR)이 16.9%로 가장 빠르게 성장하고 있는 제품 형태이며, 라우린산을 풍부하게 함유하고 있어 현재는 단순한 칼로리 대체재 이상의 용도로 활용되고 있는 BSFL(검은 군파리) 유래 지질에 대한 관심에 힘입어 성장하고 있습니다.

건조 곤충 통제품은 시각적인 단순성과 직접 급여가 중시되는 소규모이지만 눈에 띄는 소매 및 전문 유통 채널에서 여전히 사용되고 있으며, 특히 가정 내 양계 및 일부 반려동물사료 분야에서 중요한 역할을 하고 있습니다. "기타" 범주에는 분변과 퓌레가 포함되어 있으며, 시설이 여러 생산물을 취급하는 운영 모델로 전환됨에 따라 이 두 가지 모두의 상업적 중요성이 높아지고 있습니다. Entosystem사의 드럼몬드빌 공장과 Innovafeed사의 디케이터 공장의 설계 사례는 생산자들이 단일 생산품뿐만 아니라 단백질, 유지, 토양 개량제를 중심으로 공장을 구축하고 있음을 보여줍니다. 이러한 변화는 중요한 의미를 지닙니다. 왜냐하면 북미 곤충 사료 업계에서는 공장 차원의 수익성 기반으로서 단순히 사료 분말의 생산량뿐만 아니라 제품 형태의 다양화가 점점 더 중요시되고 있기 때문입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 동향

JHSAccording to Mordor Intelligence, the north america insect feed market size reached USD 466.0 million in 2025 and is projected to expand from USD 505.8 million in 2026 to USD 862.2 million by 2031, registering a CAGR of 11.3% during the forecast period (2026 - 2031).

This report is Segmented by Insect Type (Black Soldier Fly, Mealworm, and More), by Product Form (Insect Meal, Insect Oil, and More), by Application (Aquaculture, Poultry, and More), by End User (Commercial Feed Mills, and More), and by Geography (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

North America Insect Feed Market Trends and Insights

AAFCO and CFIA Approvals Expanding Permitted Feed Use

The pace of regulatory approvals remains the most operationally important growth driver in the North America insect feed market. Association of American Feed Control Officials (AAFCO) approved Black Soldier Fly Larvae (BSFL) tentative definition T60.117 in February 2024, which permitted use in salmonid, poultry, swine, and adult companion-animal food, and it also approved dried mealworm meal for adult dog food in January 2024 as the first mealworm-specific feed definition. Canada then introduced the Feeds Regulations 2024 in July 2024, which updated the national framework and simplified parts of the registration process for insect ingredient submissions. Each approval creates a new round of formulation work at commercial feed mills, so adoption tends to happen through repeat procurement cycles rather than a single purchasing decision. That pattern supports steady demand building in the North America insect feed market because each species and application approval opens another defined commercial lane. Canada's Bill C-273, introduced in April 2026, adds another layer to this theme because provisional registration within 90 days for ingredients already approved in 2 or more jurisdictions could shorten commercialization timelines and strengthen Canada's regulatory position.

Fishmeal and Soybean Meal Volatility Supporting Substitution

Price volatility in conventional feed proteins is giving the North America insect feed market a stronger economic footing than it had in earlier years. Global fishmeal prices reached USD 1,992 per metric ton in March 2026, up 40.9% year on year, while soybean meal stood at USD 312 per metric ton at the same point. This gap matters because it makes insect meal more relevant as a hedge for buyers exposed to fishmeal swings, even if insect meal still carries a premium to soy in many rations. FAO documented how El Nino-related anchovy quota reductions in Peru cut catches by 28% in 2023, which showed how quickly marine protein supply can tighten under climate stress. USDA market data from May 2026 also showed soybean meal at 46.5-48% protein trading at USD 315-360 per metric ton in U.S. corn-belt markets, so the soy benchmark remains difficult for insect meal to match on price alone. As a result, larger feed buyers are increasingly treating insect meal allocations as part of supply-chain risk management, which supports broader adoption in the North America insect feed market where fishmeal exposure is high.

Insect Meal Pricing Premium Versus Conventional Proteins

The largest commercial restraint in the North America insect feed market is still the pricing premium of insect meal against conventional proteins. USDA data from May 2026 showed soybean meal at USD 315-360 per metric ton, which stayed well below the cost of commercially produced insect meal. Fishmeal inflation has improved the substitution case in aquaculture, but swine and poultry buyers usually do not face a comparable price shock that would justify broad insect meal inclusion on economics alone. The cost curve for insect production is improving through scale, breeding advances, automation, and substrate integration, but recent setbacks show that this transition remains expensive and uneven. Darling Ingredients reported USD 58.0 million in restructuring and impairment charges in February 2026 related primarily to EnviroFlight and CTH natural casing businesses, which highlighted the pressure on current economics. Until more producers lock in multi-year contracts during favorable pricing windows, the North America insect feed market will continue to face limited penetration in commodity-grade rations.

Other drivers and restraints analyzed in the detailed report include:

- Aquaculture Feed Formulators Seeking Domestic Fishmeal Alternatives

- Premium Pet Food Demand for Hypoallergenic Proteins

- Capital Scarcity for Large Automated Facilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Black soldier fly larvae held 61.6% of North America insect feed market share in 2025, which kept BSFL clearly ahead of all other insect types in the North America insect feed market. Its position is supported by broad substrate versatility, the widest regulatory coverage, and stronger fit with automated production systems than most competing species. AAFCO's T60.117 approval gave BSFL access to salmonid, poultry, swine, and adult companion-animal uses, which widened its commercial reach in both the United States and Canada. Mealworms are forecast to grow at a 17.0% CAGR from 2026 to 2031, helped by AAFCO's January 2024 approval for adult dog food, which opened a premium companion-animal route for a new insect species.

BSFL also benefits from a more mature production profile in the North America insect feed industry, which gives buyers greater confidence in continuity of supply. Texas A&M AgriLife introduced the patented BSF Billet technology in January 2026, and the system points to 20-30% productivity gains along with room-temperature larval storage for weeks to months. Mealworms still have a meaningful opening because their value proposition is different from BSFL and more closely tied to premium pet nutrition than to bulk aquaculture volume. Crickets and houseflies remain smaller in scale, but they retain relevance where familiarity, palatability, or species-specific use cases support trial activity in the North America insect feed market.

Insect meal accounted for 57.6% of the North America insect feed market size in 2025, which kept protein concentrate as the largest product form in the North America insect feed market. This lead reflects its clearer regulatory standing, easier fit with existing feed formulation systems, and stronger evidence base across aquaculture and livestock uses. Buyers also value insect meal because its amino acid profile can work well in species-specific formulas where methionine and lysine balance matter. Insect oil is the fastest-growing product form with a 16.9% CAGR through 2031, supported by interest in BSFL lipids that are rich in lauric acid and are now being used for more than simple caloric substitution.

Whole dried insects still serve smaller but visible retail and specialty channels where visual simplicity and direct feeding matter, especially in backyard poultry and some companion-animal formats. The others category includes frass and puree, and both are becoming more commercially relevant as facilities move toward multi-output operating models. Entosystem's Drummondville site and Innovafeed's Decatur design both show that producers are structuring plants around protein, oil, and soil amendment rather than one output alone. That shift matters because the North America insect feed industry is increasingly rewarding product-form diversification, not just meal volume, as the basis for plant-level profitability.

Complete Report Scope:

- By Insect Type

- Black Soldier Fly

- Mealworms

- Houseflies

- Crickets

- Others

- By Product Form

- Insect Meal

- Insect Oil

- Whole Dried Insects

- Others

- By Application

- Aquaculture

- Poultry

- Swine

- Pet Food

- Other Animal Feed

- By End User

- Commercial Feed Mills

- Integrated Livestock Producers

- Aquaculture Farms and Hatcheries

- Pet Food Manufacturers and Others

- By Geography

- United States

- Canada

- Mexico

- Rest of North America

List of Companies Covered in this Report:

- EnviroFlight (Darling Ingredients Inc.)

- Enterra Feed Corporation

- Innovafeed SAS

- Protix B.V.

- Entosystem Inc.

- Oreka Solutions Inc.

- Oberland Agriscience Inc.

- Chapul Farms

- Amera Biotech

- BSFL Solutions Inc.

- Unique Biotech Inc.

- NutraFed, LLC

- Grubbly Farms

- Fluker's Cricket Farm, Inc.

- Nellie's Black Soldier Fly Larvae

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AAFCO and CFIA approvals expanding permitted feed use

- 4.2.2 Fishmeal and soybean meal volatility supporting substitution

- 4.2.3 Aquaculture feed formulators seeking domestic fishmeal alternatives

- 4.2.4 Premium pet food demand for hypoallergenic proteins

- 4.2.5 Co-location with food and corn-processing side streams improving unit economics

- 4.2.6 Frass monetization improving full-plant returns

- 4.3 Market Restraints

- 4.3.1 Insect meal pricing premium versus conventional proteins

- 4.3.2 Species and life-stage approval limits capping addressable demand

- 4.3.3 Preconsumer substrate restrictions and depackaging bottlenecks

- 4.3.4 Capital scarcity for large automated facilities

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Insect Type

- 5.1.1 Black Soldier Fly

- 5.1.2 Mealworms

- 5.1.3 Houseflies

- 5.1.4 Crickets

- 5.1.5 Others

- 5.2 By Product Form

- 5.2.1 Insect Meal

- 5.2.2 Insect Oil

- 5.2.3 Whole Dried Insects

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 Aquaculture

- 5.3.2 Poultry

- 5.3.3 Swine

- 5.3.4 Pet Food

- 5.3.5 Other Animal Feed

- 5.4 By End User

- 5.4.1 Commercial Feed Mills

- 5.4.2 Integrated Livestock Producers

- 5.4.3 Aquaculture Farms and Hatcheries

- 5.4.4 Pet Food Manufacturers and Others

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

- 5.5.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 EnviroFlight (Darling Ingredients Inc.)

- 6.4.2 Enterra Feed Corporation

- 6.4.3 Innovafeed SAS

- 6.4.4 Protix B.V.

- 6.4.5 Entosystem Inc.

- 6.4.6 Oreka Solutions Inc.

- 6.4.7 Oberland Agriscience Inc.

- 6.4.8 Chapul Farms

- 6.4.9 Amera Biotech

- 6.4.10 BSFL Solutions Inc.

- 6.4.11 Unique Biotech Inc.

- 6.4.12 NutraFed, LLC

- 6.4.13 Grubbly Farms

- 6.4.14 Fluker's Cricket Farm, Inc.

- 6.4.15 Nellie's Black Soldier Fly Larvae