|

시장보고서

상품코드

2072817

농업용 포깅 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Agricultural Fogging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

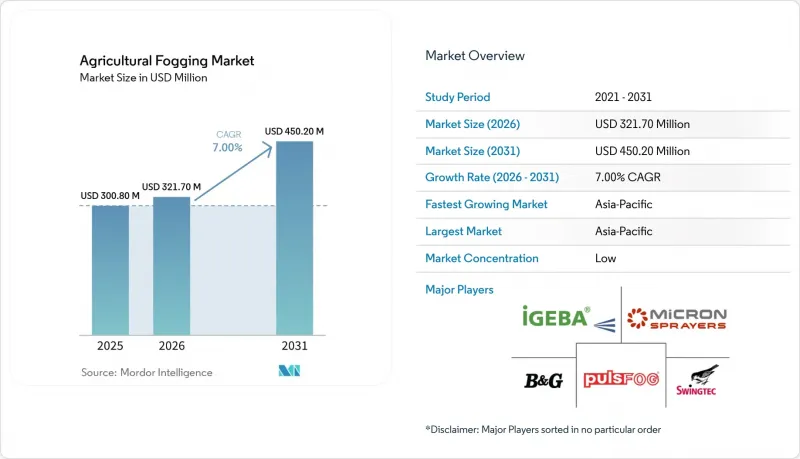

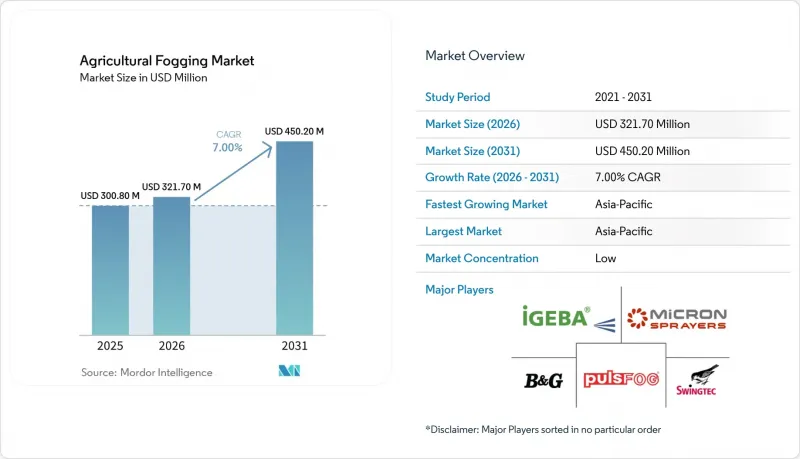

Mordor Intelligence에 의하면, 농업용 포깅 시장 규모는 2025년에 3억 80만 달러로 평가되었고 2026년 3억 2,170만 달러에서 2031년까지 4억 5,020만 달러로 성장하여 2026년부터 2031년까지 예측 기간에서 CAGR 7.0%를 나타낼 전망입니다.

본 보고서는 기계의 유형(열식 분무기 등), 동력원(연료식, 유선식, 배터리식), 용도(작물 보호·병해 관리, 온실·모종 재배장의 위생 관리 등) 및 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 농업용 포깅 시장 동향 및 인사이트

정밀한 해충 및 병해 방제에 대한 수요

농업용 포깅 시장은 베리류, 보호재배 채소, 감귤류, 관상용 식물 등의 작물에서 분무의 피복 품질이 처리 효과에 큰 영향을 미치기 때문에 정밀한 해충 및 병해 방제에 대한 수요가 높아지면서 성장세를 보이고 있습니다. Centre for Agriculture and Bioscience International(CABI)의 학술지 『Agriculture and Bioscience』에 2024년에 게재된 연구에 따르면, 동일한 운전 조건 하에서 정전기 분무 방식에서는 잎의 겉면에 327 데포짓/cm²의 부착량이 관찰된 반면, 기존 분무 시스템에서는 102 데포지트/cm²에 그친 것으로 밝혀졌습니다. 이러한 높은 부착 효율 덕분에, 생산자들이 통합 해충 관리 프로그램에서 수관 침투성 향상, 약제 낭비 감소, 그리고 보다 일관된 살포 성능 달성을 목표로 함에 따라, 정전기 분무 시스템 및 콜드 포깅 시스템의 도입이 확대되고 있습니다.

온실 및 보호재배의 확대

보호 재배는 농업용 포깅 시장의 주요 시장 성장 촉진요인으로 작용하고 있습니다. 이는 온실 재배에서 각 생육 주기 동안 정기적인 위생 관리, 작물 처리 및 환경 제어가 필요하기 때문입니다. 『International Journal of Research in Agronomy』지에 게재된 2025년 리뷰에 따르면, 중국은 보호재배 면적에서 1위를 차지했으며, 2024년에는 276만 헥타르에 달했습니다. 온실 인프라의 확장에 따라 작물 보호, 습도 관리, 병해 방제에 사용되는 분무 시스템에 대한 수요가 크게 증가하고 있습니다. 온실 분야에 특화된 탄탄한 제품 포트폴리오를 보유한 공급업체들은 보호재배의 확대와 상업 원예 사업에서 생산 주기의 빈도 증가로 인한 혜택을 누리고 있습니다.

업무용 시스템의 높은 초기 비용과 유지비

높은 초기 비용과 유지 관리비는 농업용 포깅 시장의 도입에 있어 여전히 큰 장벽으로 작용하고 있으며, 특히 재정적 제약을 겪고 있는 중소규모 농업 경영체에게는 큰 과제가 되고 있습니다. 미국 농무부 경제조업체국에 따르면, 농업 부문의 총 생산 비용은 2025년 4,731억 달러에서 2026년에는 4,777억 달러로 증가할 것으로 전망됩니다. 운영 비용 증가로 인해, 연료, 유지보수, 예비 부품 및 화학 물질 취급 인프라에 대한 추가 지출이 필요한 첨단 분무 시스템에 대한 투자 여력이 생산자들에게 제한되고 있습니다. 그 결과, 비용에 민감한 농업 경영에서는 장비의 교체 주기가 길어지고 있습니다.

부문별 분석

2025년, 농업용 포깅 시장에서 열식 분무기의 점유율이 38.5%로 가장 높았습니다. 이러한 시스템은 노지 작물의 병해충 방제, 축사 및 저장 시설의 위생 관리, 그리고 고밀도 안개의 침투와 광범위한 커버리지가 요구되는 대규모 농업 처리 분야에서 널리 활용되고 있어 꾸준한 수요를 유지하고 있습니다. 확립된 공급망, 운영자의 숙련도, 비교적 낮은 설비 비용 등의 요인이 특히 농업이 발전 단계에 있는 국가들에서의 도입을 촉진하고 있습니다. 연료식 열분무 시스템은 기동성과 처리 속도가 중요한 실외 또는 대량 처리 용도에 특히 적합합니다. 이 분야는 기존 농업에서 해충 및 병해 관리에 널리 활용되어 온 덕분에 계속해서 그 혜택을 누리고 있습니다.

농업용 포깅 시장에서 저온 분무기 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 8.1%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 이러한 시스템은 수성 제제나 생물 유래 작물 보호 제품과의 호환성이 뛰어나고, 액적 살포를 제어할 수 있다는 장점 덕분에 특히 온실 및 원예 분야에서 도입이 확대되고 있습니다. 생산자들은 저온 분무기가 정확한 부착을 보장하고, 화학 약품의 낭비를 최소화하며, 잔류물을 효과적으로 관리할 수 있다는 점을 높이 평가했습니다. 또한, 정전기 분무 기술은 수관으로의 침투성과 살포의 일관성을 높임으로써 정밀 재배 환경에서의 도입을 촉진하고 있습니다. 지속 가능한 작물 보호 프로그램으로의 전환과 생물 유래 자재와의 호환성에 대한 수요가 증가함에 따라, 상업 농업 분야에서 첨단 저온 분무 장치에 대한 수요가 계속해서 증가하고 있습니다.

지역별 분석

아시아태평양은 2025년 농업용 포깅 시장 점유율의 42.3%를 차지하고, 2026년부터 2031년까지 연평균 성장률(CAGR) 7.5%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 중국, 인도, 동남아시아 전역에서 온실 확대와 기계화된 작물 보호 기술이 급속히 확산되고 있어, 해당 지역은 계속해서 수요를 주도하고 있습니다. 온실 기반이 확대됨에 따라, 상업 원예 사업 전반에 걸쳐 작물 보호, 위생 관리, 환경 관리에 사용되는 농업용 포깅 시스템에 대한 수요가 증가하고 있습니다.

북미와 유럽은 농업용 살포 시스템 분야에서 여전히 기술적으로 선진적인 지역이며, 생산자들은 정밀 살포와 잔류물 관리를 점점 더 중요하게 여기고 있습니다. 이 지역의 상업용 온실 운영자와 특산 작물 생산자들은 제어된 액적 살포 및 생물학적 제제와의 호환성을 지원하는 첨단 분무 시스템을 지속적으로 도입하고 있습니다. 또한, 이러한 지역에서는 농약 살포 방법 및 근로자 안전 요건에 대한 규제 감독이 강화되고 있으며, 조작 제어 기능이 개선된 교정 완료된 분무 기술의 사용이 장려되고 있습니다.

유럽은 온실 재배의 지속적인 확대와 상업 원예 분야에서의 생물학적 작물 보호 기술 도입에 힘입어 농업용 포깅 시스템의 주요 성장 지역으로 부상하고 있습니다. 네덜란드 통계청에 따르면, 2024년에는 네덜란드 온실 재배 면적의 94.4%에서 생물학적 해충 방제제가 사용되었습니다. 생물학적 작물 보호에 대한 의존도가 높아짐에 따라, 온실 채소, 화훼 재배, 모종 재배 시스템에서 액적 살포를 제어하고 균일한 처리 범위를 실현하는 정밀 분무 시스템에 대한 수요가 증가하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the agricultural fogging market size was valued at USD 300.80 million in 2025 and is projected to grow from USD 321.70 million in 2026 to USD 450.20 million by 2031, registering a CAGR of 7.0% during the forecast period from 2026 to 2031.

This report is Segmented by Machine Type (Thermal Fogging Machines and More), by Power Source (Fuel-Powered, Electric Corded, and Battery-Powered), by Application (Crop Protection and Disease Management, Greenhouse and Nursery Sanitation, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Agricultural Fogging Market Trends and Insights

Precision Pest and Disease Control Demand

The agricultural fogging market is experiencing growth due to the rising demand for precision pest and disease control in crops such as berries, protected vegetables, citrus, and ornamental plants, where the quality of spray coverage significantly impacts treatment effectiveness. A 2024 study published in the Centre for Agriculture and Bioscience International (CABI) Agriculture and Bioscience journal highlighted that electrostatic spraying achieved 327 deposits/cm2 on adaxial leaf surfaces, compared to 102 deposits/cm2 with conventional spraying systems under identical operating conditions. This higher deposition efficiency is driving the adoption of electrostatic and cold fogging systems, as growers aim for improved canopy penetration, reduced chemical wastage, and more consistent application performance within integrated pest management programs.

Expansion of Greenhouse and Protected Cultivation

Protected cultivation is a key driver for the agricultural fogging market, as greenhouse production necessitates regular sanitation, crop treatment, and environmental control during each growing cycle. According to a 2025 review published in the International Journal of Research in Agronomy, China led the protected cultivation area, reaching 2.76 million hectares in 2024. The expansion of greenhouse infrastructure has significantly increased the demand for fogging systems used in crop protection, humidity management, and disease control. Suppliers with robust greenhouse-focused product portfolios are benefiting from the growing intensity of protected cultivation and the rising frequency of production cycles in commercial horticulture operations.

High Upfront and Maintenance Costs for Professional Systems

High upfront and maintenance costs remain a significant barrier to adoption in the agricultural fogging market, particularly for small- and medium-scale farming operations facing financial constraints. According to the United States Department of Agriculture Economic Research Service, total farm sector production expenses are projected to rise from USD 473.1 billion in 2025 to USD 477.7 billion in 2026. Increasing operating costs are limiting growers' capacity to invest in advanced fogging systems, which require additional expenditures on fuel, maintenance, spare parts, and chemical handling infrastructure. Consequently, equipment replacement cycles are slower in cost-sensitive agricultural operations.

Other drivers and restraints analyzed in the detailed report include:

- Mechanization to Offset Farm Labor Shortages

- Need to Reduce Chemical Volume and Improve Coverage Consistency

- Tightening Pesticide-Use and Residue Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The agricultural fogging market share for thermal fogging machines held the largest 38.5% in 2025. These systems maintain strong demand due to their extensive use in open-field crop protection, livestock buildings, storage sanitation, and large-scale agricultural treatments requiring dense fog penetration and broad-area coverage. Factors such as an established supply chain, operator familiarity, and relatively lower equipment costs support their adoption, particularly in developing agricultural economies. Fuel-based thermal systems are especially suitable for outdoor and high-throughput applications where mobility and treatment speed are critical. This category continues to benefit from its widespread application in conventional agricultural pest and disease management practices.

The agricultural fogging market size for cold fogging machines is projected to advance at the fastest 8.1% CAGR from 2026 to 2031. These systems are increasingly adopted due to their compatibility with water-based formulations, biological crop protection products, and controlled droplet application, particularly in greenhouse and horticulture operations. Growers favor cold fogging machines for their ability to ensure precise deposition, minimize chemical wastage, and manage residues effectively. Additionally, electrostatic fogging technologies are driving adoption in precise cultivation environments by enhancing canopy penetration and application consistency. The shift toward sustainable crop protection programs and the need for biological-input compatibility continue to drive demand for advanced cold fogging equipment in commercial agriculture.

Complete Report Scope:

- By Machine Type

- Thermal Fogging Machines

- Cold Fogging Machines

- Electrostatic Fogging Machines

- By Power Source

- Fuel-powered

- Electric corded

- Battery-powered

- By Application

- Crop Protection and Disease Management

- Greenhouse and Nursery Sanitation

- Storage and Post-harvest Protection

- Livestock and Poultry House Hygiene

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- France

- Italy

- Spain

- United Kingdom

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- Thailand

- Rest of Asia-Pacific

- Middle East

- Turkey

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Morocco

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific accounted for the largest 42.3% of the agricultural fogging market share in 2025 and is projected to grow at the fastest CAGR of 7.5% from 2026 to 2031. The region continues to lead demand because greenhouse expansion and mechanized crop protection practices are increasing rapidly across China, India, and Southeast Asia. The expanding greenhouse base is strengthening demand for agricultural fogging systems used in crop protection, sanitation, and environmental management across commercial horticulture operations.

North America and Europe continue to represent technologically advanced regions for agricultural fogging systems, where growers increasingly prioritize precision application and residue management. Commercial greenhouse operators and specialty crop growers across these regions continue adopting advanced fogging systems capable of supporting controlled droplet application and biological-input compatibility. The regions also benefit from stronger regulatory oversight related to pesticide application practices and worker-safety requirements, encouraging use of calibrated fogging technologies with improved operational control.

Europe is a key growth region for agricultural fogging systems due to the ongoing expansion of greenhouse cultivation and the adoption of biological crop protection in commercial horticulture. According to Statistics Netherlands, biological pest control agents were utilized in 94.4% of the greenhouse-cultivated area in the Netherlands in 2024. The growing reliance on biological crop protection is driving demand for precision fogging systems that enable controlled droplet application and uniform treatment coverage across greenhouse vegetables, floriculture, and nursery cultivation systems.

- IGEBA Geratebau GmbH

- B&G Equipment Company, Inc. (Pelsis Group)

- pulsFOG Dr. Stahl & Sohn GmbH

- Swingtec GmbH

- Micron Sprayers Limited (Goizper Group)

- VectorFog Electronic Corporation

- Martignani S.r.l.

- TIFONE S.r.l.

- Shouguang Jiafu Agricultural Machinery Co., Ltd.

- UNA Corporation

- HARDI INTERNATIONAL A/S

- Vectorfog (Vectornate Inc.)

- Shenzhen Longray Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision pest and disease control demand

- 4.2.2 Expansion of greenhouse and protected cultivation

- 4.2.3 Mechanization to offset farm labor shortages

- 4.2.4 Need to reduce chemical volume and improve coverage consistency

- 4.2.5 Re-entry interval and worker-exposure compliance favor remote and automated fogging

- 4.2.6 Rising adoption of biopesticides and water-based formulations in high-value horticulture

- 4.3 Market Restraints

- 4.3.1 High upfront and maintenance costs for professional systems

- 4.3.2 Tightening pesticide-use and residue compliance

- 4.3.3 Heat and formulation incompatibility limits some active ingredients in thermal systems

- 4.3.4 Greenhouse sealing, ventilation, and droplet-calibration demands raise failure risk for smaller growers

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Machine Type

- 5.1.1 Thermal Fogging Machines

- 5.1.2 Cold Fogging Machines

- 5.1.3 Electrostatic Fogging Machines

- 5.2 By Power Source

- 5.2.1 Fuel-powered

- 5.2.2 Electric corded

- 5.2.3 Battery-powered

- 5.3 By Application

- 5.3.1 Crop Protection and Disease Management

- 5.3.2 Greenhouse and Nursery Sanitation

- 5.3.3 Storage and Post-harvest Protection

- 5.3.4 Livestock and Poultry House Hygiene

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 Italy

- 5.4.3.4 Spain

- 5.4.3.5 United Kingdom

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 Indonesia

- 5.4.4.6 Thailand

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Turkey

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Morocco

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 IGEBA Geratebau GmbH

- 6.4.2 B&G Equipment Company, Inc. (Pelsis Group)

- 6.4.3 pulsFOG Dr. Stahl & Sohn GmbH

- 6.4.4 Swingtec GmbH

- 6.4.5 Micron Sprayers Limited (Goizper Group)

- 6.4.6 VectorFog Electronic Corporation

- 6.4.7 Martignani S.r.l.

- 6.4.8 TIFONE S.r.l.

- 6.4.9 Shouguang Jiafu Agricultural Machinery Co., Ltd.

- 6.4.10 UNA Corporation

- 6.4.11 HARDI INTERNATIONAL A/S

- 6.4.12 Vectorfog (Vectornate Inc.)

- 6.4.13 Shenzhen Longray Technology Co., Ltd.